ACIS Exam 2 Studying

1/68

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

69 Terms

Descriptive Analytics

Analytics performed that characterizes, summarizes, and organizes features and properties of the data to facilitate understanding.

Brief summaries (or factoids) of a data-set that provide a representation of that data as a whole. Generally classified as measures of central tendency or measures of variability.

First step in data analysis performed before diagnostic, predictive, or prescriptive analytics.

What happened? What is happening?

Finds anomalies.

Explains in detail what happened, faithfully representing the substance of what actually occurred without bias or error.

Different tools/techniques:

Pivot tables & charts

Ratio analysis (including DuPont ratios)

Plotting data visually

No requirement that this is done before other analyses (diagnostic, predictive, prescriptive) but often first step performed to begin to address a question of any type.

Accounting needs to be…

Analytics performed that characterizes, summarizes, and organizes features and properties of the data to facilitate understanding.

The four primary financial statements and other financial reporting items provided in an annual report or in a 10K submission to the SEC include:

Balance Sheet

Income Statement

Statement of cash flows

Statement of stockholders’ equity

Footnotes

Balance sheet

Reveals the resources (assets) available for management to utilize and invest as well as who has claims on those resources (summarized as liabilities) and those investing equity (as summarized in stockholders’ equity) at the balance sheet date

Income statement

Summarizes the company’s revenues and expenses during the year (or accounting period); reports income earned and taxes paid.

Statement of cash flows

Reveals the cash inflows and outflows during the year (or accounting period)

Statement of stockholders’ equity

Explains the changes in retained earnings from net income or losses and any (cash) dividends paid to investors

Footnotes

The footnotes to the financial statements provide details on the following:

Expected annual cash paymetns associated iwth long-term debt and lease paymetns

Accounting policies chosen:

Inventory method

Depreciation method

Pension plan assumptions

Segment performance, including sales and oeprating income by segment.

Stock market performance

Other 10K filing information

The 10K has infomration beyond the annual report such as management compensation (stock options and stock ownership), board compensation, biographies of the board (prior background, how long they’ve been on the board, etc.), and board committee membership.

Measures of central tendency include:

Mean, median and mode: Summary measures of the central tendency of the data.

Medians are usually most useful when there are extreme, or skewed, observations (as often shown by extreme minimums or maximums)

By looking at HR data for a period of time, the results can be organized to calculate the average employee salary. However, the data can be skewed by including outliers such as CEO salary, which is generally many times more than the average employee earns.

Measures of variability include:

Minimums, maximums, standard deviations

Minimums/maximums

Summary measures showing extreme values to help explain what happened

By sorting sales data from smallest to largest, you can easilysee the minimum and maximum refunds made last month

Were there any journal entries that had negative numbers (that might be found by looking at minimums), that might be erroneous?

What was the highest stock price in the past 52 weeks? What was the lowest stock price in the past three months?

Standard deviations

Summary measure that shows the extent of the variability for the sample or population

What is the standard deviation of the company’s stock price over the last quarter?

Quartiles

Division of data observations into four defined intervals based on data values as way of comparing to the overall data set

In what quartile does Ford fall based on its leverage compared to the automobile industry as a whole

Deciles

Division of data observations into 10 defined intervals based on data values as way of comparing to the overall data set.

Percentiles

Division of data observations into 100 defined intervals based on data values as way of comparing to the overall data set.

Counts

The number of occurrences of a certain data item or event.

Totals, sums, subtotals

Summary measures of the data

Graphs (line, bar, column charts)

A diagram showing interrelationships between two or more variables

Percentage change

The extent to which a data item gains or loses magnitude or value

Pivot tables

A tool that allows reorganization and summarization of certain data using cross-tabulations without changing the underlying spreadsheet (or data)

Histogram

Display of rectangles with area proportional tot he underlying frequency of the data

Ratio analysis

Quantitative analysis of financial statement items to help evaluate liquidity, solvency, profitability, and efficiency of the underlying company.

Vertical analysis

Expresses financial informaiton in relation to some relevant figure or base.

Descriptive analysis

Used to examine financial performance over a period of time, explaining what happened this year as compared to the year before.

