BA final rules

1/56

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

57 Terms

Creation of Agency RTA 1.01

To create an agency relationship:

1. Principal authorizes agent to act on principal’s behalf + under their control.

2. Agent consents to act.

Exam use: If facts show authorization, control, and consent, analyze agency regardless of labels.

Actual conduct and their relationship > disclaimers or contract labels like “independent contractor”

Yost v. Wabash College

a company or parent organization is not liable for its affiliated group’s wrongdoing without mutual assent and the group acting on the principal's behalf— the principal having control over branding/rules for the group is NOT enough

Cloudberry

franchise agreement with disclaimer that they are not agents is not dispositive

instead, franchisor/principal liability depends on whether they actually exercises sufficient day-to-day control over the franchise’s ops to create an agency relationship,

and a franchisee is AUTOMATICALLY liable for its own employees (respondeat superior/vicarious liability)

Respondeat Superior:

Vicarious Liability

Vicarious Liability - A principal is vicariously liable for the acts of its agent committed within the scope of the agency relationship

Employer is vicariously liable for acts of its employees committed in scope of employment

Agent’s authority RTA 2.01, 2.02, 2.03

Actual Authority (RTA 2.01–2.02):

Agent reasonably believes principal authorized action based on principal’s words/conduct.

Can be:

Express actual authority (clear oral or written permission) OR

Implied actual authority ( can do whatever is necessary or incidental to carry out express authority)

Apparent Authority RTA §§2.03 - Third party reasonably believes agent has authority from principal’s manifestations. Elements:

Principal creates appearance of agent’s authority

Appearance is communicated (directly or indirectly) to the third party.

Third party reasonably relies on that appearance of authority in entering the transaction.

Castillo v. Case Farms of Ohio

a principal is liable for a third party’s actions when it hires them to do a job and those actions happen while doing what is reasonably needed to complete that job, even if the principal labels the job title/contract something denying agency

Agent’s Fiduciary Duties (RTA 8.01)

RTA 8.01 Duty of Loyalty - An agent must act loyally for the principal’s benefit in anything connected with the agency relationship (cant act for just their own personal gain)

No competing: Agent cant start their own biz that competes w principal’s

No acting as an adverse party: Agent cannot be on the other side of a deal or be opposing party to the principal.

No self-dealing aka agent selling to themselves

No conflicts of interest: agent can’t have personal financial interest in deal where it conflicts with what principal wants

No misuse of info: Agent cannot use or share the principal’s confidential information for personal benefit.

No secret profits: Agent cannot accept extra money, gifts, or benefits from third parties because of their role.

If breached: Agent may have to pay damages and give back any profits they improperly made (disgorgement).

other duties: duty of care and good faith to the principal

Food Lion, Inc. v. ABC

Agency fiduciary duty breach example:

an employee breached the duty of loyalty by “acting as an adverse party” = intentionally advanced another party’s interests that was directly adverse to their employer

Agency exam checklist:

Creation of agency RTA 1.01

Agent’s authority RTA 2.01, 2.02, 2.03

Agent’s fiduciary duties RTA 8.01

1. Was there an agency relationship? Always cite RTA §1.01. Identify assent, control, and acting on behalf of the principal.

Did agent act within the scope of authority of the agency relationship?

Analyze actual authority (2.01) AGENT believed + they could act on behalf + based on principals manifestations

(Express or implied (2.02) told explicitly to do vs anything necessary or incidental to carry out as agent reasonably understands

Analyze apparent authority (2.02) THIRD PARTY believed + agent had authority based on principals manifestations

1) Principal creates appearance of agent’s authority

2) Appearance is communicated to the third party.

3) 3rd part reasonably relies on appearance of authority

Address vicarious liability.

Consider fiduciary duties, especially the duty of loyalty.

Forming a partnership RUPA 202 and Managing a partnership RUPA 401(b)

§ 202(a) – Partnership Formation - Partnership = 2+ persons carry on as co-owners intending to run a business for profit

§ 202 (c.) if they share profits (or at least discuss it)→ courts will presume theres a partnership (NOT required but it helps)

BUT it can be rebutted:

employee who’s paid wages from profits is NOT a partner

creditor who receives repayment from profits is NOT a partner

§ 401 (b) If partnership agreement is silent,default rule is partners share profits and losses equally

Partnership formation supported by:

Contributing capital and/or labor (Kovacik exception - only liable for capital losses if you only contributed capital and vice versa)

Holmes - No written agreement, no intent, no profit-sharing is OK as long as you still acted like cowners + intending to run business for profit

Partnership formation DEFEATED by:

labelling your Intent “we’re not partners” is NOT binding if they acted as above BUT its evidence against it

no management rights (no co-ownership) AND no loss sharing → no partnership

Partnership fiduciary duties RUPA 409

RUPA § 409b Partners owe Duty of Loyalty

Partners cannot;

Steal from the partnership

Self-deal (pocket side deals)

Compete with partnership

Meinhard, Gibbs- duty of loyalty breaches

RUPA § 409c - Partners owe Duty of Care

prohibits gross negligence, recklessness, intentional misconduct, or knowing violation of the law

ordinary negligence = shared losses (dont want to punish for bad biz decisions)

RUPA § 409d - Partners owe Duty of Good Faith and Fair Dealing

catch all for ALL unfair/dishonest conduct. Can’t be waived.

