Econ Exam #3

1/223

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

224 Terms

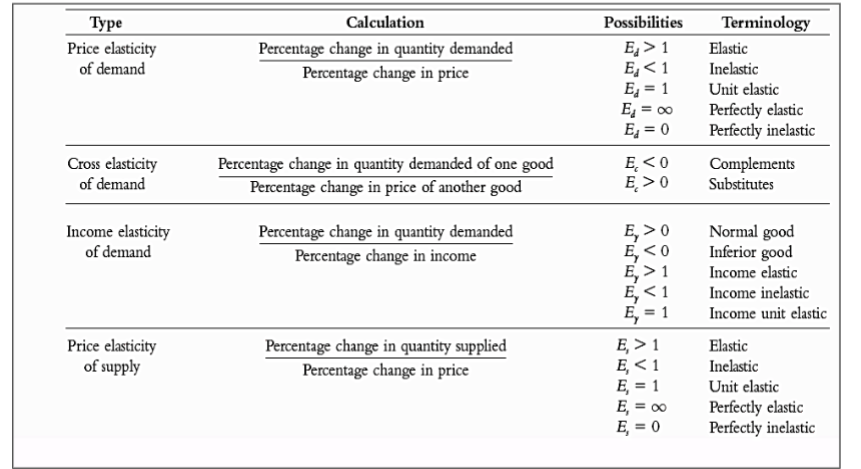

the law of demand and price elasticity

The law of demand states that price and quantity demanded are inversely related, ceteris paribus

But it doesn't tell us by what % the quantity demanded changes as price changes

Suppose price rises by 10%. As a result, quantity demanded falls.

elasticity

The general concept of elasticity provides a technique for estimating the response of one variable to changes in another. It has numerous applications in economics.

Price Elasticity of Demand (Consumers)

A measure of the responsiveness of quantity demanded to changes in price.

elasticity is not slope

for a linear demand function (straight line) slope is constant

elasticity (Ed) changes along the demand curve

calculating price elasticity of demand

identify two points on a demand curve

when calculating price elasticity of demand, we use the average of the two quantities demanded

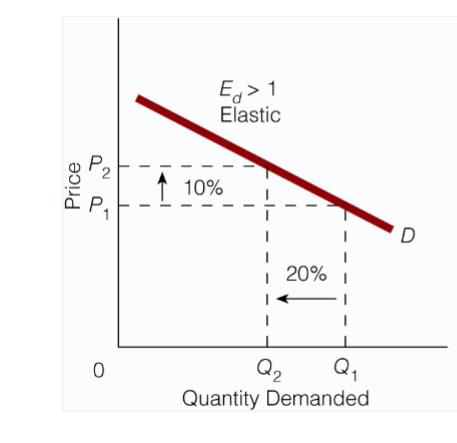

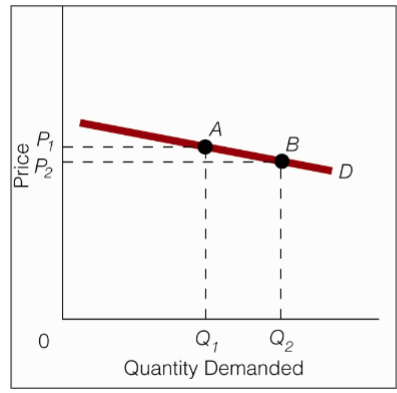

graphical representation of price elastic demand

the % change in quantity demanded is greater than the % change in price

quantity demanded changes proportionately more than price changes

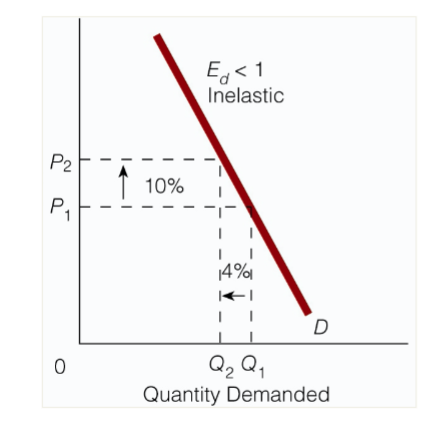

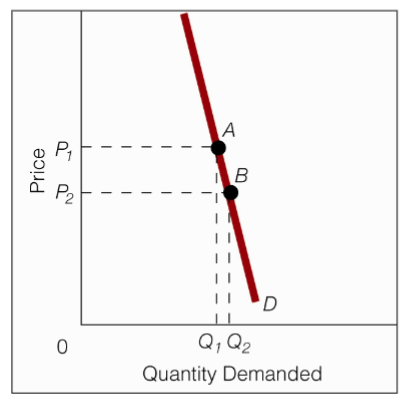

graphical representation of price inelastic demand

the % change in quantity demanded is less than the % change in price

quantity demanded changes proportionately less than price changes

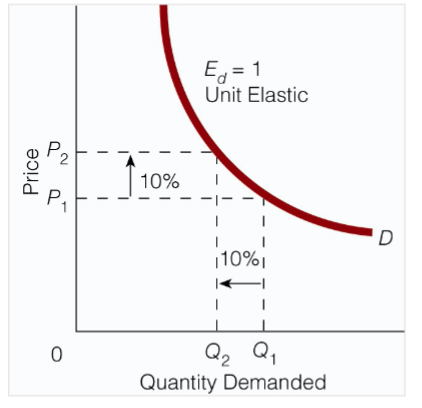

graphical representation of price unitary elastic demand

the % change in quantity demanded is equal to the % change in price

quantity demanded changes proportionately to price changes

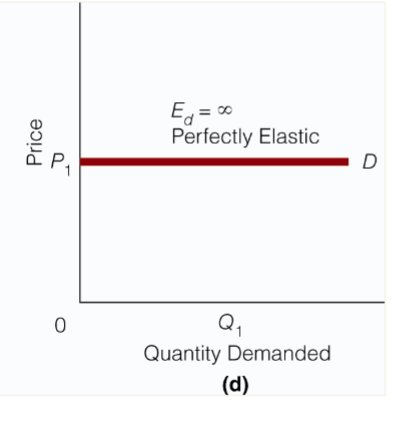

graphical representation of perfectly elastic demand

a small % change in price causes an extremely large % change in quantity demanded (from buying all to buying nothing)

