Micro

1/90

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

91 Terms

What is the relationship between economic and accounting profit

Economic profit is always smaller because they take opportunity costs into account

How should a farmer in a perfectly competitive market maximize profit

By producing quantity where marginal cost is equal to the market place

Which of the following does NOT increase the elasticity of demand

Many loyal customers

What is the primary way that monopolist affect welfare in their markets

Monopolists reduce total welfare because they reduce quantity of production compared to production in a perfectly competitive market

Markets organize economic activity primarily through

prices

Which of the following markets is the closest to a perfectly competitive market?

the market for soybeans grown by farmers across the U.S

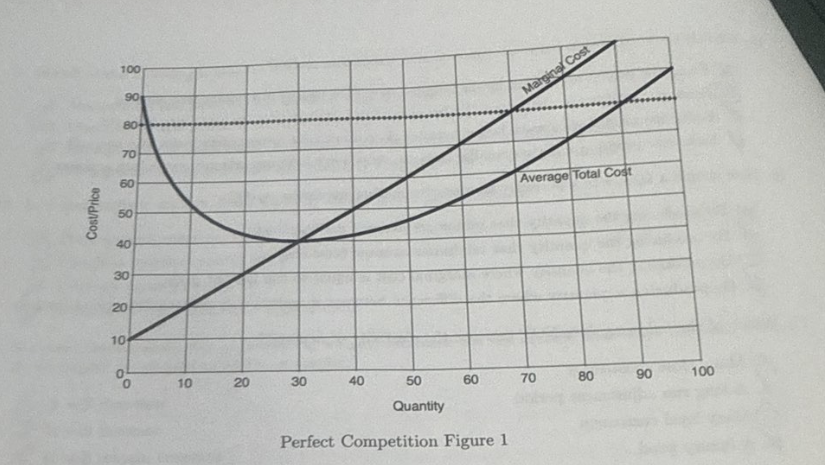

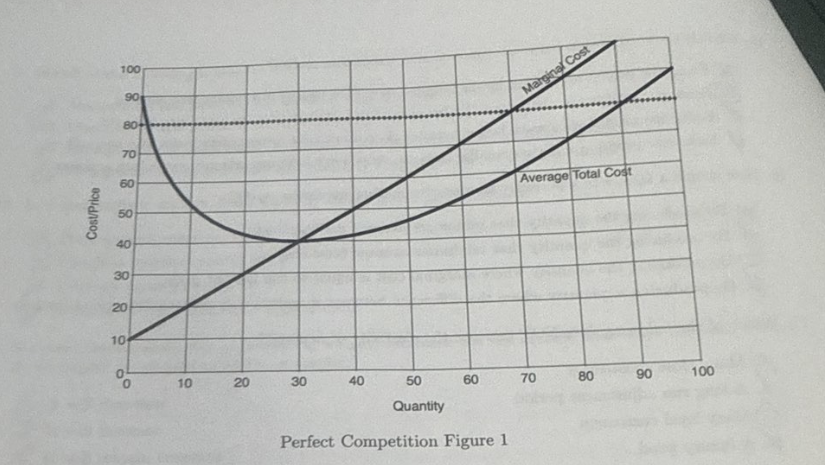

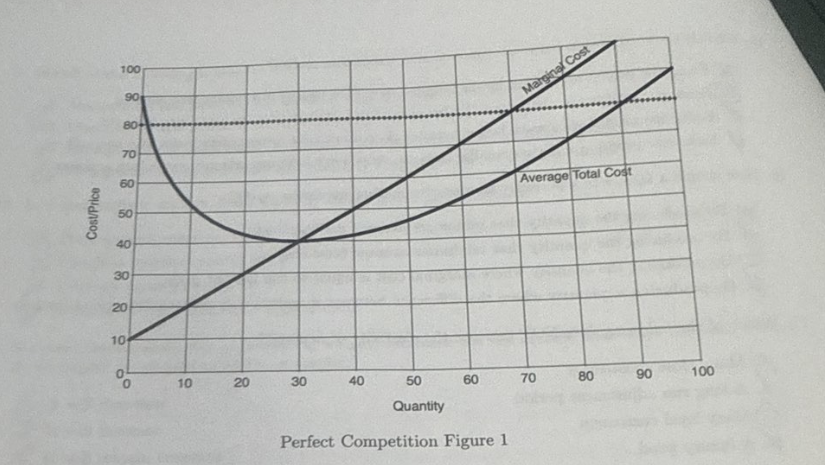

Refer to the Perfect Competition Figure 1. Suppose this is a perfectly competitive market and the market price is equal to $80. What is the profit-maximizing quantity for the firm?

$70

Refer to the Perfect Competition Figure 1. Suppose this a perfectly competitive market and the market price is equal to $80. What is the firms total profit?

1400

Refer to Perfect Competition Figure 1. Suppose this is a perfectly competitive market. We know that if the price is too low, the firm will exit in the long run. What is the lowest price that the firm will tolerate in the long run without exiting the market.

$40

A market failure happens when

Markets left to themselves produce an inefficient outcome

What does the price elasticity of demand measure

The responsiveness of quantity demanded to a change in price

The production possibilities frontier shows

Feasible output combinations

Which of the following is NOT a characteristic of a perfectly competitive market?

A firms production quantity affects the market place

The law of supply states that, everything else held constant, when the price of a good increase