Defenses to FD breaches

no Duty of Loyalty breach:

failed meinhard test (not in scope of partnership’s business),

didn’t use partnerships resources (no stealing)

No Duty of Care breach: conduct was ordinary negligence

No Duty of Loyalty OR Care breach: partnership agreement modified duties (can never waive Duty of GFFD)

Vechitto v Vechitto

ice cream business (partnership) lawsuit

EXTRAORDINARY acts outside the ordinary course of business (filing lawsuit for a non-litigation ice cream business) required unanimous partner consent even if getting unanimous consent was futile.

Meinhard

Partnership fiduciary duty breach example:

a partner breached the duty of loyalty by “self dealing/stealing opportunities from partnership”

when deal falls within scope of partnership’s venture, failing to give partnership FIRST DIBS = breach of duty of loyalty

To determine if opportunity falls within scope of partnership’s venture use:

Line of business test - does partnership have sufficient experience/ability in that field

Expectancy test - could the partnership reasonably expect to receive the opportunity?

Gibbs

Partnership fiduciary duty breach example:

departing partner breached the duty of loyalty by “competing against the partnership” taking confidential info to their new firm giving them a competitive advantage

Partnership Liability RUPA 305, 306

RUPA §305 – PARTNERSHIP’s Liability for Partner Acts

Partnership liable if partner’s act is in ordinary course of business OR with actual/apparent authority.

RUPA §306 – PARTNER’S personal Liability

Partners are jointly and severally liable for all partnership obligations (EACH partner can be held fully responsible for debt/harm)

Exceptions:

LLP Exception (§306c) If the partnership is an LLP, partners are not personally liable for partnership obligations.

incoming new partners not liable for partnership obligations BEFORE they joined

3rd party has agreement saying i wont hold partnership/partners liable

In re keck - post-exit partner liability

In re keck

(bc of RUPA §306 joint and several liability ) Partners REMAIN liable for acts occurring while they were partners even AFTER they leave the partnership

Forming an LLC RULLCA 201(a)

RULLCA 201(a) - An LLC is formed once:

File Charter with Sec of State

Required contents:

Name and Mailing address of LLC

Registered agent’s info

Lawful purpose (“any lawful business”)

If Charter properly filed, LLC exists, members get limited liability protection, and entity can contract, sue and be sued

Defective Formation (No Filing)

Court will still recognize impoperly filed LLC if:

De Facto Corporation Doctrine requires:

(1) statute allowing formation, (2) bona fide attempt to comply, (3) use of corporate powers

Corporation-by-estoppel prevents parties from denying the existence of a corporation if they treated a business as one. Applies when:

1) business holds itself out as a corporation

) third party relies on the existence of entity in good faith.

stone v jetmar - no filing so NO LLC. no defacto or estoppel either

stone v jetmar

Drafted charter but never filed → no LLC exists

Court rejected:

De facto doctrine (no bona fide filing attempt)

Corp by Estoppel (bad faith / misleading conduct)

Managing an LLC RULLCA 407 (DELLCA 18-402)

RULLCA § 407 – LLC Management & Voting Defaults:

Default: member-managed LLC UNLESS Operating Agreement (OA) says manager-managed.

Voting:

ordinary acts = majority of members;

extraordinary acts = unanimous consent

1 member = 1 vote (but OA can change voting rules)

If an LLC governance or voting power is disputed, check OA first; if silent, apply member-managed default + majority/unanimous split above.

Haley v. Talcott - dissolve LLC if voting is deadlocked

LLC limited liability RULLCA 304(a)

RULLCA § 304(a) (LLC Limited Liability) - Members/managers NOT personally liable for LLC debts/obligations

Exceptions:

Personal wrongdoing - harming people, violating laws

Contractual obligations - they sign a K that they’ll pay for the debts

Veil piercing - NetJets Veil Piercing 2-Prong Test

owner and business acted as Single economic entity (alter ego/ used business assets as their own).

overall element of injustice or unfairness if shield respected (fraud, misuse, illegality).

