C30 CIA DISCOUNT

1/31

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

32 Terms

Discount Rate

Rate used to discount estimate of future CFs

Consistent w/ timing, liquidity, currency of insurance contract CFs

Can be a single rate → spot rate

Or curve of rates varying by duration → yield curve

Fulfilment Cash Flows (FCF)

PV of ests of future CFs + RA for non-financial risk

Liquidity/Illiquidity Premium

Adjustments to liquid risk-free yield curve

Reflects diff in liquidity characteristics between financial instruments underlying risk-free rates & insurance contracts

Liquidity prem → insurer invests in gov bonds

Low risk & easily converted to cash

Liquidity prem = 0

Liquidity prem → insurer invests in biotech startups

High risk & difficult to convert to cash

Liquidity prem high

Reference Portfolio

Portfolio of assets used to derive discount rates based on current market rates

Adj to remove risk char NOT in insurance contracts

Factors that may differ between reference portfolio vs insurance contracts

Liquidity

Currency

Timing

Investment risk

Credit risk

Market risk

How to address diff in timing risk?

Assess consistency of timing of payments between reference portfolio vs insurance contracts

How to assess currency risk?

Select reference portfolio made up of investments in same currency as insurance contracts

Estimating FCFs → Grouping wrt Reinsurance

Estimate net

Net = Gross - Ceded

= (Direct + Assumed) - Ceded

Estimate gross & ceded separately

Gross = Direct + Assumed

Ceded

Net vs Gross/Ceded of Reinsurance → Considerations

DV-Re

Data availability

If sparse, hard to directly estimate PV of ceded CFs

CF Volatility

Diff segments of business may use diff groupings depending on volatility of CFs

Reinsurance Held

Consider type & consistency of reinsurance held

Segmenting data for payment patterns → Considerations

Business segments used for analyzing undiscounted liabilities

Payout period

Existence of predetermined payment schedule

Discount Rates → Characteristics

Reflect TVM, liquidity, & char of CFs of insurance contracts

Consistent w/ market prices for financial instruments w/ similar CF characteristics as insurance contracts

Exclude factors that don’t affect CFs in insurance contracts

Discount Rate → Bottom-up Method

Liquid, risk-free yield curve

Adj to reflect diff in liquidity char between financial instruments underlying risk-free rate vs insurance contracts

Discount Rate = Risk-free Rate + Liquidity Prem

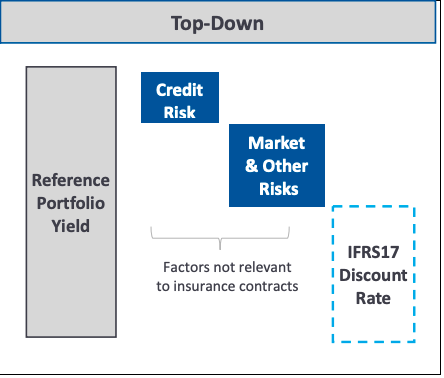

Discount Rate → Top-down Method

Yield to maturity of reference portfolio

Remove factors not relevant to insurance contracts

Ex: credit & market risk

Discount Rate = Ref Portfolio Rate - Credit/Market Risks & Other Adj

Advantage/Disadvantage of Top-down Method

Advantage: doesn’t need liquidity prem

Disadvantage: complexity of deriving & adjusting reference portfolio rate

*Opposite for bottom-up

Ex of Credit Risk

Default risk

Downgrade risk

What is considered risk-free?

Gov bonds

Liquidity Prem → Combined Approach

Top-down Discount Rate = Ref Portfolio Rate - Credit Risk - Market Risk

Market risk = 0 if only bonds

Ind Asset Liquidity Prem (ALP) = Top-down Discount Rate - Risk-free Rate

Liquidity Prem = r x ALP + c

Contract Features that affect Liquidity

Exit Costs

Ex: surrender penalties

Higher = less liquid

Inherent Value

Ex: payments the contract holder expects to receive

Low inherent value = more liquid

Exit Value

Large portion of inherent value paid @ exit = more liquid

Less liquid = _____ liquidity prem

Higher

Types of Insurance Contract Liabilities

Liability for Incurred Claims (LIC)

