Current Liabulities (CH. 8)

1/43

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

44 Terms

Current liabilities

Liabilities due witthin one year

Long-term liabilities

Liabilities due within more than 1 year

Notes payable

Written promises to repay amounts borrowed plus interest.

What would be the debits and credits be when recording notes payable, when a party receives $100,000 from a bank?

Debit (Cash): $100,000

Credit (Notes Payable): $100,000

What effect would notes payable have on the Balance Sheet?

Asset (Cash) and the sume of L+ SE would be the same dollar amount

Interest Formula

Face Value (Annual Interest Rate) (Fraction of the Year: X/12 months)

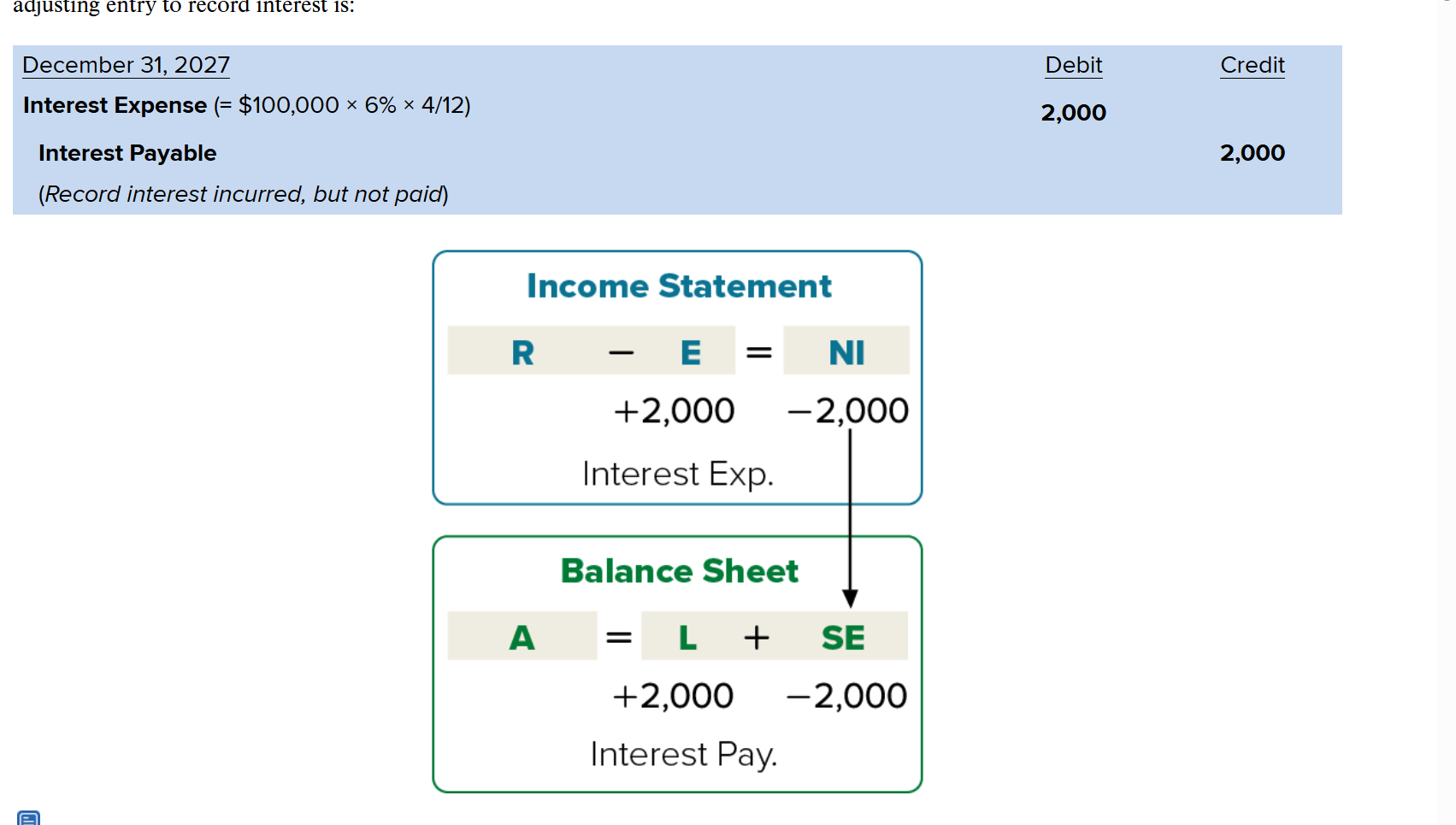

What’s the adjusting entry to record interest?