Soerries v. Dancause - allowed to pierce the corporate veil to hold the owner personally liable for patron’s death because evidence showed he commingled corporate and personal finances and disregarded the corporation’s separate legal existence

Haley v. Talcott

Court will dissolve LLC if voting is deadlocked, owners have 50/50 voting power, and OA didn’t provide a fair way to break it

Conflict between statute and LLC Operating agreement (or between 2 agreements)

Conflict b/w statutes

Taghipour More Specific provisions control > general provisions

position matters: more specific subsection controls > broader general rule

Statute vs OA

Mandatory statute “cannot be waived”, “shall”, “notwithstanding OA” → statute controls

Default statute “unless otherwise provided in OA” → OA controls

internal disputes → OA controls (unless overridden)

Conflicts between agreements

Internal parties (members, managers, transferees) → OA controls

third parties → Charter controls

Operating Agreement (OA)

LLC’s internal contract

Like bylaws in a corporation

Private agreement among members

Governs internal management unless overridden by statute or charter-type document

Netjets

piercing the veil (member-owner was NOT protected under LLC limited liability shield and liable for entity’s debts) because, under 2 prong Pierce the Veil test:

1) he was using entitys funds as his personal funds, using LLC bank account like his own pockets = operating as single economic entity

2) he was acting in self interest to avoid tax consequences = overall element of injustice or unfairness

LLC fiduciary duties RULLCA 301(a), 409(a)

301(a) Manager-managed LLC managers owe FD to the LLC and its members. members DO NOT owe FD

409(a): Member-managed LLC members owe FD of loyalty and care to the LLC and its members

Default FD owed if OA is silent:

Duty of loyalty - no self dealing, taking LLC opps, competing against LLC, or personal benefit conflicts

Duty of care - no gross negligence, reckless conduct, intentional misconduct, knowing legal violations

Duty of good faith / fair dealing cannot be eliminated, gap-filler of anything else not covered.

Miller v. HCP - you can expressly eliminate Fiduciary duties like loyalty and care in OA

Miller v. HCP

Expressly waived broad fiduciary duties (like loyalty/care) and expressly authorized the challenged transaction structure in the OA.

Normally you can rely on ICGFFD as a contractual “Gap filler” where the OA is silent to prevent people from exploiting it in bad faith

but here there was no gap because the OA SPECIFICALLY permitted the conduct being challenged

lesson:If you contract away protections that would have protected you, courts generally will not rescue you from that bargain later because you ended up with a bad outcome in the transaction

Corporate Bylaws DGCL 109(a) (MBCA 10.20)

Bylaws DGCL §109 / MBCA 10.20 - Shareholders always can adopt, amend, or repeal bylaws.

Board can too only if charter allows (DGCL)

Board can too UNLESS charter restricts board power OR shareholders change the bylaws to restrict board’s power(MBCA).

Conflicts:

If charter amendment valid → it overrides inconsistent bylaws

If bylaw conflicts with valid charter or DGCL/MBCA→ invalid

Limits on bylaws Ca, Inc v AFSCME - bylaws can regulate procedure but not mandate substantive biz decisions or force directors to breach fiduciary duties

Corporate Charter DGCL 102(b)(7), 242(b)(1)

DGCL 102(b)(7) Charter Exculpation - Charter can state that directors/officers are NOT liable ($$) for duty of care violations

EXCEPT: Charter can NOT remove liability for duty of loyalty or GFFD breaches

basically so they don’t end up with another Van Gorkom, 102b7 lets corporations eliminate directors liability for money damages when they violate duty of care

DGCL 242(b)(1) Charter Amendment:

Board must approve amendment and send it to shareholders.

Shareholders must vote properly to approve it.

Smith v. Van Gorkom

Board breached Duty of Care by approving rushed merger vote to sell the company without being adequately informed (didn’t ask questions, didn’t get a merger agreement to read, didn’t get any docs or a real valuation to decide to sell the company at $55)

Standard applied: gross negligence = breach of Duty of Care

Result: no business judgment protection → directors personally liable

102b7 now says board/directors you still breached your duty of care but you don’t have to pay tthe corporation does.

Conflicts between Corporation Charter, By Laws, or Statutes (DGCL/MBCA)

Statute (DGCL/MBCA) → Charter → Bylaws

Charter > Bylaws

Ex. Charter amendment says “Board has 5 directors” which is now inconsistent with bylaws that say “board has 3 directors”. charter controls, bylaws are INVALID

Statute (DGCL/MBCA) > Bylaws

Ex. by law says “shareholders don’t have voting rights” vs DGCL “shareholders are required to have voting rights” → statute controls, bylaw is INVALID

Corporate directors DGCL 141(a), 141(b), 141(d), 141(e), 141(k)

DGCL §141(a) Board Management:

Board manages all corporate business and affairs.

EXCEPT: if Charter gives shareholders limited management power.

DGCL §141(b) Board Procedure:

Board must have ≥1 natural person; default set by charter/bylaws.

Board Quorum = majority of total # directors must be present (charter/by laws may change quorum but NO LESS than 1/3).