Liability for Remaining Coverage (LRC)

More liquid → no claims occurred yet so easier to cancel

Basis for Varying Liquidity → LRC vs LIC

LRC: ability to cancel before expiry & receive value w/o significant exit costs

LIC: ability to obtain exit value in advance of “normal” payment dates

Direct → ability of policyholder

Reinsurance → ability of purchaser of reinsurance

Reference Curve

standardized yield curve used for comparisons in the unobservable period (30+ years)

Locked-in Yield Curve

Determined at initial recognition of group of contracts OR @ date of incurred claims

Used when:

PAA approach w/ significant financing component

Where are insurance expenses reported in the Income Statement?

Insurance service expense

Insurance finance expense

Insurance Finance Expense

Change in carrying amt of group of insurance contracts from effect & changes in:

TVM

Financial Risk

Unwinding of Discounts

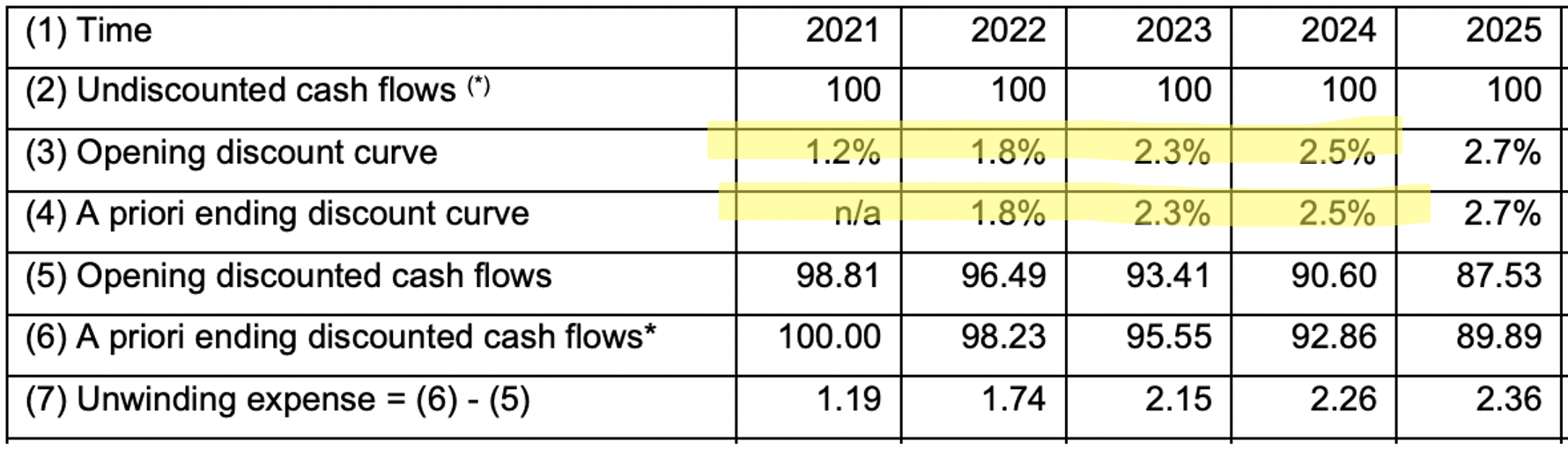

Diff between discounting CFs to beginning vs end of period

Unwinding = Ending CF - Opening CF

Unwinding of Discounts → 3 Methods

Constant Yield Curve

Uses same discount curve @ beginning & end of period

Unwinding using Spot Rates

Ending discount curve = beginning discount curve shifted by 1 period

Expectation Hypothesis

Term structure of interest rates is solely determined by market expectations of future interest rate changes

Unwinding → What’s the Ending discount curve for first year?

0%

Ending disc CF = Undisc CF

Why can’t insurer use own assets as Reference Portfolio?

Diff in Liquidity between Insurer’s Assets vs Insurance Contract Liabilities:

Insurers usually invest in liquid assets

LIC is illiquid due to inability to obtain exit value before normal payment dates

Benefits of using single Liquidity Curve for both LIC & LRC

Fewer curves to manage → could reduce # of curves by half

Operationally simpler bc less calculations