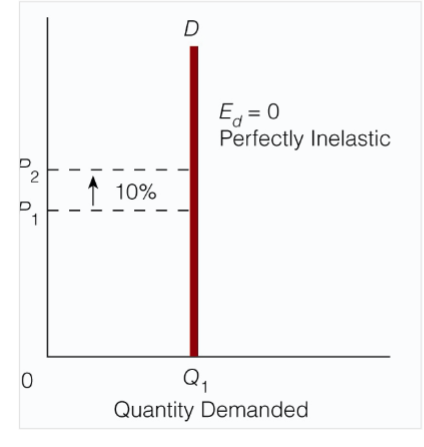

graphical representation of perfectly price inelastic demand

quantity demanded doesn’t change as price changes

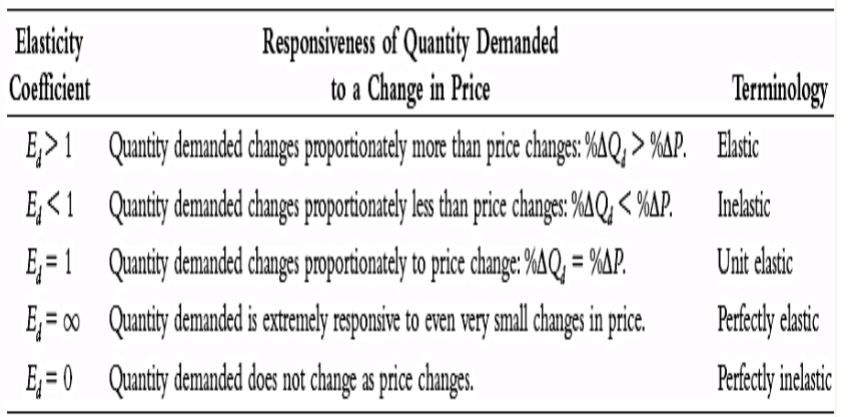

price elasticity of demand summary

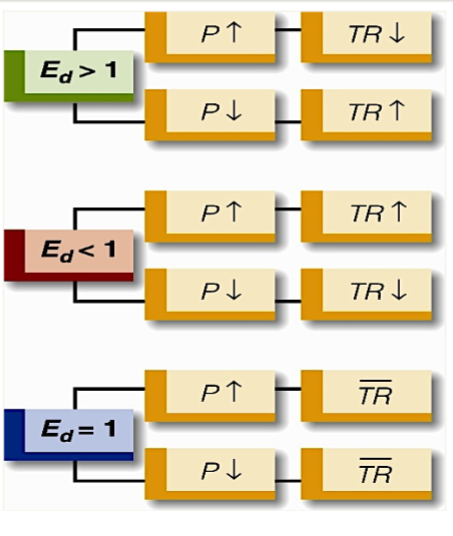

price elasticity and total revenue

total revenue (TR): of seller equals the price of a good times the quantity of the good sold (PxQ)

elastic demand and total revenue

if demand is elastic, the % change in quantity demanded is greater than the % change in price

when demand is elastic, price and total revenue are inversely related

inelastic demand and total revenue

if demand is inelastic, the % change in quantity demanded is less than the % change in price

when demand is inelastic, price and total revenue are directly related

unit elastic demand and total revenue

if demand is unit elastic, the % change in quantity demanded is equal to the % change in price

elasticity, price changes, and total revenue

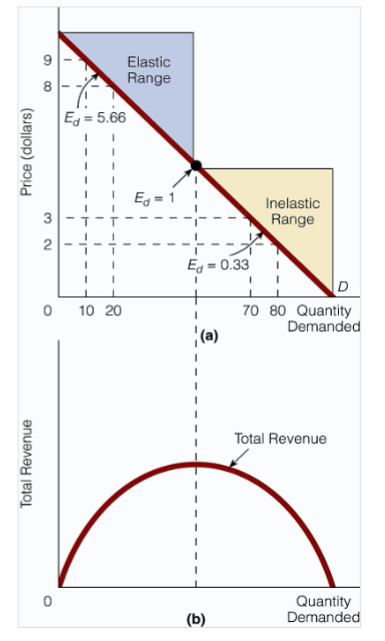

price elasticity of demand along a straight-line demand curve

In (a), the price elasticity of demand varies along the straight-line downward-sloping demand curve.

There is an elastic range to the curve (where Ed > 1) and an inelastic range (where Ed < 1).

At the midpoint of any straight-line downward-sloping demand curve, price elasticity of demand is equal to 1 (Ed = 1)

Part (b) shows that in the elastic range of the demand curve, total revenue rises as price is lowered. I

In the inelastic range of the demand curve, further price declines result in declining total revenue.

Total revenue reaches its peak when price elasticity of demand equals 1.

detriments of price elasticity

# of substitutes

necessities versus luxuries

% of ones budget spent on the good

time

number of substitutes

the more substitutes for a good, the higher the price elasticity of demand; fewer substitutes for a good, the lower the price elasticity of demand

necessities versus luxuries

generally, the more that a good is considered a luxury (a good that we can do without) rather than a necessity (a good that we can’t do without), the higher the price elasticity of demand

% of ones budget spent on the good

the greater the % of one’s budget that goes to purchase a good, the higher the price elasticity of demand; the smaller the % of one’s budget that goes to purchase a good, the lower the price elasticity of demand

time

the more time that passes (since the price change), the higher the price elasticity of demand for the good; the less time that passes, the lower the price elasticity of demand for the good

cross elasticity of demand

measures the responsiveness in quantity demanded for one good to changes in the price of another

ex: hot dogs and ketchup/mustard are complements

ex: hot gods and burgers are substitutes

income elasticity of demand

measures the responsiveness of quantity demanded to changes in income

income elastic: the % change in quantity demanded of a good is greater than the % change in income

income inelastic: the % change in quantity demanded of a good is less than the % change in income

income unit elastic: the % change in quantity demanded of a good is equal to the % change in income

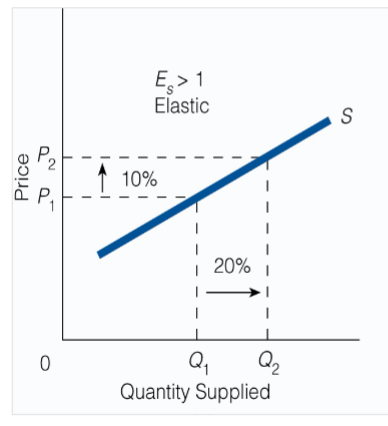

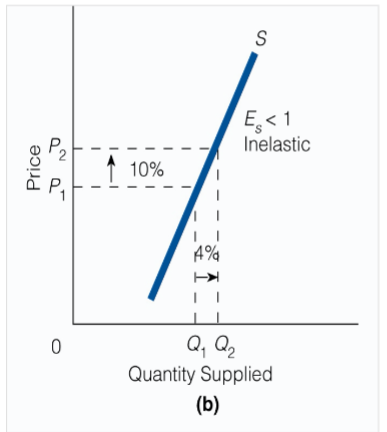

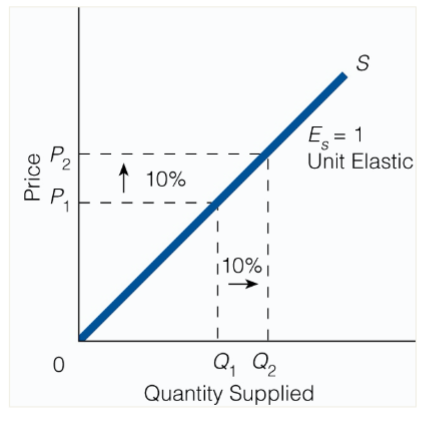

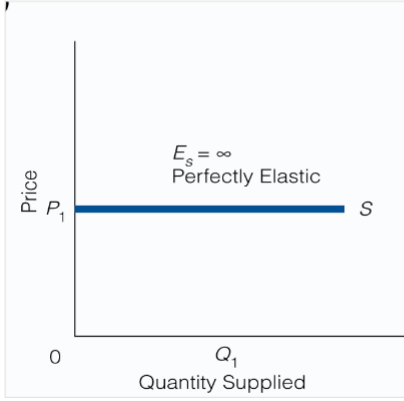

price elasticity of supply

measures the responsiveness of quantity supplied to changes in price

graphical representation of elastic supply

The percentage change in quantity supplied is greater than the percentage change in price: Es > 1 and supply is elastic.

graphical representation of inelastic supply

The percentage change in quantity supplied is less than the percentage change in price: Es < 1 and supply is inelastic.

graphical representation of unit elastic supply

The percentage change in quantity supplied is equal to the percentage change in price: Es = 1 and supply is unit elastic.

graphical representation of perfectly elastic supply

A small change in price changes quantity supplied by an infinite amount: Es = ∞ and supply is perfectly elastic.

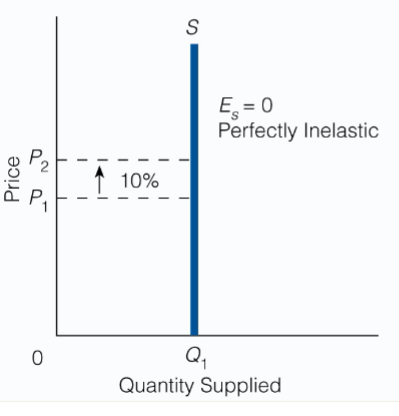

price elastic graphical representation of supply

A change in price does not change quantity supplied: Es = 0 and supply is perfectly inelastic.

price elasticity of supply and time

The longer the period of adjustment is to a change in price, the higher the price elasticity of supply will be.