Board actions approved by majority of those present (>50% votes or it fails)

DGCL §141(d) Classified/Staggered Boards:

Charter/bylaws may create staggered/classified boards where directors are divided up into classes who each serve staggered terms; cannot all be removed at once

DGCL §141(e) Good Faith Reliance Protection:

Directors protected from liability if they rely in good faith on info, records, audits from experts

Notice & Fairness Rule (Adlerstein):

Boards must conduct affairs with minimum standards of fairness.

Board action invalid if board intentionally withheld notice from director to prevent him from using controlling voting power

DGCL §141(k) Director Removal: Stockholders may remove directors (or entire board) by majority vote, with or without cause.

Exception: classified boards usually require cause BUT charter can allow no-cause removal

cannot remove directors/board if it would violate proportional representation (aka to protect minority shareholders, you can’t remove directors they used their cumulative voting power to elect))

Capital structure DGCL 152, 157

DGCL § 152 – Issuance of Stock

Board decides what the company gets in exchange for stock (cash, property, services, etc.) and it can NOT give this power to officers

Board must approve the deal before stock is issued.

DGCL § 157 – Stock Rights / Options:

Board must approve and have a written document for any promise for stock rights or options (promise to giving someone the right to buy stock later)

Grimes v Alteon - officer making an oral promise to sell stock to sommeone is invalid, need to have board approval in a written document

Distributions MBCA 6.40

Distributions - transferring money/property (dividends, share buybacks, shareholder payouts) from corporations → shareholders

MBCA §6.40 Corporate Distributions - Board can NOT make distributions if corporation FAILS either:

Equity Insolvency Test = cannot pay debts as they come due OR

Balance Sheet Test = total assets < (total liabilities+liquidation prefs)

Defense: MBCA 6.40(d) Board can say “no this distribution IS allowed because we relied on reasonable accounting practices”

Restrictions on Distributions:

Charter may add STRICTER limits than MBCA

Charter cannot REMOVE MBCA minimum protections

bylaws are irrelevant to § 6.40 analysis

MBCA vs Delaware Law:

DE law- A corporation can only make a distribution or stock repurchase out of “surplus.”

Delaware is more flexible than MBCA 6.40: Klang v Smith - directors have reasonable latitude to depart from stale values on old balance sheets to calculate surplus (good faith/reasonable valuations)

MBCA 6.40 - more rigid, under § 6.40(d) they can also rely on reasonable accounting/valuations to rebut failure of either test but they still MUST pass BOTH the equity insolvency AND balance sheet test AFTER any valuation

Klang v Smith

DE law- A corporation can only make a distribution or stock repurchase out of “surplus.”

Klang v Smith (Delaware) -

Board approved major share repurchase during merger even though OLD balance sheet showed negative net worth

even though corp had NO surplus from their old valuations, directors were still allowed to buy buck shares using updated valuations and expert opinons to show they had sufficent surplus for the share repurchases.

Delaware is more flexible than MBCA 6.40: Klang - directors have reasonable latitude to depart from stale values on old balance sheets to calculate surplus (good faith/reasonable valuations)

MBCA 6.40 - more rigid, under § 6.40(d) they can also rely on reasonable accounting/valuations to rebut failure of either test but they still MUST pass BOTH the equity insolvency AND balance sheet test AFTER any valuation

Shareholder Voting DGCL 212(a), 214, 216, 242(b)(4) (MBCA 7.27(b))

DGCL §212(a) 1 share =1 vote default. (charter can modify)

DGCL §214 Cumulative voting shareholders can essentially pool votes but it MUST be expressly authorized in charter, its NOT a default

cumulative votes = shares × number of director seats being elected

DGCL §216

Shareholder quorum (majority of shares entitled to vote) must be present. charter or bylaws can RAISE or LOWER shareholder quorum requirement, but no less than 1/3

Director Elections: Directors are elected by a plurality (most votes wins even if its less than 50%) of the votes of the shares present

Other Matters: Most other corporate actions require majority of shares (must be >50% votes) present at the meeting

DGCL § 242(b)(4) supermajority vote protection

If a corporation’s charter requires a supermajority vote (like 60-80%) for an action, then it also requires the SAME supermajority vote to amend/remove that action/rule

MBCA § 7.27(b) – BROADER than DGCL

Any supermajority voting OR quorum requirement in charter requires same supermajority to amend/alter/repeal.

Close corporations DGCL 202, 218(c), 342

DGCL § 202 - Corp can restrict stock transfers to control who can become shareholders in a close corporation

stock transfer restrictions MUST be in the charter, bylaws, or agreement

restrictions are only enforceable if (1) clearly noted on the stock certificate OR (2) holder had actual knowledge at acquisition OR (3) there is affirmative assent after acquisition. Mere awareness, receipt, or implied notice is not enough.