Quantity supplied increases

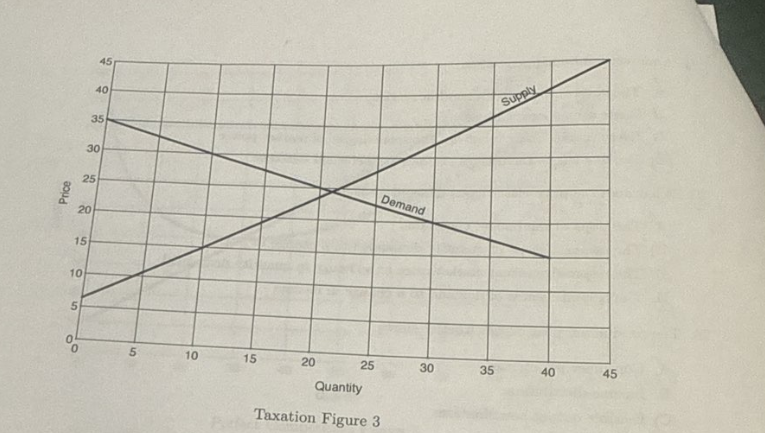

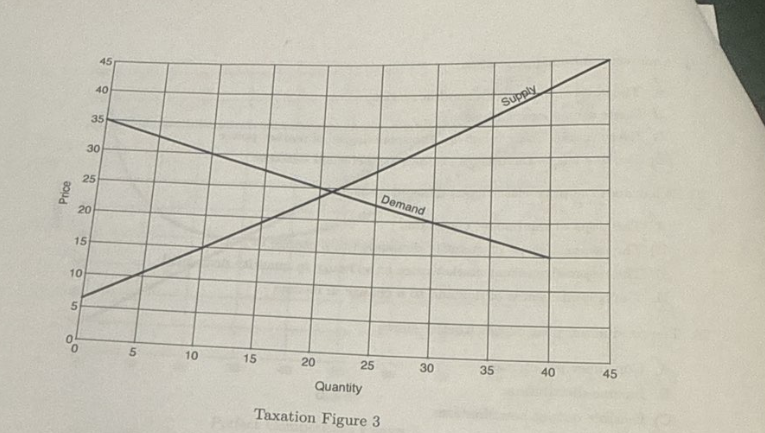

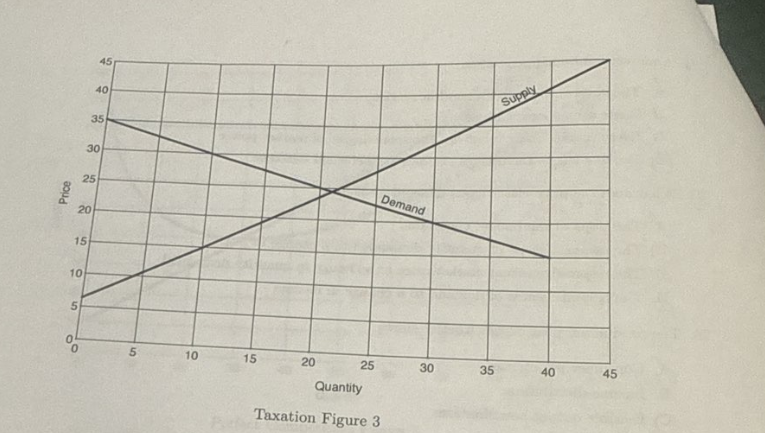

Refer to Taxation Figure 3. If the government imposes a per-unit tax equal to $15, what will the total tax revenue be

$150

Refer to taxation figure 3. If the government imposes a per-unit tax of $15, what is the post tax consumer surplus

25

Refer to Taxation Figure 3. Suppose that the government increases the per-unit tax from $15 to $30. Which of the following is true about tax revenue?

Tax revenue will fall. This is the Laffer Curve

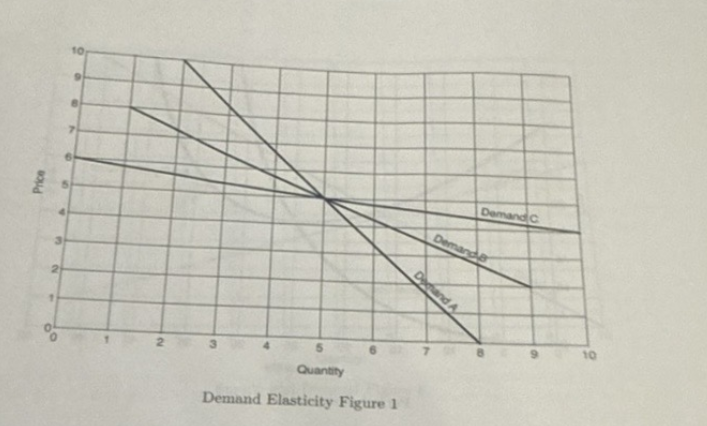

Refer to the Demand Elasticity Figure 1. Which of the following demand curves is the most elastic

