AIS Final Prt 3

1/72

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

73 Terms

Inaccurate financial statements

Processing integrity controls

Use of packaged software

Training and experience in applying accounting standards and XBRL

Audits

Fraudulent financial reporting

audits

Poorly designed reports and graphs

Responsibility accounting

Balanced scorecard

Training on proper graph design

Inaccurate adjusting entries

Data entry processing integrity controls

Spreadsheet error protection controls

Standard adjusting entries

Reconciliations and control reports

Audit trail creation and review

Unauthorized adjusting entries

Access controls

Reconciliations and control reports

Audit trail creation and review

Inaccurate updating of general ledger

Data processing integrity controls

Reconciliations and control reports

Audit trail creation and review

Inaccurate or invalid general ledger data

Data processing integrity controls

Restriction of access to the general ledger (“G/L”)

Review of all changes to G/L data

Unauthorized disclosure of financial statement

Access controls

Encryption

*Loss or destruction of data

Backup and disaster recovery procedures

Inaccurate payments

Process integrity controls

Supervisory review

Employee review of earnings statement

Failure to make required payments

& Untimely payments

Configuration of system to make required payments using current instructions from IRS

(Publication Circular E)

Theft or fraudulent distribution of paychecks

Restriction of physical access to blank payroll checks and the check signature machine

Restriction of access to the EFT system

Prenumbering and periodically accounting for all payroll checks and review of all EFT direct deposit transactions

Require proper supporting documentation for all paychecks

Use of a separate checking account for payroll, maintained as an imprest fund

Segregation of duties (cashier versus accounts payable; check distribution from hiring/firing; independent reconciliation of the payroll checking account)

Restriction of access to payroll master database

Verification of identity of all employees receiving paychecks

Redepositing unclaimed paychecks and investigating cause

Errors in payroll processing

Data processing integrity controls: batch totals, crossfooting of the payroll register, use of a payroll clearing account and a zero-balance check

Supervisory review of payroll registers and other reports

Issuing earnings statements to employees

Review of IRS guidelines to ensure proper classification of workers as either employees or independent contractors

Inaccurate time and attendance data

Biometric authentication

Segregation of duties (reconciliation of job-time tickets to timecards)

Supervisory review

Inaccurate updating of master data

Data processing integrity controls

Regular review of all changes to master payroll data

Unauthorized changes to payroll master data

Segregation of duties: HRM department updates master data, but only payroll department issues paychecks

Access controls

Violations of employment laws

Thorough documentation of hiring, performance evaluation, and dismissal procedures

Continuing education on changes to employment laws

Hiring unqualified or larcenous employees

Sound hiring procedures, including verification of job applicants’ credentials, skills, references, & employment history

Criminal background investigation checks of all applicants for finance-related positions

*Inaccurate/Invalid master data

Data processing integrity controls

Restriction of access to master data

Review of all changes to master data

*Unauthorized disclosure of sensitive information

Access controls

Encryption

Tokenization (of customer personal information)

Disruption of operations

Backup and disaster recovery plans

Network and logical access controls

Loss of inventory or fixed assets due to fire or disasters

Physical safeguards

Insurance

Sub optional investments in fixed assets

Proper approval of fixed-asset acquisitions, including use of requests for proposals to solicit multiple competitive bids

Poor performance

Training

Performance/managerial reports

Theft of Fixed Assets

Physical inventory of all fixed assets

Restriction of physical access to fixed assets

Maintaining detailed records of fixed assets, including disposal

Over & under production

Production planning systems

Restriction of access to production orders & schedules

Review and approval of production orders & schedules

Poor product design resulting in excess costs

Analysis of costs arising from product design choices

Analysis of warranty and repair costs

Incomplete or inaccurate orders

Data entry edit controls (see Chapter 13)

Restriction of access to master data

Invalid orders

Digital or written signatures

Uncollectable accounts

Credit limits checked and if sale exceeds limit, specific authorization needed

Specific authorization to approve sales to new customers or sales that exceed a customer’s credit limit

Review aging of accounts receivable reports

Stockouts and excess inventory

Perpetual inventory control system

Use of bar codes or RFID

Training

Periodic physical counts of inventory

Sales forecasts and activity reports

Loss of customers

CRM systems, self-help websites, and proper evaluation of customer service ratings

Picking the wrong items or the wrong quantity

Automation of picking using bar-code and RFID technology

Reconciliation of picking lists to sales order details

Theft of inventory

Restriction of physical access to inventory

Documentation of all transfers of inventory between

receiving and inventory employees

RFID and bar-code technology

Restrict ability to cancel sales

Control creation of and shipments to “one-time” customers

Periodic physical counts of inventory and reconciliation to recorded quantities

Segregate custody versus receiving of inventory

Shipping errors

(fail to ship the goods, wrong quantities, wrong items, ship to wrong address, duplication)