Debit: Interest Expense

Credit: Interest Payable

Caddell Corporation borrows $100,000 from a bank on August 1, Year 1, by signing an 8 percent, six-month note for the amount borrowed plus accrued interest due six months later on February 1, Year 2. Which of the following is recorded on August 1, Year 1?

A. $104,000 debit to Cash

B. $104,000 debit to Notes Payable

C. $100,000 credit to Cash

D. $100,000 credit to Notes Payable

D. $100,000 credit to Notes Payable

Windsor Corporation borrows $100,000 from a bank on November 1, Year 1, by signing a 9 percent, six-month note for the amount borrowed plus accrued interest due six months later on May 1, Year 2. What is the interest expense per month on this note?

INTEREST= Principle (Rate) (Time)

$100,000×9%×1/12=$750

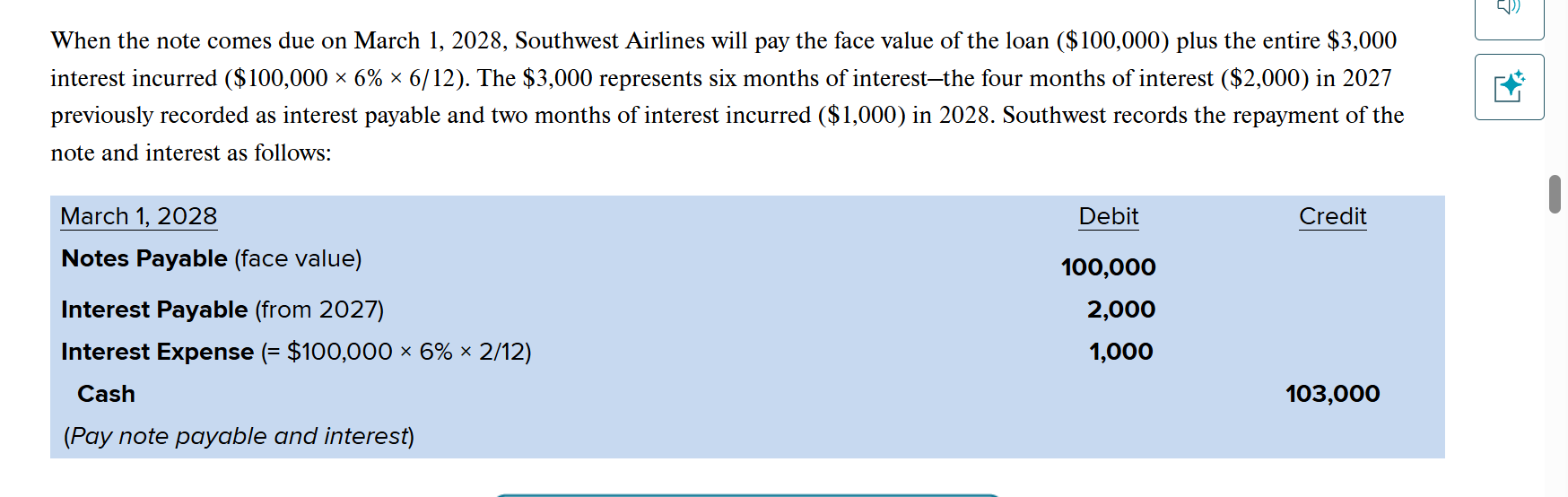

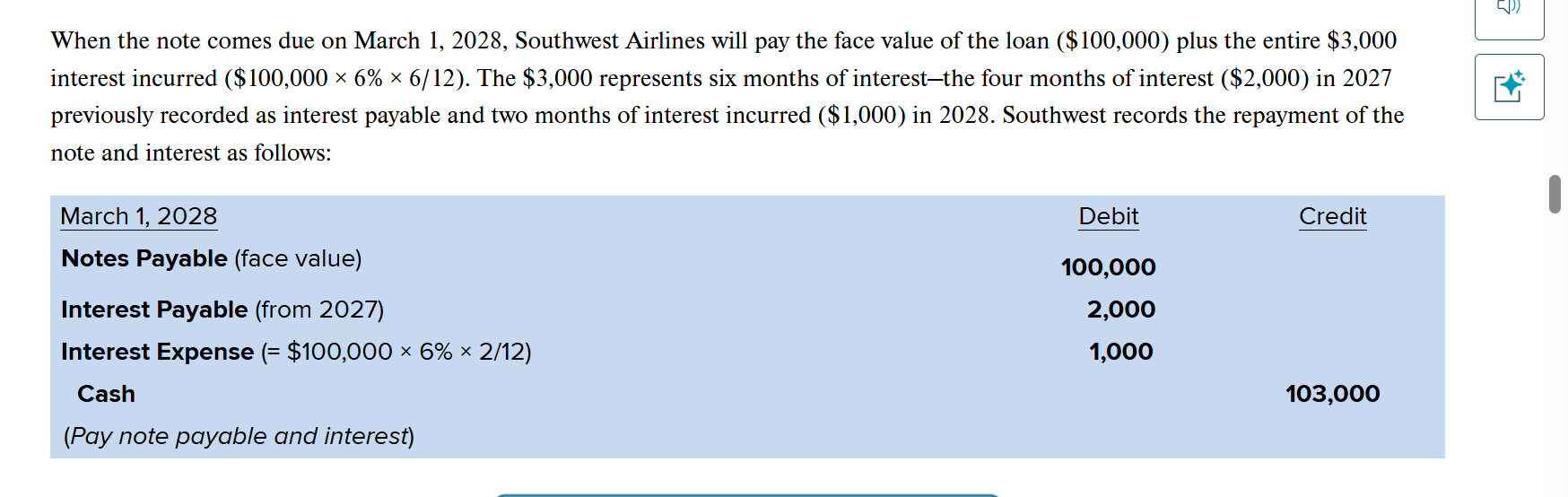

Why is Interest Payable debited instead of Interest Expense on the repayment date?

Interest Payable was already recorded as Interest Expense in the prior year via an adjusting entry. Debiting it on the repayment date simply eliminates that liability — recognizing it again as Interest Expense would double-count it.

Why does Cash credited equal $103,000 and not just $100,000?

Because the borrower repays both the principal ($100,000) and the full six months of accrued interest ($3,000) simultaneously on the due date.

How do you split interest between two accounting periods?

Identify how many months fall in each year. Here, 4 months in 2027 ($100,000 × 6% × 4/12 = $2,000) and 2 months in 2028 ($100,000 × 6% × 2/12 = $1,000).