Henry case

DGCL § 218 (c.) - stockholders can bypass the default "one share, one vote" rule of § 212(a) and agree in writing and sign a contract to vote their shares together instead of voting separately.

DGCL § 342 - It is a close corporation if in the charter specifically calls it a close corp and states 3 conditions:

1) Limits stock to small # of people (30 shareholders max)

2) restricts stock transfer

3) not publicly traded (can’t make a public offering of its stock)

Henry v. Phixios

corp (not a closed one) tried to revoke sharholder’s shares under stock transfer restrictions in a shareholder agreement, but the restriction was not on the stock certificate, and the company could not prove the shareholder had actual knowledge at issuance or clearly agreed later. email receipt wasn’t good enough to = assent

•Under DGCL §202, stock transfer restrictions are unenforceable unless (1) clearly noted on the certificate OR (2) holder had actual knowledge at acquisition OR (3) there is affirmative assent after acquisition. Mere awareness, receipt, or implied notice is not enough.

shareholder proposals Rule 14a-3, 14a-8, 14a-9

Governance proposals - shareholders want the company to vote on their own ideas. Can be done 2 ways:

1) Run their own proxy campaign (very expensive)

Prepare a proxy statement Rule 14a-3 - You cannot solicit a proxy unless you have given the target of the solicitation a proxy statement first

Proxy statement - like an info sheet that explains everything about the vote like who is asking for the vote, how much the campaign costs, whos paying for it, whens the shareholding meeting, what exactly is being voted on)

Soliciting - almost any communication trying to influence votes, direct or not.

2) Rule 14a-8 - allows shareholders to have their proposals included in the company’s Proxy Statement (Much Easier/cheaper)

The company prints it, sends it, and pays the costs

but to submit a proposal you must: Own $2,000 of stock (or 1%) and hold it for at least 1 year prior to submission date

1 proposal per meeting per shareholder max

Proposal Limits: company can exclude the proposal if its if it falls under one of 13 substantive categories, most notably if it is improper under state law or violates the law (a bunch of other reasons too, these are most crucial).

If company thinks the proposal falls in one of these limits, has to 1st get SEC approval/request a no-action letter before excluding the proposal

No Lying (Rule 14a-9) - you can’t make false statemens/ mislead shareholders or omit material facts in a proxy statement

“material fact” is a fact “a reasonable shareholder would consider important in deciding how to vote”

Conflicts of interest DGCL 144

under delaware law, when theres a conflict of interest (like duty of loyalty beach) deal isnt automatically void yet but its under scrutiny unless its properly cleansed

DGCL §144 – Interested Director Transactions (Safe Harbor) - Conflicted director transaction (director personally benefits bc he is on both sides of the deal) is NOT void/voidable if cleansed by statutory safe harbor or proven entirely fair.

Safe harbors: (i) disinterested director approval, (ii) disinterested stockholder approval, or (iii) entire fairness review satisfied.

Disinterested Director Approval (§144(a)(1)):

If the conflict is fully disclosed and the majority of the disinterested directors approve it in good faith.

Disinterested directors must be informed and independent (not conflicted, theyre neutral and unbiased).

OR

Disinterested Shareholder Approval (§144(a)(2)):

if fully informed, uncoerced (VOLUNTARY) majority of disinterested shareholders approve then conflict is OK

Must include material facts

gantler - disinterested shareholder approval didn’t work here because they board gave them misleading disclosures (weren’t fully informed - board told the shareholders they “Carefully considered” but didnt seriously consider and no real process) and the vote was legally required so it wasn’t fully voluntary (coerced)

OR

if you dont get disinterested director approval OR disinterested stockholder approval, court will say okay prove this conflict deal was still fair then:

Entire Fairness Standard - Conflicted transaction is valid only if BOTH fair dealing + fair price are proven.

Fair dealing = was deal negotiated fairly? was it rushed? was it controlled by the conflicted person?

Fair price = was the deal economically reasonably and objectively fair?

valeant - entire fairness review. executives set up unfair system where they got huge bonuses because unfair dealing (the people decidiing the bonuses got bonuses too) and unfair price (too high, based on inflated #s) so directors had to pay back bonuses

Derivative Litigation - DE Chancery Rule 23.1 (MBCA 7.42)

Derivative Litigation:

Shareholder sues on behalf of corporation to force corp to sue directors; corp sues directors; recovery goes to corp.

Shareholder may get attorney’s fees if suit succeeds.

Demand Requirement - Have to ask the board to fix issue before suing directors in derivative suit. 2 ways to satisfy demand requirement to get to derivative litigation:

Wrongful refusal - shareholder makes the demand and board rejects request

Demand futility - Demand can be excused bc directors are incapable of making an impartial decision *** most relevant . (aronson)

Delaware Chancery Rule 23.1 - Requirements to bring a Derivative Suit (incentivizes only meritorious claims)

1. Contemporaneous ownership (shareholder can only bring suit if they owned shares at the time of the harm)

2. Court must approve any settlement

3. Demand requirement (shareholders must have written demand that directors take action first)

4. Standing requirement (must remain shareholders during the litigation)

MBCA § 7.42 (Universal Demand Rule)

Shareholder must ALWAYS make written demand before suing.

