Core Act D (MCS)

1/43

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

44 Terms

Cartn revenue recognition

consultancy = over time

manufacturing = point in time

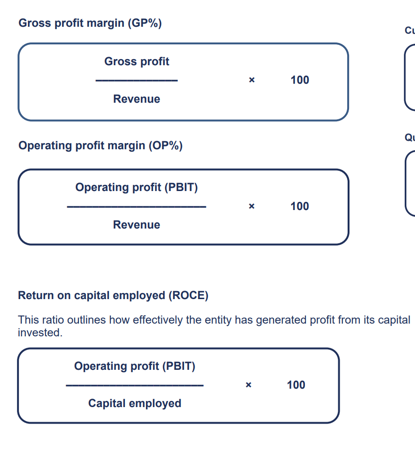

profitability ratios

gross profit margin

operating profit margin

net profit margin

ROCE

earnings per share

ROE

gross profit margin impacts

cost of raw materials

selling prices

sales mix

operating profit margin impacts

salaries

legislation

sales mix

net profit margin impacts

tax rates

interest rates (capital structure)

exceptional items

ROCE impacts

new debt/equity

COS

asset replacement

earnings per share impacts

new shares

bonus share issues

tax/interest rate

ROE impacts

new shares

dividend policy

tax/interest rates

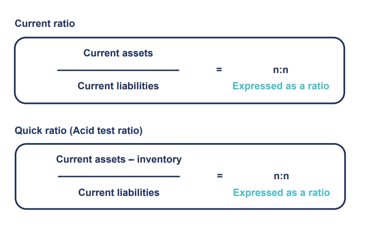

liquidity ratios

current

quick

current ratio impacts

long term finance

sales of non-current assets

inventory valuations

quick ratio impacts

long term finance

sales of non-current assets

bad debt write-off

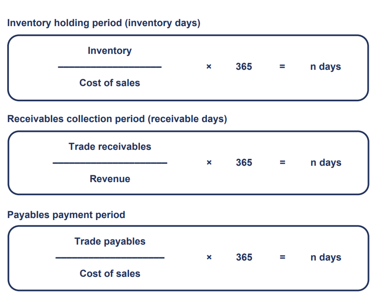

efficiency ratios

operating cycle

asset turnover

asset turnover impacts

asset replacement

production efficiency

demand

receivable days impacts

customer mix

credit policy

prompt payment discounts

payables days impacts

supplier mix

supplier relationships

prompt payment discounts

inventory days impacts

machinery breakdowns

distribution issues

demand issues

capital structure ratios

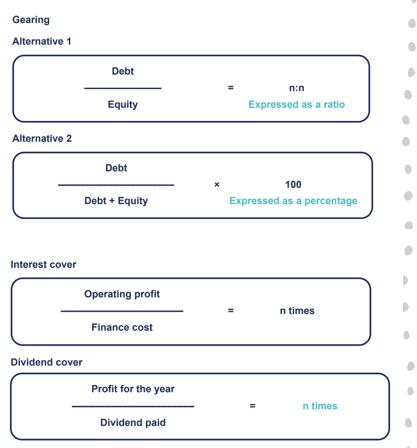

gearing

interest cover

dividend cover

gearing impacts

debt repayments

equity/debt issues

dividends

interest cover impacts

demand

interest rates

long-term debt

dividend cover impacts

payout policy

operational factors

interest/tax rates

ratio analysis cons

backward looking

diff methods

limited qualitative insights

profitability ratios formulae

liquidity ratios formulae

efficiency ratios formulae

capital structure ratios formulae

intangible assets recognition criteria

IAS 38

FRIC

future economic benefits

reliable cost measurement

identifiable

control

intangible assets subsequent treatment

amortise over useful life (finite assets, except goodwill)

impairment review (indefinite assets and goodwill)

revaluation (rare as need market)

intangible assets capitalised

purchased separately at purchase cost

purchased w/ acquisition at FV

development costs (criteria)

development cost capitalise criteria

PIRATE

probable future benefit

intention to complete

resources adequate to complete

ability to use/sell

technically feasible to complete

expenditure reliably measured

intangible assets: written off as expense in SPL

Research costs

Development costs (if don’t meet criteria)

Advertising costs

Internally generated goodwill

revenue recognition

IFRS 15

COPAR

contract

obligations

price

allocate price to performance obligations

recognise revenue

foreign exchange (non-group)

IAS21

functional currency = primary econ env

presentation currency = financial statements

fx spot rate

NIC

non-monetary items outstanding

initial recognition

cash settlement

fx exchange differences

SPL

fx closing rate

outstanding monetary items

lessor accounting

IFRS 16

finance lease: risks/rewards w/ lessee

operating lease: no risks/rewards

provisions

IAS 37

present obligation from past event

probable outflow

reliable estimate

contingent liability

IAS 37

disclose in note

contingent asset

IAS 37

probable: disclose in note

virtually certain: recognise

intangible assets definition

Identifiable non-monetary asset without physical substance eg licenses and patents

finance lease criteria

STOMP

•Specialised to lessee

•Transfers ownership of asset

•Option to purchase asset at price < FV

•Major part of economic life = lease term

•PV lease = FV

finance lease accounting treatment

Net investment = PV of future lease payments discounted at interest rate implicit in lease -> SFP

Unwind financial asset = add interest and deduct lessee cash payments -> SFP

Record gain/loss on disposal (lower of FV of asset or PV lease payments) -> SPL

operating lease accounting treatment

Asset recognised PPE -> SFP

Lease payments -> SPL

ROE formula

profit after interest and tax/total equity x100