This refers to goods whose quantity supplied can increase with time, a characteristic of most goods. The obvious reason is that additional production takes time.

It does not, however, cover instances when additional production may be impossible, say, original Picasso paintings.

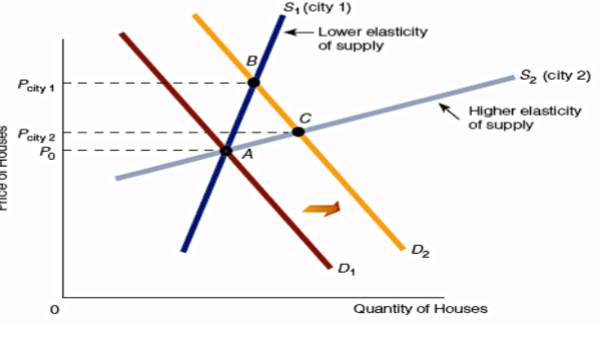

housing prices and elasticity of supply

S1 rep resents the supply of housing in city 1, and S2 represents the supply of housing in city 2.

S1 has lower elasticity of supply than S2.

Suppose the demand for housing in each city rises from D1 to D2. As a result, the price of houses rises in both cities, but it rises by more in city 1 than city 2. In other words, the lower the elasticity of supply, the greater the increase in price.

summary of the four elasticity concepts

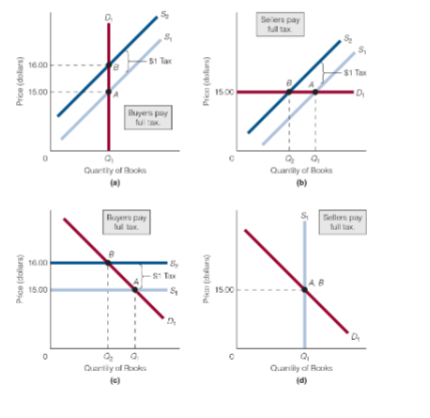

elasticity and the tax

utility theory

Utility is a measure of the satisfaction, happiness, or benefit that results from the consumption of a good

A UTIL is an artificial construct used to measure utility

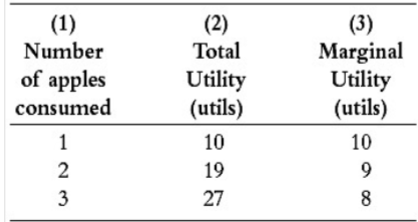

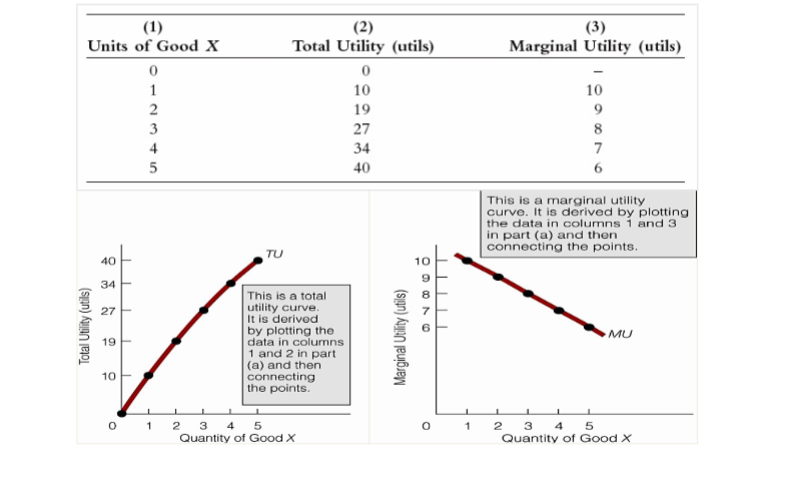

Total utility is the total satisfaction a person receives from consuming a particular quantity of a good

Marginal utility is the additional utility a person receives from consuming an additional unit of a particular good

law of diminishing marginal utility

The marginal utility gained by consuming equal successive units of a good will decline as the amount consumed increases

The total utility of something can be rising as the marginal utility of that something is falling

total utility, marginal utility, and the law of diminishing marginal utility

Both total utility and marginal utility are expressed in utils

Marginal utility is the change in total utility divided by the change in the quantity consumed of the good

law of diminishing marginal utility- application

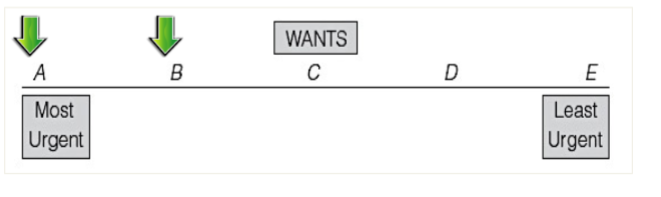

the law of diminishing marginal utility is based on the idea that if a good has a variety of uses but only 1 unit of the good is available, then the consumer will use the first unit to satisfy his or her most urgent want

if 2 units are available, the consumer will use the second unit to satisfy a less urgent want

interpersonal utility comparison

Comparing the utility of one person receives from a good, service, or activity with the utility another person receives from the same good, service, or activity

no interpersonal utility comparison

Caution: the utility obtained by one person cannot be scientifically or objectively compared with the utility obtained from the same thing by another person bc utility is subjective

consumer equilibrium

The analysis is based on the assumption that individuals seek to maximize utility

Occurs when the consumer has spent all income and the marginal utilities per dollar spent on each good purchased are equal

Where the letters A-Z represent all the goods a person buys

marginal utility analysis and the law of demand

Marginal utility analysis can be used to illustrate the law of demand, which states that price and quantity demanded are inversely related, ceteris paribus.

Starting from consumer equilibrium in a world containing only two goods, A and B, a fall in the price of A will cause MUA /PA to be greater than MUB /PB.

As a result, the consumer will purchase more of good A to restore herself to equilibrium.

marginal utility analysis and the law of demand

Marginal utility analysis can be used to illustrate the law of demand, which states that price and quantity demanded are inversely related, ceteris paribus.

Starting from consumer equilibrium in a world containing only two goods, A and B, a fall in the price of A will cause MUA /PA to be greater than MUB /PB.

As a result, the consumer will purchase more of good A to restore herself to equilibrium.

diamond-water paradox

The paradox: Water is cheap, and diamonds are expensive!

The observation that things that have the greatest value in use sometimes have little value in exchange and things that have little value in use sometimes have the greatest value in exchange.

How can this be explained???

Utility theory provides a solution!

diamond-water paradox resolved

The total utility of water is high because water is extremely useful.

The total utility of diamonds is low in comparison because diamonds are not as useful as water.

The marginal utility of water is low because water is so plentiful that people end up consuming it at low marginal utility.

The marginal utility of diamonds is high because diamonds are so scarce that people end up consuming them at high marginal utility.

Do prices reflect total or marginal utility? Marginal utility.

behavioral economics

Behavioral economists argue that some human behavior doesn't fit neatly- at a minimum, easily- into the traditional economic framework

Behavioral economists believe they have identified human behaviors that are inconsistent with the model of men and women as rational, self-interested, and consistent

these behaviors include the following

Individuals are willing to spend some money to lower the incomes of others even if it means their incomes will be lowered

Individuals don't always treat $1 as $1; some dollars seem to be treated differently from other dollars

Individuals sometimes value a good more if it is theirs than if it isn't theirs and they are seeking to acquire it (endowment effect)

business firm

An entity that employs factors of production (resources) to produce goods and services to be sold to consumers, other firms, or the government

Supply side

market coordination- invisible hand

The process in which individuals perform tasks, such as producing certain quantities of goods, based on changes in market forces, such as supply, demand, and price

managerial coordination and business firms- visible hand

The process in which managers direct employees to perform certain tasks

why do business firms arise in the first place?