C (flattest)

Tradeoffs arise in an economic decision because:

Resources are scarce

Demand for which of the following is most likely to be inelastic?

Life saving insulin for diabetics

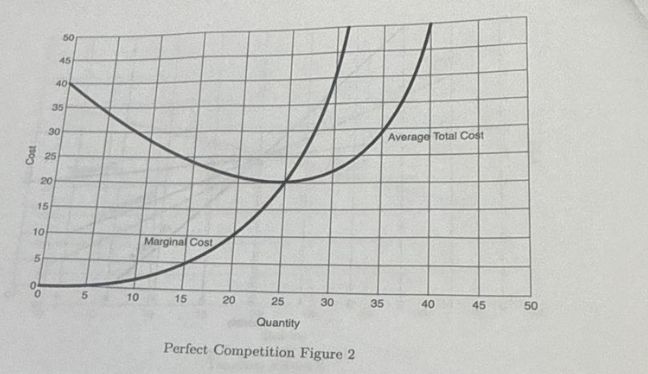

Refer to the Perfect Competition Figure 2. Suppose that the market is perfectly competitive and all of the firms share the same average total cost and marginal cost curves as displayed. What do we expect to happen to the market price in the long-run?

Competition will drive market down to $20

Which of the following supply curve for milk to shift out (i.e to the right)?

An improvement in milk bottling technology

If rent control sets a binding price ceiling on the market, then which of the following is true?

