IB Business Management: Formulas that are not in the booklet

1/45

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

46 Terms

Current assets =

Stock + Cash + Debtors

Contribution per unit =

Price - Average Variable Cost

Cost to buy =

Price * Quantity

Current Liabilities =

Overdraft + Tax + Dividends + Creditors

Closing balance in a clash flow =

Opening balance + Net Cash flow

Total Costs =

total fixed costs + total variable costs

Profit =

total revenue - total cost

OR

Total contribution - total fixed costs

Cost of goods sold =

Opening stock + Purchases - closing stock

Average cost =

Total costs / Output level

Cost to make =

Total fixed costs + (Average variable costs * quantity)

OR

Total fixed costs + Total variable costs

Gross profit =

Sales revenue - costs of goods sold

Capital employed =

Loan capital + share capital + retained profit

OR

internal sources of finance + external sources of finance

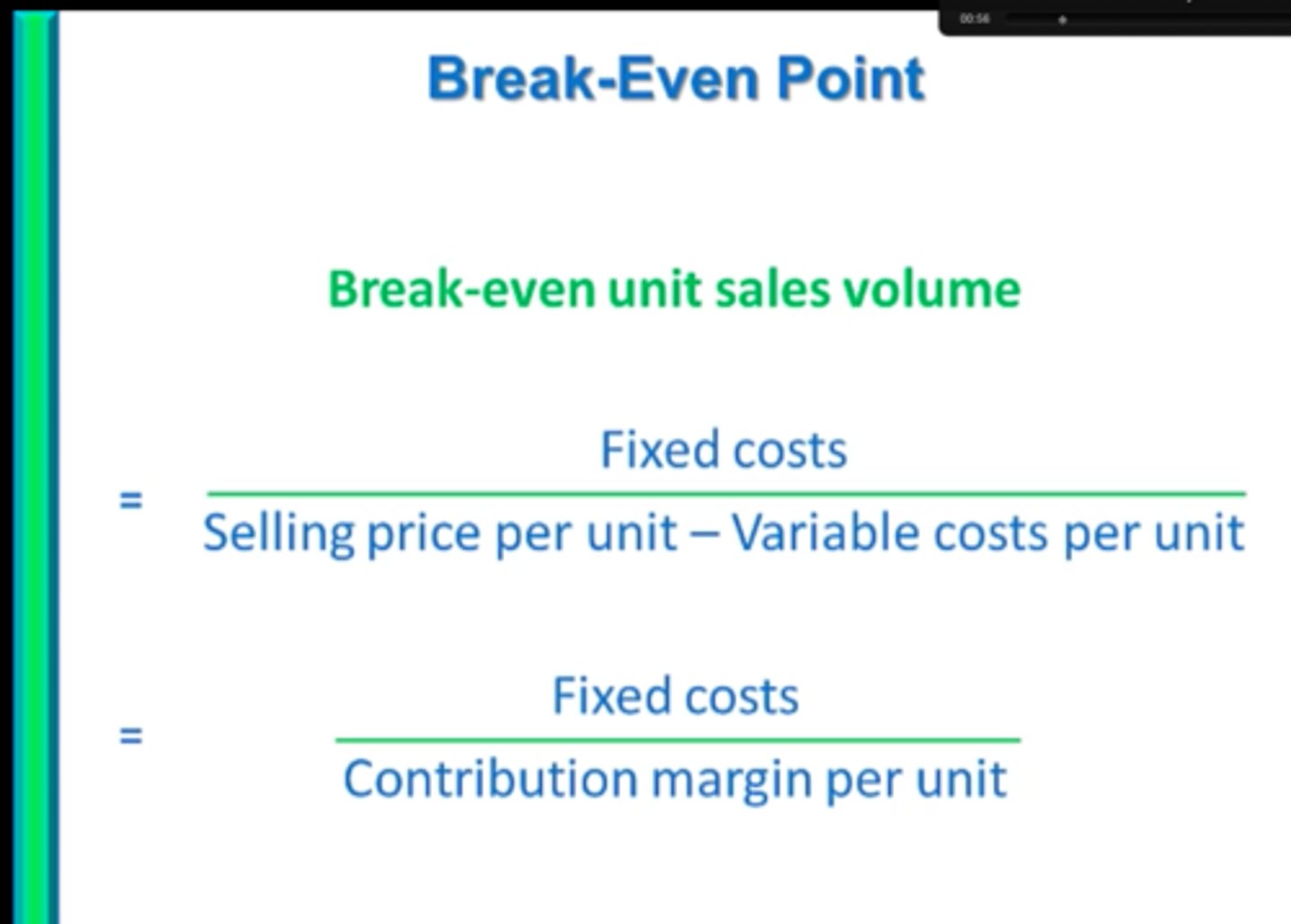

Break-even quantity =

Total fixed costs / unit contribution

Labour productivity =

Total output / number of workers

