CFA Volume 4 (Fixed-Income)

1/432

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

433 Terms

Loans

Debt instruments formed and governed by a private agreement usually between an individual or company and a financial intermediary, such as a bank.

Principal payments are distributed over the life of the instrument (e.g., commercial and residential real estate loans).

Investors face lower credit risk because the borrower’s liability is reduced over time and more cash is received sooner.

Bonds (Fixed-Income Securities)

More standardized contractual agreements between larger issuers and investors. The committed periodic cash flows of a bond distinguish it from equity securities.

Bond Issuer

Borrows money most often to fund operations or capital expenditures. Any legal entity liable for all interest and principal payments.

Bond Investor

Lenders who provide funds to the issuer in exchange for interest payments and future repayment of principal.

Bond Principal

At issuance, when investors purchase a bond in exchange for cash (i.e., this is the amount borrowed). Also referred to as the bond's par value.

This is paid at the end of the maturity and is added on top of the last coupon payment (this will be the largest payment made over the course of the bond).

Coupon Payment

The amount the issuer pays the investor (equals the coupon rate times the par value of the bond). The coupon rate is always provided as an annual amount.

If not stated, the assumption is that coupons are paid semiannually.

Bond Maturity

The date of the final payment the issuer makes to investors.

Bond Tenor

Refers to the remaining time to maturity.

The final coupon payment is made up of

The coupon payment + the principal (the total amount borrowed at inception).

Money market securities

Fixed-income securities with a tenor of year or less at issuance (e.g., government T-bills).

Differences in yield measures quotes for money market instruments versus bonds:

1) Bond YTMs are annualized and compounded, while yield measures in the money markets are annualized but not compounded; the return on a money market instrument is stated on a simple interest rate basis

2) Bond YTMs are usually stated for a common periodicity for all YTMs, money market instruments with different times-to-maturity have different periodicities for the annual rate

3) Bond YTMs YTMs can be calculated using standard TVOM analysis, money market instruments are often quoted using non-standard interest rates and require different pricing equations than those for bonds (e.g., AOR)

Factors that result in differences in YTMs of two bonds:

1) Credit risk

2) Different currencies

3) Liquidity

4) Tax differences

5) Times to maturity

This concept of differences is known as maturity structure of interest rates or term structure of interest rates.

Capital market securities

Fixed-income securities with tenors longer than one year at issuance.

Perpetual bonds

Less common bond type with no stated maturity.

Face Value

The amount an issuer agrees to repay to investors at maturity.

Different ways a bond's interest can be paid:

1) A fixed coupon paid on specific dates (monthly, quarterly, semi-annual, annual)

2) A variable coupon determined and paid on specified dates

3) Part of a single payment with the principal at maturity

Floating-rate notes (FRNs)

Bonds with variable interest payments. Investors face less interest rate risk because coupon payments adjust with interest rates, unlike fixed-coupon bonds, though there is still credit risk. They also face less price risk because cash flows adjust to changes in interest rates, and are therefore used to hedge certain exposures and match asset and liability cash flows.

Attractive to investors that seek to benefit from rising interest rates.

Investors face less interest take risk because coupon payments adjust with interest rates. However, if credit risk increases, investors will seek a higher yield as compensation, causing the price to fall irrespective of any changes in the MRR.

At the beginning of the period, the coupons is set but not paid until the end of the period.

Coupons for FRNs

Determined as a combination of a market reference rate (MRR) and an issuer-specific spread (refereed to as credit spread). MRR resets periodically, and the coupon only changes with changes in the MRR.

= MRR (variable) + Credit Spread (fixed)

Different cash flow structures

1) Bullet structure

2) Amortizing loans

3) Variable interest

4) Zero coupon

5) Deferred coupon

Credit Spread

Issuer-specific, set at the time of FRN issuance, usually constant over the bond's life, and is expressed in basis points (bps), or hundredths of a percentage point. The higher the issuer's credit quality, the lower the spread.

For FRNs this is the amount that is added on top of the MRR to calculate the coupon payment.

The more risk the investor faces, the wider the spread. This is the same calculation as Expected Loss.

If credit spread = expected loss, we say investor is “fairly” compensated.

Bid-Offer Spread

Related to how liquid the bond is, the more illiquid the bond the wider the spread -I. Recently issues bonds will be more traded than seasoned bonds. Sovereign bonds are more liquid than corporate bonds.