Firms are formed when benefits can be obtained from individuals working as a team

Efficiency of working together

Sum of team production > sum of individual production

problem of and solutions for “team” work

problem: shirking- the behavior of a worker who is putting forth less than the agreed to effort

solution: monitor- person (manager) in a business firm who coordinates team production and reduces shirking

problem: monitor shirking

solution: make the monitor a residual claimants- persons who share the profits of a business firm

the efficiency wage theory (above-market wage will reduce shirking)

human resource management

why firms exist as an alternative to having a separate contract with each factor of production- Ronald Coase

“The costs of negotiating and concluding a separate contract for each exchange transaction which takes place on a market must also be taken into account. . . .

It is true that contracts are not eliminated when there is a firm, but they are greatly reduced. A factor of production (or the owner thereof) does not have to make a series of contracts as would be necessary, of course, if this co-operation were a direct result of the working of the price mechanism. For this series of contracts is substituted one.

At this state, it is important to note the character of the contract into which a factor enters that is employed within a firm. The contract is one whereby the factor [the employee], for a certain remuneration (which may be fixed or fluctuating), agrees to obey the directions of an entrepreneur within certain limits.” Ronald Coase

markets: inside and outside the firm

economics is largely about trades or exchanges; it’s about market transactions

in supply-and-demand analysis, the exchanges are btw buyers of goods and services and sellers of goods and services

in the theory of the firm, the exchanges take place at two levels:

(1) at the level of individuals coming together to form a team

(2) at the level of workers choosing a monitor

employees submit to the monitor’s commands because they realize that only a well-known team will yield the benefits they desire

firm’s objective: maximizing profit

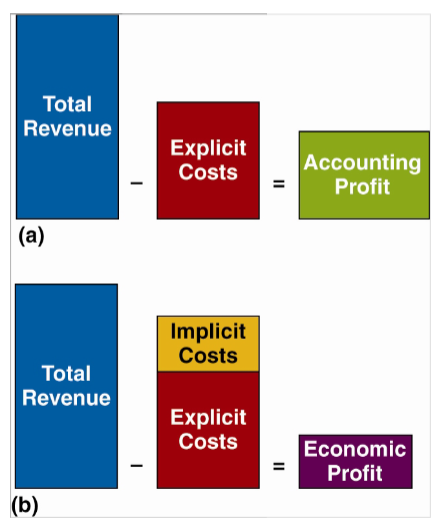

The difference btw total revenue and total cost

explicit and implicit cost

explicit cost- a cost incurred when an actual (monetary) payment is made

implicit cost- a cost that represents the value of resources used in production for which no actual (monetary) payment is made (opportunity cost)

accounting, economic, and normal profit

Accounting profit: the diff btw total revenue and explicit costs

Economic profit: the diff btw total revenue and total cost, including both explicit and implicit costs

Normal profit: zero economic profit. A firm that earns normal profit is earning revenue equal to its total cost (explicit plus implicit costs). This is the level of profit necessary to keep resources employed in that particular firm