Horizontal analysis

Provides comparative changes about various line items of each financial statement over time.

Displays the dollar and percentage change in financial statements from one period to the next.

Examples of Descriptive Analytics

Descriptive analytics of financial performance using tables and graphs

Considering the right comparison group for analysis

Descriptive analytics using pivot tables and bar charts for accounts receivable aging

Profitability by customer and SKU (individual product)

Horizontal, vertical, and DuPont anaysis of financial performance

Using descriptive analytics to identify phenomena that mgiht require additional analysis, including diagnostic analytics

Pivot chart

Visualization of summarizations included in the pivot table

Percentage change (increase or decrease)

(New - Old) / Old

DuPont Ratio Analysis

Summarizes and disaggregates company performance and can help answer the important question of what happened.

Originally created by the DuPont Corporation to decompose performance (return on equity) into three component parts: profitability (profit margin), activity (asset turnover), and solvency (financial leverage) ratios.

Return on equity, return on assets

Return on equity

Profit margin (net income/sales) x Asset turnover (sales/total assets) x Financial leverage (Total assets/equity)

Measure of profitability generated for each dollar of stockholders’ investment defined as net income (aka net profit) divided by stockholders’ equity, or net income/sales.

Return on assets

Sometimes done for return on assets instead of return on equity (ROE).

A measure of profitability for each dollar of resources (assets) available for management to use, computed as net income / total assets.

Profit margin (net income/sales) x Asset turnover (sales/total assets).

Histograms

Most part expected to be normal (bell curved symmetric about the mean)

Just below 0 → missing observations/lower expected frequency (suggesting anomaly)

Just above 0 → extra observations (higher than expected frequency, also suggesting anomaly)

Descriptive analytics leads to additional questions:

Why would this be?

Did managers make this happen?

Do managers not like small losses? Do they prefer small gains?

Do managers use the flexibility within accounting standards to make earnings higher (or lower) than the expected? If they do manage earnings, how do they do that?

What incentives do they have to manage earnings up or down? To maximize bonus? To maintain a string of positive earnings?

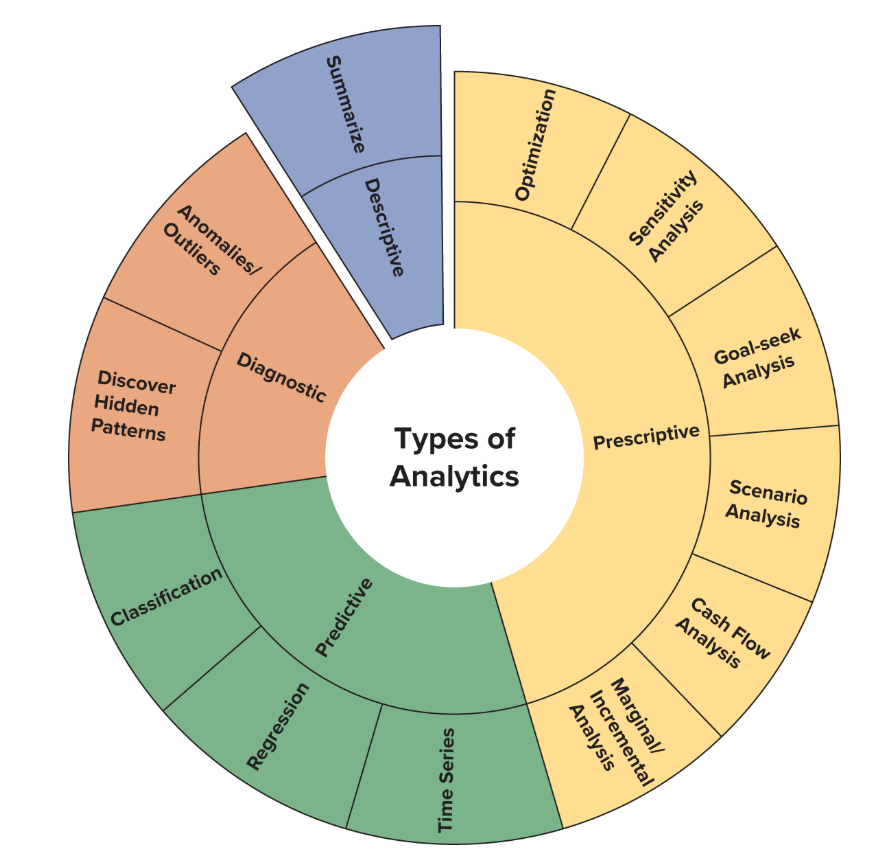

Types of analytics

Sparklines

Brief visuals that fit within one cell in Excela nd visually depict what happens in the cells next to it.