The price ceiling is below the equilibrium rent price and creates a shortage in the market

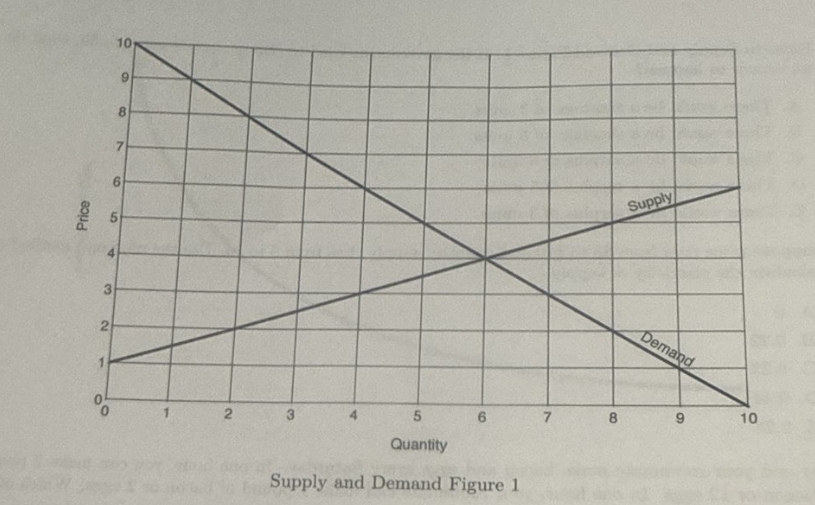

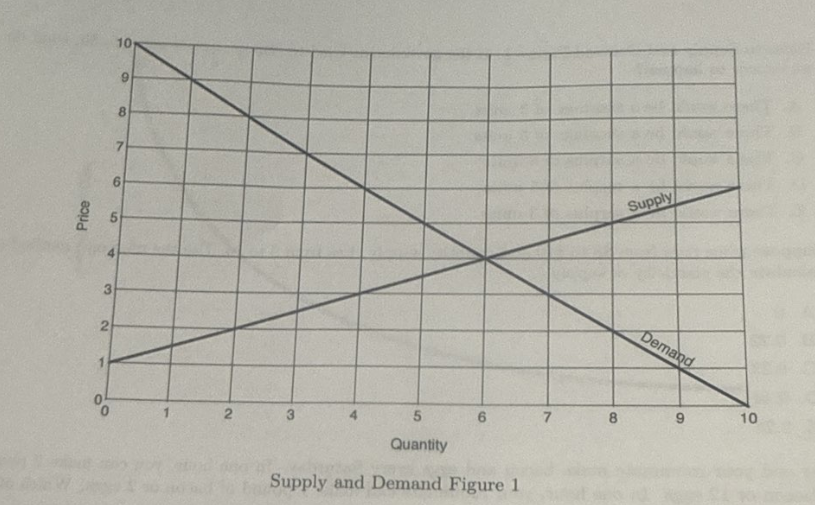

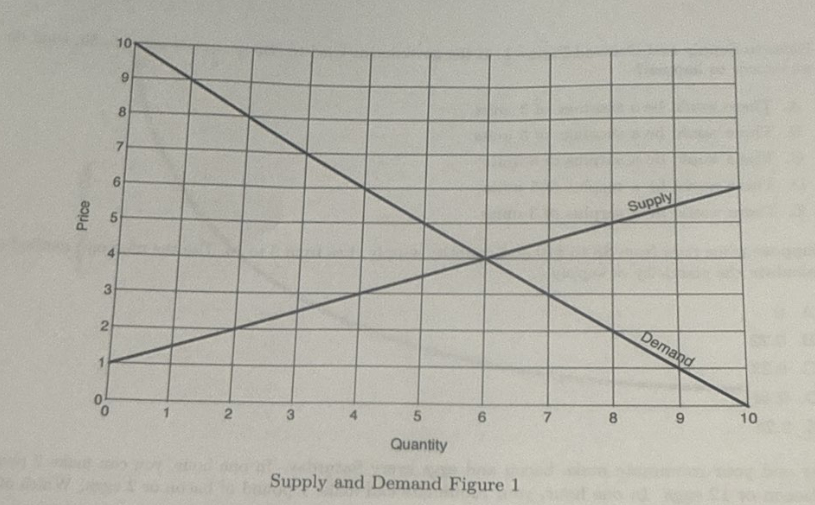

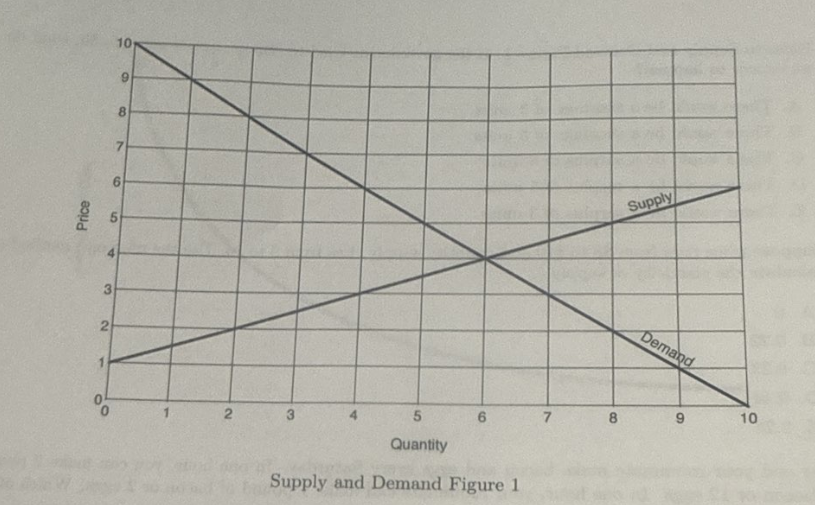

Consider the Supply and Demand Figure 1. What is the marginal consumer’s willingness to pay for the item

$4

Refer to the Supply and Demand Figure 1. What is the market equilibrium quantity

6

Consider the Supply and Demand Figure 1. What is the total surplus in the market

27

Refer to the Figure Supply and Demand 1. If the government tried to impose a price equal to $5, what do we expect to happen

There would be a surplus of 3 units

Suppose price rises from $8 to $10 and quantity supplied rises from 9 to 15 units. Use midpoint method to calculate elasticity of supply.

2.25

