International financial spillovers

1/16

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

17 Terms

Taper-Tantrum 2013 overview

In May 2013, Fed chairman first raised possibility of reducing its large scale asset purchase programme (QE)

The timing of this surprised markets

shifted investor expectations of MP & QE

Stress lasted for a few months

Affected other markets including EMEs

Taper-Tantrum 2013 - Effects on EMEs

US interest rates rose sharply + treasury yields spiked (1.5% → 3%)

Investors withdrew K from EMEs - Broad-based sell off of EME assets to move to invest in US

Bond yields rose as bond p fell

Stock markets fell

Heterogenous effect

Why was US using QE before TT 2013

During GFC, the Fed reduced its target for short-term interest rates to virtually zero.

No scope to use conventional MP → CB turned to unconventional MP (QE)

Between 2008 and 2012, the Fed initiated 3 aggressive rounds of QE, expanding balance sheet from under $1 trillion → $3 trillion prior to TT. By using QE, the Fed significantly reduced the available supply of these safe assets. This bid up asset prices and compressed term premiums, which successfully forced down long-term yields

Reasons for heterogeneous impact on EMEs

Macroeconomic Fundamentals (MFs)

CA / GDP + R / GDP + Debt / GDP + Inflation

Policy

ER regime + inflation targets

Financial market structure

Capitalization of domestic equity market as a share of GDP + level of foreign investor participation

Amount of K flowing in prior to TT

More in - more out hypothesis

Ahmed et al. (2017) - OV

Focus on MF and how they explain heterogeneity

Also looks at other severe EME-wide financial stress since 1990s

Mexico crisis

Asian Crisi

GFC

35 EMEs

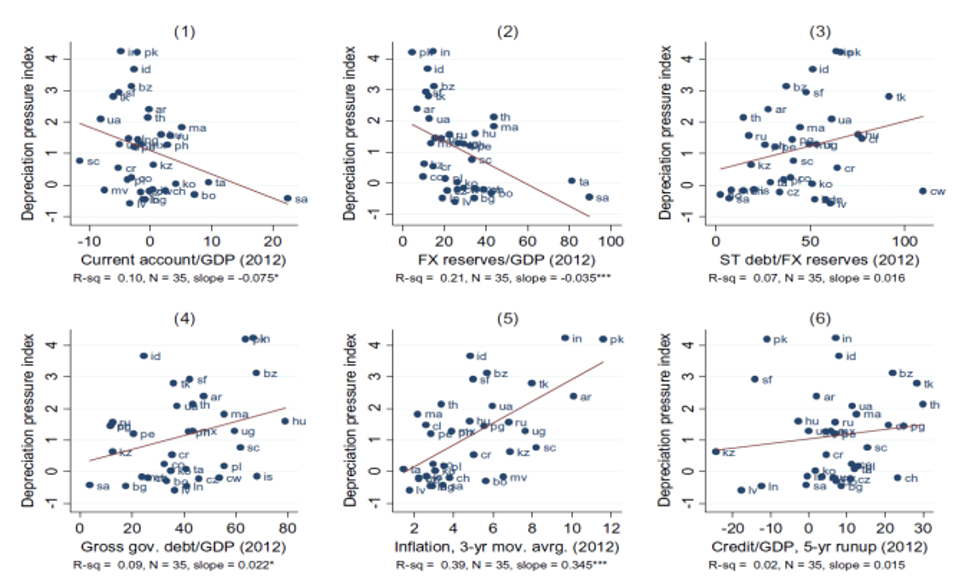

Ahmed et al. (2017) - Regression

Combines all of TT into 1 ‘episode’

Financial variables:

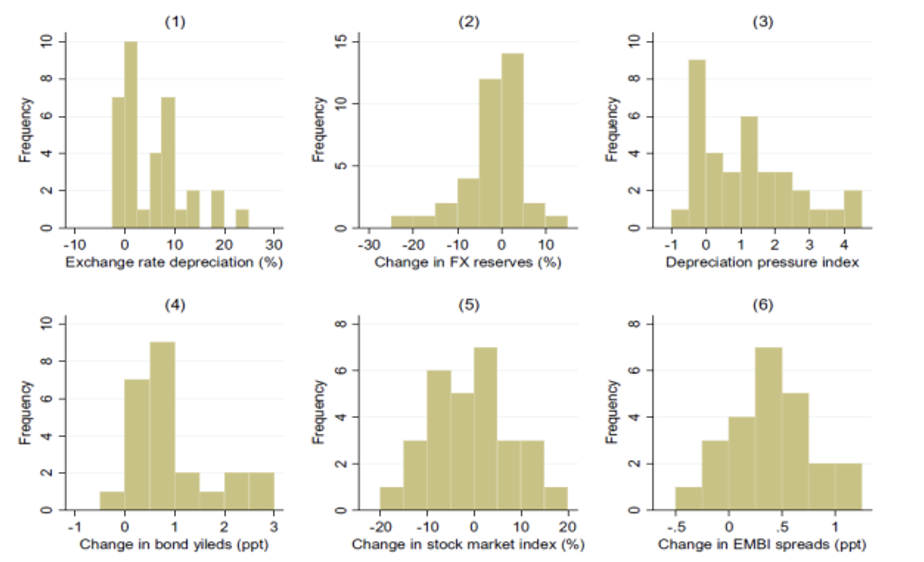

ER depreciation + Depreciation pressure index (includes use of R to mitigate) + change in local currency bond yields + EMBI spread (difference between EME & developed interest rate) + stock market index changes

Xi, j - Set of explanatory var (j) specific to country i

includes MF measured in yr prior to onset of stress event

Ahmed et al. (2017) - Hetero performance

Very heterogenous effects across both countries and variables

Ahmed et al. (2017) - Univariate regression

Doesnt control for anything

F reserves + CA / GDP + Debt / GDP + Inflation sig

Ahmed et al. (2017) - Multivariate regression results

Variables describing strength of MF matter (sig)

MF on the whole play a key role in explaining heterogeneity of financial performance in EMEs

even when controlling for other factors

Some evidence that more in - more out var also matter

High K inflows pre crisis

Greater ER appreciation prior

Mishra et al. (2014) - OV

Examines the role of macro fundamentals and other factors in the impact of tapering announcements on EMEs’ financial variables using event study approach

Considering ER (against US $), government bond yields, and equity prices

Macro fundamentals cover inflation, fiscal balance/GDP, CA/GDP, and Reserves/GDP

Other factors include financial depth variables (such as stock market capitalization/GDP and bank credit/GDP), EME growth prospects, China’s growth etc.

21 EMEs

Mishra et al. (2014) - Conjecture

Countries with weaker fundamentals are harder hit

Larger ER depreciation

Higher increase in bond yields

Larger fall in equity prices

Mishra et al. (2014) - Event study approach

Use 2-day window around FOMC meetings and release on minutes

Jan 2013 → Jan 2014 period

narrow window reduces possibility that ER or other dependent variables are affected by other factors

Use 2-day change in financial variables as dependent variable

Examine financial market reactions to US MP events considering country characteristics (CC)

CC includes MF

identify negative events from set of 17 possible times

Events associated with ER depreciation + yields increase + equity price falls

Then study which CC influences market reaction

By interacting CC with event dummies

Mishra et al. (2014) - RESULTS

CC matter for market reaction

Strong relevance of MF

E.g. when dependent var is two-day change in ER → Countries with stronger MF (e.g., higher current account balances) had lower depreciation

Countries with deeper financial markets underwent smaller ER depreciation

Similar results to Ahmed et al. (2017)