Must wait 90 days unless rejection or irreparable harm.

Aronson

Shareholders think directors did something shady, but before they can file a derivative lawsuit on behalf of the company forcing the corp to sue the shady directors the law say “did you ask the board to fix it first?”= demand requirement

In Aronson, they argued it was useless to ask the board first but court said NO demand was not futile, heres a test to check if Demand is excused for futility:

1) If there is reasonable doubt that the directors are impartial/ disinterested and independent (aka i have some doubts i think theyre biased, im not going to ask a compromised board) OR

2) The decision they made is so irrational that the business judgment rule isn’t valid

Direct vs Derivate Suit

Shareholder Litigation: Direct/Derivative Suits

Direct claim ONLY impacts shareholder filing suit in a way that is different from others

Derivative claim impacts EVERY shareholder

Direct claim ONLY impacts shareholder filing suit in a way that is different from others

Derivative claim impacts EVERY shareholder

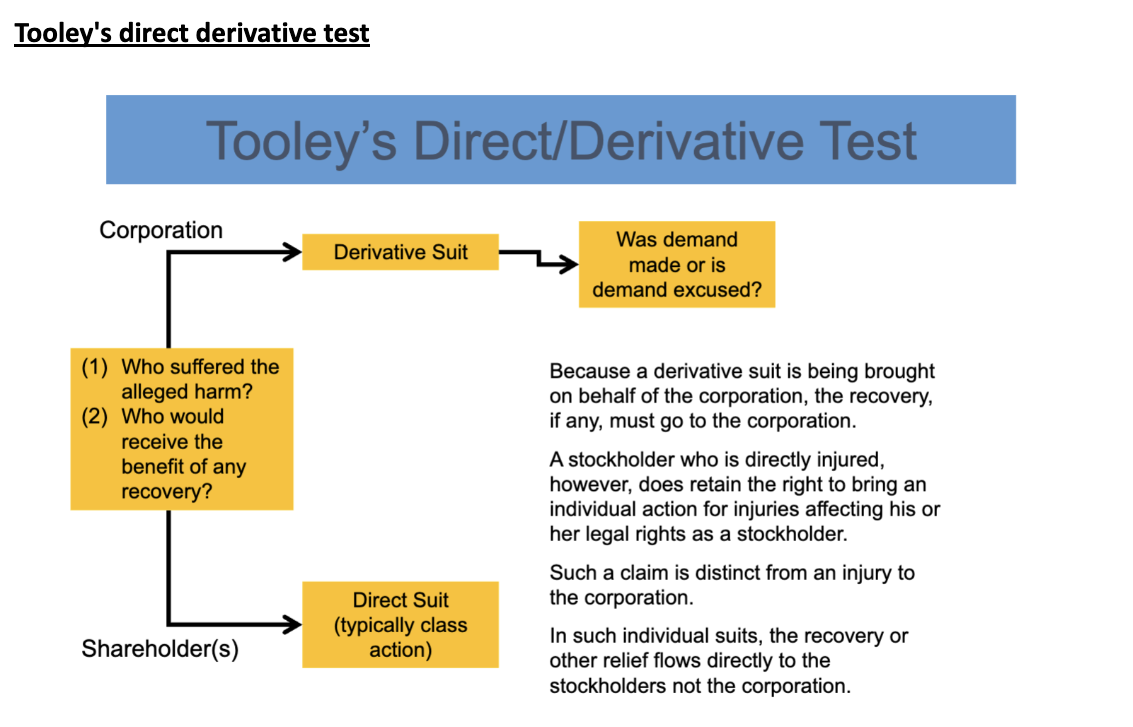

Tooley

Rule: whether a shareholder claim is direct or derivative depends only on who suffered the alleged harm and who would receive the benefit of recovery.

derivative = the harm is to the corporation or shared equally by all shareholders,

direct - the injury is unique to the suing shareholder and the remedy flows directly to them

facts:

Minority shareholders sued after a merger was delayed and took 22-days to close.

They claimed they lost the time-value of money (the idea that money is worth more the sooner you receive it because it can be invested and grow).

but their right to receive the merger price had not yet “ripened” (not fully due yet) meaning they were not yet clearly entitled to immediate payment when the delay happened.

The alleged harm (delay/overpayment-type value loss) affected all shareholders equally in the merger context, not a uniquely targeted group = derivative

Exam use:

This is a classic derivative situation

Beam v stewart

The board had 6 directors, and plaintiff argued demand was futile because several directors had close personal friendships and social relationships with controlling shareholder Martha Stewart (including attending events and long-term social ties).