You and your roommate make bacon and eggs every Saturday. In one hour, you can make 2 pounds of bacon or 12 eggs. In one hour, your roommate can make 1 pound of bacon or 2 eggs. Which of the following is true?

You have absolute advantage in both bacon and eggs,

You and your roommate make bacon and eggs every Saturday. In one hour, you can make 2 pounds of bacon or 12 eggs. In one hour, your roommate can make 1 pound of bacon or 2 eggs. Which of the following is true?

Your roommate has the comparative advantage in eggs, but you have the comparative advantage in bacom

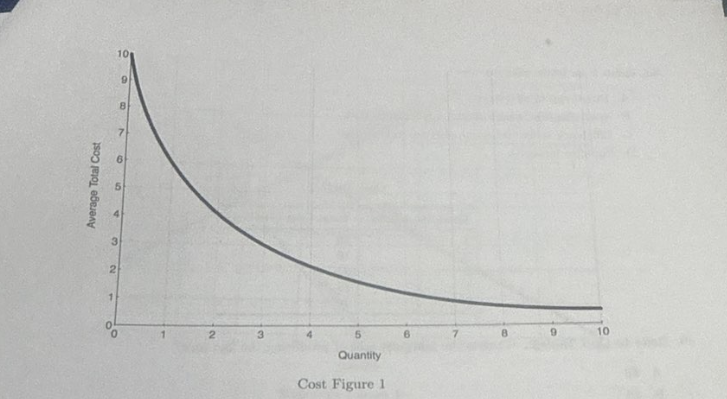

Refer to the average total cost displayed in Cost Figure 1. How would we characterize this cost function?

Economies of Scale

If the government set a binding minimum wage above the market wage, we expect to see

Low demand for labor, resulting in unemployment

Which of the following is NOT a potential barrier to entry that may produce a monopolist?