Zero-coupon bonds (pure discount bonds)

Bonds that do not pay periodic interest and instead pay interest as part of a single payment with principal at maturity. Typically issued at a discount to par.

Seniority

A debt issuer's priority of repayment among all issuer obligations.

Senior Debt

Has priority over the other debt claims in the case of bankruptcy or liquidation.

Junior Debt (Subordinated Debt)

Has lower priority than senior debt and paid only once senior claims are satisfied.

Contingency Provision

A clause in a legal agreement that allows for an action if an event of circumstance occurs. Most common for bonds involving embedded options (call, put, and conversion to equity options).

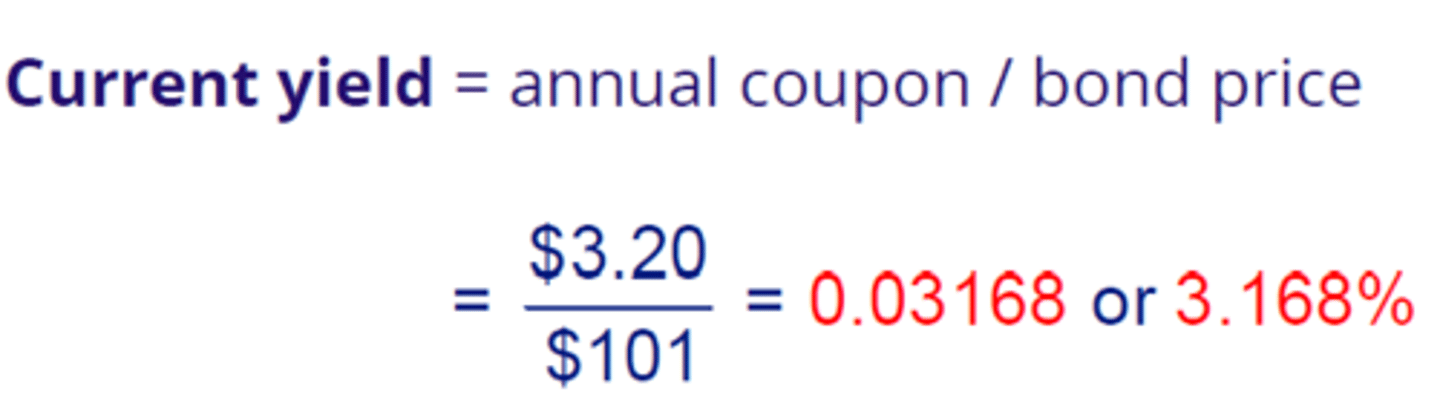

Current Yield

Equal to the bond's annual coupon divided by the bond's price and expressed as a percentage (analogous to dividend yield for an equity security).

Has several limitations and is not as accurate as the YTM.

The denominator is the current price, not the face value.

Yield-to-Maturity

The internal rate of return (IRR) calculated using the bond's price and its expected cash flows to maturity (usually quoted as an annual rate).

Reflects the level of risk the investor is taking on (i.e., the higher the risk the higher the YTM). The yield curve is upward sloping (YTM increases as the time to maturity increases because the investor has to wait longer to receive their cash flows).

Reflects what the investor (bond holder) earns.

In comparison to the currency yield, the YTM takes into consideration the timing of coupons, the principal amount investor receives at maturity, and the current price.

Reflects the return the the price paid today and the amount received at maturity.

An investor's rate of return on a bond will equal the bond's yield-to-maturity as long as the investor:

1) Receives all promised interest and principal payments as scheduled (i.e., no default)

2) Holds the bond until maturity

3) Reinvests all periodic cash flows at the yield-to-maturity

Bond Indenture

Legal contract that describes the form of the bond, the obligations of the issuer, and the rights of the bond holders. Also identifies the issuer's source of repayment, any commitments made by the issuer to bond holders, as well as any provisions that support or enhance the issuer's ability to repay its debt in full.

Does not include the identity of the lender.

Unsecured Bonds

Cash flows are the sole source of repayment. Typical for corporate bonds for issuers of high credit quality.

Secured Bonds

When issuer offers investors a legal claim (or lien or pledge) on specific assets as secondary sources of debt repayment (i.e., collateral). Typical for corporate issuers with less stable operating cash flows.

Borrowing costs decrease when bonds are securitized.