Labour turnover =

(number of staff leaving / total number of staff) * 100

Straight line annual depreciation =

purchase cost / useful lifespan

net profit =

Gross Profit - Expenses

Absenteeism =

(number of absent staff / total number of staff) * 100

Average costs =

Total costs / output

average fixed costs =

total fixed costs / quantity

average variable cost =

total variable cost / quantity

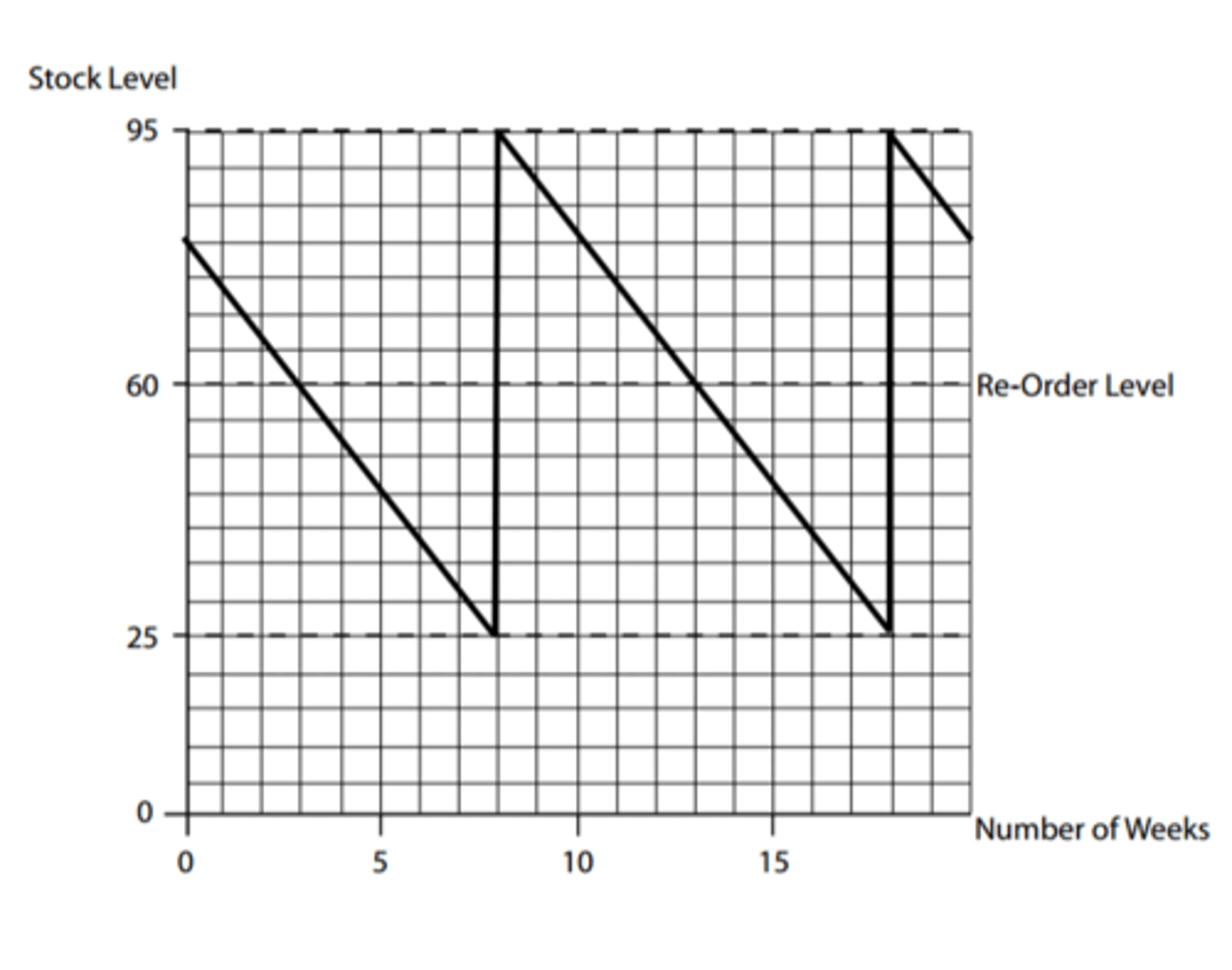

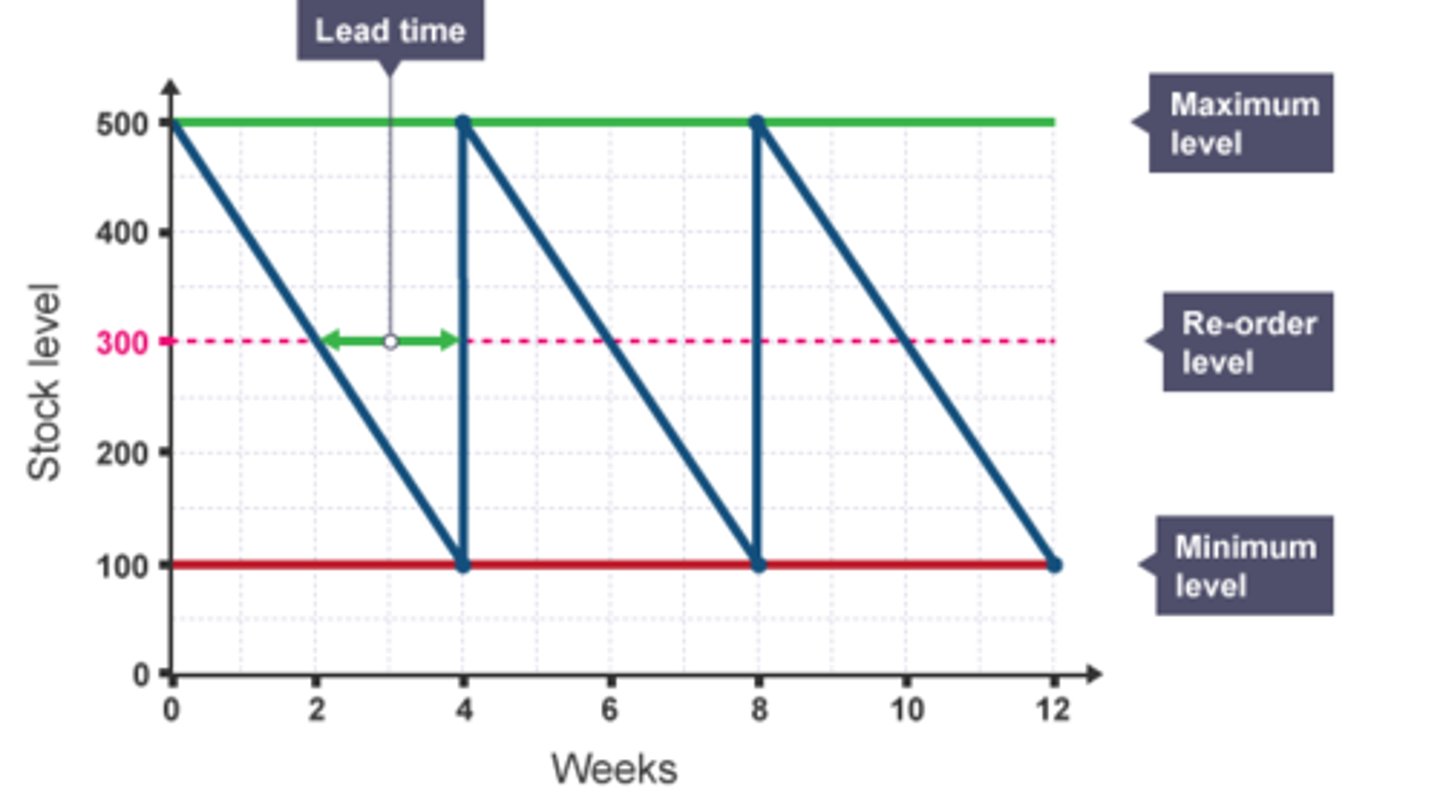

Buffer stock =

(max. daily usage max. lead time) - (average daily usage average lead time)

cost to buy =

Price * Quantity

cost to make =

Variable costs * Quantity

current liabilities =

Trade payables + short term loans + current portion of long term loans + notes payable + accrued expenses + prepaid revenues + other short term debts

Declining Balance Depreciation =

(cost of an asset - residual value) / useful life of an asset

lead times =

supply delay + reordering delay

margin of safety =

Total Sales - Break Even Sales

market share =

(total own sales revenue/total industry sales revenue) * 100

net assets =

total assets - total liabilities

net cash flow =

cash inflow - cash outflow

net current assets

current assets - current liabilities

Net profit before interest and tax =

Gross Profit - Expenses

opening balance =

Closing balance of previous period

payback period =

investment required / annual net cash inflow

reducing-balance annual depreciation =

asset book value * depreciation rate (%)

re-order level =

(maximum daily usage rate * lead time) + safety stock

re-order quantity =

Average Daily Usage x Average Lead Time

straight line annual depreciation =

(historic cost − residual (scrap) value) / estimated life of the asset

target profit =

net sales revenue - (variable costs + fixed costs)

target price =

(total costs + target profit) / output

variances analysis =

actual amount incurred - corresponding budgeted

working capital =

current assets - current liabilities

equity =

Assets - Liabilities

Return on capital employed (ROCE)

(Operating profit / capital employed) * 100

Profitability =

Net profit / Sales Revenue