High profits

Gains from trade arise because

Specialization lowers overall opportunity cost

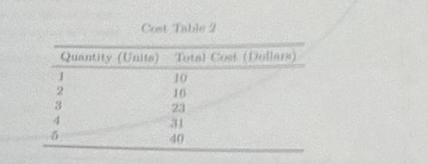

Refer to Cost Table 2. What is the marginal cost of producing the 2nd unit?

$6

Refer to Cost Table 2. If the firm is operating in a perfectly competitive market with the market price of $8, how many units should the firm produce to maximize profit

3 units

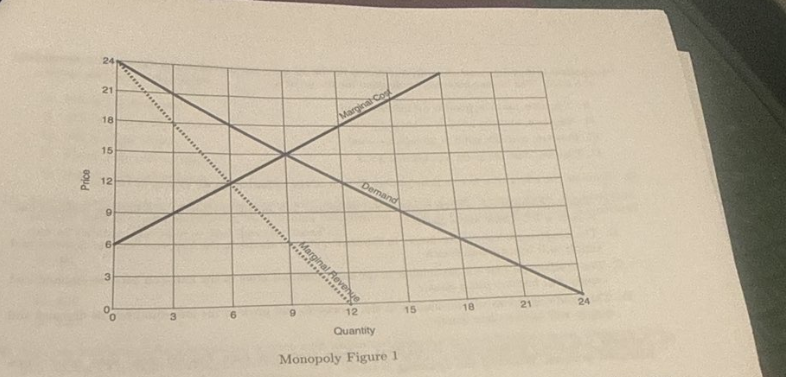

For this problem, refer to Monopoly Figure 1. Given the monopolist marginal costs and the market demand, what is the profit-maximizing quantity of production.

Q*=6 (MC = MR)

For this problem, refer to the Monopoly Figure 1. Given the monopolist profit-maximizing quantity of production, what is the deadweight loss relative to a perfectly competitive market?

9

Which best describes equity (or equality)

Fair distribution of outcomes

Assume that a 4 percent decrease in income results in a 6 percent increase in the quantity demanded of a good. The income elasticity of demand for the good is:

negative, and the good in an inferior good

Consider the effect of a tax as time passes. Which of the following do we expect to be true?

The deadweight loss will be smaller in the short-run and grow in the long-run because demand and supply will become more elastic

Suppose you find research that shows college graduates can earn $20,000 more than non-college educated workers. Which of the following is true?

The higher wage of college-educated in an incentive to finish college

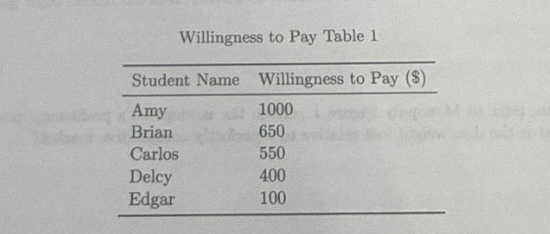

Refer to the Willingness to Pay Table 1, which presents the willingness to pay for a flight to Paris for five different students. If price is equal to $400, what is the total consumer surplus for the students?

$1000

Suppose a firm is in a perfectly competitive market. What is the relationship between the firm’s marginal revenue and the market price

MR is equal to price

You pay $10/month for a streaming service with unlimited episodes of your favorite show. Suppose that you can earn $20/hour working at Outback steakhouse. What is the marginal explicit (monetary) cost of watching one hour of your favorite show.

$0

Which of the following is true?