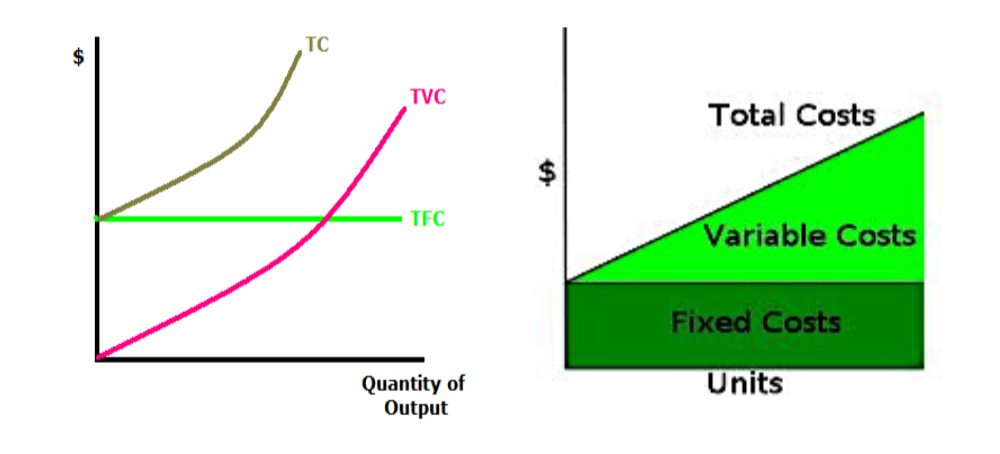

production and cost: fixed and variable inputs

Production is a transformation of resources or inputs into goods and services

Fixed input: an input whose quantity cannot be changed as output changes

Variable input: an input whose quantity can be changed as output changes

production and cost: short and long run

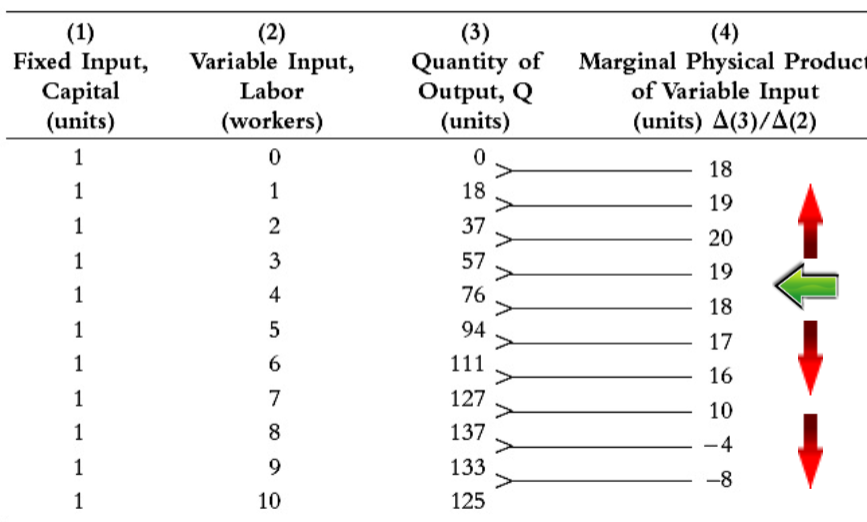

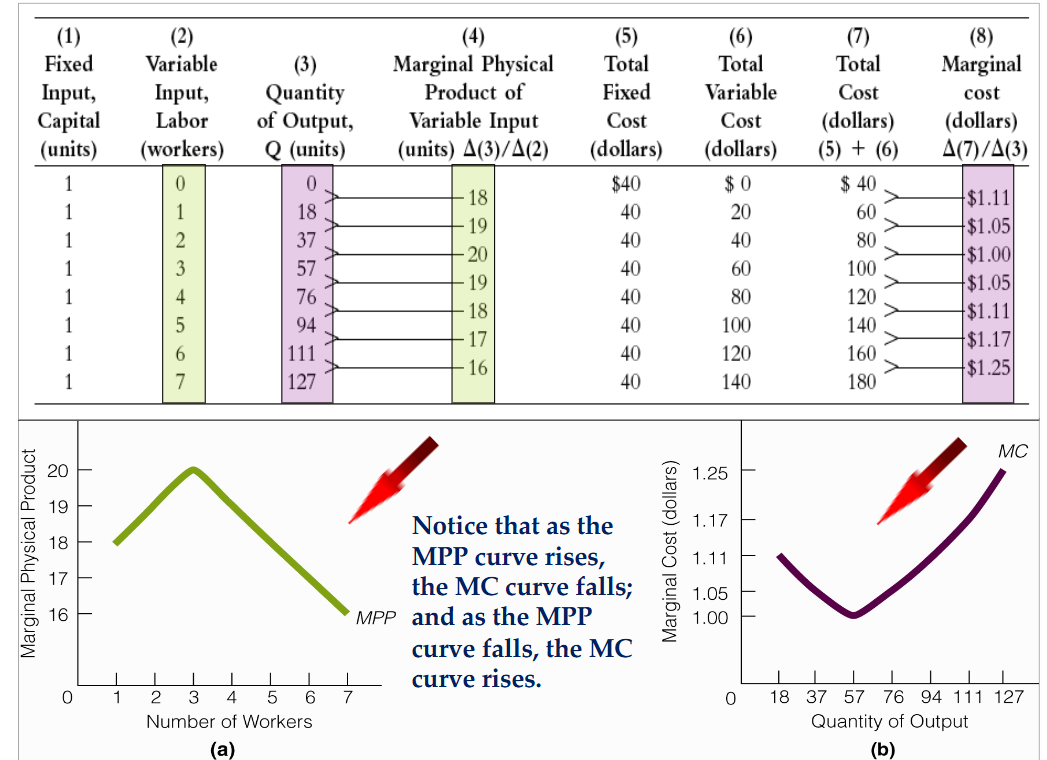

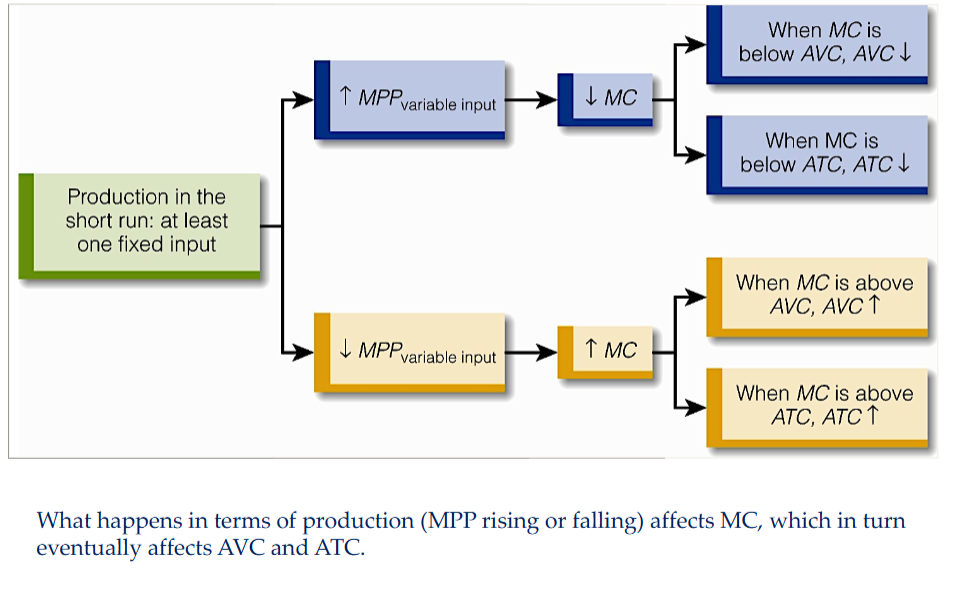

marginal physical product (MPP)

The change in output that results from changing the variable input by one unit, holding all other inputs fixed

production in the short run and the law of diminishing marginal returns

In the short run, as additional units of variable input are added to fixed input, the marginal physical product of the variable may increase at first

Eventually, the marginal physical product of the variable input decreases

The point at which marginal physical product decreases is the point at which diminishing marginal returns have set in

law of diminishing marginal returns

As ever-larger amounts of a variable input are combined with fixed inputs, eventually, the marginal physical product of the variable input will decline

production in the short run and the law of diminishing marginal productivity

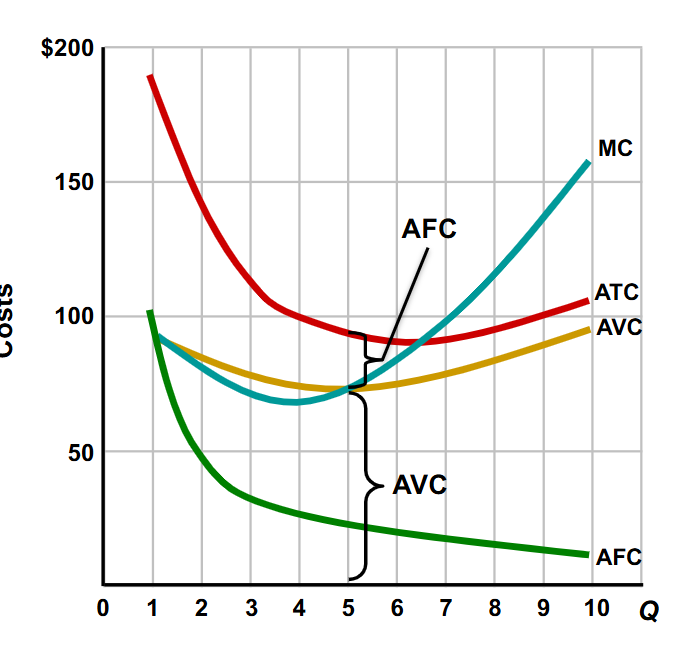

fixed, variable, total, and marginal cost

Fixed costs (FC): costs that do not vary with output; the costs associated with fixed inputs

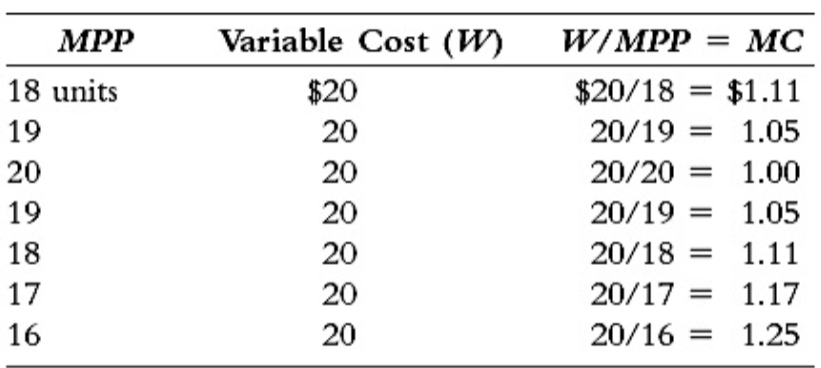

Variable cost (VC): costs that vary with output; the costs associated with variable inputs

Total cost (TC): the sum of fixed costs and variable costs. TC = TFC + TVC

Marginal cost (MC): the change in total cost that results from a change in output

marginal physical product and marginal cost

how MPP affects MC

average productivity

When the news media uses the word productivity, it is usually referring to average physical product instead of marginal physical product

To illustrate the difference, suppose 1 worker can produce 10 units of output a day and 2 workers can produce 18 units of output a day.

