Economics

1/58

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

59 Terms

What is Economics?

Economics is the study of human behavior. It involves how people use limited resources to satisfy their needs and unlimited wants.

What is Production?

Production is the process of making a good or services, such as producing a car.

What is Income?

Income as the money given to those involved in the production of goods and services, such as wages.

What is Expenditure?

Expenditure as the spending of income on goods and services.

What is Microeconomics?

Microeconomics often looks at the factors that influence the small bits, units or various parts making up the overall Australian economy including the decisions made by individual consumers or single firms.

What is Macroeconomics?

Macroeconomics takes a wider ‘bird’s-eye’ look at the whole economy and the larger flows affecting overall economic conditions in the country.

What is Positive economics?

Free of personal opinion

based on fact and hard evidence

can be proved or disproved

What is Normative economics?

Based on personal opinion

Based on valued judgments

About the way things should be

Cannot be proved or disproved

What is Relative Scarcity?

Relative scarcity is the fundamental economic problem of having unlimited human wants and needs but limited resources available to satisfy them.

Wants are:

Three types of Resources?

Land, Labour, Capital

What is Opportunity cost?

“The benefit sacrificed when choosing one option over another”

A Production Possibility Frontier shows?

Relative scarcity

Economic choices

Normative

Opportunity cost

Technical efficiency

Productivity / efficiency

Underutilisation of resources

Steps for cost benefit analysis are

Add up all direct and indirect costs

Add up all direct and indirect benefits

Divide benefits by costs

Greater than 1.0 means net benefit, and therefore worth doing

The three basic economic questions are?

What and how much to produce?

How to produce?

For whom to produce?

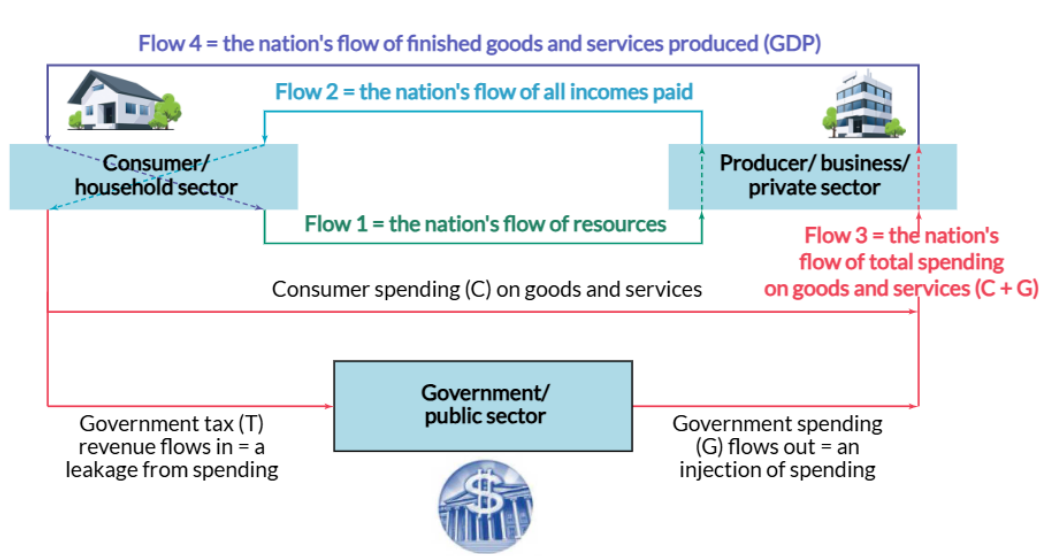

What does the circular flow model look like?

What is the traditional view of the Consumer?

Act rationally and in self-interest

Make informed and smart decisions

Maximise utility and marginal benefit

Have ordered preferences

What does it mean by ‘consumers act rationally;?

They act in their self-interest to maximise their satisfaction.

What is meant by ‘consumers make informed decisions’?

Economists assume that consumers have access to relevant and accurate information to make their rational decisions

What is the law of marginal utility?

In Economics, the law of diminishing marginal utility means that each additional (or marginal) unit of a good or service that is consumed generates less utility (satisfaction) than the previous one.

What are subsidies?

A government payment to make some goods or services more attractive and affordable, or possibly it may even be provided free of charge. Then, rational and self-interested consumers are normally keen to take up these offers.

What are Tax Rebates?

They reduce the amount of tax paid on taxable incomes making the item cheaper and more attractive to purchase than otherwise.