For monopolist, marginal revenue is less than market price. For perfectly competitive firms, marginal revenue equals market price

What is the difference between positive and normative statements

Positive is fact based, and normative are opinions

The law of demand states that, everything else held constant, when price of a good increase

Quantity demanded decreases

Demand for normal goods increase when which of the following happens

income rises

Which of the following may shift the demand curve for the red meat out (i.e to the right)

Research showing that red meat consumption decreases the risk of Alzheimer’s disease

In the short-run, a firm may continue to operate even with negative profits if which of the following is true

The market price exceeds average variable cost

Efficiency means

Maximizing output from scarce resources

Which best illustrates tradeoff

Studying over sleeping

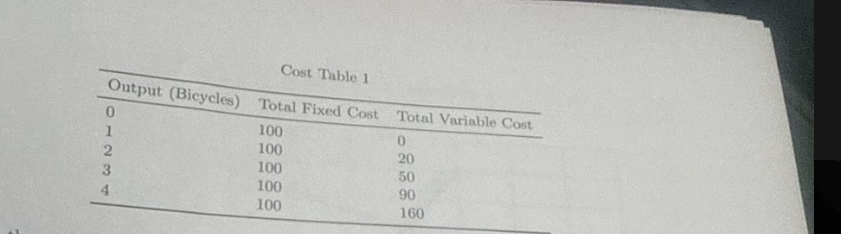

Refer to the cost table listed in Cost Table 1. what is the average total cost when producing 2 bicycles?

$75

Refer to the cost listed in Cost Table 1. What is the efficient scale of production?

Q=3

Suppose that the price rises from $8 to $10 and quantity supply rises from 9 to 15. Use midpoint method to calculate the elasticity of supply

2.25

what best illustrates a trade off

Studying instead of sleeping

Suppose demand and supply both decrease (shift in) at the same time. What do we expect to happen

Equilibrium quantity falls, but the effect on price is unclear

Gains from trade arise because

specialization lowers overall opportunity cost

You pay $10 a month for a streaming service with unlimited episodes of your favorite show. Suppose that you can earn $20/hour working at Outback steakhouse. What is the marginal explicit (monetary) cost of watching one hour of your favorite show?

$0

You pay $10 a month for a streaming service with unlimited episodes of your favorite show. Suppose that you can earn $20/hour working at Outback steakhouse. What is the marginal implicit (opportunity cost) cost of watching one hour of your favorite show?

$20

You and your roommate make bacon and eggs every Saturday. In one hour you can make 2 pounds of bacon and 12 eggs. In one hour, your roommate can make 1 pound of bacon and 2 eggs. Which of the following is true.

You have absolute advantage in both bacon and eggs

You and your roommate make bacon and eggs every Saturday. In one hour you can make 2 pounds of bacon and 12 eggs. In one hour, your roommate can make 1 pound of bacon and 2 eggs. Which of the following is true.

Your roommate has the comparative advantage in bacon, but you have the comparative advantage in eggs

The law of demand states, everything else held constant, when the price of a good increases:

Quantity demanded decreases

Suppose the marginal cost of producing widgets increases but the market price stays the same. What do we expect to happen to producer surplus

It will decrease

If bread and cheese are compliments, which of the following will be true

When the price of bread rises, quantity demanded for cheese will fall

Which of the following is NOT a potential barrier to entry that may produce a monopolist

High Profits

Efficiency means

Maximizing output from scarce resources

Which of the following would cause the supply curve for milk to shift out (i.e to the right)?

An improvement in milk bottling technology

Suppose you find research that shows college graduates earn $20,000 more than non-college education workers. Which of the following is true?

The higher wage of college-educated workers is an incentive to finish college

Which best describes equity (or equality)

Fair distribution of outcomes

Which of the following markets is closest to a perfectly competitive market?

The market for soybeans grown by farmers across the U.S

How should a farmer in a perfectly competitive market maximize profits?