Accounts receivable aging

Popular technique used to determine if credit sales are ultimately going to be collected (or collectible).

The longer the receivable is due and outstanding, the lower the likelihood that the receivable will ever be collected. (Greatest amount of receivables would be in the earliest days due to this)

Diagnostic Analytics

Why did it happen?

What are the reasons for past results?

Analytics performed to investigate the underlying reasons for past results that cannot be answered by simply looking at the descriptive data.

Two categories

Anomalies/outliers - identify unusual, unexpected results or transactions

Discover hidden patterns

Performing drill-down analytics - by looking for patterns in the underlying data set or an external dataset, we can identify potential correlations. Looks for underlying patterns in the data by examining the data at a more detailed level.

Performing statistical analyses - looks to uncover patterns in the data or how data moves together

Considered to help management decide next steps in a rational way rather than based on emotion

Can also be performed through the use of hypothesis testing, either investigating a difference in means or using regression to understand a relationship between the independent and dependent variables.

Anomaly

Something that departs, or deviates, from the norm or the expectation.

Could tell us why something happened

Outlier

Similar to an anomaly

Observation or data point that lies outside its expected distribution

Could be error, fraud, or truth

To detect an anomaly or an outlier…

It is important to establish the norm or expectation

Expectation could be:

Standard cost (estimated cost of producing a good or service)

GAAP (generally accepted accounting principles)

Performance by similar companies or performance by the industry as a whole

Management by exception

The practice of bringing specific issues to the attention of management if they depart from expectation