What is the journal entry to record repayment of a note when interest was partially accrued in a prior year?

Account | Debit | Credit |

|---|---|---|

Notes Payable | 100,000 | |

Interest Payable | 2,000 | |

Interest Expense | 1,000 | |

Cash | 103,000 |

What would the entry look like if no adjusting entry had been made at year-end?

Account | Debit | Credit |

|---|---|---|

Notes Payable | 100,000 | |

Interest Expense | 3,000 | |

Cash | 103,000 |

contingent liability

It is an existing uncertain situation that might result in a future loss.

Examples of Contingent Liability

Lawsuits

Product Warranties

Enviormental Problems

Premium Offers

The accounting treatment for a lawsuit depends on:

the ability to estimate the amount of payment

the likelihood of payment

How is contingent liability recorded on the adjusting entry?

Debit: Loss

Credit: Contingent Liability

When is the contingent liability recorded?

When the likleihood of payment is probable and the amount of payment is reasonably estimable

If the likelihood of payment, and the amount estimated is within the range of $5-$8 million, how should the contingent liability be recorded?

Record the minimum amount within the range. That being $5 million as a liability.

How do you find the warranty liability?

Estimated Warranty Liability = Sales × Expected Warranty Cost %

How do you record contingent liabilities for warranties in the journal entry?

Debit: Warranty Expense

Credit: Warranty Liability

What accounts would you use in the journal entry when recording actual warranty expenditures?