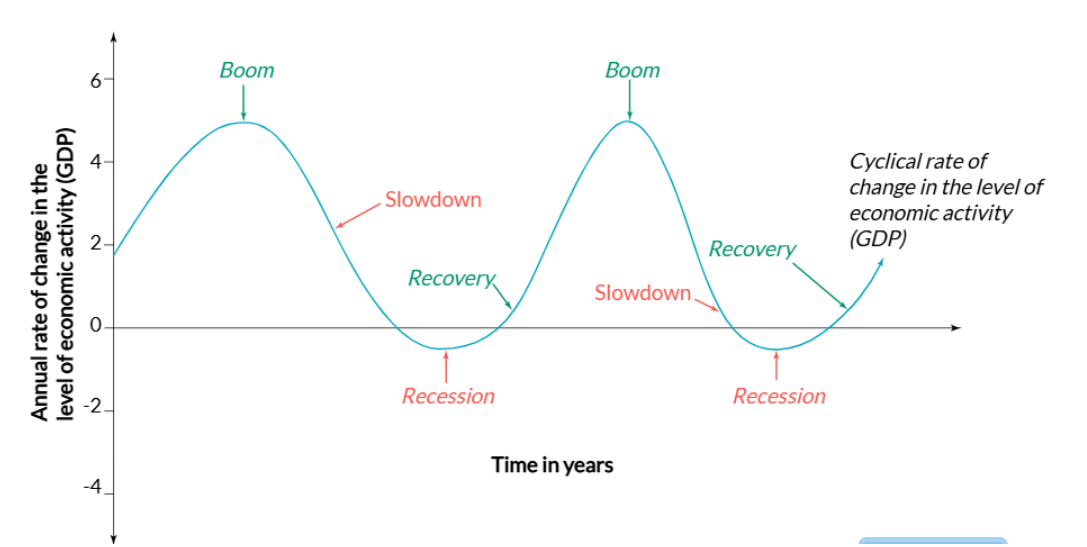

What is the business cycle?

Material living standards reflect…

income per person

level of consumption of good and services per person

the purchasing power of incomes

Non material living standards reflect…

The quality of daily life

Hapiness

Life expectancy

Mental and physical health

freedom

state of the environment

leisure time

crime rates

literacy rates

quality of relationships

What is the traditional view of a business

Businesses seek to maximize their profit

In both the short-term and especially long-term.

Profit = Total revenue - Total value of production costs

As of June 2025, 2.7 million businesses trading in Australia

How do businesses maximise profits?

To maximise their profits, most firms make decisions that seek to do two main things — maximise their sales revenues and minimise their production costs

What are the 5Ps of Marketing

Product — “better than the rest”

Price — High for profits, but low for sale. Just right.

People — ‘Enhance the consumer’s experience’

Place — Location or convenience

Promotion — Consumers need to know your potential product is being sold. Can include selling strategies drawn from behavioural economics

What is the law of demand?

The law of demand simply states that the quantity of a particular good or service that buyers are prepared to purchase, varies inversely with the change in price

OR//

As the price increases, there is a contraction in the quantity demanded, causing a movement upwards along the demand line.

As the price decreases, there is an expansion in the quantity demanded, causing a movement downwards along the demand line.

What is Supply?

The law of supply simply states that the quantity of a particular good or service that sellers are prepared to supply, varies directly with the change in price

OR//

As the price increases, there is an expansion in the quantity supplied, causing a movement upwards along the supply line.

As the price decreases, there is a contraction in the quantity supplied, causing a movement downwards along the supply line.

What is Equilibrium

At equilibrium, the quantity demanded exactly equals the quantity supplied, and there is no force for further change; The market is stable

When does the demand curve shift to the right?

When there is in an increase in demand

When does the demand curve shift to the left?

When there is a decrease in demand

When there is an increase in supply which way does the supply curve shift?

The supply curve shifts to the right

When there is a decrease in supply which way dopes the supply curve shift?

The supply curve shifts to the left

What is Behavioral Economics?

Behavioral economics combines traditional economic theory and psychology to explore why people make irrational decisions.

What is bounded self interest?

People are motivated by their own benefit but also gain satisfaction from helping others through things like charity, volunteering, and kindness.

What is Status Quo Bias?

People prefer familiar choices and often stick with defaults, habits, or routines even when better options exist.

What is Bounded willpower?

People know what they should do but often give in to short-term temptations instead of long-term benefits.

What is Herd Behavior?

People follow what others are doing, especially when they are uncertain or think the crowd knows best.

Framing Bias

Decisions are influenced by how information is presented rather than the actual facts.

Anchoring Effect

People rely heavily on an intial piece of information, which influences later decisions and judgments.

What is overconfidence bias?

People overestimate their knowledge, abilities or chances of success.

what is vividness bias?

People give more weight to memorable or emotional information than to reliable evidence and statistics.

What is present bias?

People value immediate rewards more than future benefits, often leading to procrastination or poor long-term decisions.

What is Loss Aversion?

People dislike losses more than they enjoy equivalent gains and often act to avoid losing.

What is Narrative Fallacy?

People are persuaded by simple, believable stories even when the evidence is weak or incomplete.

What is the nudge?

Choices can be presented in a way that encourages certain behaviors without removing freedom of choice.

What is a Monopoly?

A monopoly is a market structure where a single company or entity is the sole provider of a particular good or service, giving it absolute control over the market.

What is an Oligopoly?

An oligopoly is a market structure where a small number of large firms dominate an industry.

What is a Pure Competition Market?

A pure (or perfect) competition market is an idealized theoretical market structure where many small firms sell identical products, no single company influences the price, and there are no barriers to entry or exit.

What is a monopolistic competitive market?

A monopolistic competitive market is an industry where many businesses sell products that are similar but not perfectly identical. Because each product is slightly different—due to branding, features, or location.

What is a substitute product?

Substitute and something that is a direct alternative of a product

What is a complementary product?

Complimentary is something linked and used with a product

What is Market Surplus

Market surplus occurs when the quantity supplied of a good or service exceeds the quantity demanded at a specific price.

What is Market Shortage?

A market shortage occurs when the quantity demanded for a good or service exceeds the quantity supplied at a given price.

What is Market Failure?

Market Failure is when the goods and services produced by firms dont meet societies needs and wants.

Why do Taxes occur?

Taxes increase the costs faced by firms and consumers, discouraging the production and consumption of goods and services that have negative impacts on society.

What are Government Disincentives?

Government disincentives are measures such as taxes, fines, and charges that discourage certain behaviours or activities among individuals.