Source of repayment for sovereign bonds

Tax revenues

Source of repayment for unsecured corporate bonds

Operating cash flows

Examples of debut bond issuers

- New corporate legal entities formed after a merger, acquisition, or divestiture, which usually refinance all existing debt outstanding

- Companies that reach a more mature stage of the life cycle with more predictable cash flows

- Sovereign governments that raise external foreign currency debt for the first time

Debut issues often require a lot of time for underwriters to market the issuance to investors through roadshows.

Trustee

The financial institution that represents the interests of the investor but is appointed by the issuer. Works with the issuer to create the bond indenture. These are usually financial institutions.

Source of repayment for secured corporate bonds

Operating cash flows and collateral cash flows or sale

Source of repayment for asset-backed security (ABS)

Loan/receivable cash flows

Bond Covenants

Restrictive clauses in a bond contract that limit the issuer from taking actions that may undercut its ability to repay the bonds.

Affirmative covenants specify what issuers are required to do, whereas negative covenants specify what issuers are prohibited from doing. Affirmative covenants are administrative in nature (e.g., payment of interest and principal).

Examples of affirmative bond covenants

Use of proceeds from the bond issuer, provision of timely financial reports, insure and perform periodic maintenance on financed assets. Also include parí passu clause (or "equal footing"), which ensures that a debt obligation is treated the same as the borrower's other debt obligations with similar seniority.

Cross-Default Clause

An affirmative covenant that states borrowers are considered in default if they default on another debt obligation.

Examples of negative bond covenants

Limitations on investments, disposal of assets, issuance of debt senior to existing obligations.

Negative covenants seek to ensure that an issuer maintains the ability to make interest and principal payments.

Bullet Bond

Standard fixed-coupon bond, where bond issuer receives the principal at settlement, makes periodic fixed coupon payments, and repays the principal at maturity

Amortizing Debt

Fixed-income instruments that periodically retire a portion of principal outstanding prior to maturity. Offer a borrower the ability to spread payments more evenly over the life of the instrument (e.g., commercial and residential real estate mortgage loans). Over time, the interest portion of the payment declines while the principal repayment portion increases.

Investors receive higher near-term cash flows on this amortizing debt relative to bullet bonds and face lower credit risk because the borrower's liability is reduced over time.

Partially amortizing bond

Combine elements of bullet bond and fully amortizing bond (i.e., can include a large, lump-sum payment or balloon payment). The last coupon payment includes a very small portion of principal. Because of balloon payment at the end, the last payment is usually larger than the last payment of a fully amortizing loan.

Sinking Fund

An issuer's plans to set aside funds over time in an escrow account to retire the bond early based on terms agreed upon issuance. Reduces credit risk while increasing reinvestment risk due to a reduction of principal outstanding prior to maturity.

With a sinking fund, the issuer must redeem part of the issue before maturity, but the specific ones to be redeemed are not known. Therefore, sinking funds face the risk of redemption before maturity.

Used by issuers to periodically retire a bond’s principal outstanding. Like amortization, sinking funds reduce credit risk while increasing reinvestment risk due to a reduction of principal outstanding prior to maturity.

Deferred Coupon Bond

Bond that pays no coupons for its first few years but then pays a higher coupon than it otherwise normally would for the remainder of its life. Issuers for this bond type usually seek to conserve cash immediately following the bond issue, which may indicate lower credit quality or that the issuer is financing a project that does not generate income until completion (construction).

Example: a 10-year bond pays no interest for 3 years, then pays $229.25, followed by payments of $35 semiannually for seven years, and an additional $1,000 at maturity.

Theoretically, the price of a callable bond should never rise above its __________________.

Call price

Waterfall Structure

Used to determine the timing of cash flows to investor classes with different priority claims to the same cash flows.

Interest or coupon payments are usually paid to all classes with no preference, but the repayment of principal occurs sequentially so that the most senior investor class with the highest ranking in the capital structure receives principal payments first.

Typical of ABSs.

Loans or FRNs are attractive to investors seeking to benefit from ______________ interest rates.

Rising

Four types of Amortizing Loans

1) Fully amortizing

2) Partially amortizing

3) Sinking fund provision

4) Waterfall structure (ABSs and MBSs)

These reflect different ways to pay off the principal.

Fully Amortizing Loan

The principal is fully paid off by maturity.

Only a fully amortizing structure features payments that are all equal.

Step-Up Bonds

Bond coupon increases by specific margins at specified dates. Used to protect investors against rising rates and, in some cases, to provide an incentive for issuers to take advantage of a contingency provision (an example of cash flow changes based on an event are higher coupons due to deterioration in issuer's credit quality).