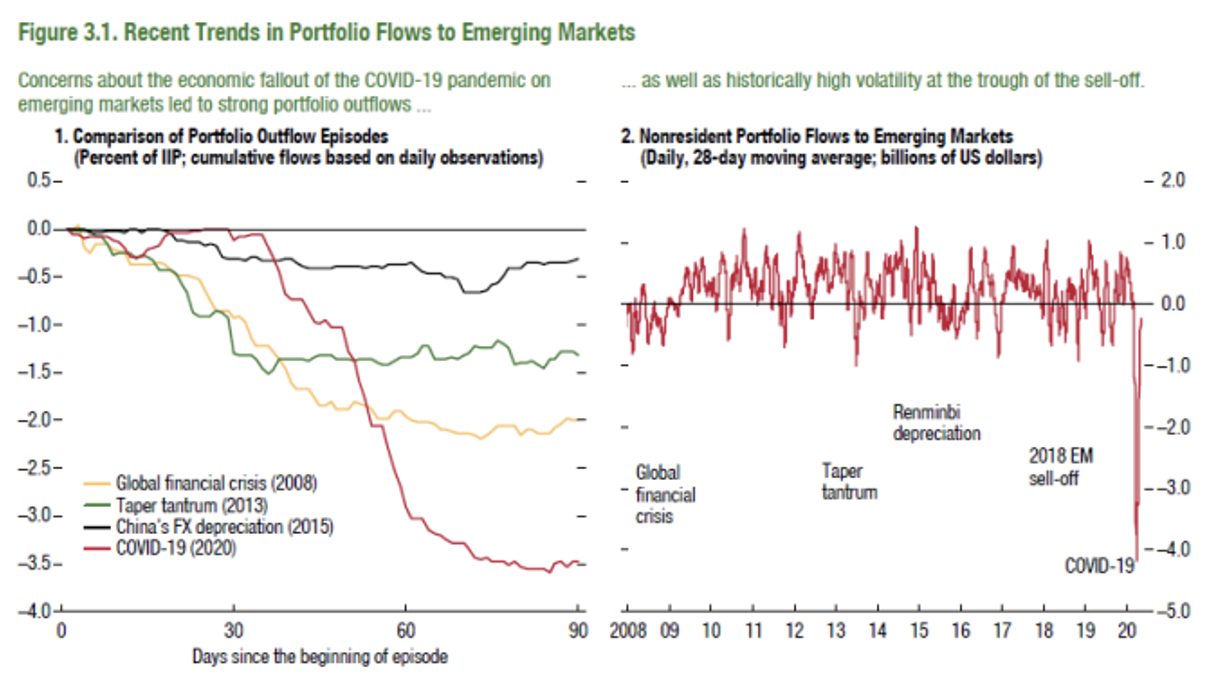

Covid 19 & portfolio flows in EMEs - OV

C19 created huge volatility in financial markets in EMEs

Sharp unprecedented reversal of portfolio flows

Equity & debt securities

IMF 2020 - data

Very high onset of K returning to domestic markets

more than TT or GFC

F investors portfolio flows into EMEs sharply reversed

BUT not sustained

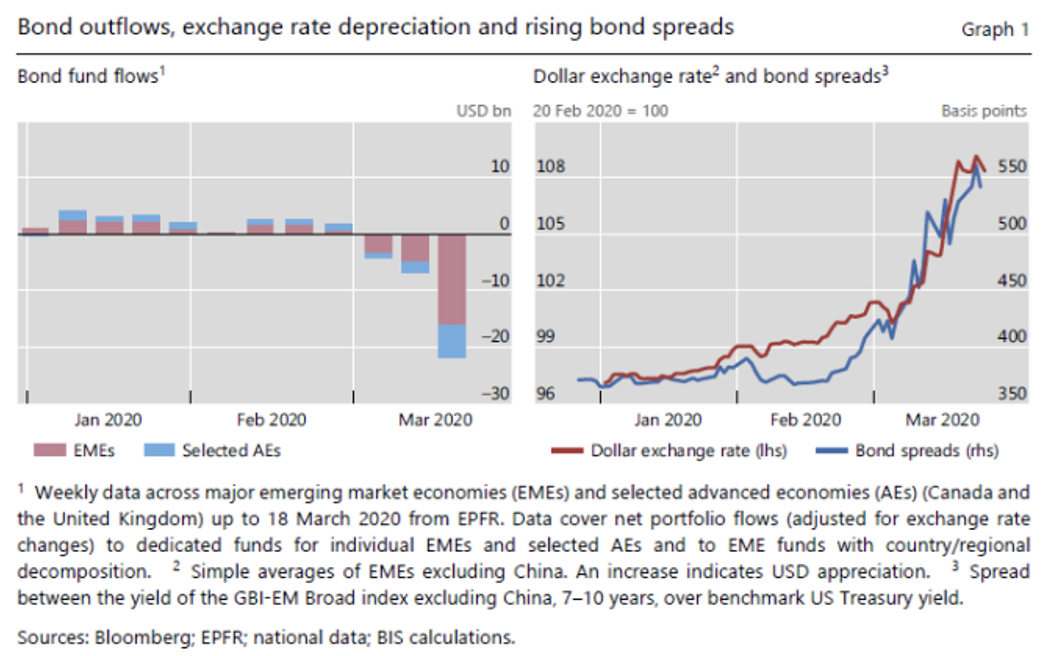

Hofmann et al. (2020) - data

Sharp reduction of K into EME bonds (more than in advanced economies)

Large depreciation of EME currency

Sharp spike in bond spread - investors demanded significantly higher interest rates to hold riskier EME debt during this crisis period

IMF 2020 - results

Large heterogeneity in effects between EMEs

Stronger domestic fundamentals helped mitigate portfolio outflows

although dont always lead to surges in inflows

Greater F investor participation in local currency bond markets may create trade-offs

It can help reduce borrowing costs BUT High Demand leads to price increase and interest rates down

It may also increase price volatility BUT F investors very sensitive to global factors