By producing the quantity where marginal cost is equal to market price

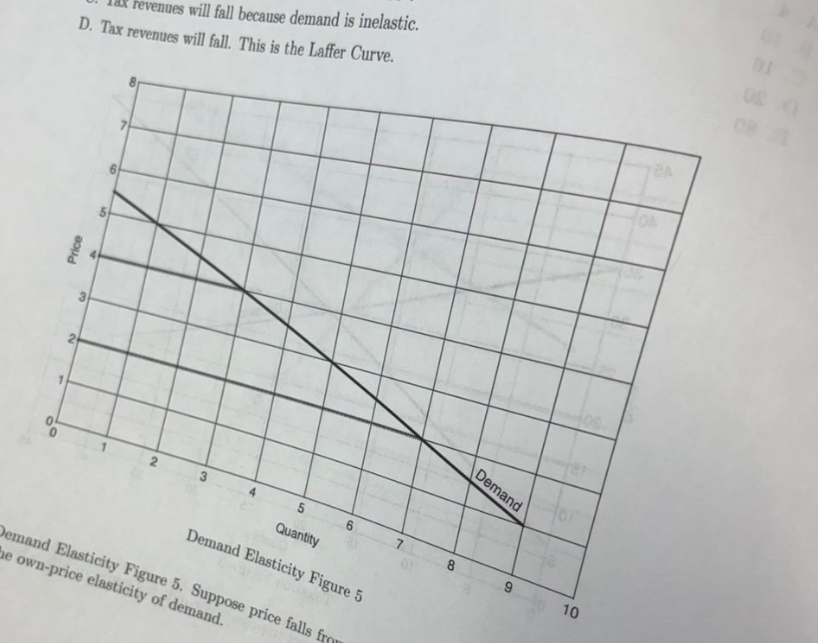

Refer to the Demand Elasticity Figure 5. Suppose price falls from $4 to $2. Use the midpoint method to calculate the own-price elasticity of demand

1.2

Refer to Taxation Figure 3. Suppose to government increases per unit tax from $15 to $30. Which of the following is true about tax revenues

Tax revenue will fall. This is the Laffer Curve

What is the difference between a positive and normative statement

Positive statements are fact based and normative are opinions

Consider the effect of tax as time passes. Which of the following do we expect to be true

Deadweight loss is smaller in the short run and grows in the long run because supply and demand become more elastic over time

Demand for normal good increases when which of the following happens

Income rise

Consider Supply and Demand Figure 1. What is total surplus in the market

27

What is the primary way that monopolist affect welfare in their markets

Monopolists reduce total welfare because they reduce quantity of production compared to production in a perfectly competitive market

Which of the following is true

For monopolist, marginal revenue is less than market price. For perfectly competitive firms, marginal revenue is equal to market price

In the short run, a firm may continue to operate even with negative profits if which of the following is true

The market price exceeds average variable costs

If rent control sets a binding price ceiling on the market, then which of the following is true

The price ceiling is below the equilibrium rent price and creates a shortage of apartments

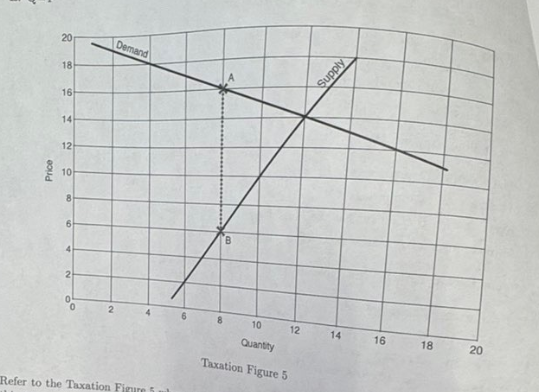

Refer to Taxation figure 5. where there is a per-unit tax imposed on the market. How does the tax reduce the quantity sold in the market

$8

Refer to Taxation Figure 5 where there is a pre tax unit imposed on the market. How do the relative elasticities of demand and supply affect the tax burden

Demand is more elastic, so the sellers bear more of the tax burden

Which of the following is true

Monopolists are price setters and perfectly competitive firms are price takers

Markets organize economic activity primarily through

Prices

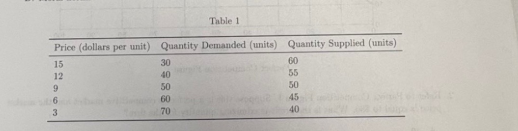

For Table 1. If price were $6, which of the following would be expect

A shortage of 15 units, causing price to rise

Tradeoffs arise in economic decisions because

resources are scarce

A natural monopoly occurs when

the production process exhibits strong economies of scale

In a monopolist market, firms typically can earn positive profits because

price exceeds marginal costs