Marginal physical product is 8 units (MPP of labor = ∆Q / ∆L). Average physical product, which is output divided by quantity of labor is equal to 9 units.

labor productivity

Labor productivity is used in newspapers and in gov docs, it refers to the average (physical) productivity of labor on an hourly basis

By computing the average productivity of labor for diff countries and noting the annual % changes we can compare labor productivity btw and within countries

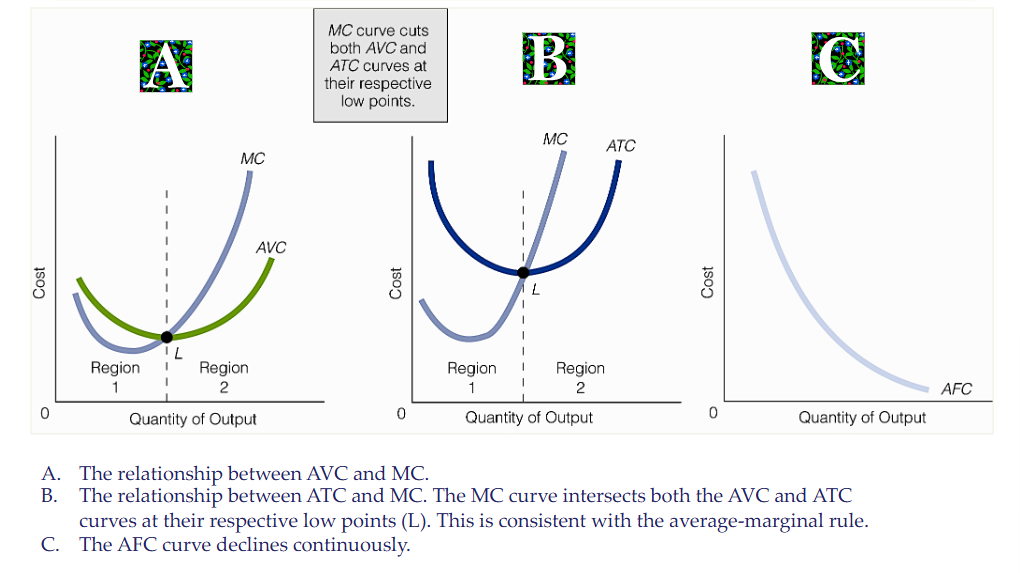

average fixed, variable, and total cost

Average fixed cost (AFC): total fixed cost divided by quantity of output

Average variable cost (AVC): total variable cost divided by quantity of output

Average total cost (ATC) or Unit Cost: total cost divided by quantity of output

average-marginal rule

When the marginal magnitude is below the average magnitude, the average magnitude falls

When the marginal magnitude is above the average magnitude, the average magnitude rises

average and marginal cost curves

tying short-run production to costs

sunk cost

A cost incurred in the past that cannot be changed by current decisions and therefore cannot be recovered

Economists advise individuals to ignore sunk costs

production and costs in the long run

In the short run, there are fixed costs and variable costs; therefore, total cost is the sum of the two

A period of time in which all inputs in the production process can be varied (no inputs are fixed). In the long run, there are no fixed costs, so variable costs are total costs

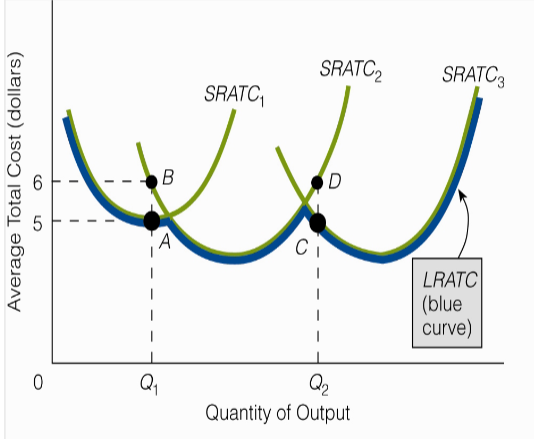

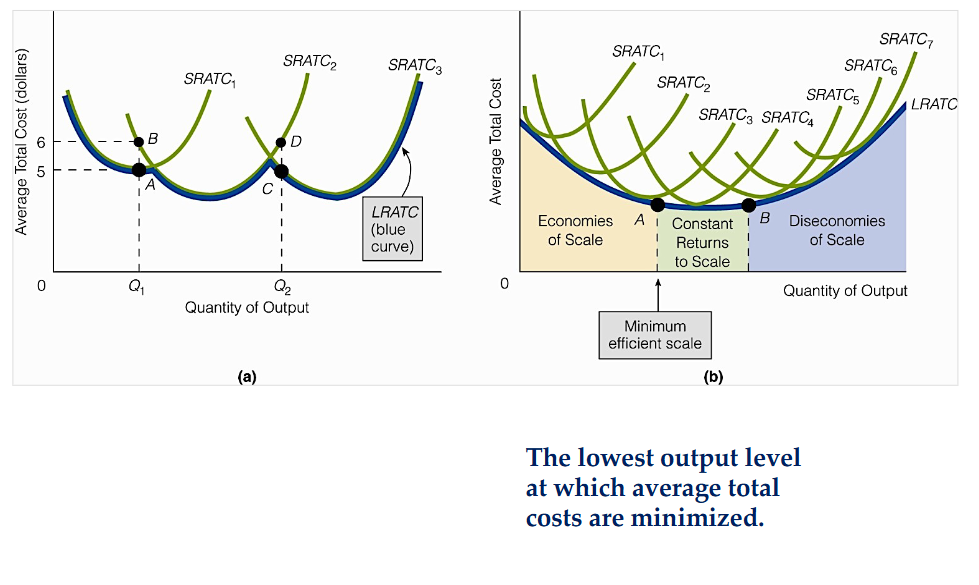

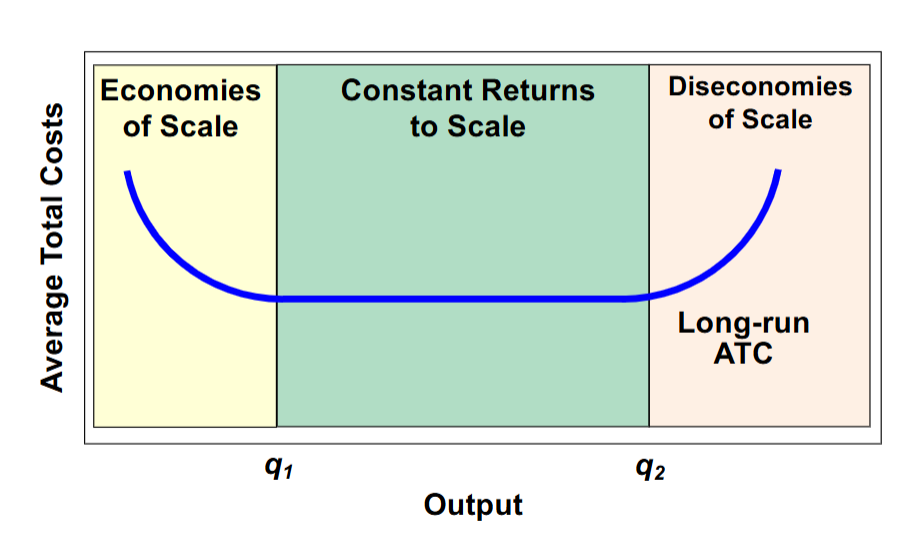

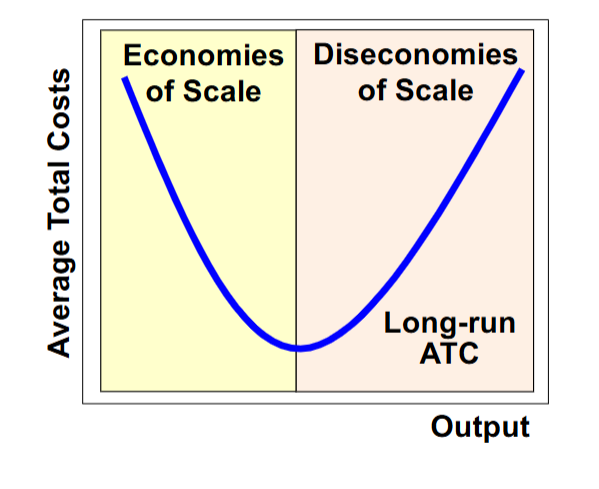

long-run average total cost (LRATC) curve

A curve that shows the lowest (unit) cost at which the firm can produce any given level of output

there are three short-run average total cost curves for three different plant sizes

if these are the only plant sizes, the long-run average total cost curve is the heavily shaded, blue scalloped curve