Reconciliation of shipping documents with sales orders, picking lists, and packing slips

Use RFID systems to identify delays

Data entry via bar-code scanners and RFID edit controls

Data entry edit controls (if shipping data entered on terminals)

Configuration of ERP system to prevent duplicate shipments

Failure to bill the customer

Separation of shipping and billing functions

Periodic reconciliation of invoices with sales orders, picking tickets, and shipping documents

Billing Errors

Configuration of system to automatically enter pricing data

Restriction of access to pricing master data

Data entry edit controls

Reconciliation of shipping documents (picking tickets, bills of lading, & packing list) to sales orders

Posting errors in accounts receivable

Data entry edit controls

Reconciliation of batch totals

Mail monthly statements to customers

Reconciliation of subsidiary accounts to general ledger

Inaccurate or invalid credit memos

Segregation of duties of credit memo authorization from both sales order entry and customer account maintenance

Configuration of system to block credit memos unless there is either corresponding documentation of return of damaged goods or specific authorization by management

Cash flow problems

Lockbox arrangements, EFT, or credit cards

Discounts for prompt payment by customers

Cash flow budgeting

Purchasing items not needed

Perpetual inventory system

Review and approval of purchase requisitions

Centralized purchasing function

Purchasing items at inflated prices

Price lists

Competitive bidding

Review of purchase orders

Budgets

Purchasing goods of poor quality

Purchasing only from approved suppliers

Review and approval of purchases from new suppliers

Tracking and monitoring product quality by suppliers

Holding purchasing managers responsible for rework & scrap costs

Unreliable suppliers

Requiring suppliers to possess quality certification (e.g., ISO 9000)

Collecting and Monitoring supplier delivery performance data

Purchasing from unauthorized suppliers

Maintaining a list of approved suppliers and configuring the system to permit purchase orders only to approved suppliers

Review and approval of purchases from new suppliers

EDI specific controls (access, review of orders, encryption, policy)

Kickbacks

Prohibit acceptance of gifts from suppliers

Job rotation and mandatory vacations

Requiring purchasing agents to disclose financial & personal interests in suppliers

Supplier audits

Accepting unordered items

Requiring existence of approved purchase order prior to accepting any delivery

Mistakes in counting

Do not inform receiving employees about quantity ordered

Require receiving employees to sign receiving report

Incentives

Use of bar codes and RFID tags

Configuration of the ERP system to flag discrepancies between received & ordered quantities that exceed tolerance threshold for investigation

Not verifying receipt of services

Budgetary controls

Audits

Errors in supplier invoice

Verification of invoice accuracy

Requiring detailed receipts for procurement card purchases

ERS

Verification of freight bill and use of approved delivery channels

Mistakes in posting to accounts payable

Data entry edit controls

Reconciliation of detailed accounts payable records with the general ledger control account

Failure to take advantage of discounts for prompt payments

Filing of invoices by due date for discounts

Cash flow budgets

Paying for items not received

Requiring that all supplier invoices be matched to supporting documents acknowledged by both receiving & inventory control

Budgets (for services)

Verification of all receipts for travel expenses

Use of corporate credit cards for travel expenses

Duplicate payments

Requiring a complete voucher package for all payments

Policy to pay only from original copies of supplier invoices

Cancelling all supporting documents when payment is made

Theft of Cash *@2

Physical security of blank checks and check-signing machine

Periodic accounting of all sequentially numbered checks by cashier

Access controls to EFT terminals

Use of dedicated computer and browser for online banking

ACH blocks on accounts not used for payments

Separation of check-writing function from accounts payable

Requiring dual signatures on checks greater than a specific amount

Regular reconciliation of bank account with recorded amounts by someone independent of cash disbursements procedures

Restriction of access to supplier master file

Limiting the number of employees with ability to create one-time suppliers and to process invoices from one-time suppliers

Running petty cash as an imprest fund

Surprise audits of petty cash fund

Check alteration

Check-protection machines

Use of special inks and papers

”Positive Pay” arrangements with banks

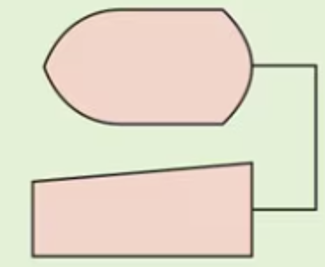

start / end

End (of a process)

activity in process

gateway

flow

annotation info

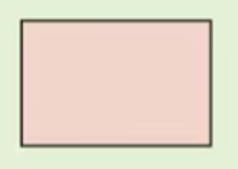

doc

multiple copies of one paper doc

electronic output

electronic data entry

electronic input and output device

computer processing

manual operation

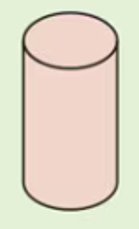

database

magnetic tape

paper document file

n = numberically

a = alphabetically

d = date

journal / ledger