Perfectly Competitive Market Clearing Model

1/17

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

18 Terms

Demand

The quantity of some good or service consumers are willing and able to purchase at each price

Law of Demand - Ceteris Paribus

If price goes up, then quantity demanded goes down.

If price does down, then quantity demanded goes up.

Normal Good

A product for which demand increases when income rises, and vice versa

Inferior Good

A product for which demand decreases when income rises, and vice versa

Substitute

A good or service that we can use in place of another good or service

Complements

Goods or services that are often used together so that consumption of one good tends to enhance consumption of the other

Market Demand Curve

A graph plotting the total quantity of an item demanded by the entire market, at each price.

Shift in Demand

Happens when a change in some economic factor (other than price) causes a different quantity to be demanded at every price

Demand Determinants

Income

Changing tastes or preferences

Changes in the population

Price of substitute or complement changes

Changes in expectations about future

Supply

The amount of some good or service a producer is willing to supply at each price

Law of Supply - Ceteris Paribus

If price goes up, then quantity supplied goes up

If price goes down, then quantity supplied goes down

Shift In Supply

When a change in some economic factor (other than price) causes a different quantity to be supplied at every price. Also explains why quantity supplied changes when price stays constant.

Inputs or Factors of Production

The combination of labor, materials, and machinery that is used to produce goods and services

Supply Determinants

Natural conditions

Input Prices

Technology

Government Policies

Number of firms producing the good

Perfect Competition

Markets in which all firms in an industry sell an identical good and there are many buyers and sellers, each of whom is small relative to the size of the market

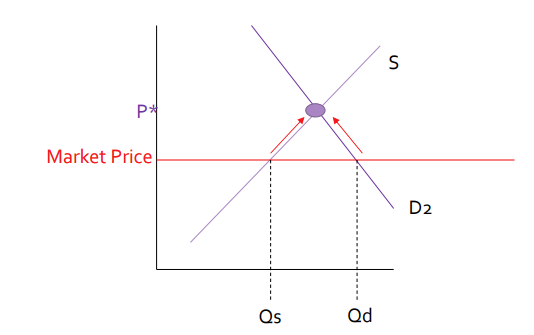

Equilibrium

The point at which there is no tendency for change. A market is in equilibrium when the quantity supplied equals the quantity demanded.

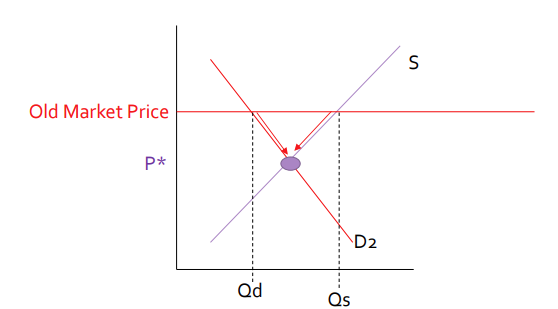

Shortage

When the quantity demanded exceeds the quantity supplied

Surplus

When the quantity demanded is less than the quantity supplied