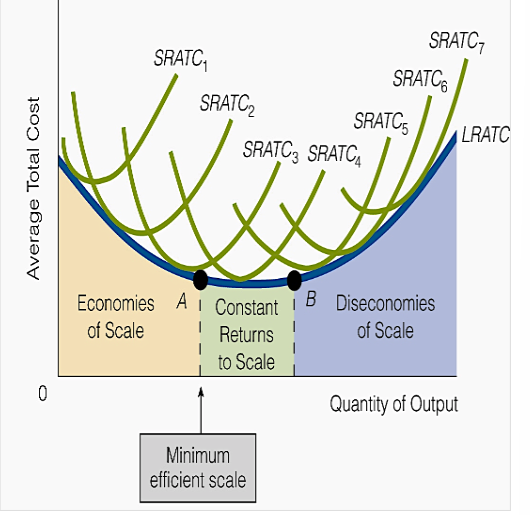

LRATC

the long-run average total cost curve is the heavily shaded, blue smooth curve

the LRATC curve is not scalloped because it’s assumed that there are so many plant sizes that the LRATC curve touches each SRATC curve at only one point

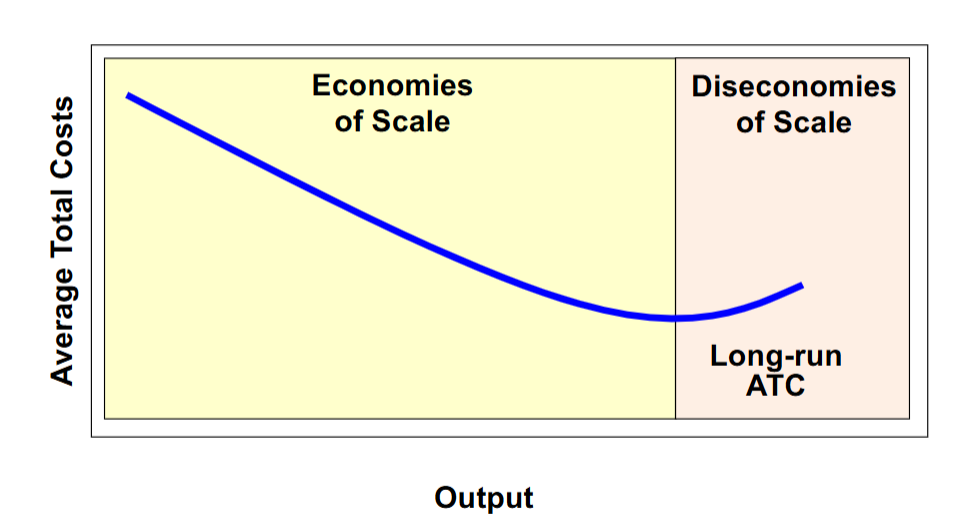

economies of scale

Economies of Scale exist when inputs are increased by some percentage and output increases by a greater percentage, causing unit costs to fall. (LRATC is falling)

Constant Returns to Scale exist when inputs are increased by some percentage and output increases by an equal percentage, causing unit costs to remain constant. (LRATC is constant)

Diseconomies of Scale exist when inputs are increased by some percentage and output increases by a smaller percentage, causing unit costs to rise. (LTRAC is rising)

Minimum Efficient Scale - The lowest output level at which average total costs are minimized.

why economies of scale?

Up to a certain point, long-run unit costs of production fall as a firm grows. There are two main reasons for this:

Growing firms offer greater opportunities for employees to specialize.

Growing firms can take advantage of highly efficient mass production techniques and equipment that ordinarily require large setup costs and thus are economical only if they can be spread over a large number of units.

why diseconomies of scale?

In very large firms, managers often find it difficult to coordinate work activities, communicate their directives to the right persons in satisfactory time, and monitor personnel effectively.

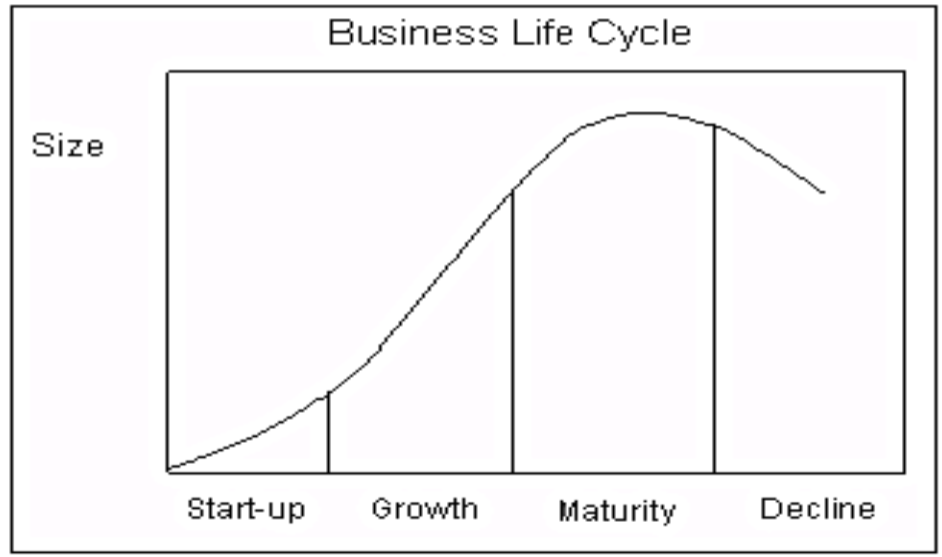

business life cycle

shifts in cost curves

a firm’s cost curves will shift if there is a change in:

taxes

input prices

technology

cost curves

long-run production costs

the firm can change all input amounts, including plant size

all costs are variable in the long run

long-run ATC

different short-run ATCs

economies of scale

economies of scale

labor specialization

managerial specialization

efficient capital

other factors

constant returns to scale

diseconomies of scale

control and coordination problems

communication problems

worker alienation

shirking

minimum efficient scale (MES)

lower level of output where long-run average costs are minimized

can determine the structure of the industry

MES and Industry Structure

TFC, TVC, and TC

market structure

A particular environment of a firm, the characteristics of which influence the firm's pricing and output decisions

diff forms of market structure

Perfect competition

Monopolies

Oligopolies

the theory of perfect competition

A theory of market structure based on four assumptions:

There are many sellers and many buyers, none of which is large in relation to total sales or purchases.

Each firm produces and sells a homogeneous product.

Buyers and sellers have all relevant information with respect to prices, product quality, sources of supply, and so on.

There is easy entry into and exit from the industry.

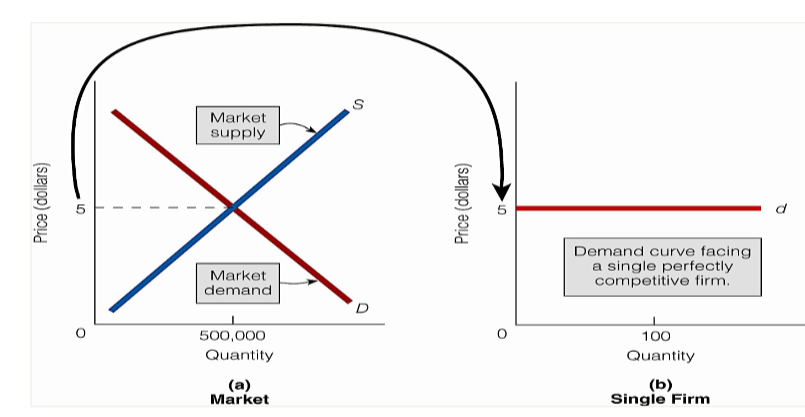

a perfectly competitive firm is a price taker

A seller that doesn't have the ability to control the price of the product it sells; it takes the price determined in the market