Stewart allegedly held overwhelming voting power (~94%) and one director had previously done a favor (contacting a publisher at Stewart’s request), but there were no specific facts showing coercion or control over decision-making.

rule: pre-suit demand is not excused where a shareholder relies on friendship, social ties, or a controlling shareholder’s influence alone, because independence is rebutted only by particularized facts showing directors are actually beholden or unable to exercise independent judgment.

exam

distinguish it when facts show something stronger than Beam— a director is financially dependent, repeatedly follows controller instructions, or faces credible retaliation, because Beam says mere social connection isnt enough to produce bias

Duty of Oversight/ BJR Cases: Stone, Murchand, Caremark, Disney

Business Judgment Rule (BJR) protects directors from duty of care breach liability as long as they acted informed and in good faith—they weren’t careless on purpose.

The exculpation clause (DGCL §102(b)(7)) meant directors couldn’t be sued for money damages just for mistakes in duty of care.

duty of oversight - directors have a duty to try in good faith to assure a reasonable information and reporting system exists..

In re Caremark - HAD a functioning compliance system, didnt violate duty of oversight

Caremark Standard: Directors breach the duty of oversight ONLY if there is an utter failure to implement ANY compliance system or a sustained failure to monitor it in good faith.

facts

Employees violated federal healthcare laws through improper referrals.

Board had a compliance program and reporting structure in place.

Violations occurred despite the system, but there was no evidence the board ignored known problems or lacked oversight entirely.

Exam use

This is an extremely HIGH standard. Even with violations, directors are protected if they made a good-faith effort to build monitoring systems.

BJR/oversight - protected → acted in good faith, functioning compliance system, even if employees still made mistakes

Exculpation Clause - no director liability

Stone v. Ritter HAD a functioning compliance system, didnt violate duty of oversight

rule: Directors are only liable for compliance failures if they act with bad faith, intentional misconduct, or knowingly break the law, not just because a decision costs a lot or looks dumb in hindsight.

facts

Bank employees violated a federal statute by failing to file required reports, but directors were unaware of it.

The board had an internal compliance system (policies, reporting system, and periodic compliance reports).

No “red flags” reached the board showing ongoing violations or systemic breakdown.

Exam use

BJR/oversight - protected → acted in good faith, functioning compliance system, board didnt know of the red flags even if employees still made mistakes

Exculpation Clause - no director liability

Marchand v. Barnhill - COMPLETELY IGNORED monitoring system, BREACHED duty of oversight

rule: When a company faces a mission-critical risk, directors must make a good-faith effort to create board-level monitoring systems for that specific risk.

facts

Blue Bell ice cream had a deadly listeria outbreak that shut down the company.

The board had no food safety committee, no regular reporting system, and no structured oversight of food safety.

Management knew of food safety issues (“red flags”), but the board was not informed.

Exam use

Much stronger Caremark claim than Stone/Caremark because there was no meaningful board-level system for a core risk.

BJR - likely not protected, didnt act in good faith to monitor red flags and NO reporting/oversight system

exculpation clause - since they potentially breached duty of care, directors might not be shielded from liability

duty of oversight - consciously ignored, no system in place

In re Walt Disney Co. (bad business decision, sloppy approval process but informed and in good faith so OK)

rule: Directors are not liable for duty of care breach for bad decision of approving huge executive compensation unless they act in bad faith, meaning a conscious disregard of their duties—not just poor judgment or sloppy process.

facts

Ovitz was president of disney. Disney’s board approved a very large severance payout (~$130–140 million) when he was fired early.

The approval process was described as informal and “sloppy,” but directors did review materials and discussed the decision over time.

Ovitz failed in the role, but there was no evidence the board intentionally ignored its duties or tried to harm the company.

BJR - applies. maybe a bad decision to hire him since he sucked, but was informed and in good faith so protected. not careless on purpose

exculpation - no director liability for duty of care mistakes

Duty of care/ Business Judgment Rule (BJR) exam steps

Business Judgment Rule (BJR) protects directors from duty of care breach liability as long as they acted informed and in good faith—they weren’t careless on purpose.

Duty of care = gross negligence standard

Plaintiff rebuts BJR defense by showing gross negligence

mainly you don’t get BJR protection if you acted careless in bad faith (consciously ignored red flags) or made totally uninformed decisions

compare to van gorkum - NO BJR, directors LIABLE because they approved a major corporate decision without being reasonably informed and without proper investigation.

gagliardi - bjr protection (no conflict of interest, bad biz decision but no bad faith)

apply exculpation clause (DGCL §102(b)(7)) meant directors couldn’t be sued for money damages just for mistakes in duty of care BUT they can be liable if they acted in bad faith OR violated duty of loyalty/duty of oversight (no oversight system)

Ebay

board can’t use defensive tactics like poison pills or share dilution to fight off a shareholder they dislike who isn’t actually trying to takeover

eBay owned part of craigslist and had some control rights, but craigslist leaders wanted to keep the site “community-based” and not focused on profit, creating a conflict between shareholder profit and personal mission goals.

craigslist leaders used a poison pill (stops outsiders from buying more stock), staggered board (makes it harder to remove directors), and share dilution (reduces eBay’s ownership) mainly to block eBay, not because of a real takeover.