Payment-in-kind

Feature of a loan that allows an issuer concerned about future cash flow problems to pay periodic interest in the form of an increase in the bond or loan principal outstanding rather than as a cash payment. Most frequently used by firms with relatively high reliance on debt financing and are usually associated with a higher interest rate to compensate investors assuming greater principal risk.

Zero-Coupon Bonds

Repay principal at maturity and have no coupon payments. Often referred to as discount bonds since they are priced below par if interest rates are positive.

Different fixed-income instrument cash flow structures:

1) Standard, fixed-rate bond ("bullet bond")

2) Amortizing principal

3) Variable interest

4) Zero coupon

Contingency Provision

Clause in a legal document that allows for some action if a specific event or circumstance occurs. The most common for bonds involves the right — but not obligation — for an issuer to take an action specified in an indenture.

Most common for callable bonds, putable bonds, and convertible bonds.

Callable Bonds

Issuer has the right to redeem (or "call") all or part of the bond prior to the specific maturity date. This offers the issuer the flexibility to refinance debt if market interest rates were to fall.

Generally has a higher yield than a putable bond because more risk to the investor.

If a callable bond’s YTM rises about its coupon rate, the call feature is less valuable and a callable bond behaves much like a non-callable bond with respect to price movements due to interest rates changes.

Call Premium

The amount by which the Call Price exceeds the par value of the bond. If the Call Price at time t is $102.32, the Call Premium = $2.32.

Call Risk

The uncertain maturity and limited price appreciation associated with callable bonds. Investors expect to be compensated for callable bonds with a higher yield versus a similar, non-callable bond given this uncertainty.

Different types of variable interest debt:

1) MRR + Credit Spread

2) Step-Up Bonds

3) Leveraged Loans

4) Credit-Linked Notes

5) Payment-in-Kind (PIK) Bonds

6) Green Bonds

7) Index Linked

Putable Bonds

Bondholders (Investors) have the right to sell the bond back to the issuer at a pre-determined price on specified dates. The put price is usually the par value of the bond. Put provision benefits bondholders by guaranteeing a pre-specified selling price at the redemption dates.

Usually have a lower yield than a callable bond because less risk to the investor.

If a putable bond’s YTM is less than its coupon rate, the put feature is less variable and the putable bond’s price behaves like an option-free equivalent bond with respect to interest rate changes.

Capital Gain from Bond Investment

A bond investment will generate a capital gain or loss if sold prior to maturity at a price different from the purchase price.

100 bps = _____ %

1%

Convertible Bond

Debt instrument with a contingency provision related to the issuer's outstanding common equity. Grants bondholders the right to exchange the issuer's bond for a number of its common shares in the future at an effective price per share known as conversion price. Common among growth companies that may have limited cash flow to pay interest and principal but are willing to raise equity at a higher conversion price in the future.

Bondholders are often willing to accept a YTM that is very low in exchange for conversion rights (i.e., conversion option is favorable for the bondholder so should trade at a lower spread).

Conversion Ratio

Represents the number of common shares a bond may be converted into for a specific par value.

= Convertible bond par value / Conversion price (common equity)

Conversion price will likely be less than the bond’s par value (e.g., 1,000 FV vs. EUR75 for stock).

Conversion price is set at the time the bond is issued, but the share price of common equity of the firm will fluctuate over the life of the bond so the option may go in- and out-of-the-money. If the issuer’s share price far exceeds the conversion price, the bond’s price will more closely track its conversion value.

Eurobonds

Bonds issued and traded in cross-border market named for the currency in which they are denominated (i.e., issued outside the jurisdiction of any single country). Usually unsecured. Can be considered attractive because usually have fewer tax constraints/regulations. Not registered with the SEC so so cannot be sold to a majority of US investors.

All three components may disagree (e.g., US firm, Australian investor, denominated in Japanese yen).

"Euro" in the name is irrelevant.

Three dimensions of fixed-income categorizations:

1) Issuer type (sector)

2) Credit quality

3) Time to maturity

Credit Rating

Letter-grade, qualitative measure of an issuer's ability to meet its debt obligations based on both the probability of default and the expected loss under a default scenario for the issuer’s senior unsecured debt.

Call Premium

The amount of money on top of par (NOT the current price) that is paid for the call option. This is usually baked into the Call Price and can be represented in monetary amount, percentage, ratio, etc.

Bermuda Call Option

Series of dates that the option can be exercised.

European Call Option

A single specified date that the option can be exercised.