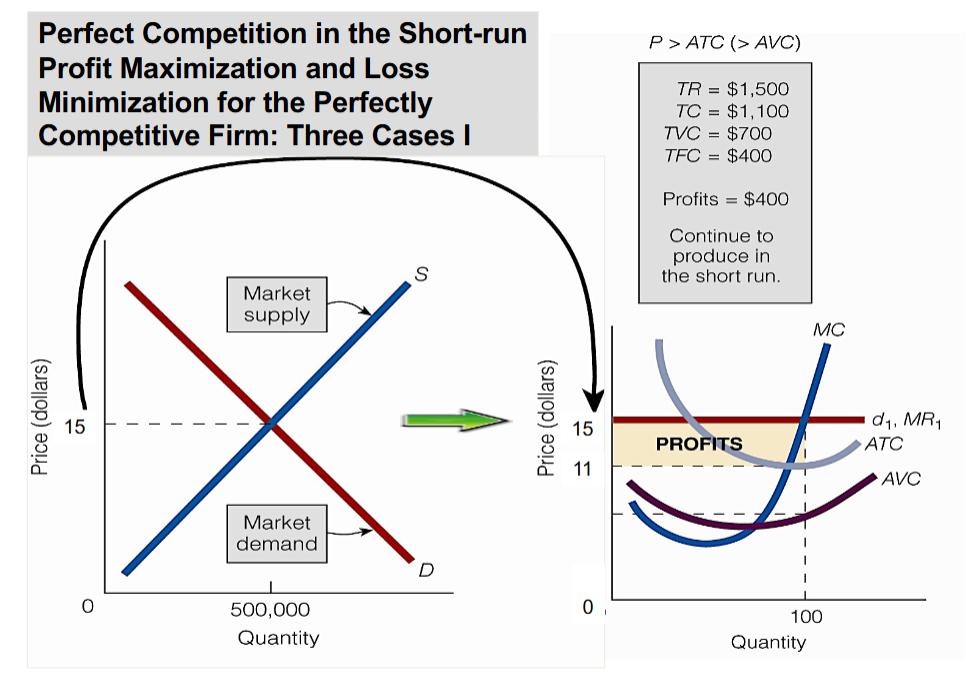

market demand curve and firm demand curve in perfect competition

The market, composed of all buyers and sellers, establishes the equilibrium price (a)

A single perfectly competitive firm then faces a horizontal (flat, perfectly elastic) demand curve

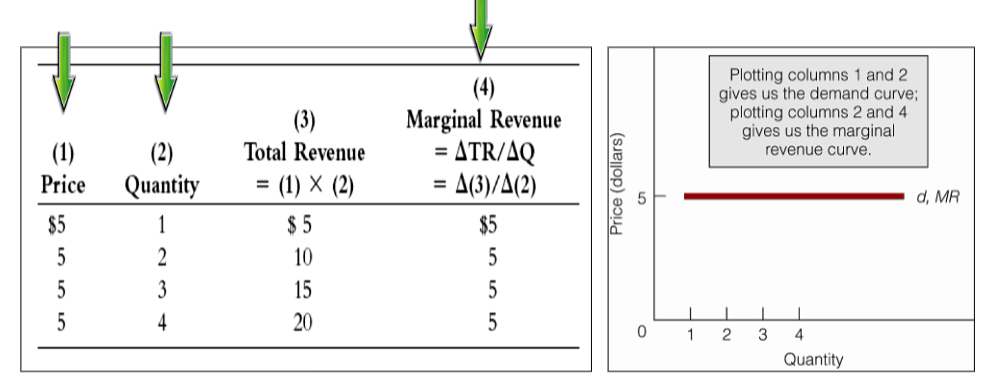

marginal revenue (MR)

The change in total revenue that results from selling one additional unit of output

the demand curve and the marginal revenue curve for a perfectly competitive firm

by computing marginal revenue, we find that it is equal to price

by plotting columns 1 and 2, we obtain the firm’s demand curve

by plotting columns 2 and 4, we obtain the firm’s marginal revenue curve

the two curves are the same

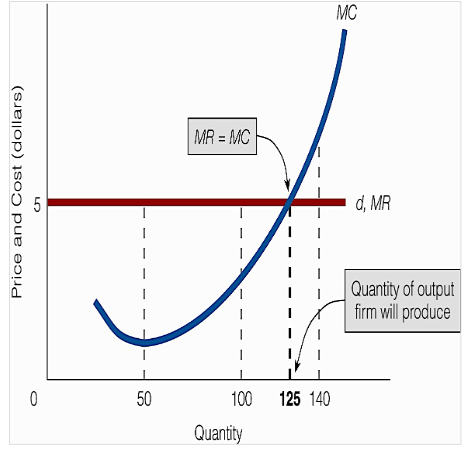

quantity of output the perfectly competitive firm will produce

The firm’s demand curve is horizontal at the equilibrium price. Its demand curve is its marginal revenue curve. The firm produces that quantity of output at which MR = MC

profit maximization rule

profit is maximized by producing the quantity of output at which MR = MC

for perfect competition, profit is maximized when P = MR = MC

resource allocative efficiency

Producing a good—any good—until price equals marginal cost ensures that all units of the good are produced that are of greater value to buyers than the alternative goods that might have been produced.

A firm that produces the quantity of output at which price equals marginal cost (P = MC) is said to exhibit resource allocative efficiency.

For a perfectly competitive firm, profit maximization and resource allocative efficiency are not at odds.

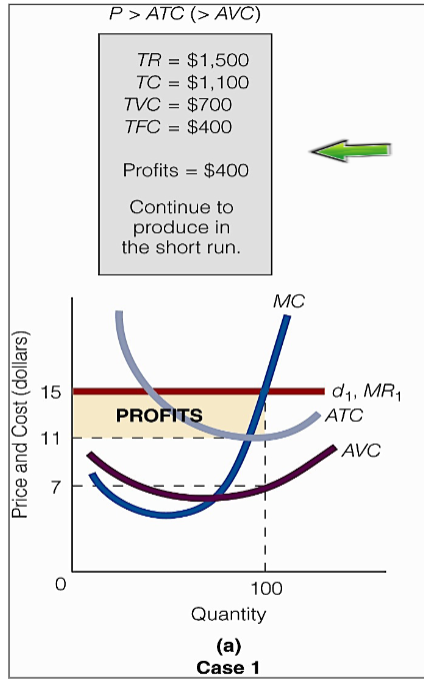

perfect competition in the short-run

profit maximization and loss minimization for the perfectly competitive firm - case I

in case 1, TR TC and the firm earns profits

it continues to produce in the short run

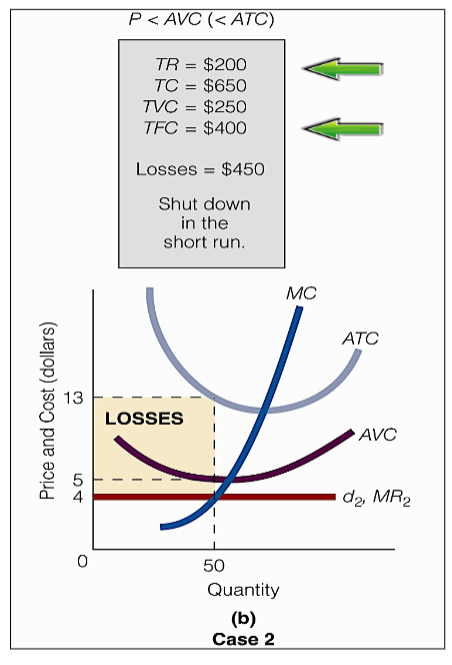

perfect competition in the short-run

profit maximization and loss minimization for the perfectly competitive firm - case II

in case 2, TR < TC and the firm takes a loss

it shuts down in the short run bc it minimizes its losses by doing so