Gagliardi v. TriFoods International, Inc

BJR rule: Courts will not second-guess directors’ business decisions if they acted in good faith, without conflicts, and with a rational business purpose—even if the decision turns out badly.

Shareholder challenged a series of poor business decisions (e.g., bad expansion, overpaying, bad strategy),

Court applied BJR - said it showed no conflict of interest ) or bad faith .

No facts showed corporate waste (decision so irrational that no reasonable business could justify it) or self-dealing, so courts refused to intervene.

Van Gorkam

rule: Directors lose BJR protection and can be liable if they approve a major corporate decision without being reasonably informed and without proper investigation.

CEO proposed selling the company at an arbitrary price (no real valuation process), and the board approved it after a short meeting with no documents, no preparation, and no meaningful review of financial information.

→ shows lack of informed decision-making

Court found gross negligence so the BJR did not apply.

AFSCME

by laws can regulate PROCEDURE (like changing corp election procedures) not substantive biz decisions(cant override boards management power) OR forced directors to breach fiduciary duties

Shareholders proposed a bylaw requiring the company to reimburse proxy fight expenses for certain shareholder nominees → court said this was mostly procedural so it OK

But bylaws also required reimbursement even when doing so would breach directors’ fiduciary duties conflicting with DGCL §141(a) = NOT ok

Third Point LLC v. Ruprecht

A board can use a poison pill or similar defense against activist shareholders if board reasonably believes they threaten the company and the defense isn’t SO EXTREME it block shareholders from still using other methods (like voting or proxy fights) to challenge management

Activist hedge fund was rapidly buying shares and could gain creeping control which the board reasonably saw as a threat.

Board had a strong independent board (mostly outside directors), used expert legal/financial advisors, and acted in good faith (informed, protective purpose rather than self-interest).

Poison pill was not coercive (forcing shareholders) or preclusive (completely blocking challenges) because activists could still run a proxy contest.

Exam trigger: Use this when a board adopts takeover defenses (especially a poison pill) against activists or hostile investors.

ask whether the board had a reasonable threat perception under Unocal and whether the response was proportionate rather than completely blocking shareholder power.

but only apply it if actually defensive

Takeovers/Poison Pills

A merger of two companies (or acquisition of one by the other) where both boards support combo business = a friendly takeover

hostile takeover one company tries to get control over another accompany without board approval from the target company

Activist Investor

A shareholder (often hedge fund or large investor) who buys enough stock to influence company decisions.

Wants changes like selling the company, replacing directors, cutting costs, or changing strategy.

Defensive Measures

Poison Pill = gives existing shareholders (except the hostile buyer) the right to buy additional shares at a discount if a buyer (aka hostile buyer) acquires more than a set percentage of stock (like 10–20%).

issuing more shares dilutes the hostile buyer’s ownership, makes the takeover much more expensive (has to buy more shares to get power back) and pressures the buyer to negotiate with the board instead of taking control directly.

A pill can always be waived or amended by the directors

Staggered Board = only some directors can be replaced each years

Unocal Test = For defensive measures:

Board must reasonably believe takeover threatens company.

Defense must be proportional (not overly extreme to wear it completely blocks shareholders from still using other methods (like voting or proxy fights) to challenge board power)

Salamone

A shareholder voting agreement is basically a private contract where shareholders agree in advance on how they will vote their shares on certain company decisions.

rule: When a shareholder voting agreement is unclear, courts treat it like a contract and will not assume the parties meant to limit normal majority voting power unless the agreement clearly and convincingly says so.

Ambiguous voting language (“majority of the holders”) could mean either people or shares, so the court looked at the whole contract structure instead of one phrase alone.

Default majority control (normal rule = more shares usually means more power) stays in place unless there is clear and convincing evidence (strong proof) that the parties intentionally changed it.

Exam trigger: Use this when shareholders fight over an unclear voting/control agreement. argue that unclear terms are read to preserve default majority voting unless the contract clearly restricts it

inside vs independent directors

Inside directors - full time employee of the company. CEO always one. Sometimes also Chair of the board. After 2008 recession, new fed regulations introduced encouraged publically traded companies to separate chair and CEO. If you didn’t you had to explain why it made sense for one person to serve as both.

Independent directors - outside directors, but not all outside directors are independent. If they receive any fees for their services they are not independent.