Debit: Warranty Liability

Credit: Cash

How to find the amount of actual warranty liability claims that have been paid?

Total Estimated Warranty Liability - Actual Warranty Expenditures

Contingent Gains

An exisiting uncertain situation that might result in a gain

When is a Contingent Gain recorded?

It’s recorded when the gain is known with certainty

Liquidity

How fast an asset can convert to cash in a relatively short time to pay currently maturing debts

What are the 3 measures of Liquidity

Acid-Test Ratio

Working Capital

Current Ratio

Working Assets

It’s the difference between Current Assets and Current Liabilities. Or how much money you’ll have left after paying off your liabilities?

Why is working capital not the best measure of liquidity?

It does not factor in the relative size of the company

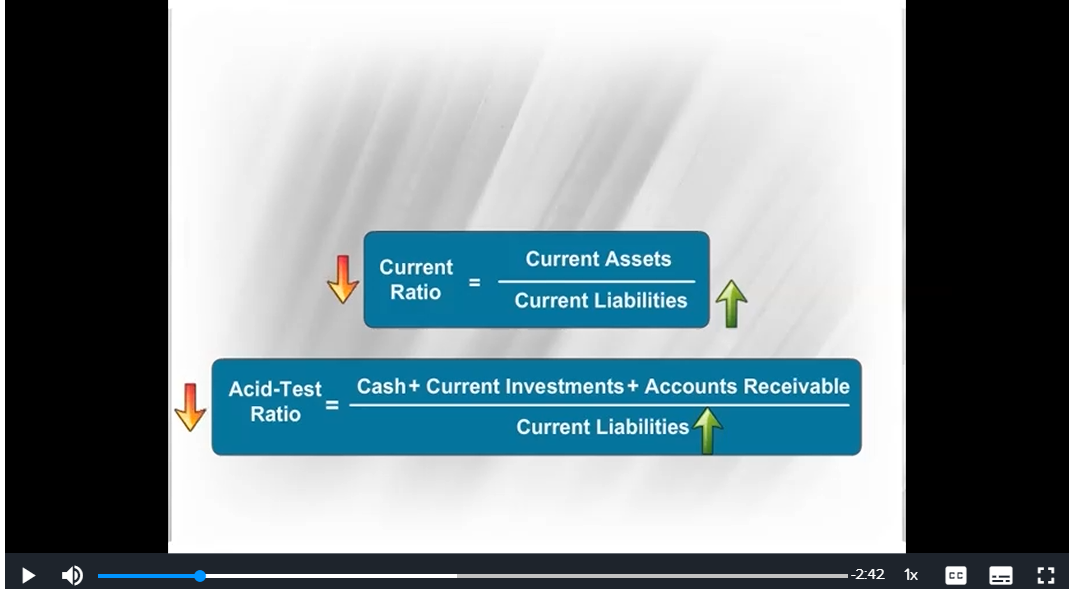

Current Ratio Formula

Current Assets / Current Liabilities

What do current assets include?

Cash + Current Investments + Accounts Recievable + Inventories + Prepaid Expenses

What does it imply if the current ration is > 1?

Current assets exceed current liabilities — generally healthy

What does it imply if the current ration is equal to 1?

Just enough assets to cover liabilities — tight

What does it imply if the current ration is < 1?

Liabilities exceed current assets — potential liquidity problem

In general, the higher the current ratio, the greater the company’s liquidity. True or False?

True

What does it imply if the current ratio is 2?

For every $1 of liabilities, there’s $2 worth of current Assets

Acid Test Ratio / Quick Ratio

Similar to current ratio, It is based on a more conservative measure of current assets available to pay current liabilities.

Acid Test Ratio Formula

Quick Assets (Cash + Current Investments + Accounts Receivables) / Current Liabilities

Is Acid Test Ratio < Current Ratio?

Yes

What factors make the acid test ratio a more accurate measure for liquidity than the current ratio?

It does not factor in current assets such as inventory and prepaid expenses

What does the numerator in the acid base ratio tell us? Quick Assets (Cash + Current Investments + Accounts Receivables) / Current Liabilities

They are accounts that could be quickly be converted to cssh

What happens when you increase current liabilities in both the current ratio and acid test ratio?

current ratio and acid test ratio will decrease