American Call Option

Option can be exercised on or after a specific date (i.e., "continuous" after a certain date).

Investment-grade issuers

Those with a credit rating of BBB- or higher.

Contingent Convertible Bonds (CoCos)

Bonds that automatically convert into equity if a specific event or circumstance occurs, such as the issuer's equity capital falling below the minimum requirement set by the regulators (i.e., in comparison to standard convertibles, not at the discretion of the investor, therefore offering higher yield than otherwise similar bonds).

Not an "option" or "right" but event-based.

Convert debt into equity to increase its capital and reduce the bank’s likelihood of default. While standard convertibles will be converted when the share price increases, CoCos are converted on the downside.

High Yield Issuers

Those with a credit rating of BB+ or lower. Also known as speculative grade or junk. High-yield investors expect greater return for assuming a higher probability of default ad often compare returns to those of equity investments

High-yield issues tend to be restricted to 10-years maturities or less.

Conversion Value

= Conversion Ratio x Current Share Price

Reflects how much the investor "pays" to convert bonds to common equity. This value helps the investor assess whether the option is good value. If the issuer’s share price far exceeds the conversion price, the bond’s price will more closely track its conversion value.

Domestic Bonds

Issuer, investor, and currency are all in the same place (e.g., US firm, US investor, denominated in USD).

Foreign Bonds

Investor and currency agree, while issuer is different (e.g., US firm, British investor, denominated in GBP).

Original Issued Discount (OID) Bonds

Issued below par (at a discount), with capital gain or loss usually taxed annually.

Global Bond

A type of Eurobond that is issued internationally as well as its domestic economy (i.e., outside the jurisdiction of any one country).

Three ways fixed-income indexes differ from equity indexes:

(1) A single issuer may have many individual fixed-income securities outstanding; all bonds that meet index eligibility requirements are included in indexes, causing fixed-income indexes to have many more constituent securities than equity indexes have

(2) The finite maturity of bonds and the higher frequency of new issuance lead to far more changes in constituents (turnover) in fixed-income indexes than in equity indexes

(3) Bond index constituents are usually weighted by market value of debt outstanding

Major participants in secondary bond markets

Institutional investors, financial intermediaries, and central banks

Distressed Debt

Bonds of issuers believed to be very close to or in bankruptcy. Typically trade in the secondary market at a price well below par, because bondholders are unlikely to receive all promised future interest and principal payments.

Hedge funds and other opportunistic investors seeking more equity-like returns (from price appreciation) are often the buyers of distressed bonds.

Instrument that offers the most flexible and immediate access to short-term funding

Credit lines

Examples of short-term, risk-free fixed-income securities

Treasury bills

Examples of short-term, investment-grade fixed-income securities

Repo commercial paper, asset-backed commercial paper

Examples of intermediate, risk-free fixed-income securities

Treasury notes

Examples of intermediate, investment-grade fixed-income securities

Unsecured corporate bonds, asset-backed securities

Examples of intermediate, high-yield fixed-income securities

Secured corporate bonds, leveraged loans

Examples of long-term, risk-free fixed-income securities

Treasury bonds

Examples of long-term, investment-grade fixed-income securities

Unsecured corporate bonds, mortgage-backed securities

Characteristics of typical positions held by financial intermediaries and central banks

Range of maturities, risk free

Characteristics of typical positions held by pension funds and insurance companies

Long term, risk free/investment grade

Characteristics of typical positions held by money market funds

Short term, risk free/investment grade

Characteristics of typical positions held by corporate issuers

Short term, investment grade

Characteristics of typical positions held by bond funds and ETFs

Intermediate term, investment grade

Characteristics of typical positions held by asset managers, hedge funds, and distressed debt funds

Intermediate term, gradually moving from investment grade to high yield

Uncommitted lines of credit

The least reliable form of bank borrowing in which a bank offers, without formal commitment, a line of credit for an extended period of time but reserves the right to refuse any request for its use (i.e., bank can refuse at any point if circumstances change, so cannot be used as a primary source of financing). Usually does not have collateral. Bank charges a base rate or a MRR plus issuer-specific credit spread on any principal outstanding.

Primary attraction is that they do not require the company to pay any compensation other than interest on balances outstanding to the bank (i.e., smaller capital commitment).

Three main types of fixed-income indexes

1) Aggregate indexes (e.g., Bloomberg Barclays Aggregate Index)

2) Narrower focus (e.g., JPMC Emerging Markets Bond Index Plus)

3) Incorporating ESG factors