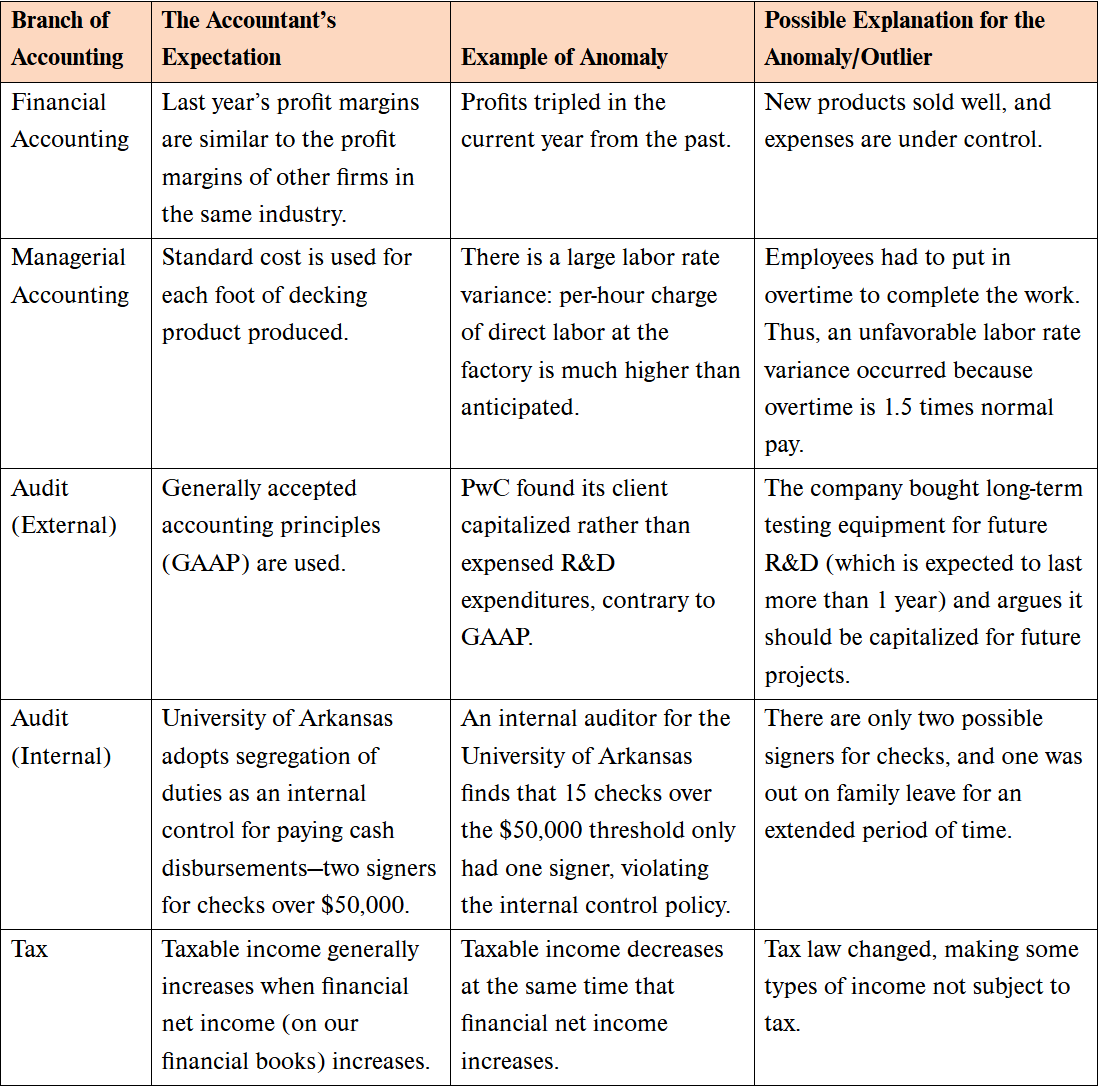

Accountant’s expectation, example, and possible explanation

Diagnostic analytic techniques for identifying anomalies and outliers

Testing for separation of duties

Unusual activity

Duplicate transactions

Fuzzy matching

Sequence checks

Performing:

Bank reconciliations

Variance analysis

Benford’s law

Internal controls testing - separation of duties (segregation of duties)

A common internal control that requires more than on eperson to complete accounting tasks to help prevent fraud and/or errors from occurring. It is important to separate:

Custody of assets

Authorization of hte use of the assets

Recordkeeping

Using diagnostic analyses to evaluate the segregation of duties (or other internal controls)

Was there a violation of the segregation of duties?

Were some large cash disbursements approved by someone who also had recordkeepign responsibility or who had custody of the assets, violating the company’s internal controls of the segregation of duties?

If there was a violation of the segregation of duties, why did it occur?

Was it fraudulent or an error or were there extenuating circumstances that would justify or excuse the violation?

Internal controls testing - unusual weekend, holiday, or end of the quarter accounting activity

Sometimes unusual transactions occur on holidays, weekends, or end of the quarter (end of accounting period), when it is harder to find approval and authorization for certain transactions.

Diagnostic analyses - evaluating holiday, weekend, or end-of-the-quarter activity

Was there abnormal weekend, holiday, or end-of-the-quarter activity?

Were there a large number of transactions that occurred on those dates, and did they have proper authorization?

If there were a lot of abnormal weekend, holiday, or end-of-the-quarter accounting activity, why did it occur?

What was the nature of the transactions?

Was it fraudulent or an error or were there extenuating circumstances that would justify or excuse the violation?

Testing for duplicate transactions

Occassionally, invoices (or other transactions) are recorded twice on the same date, for the same amount, and with the same vendor. We call these duplicate transactions.

If receive error message from accounting system stating that invoice has already been processed → they will gain assurance that the system is working properly.

Were there duplicate invoices (or other transactions) recorded twice on the same date, for the same amount, and with the same vendor?

If there were dplicate invoices, why did it occur?

What was the nature of the transactions?

Why are there duplicates of some transactions in the financial reporting records? Are tehy fraud or just errors?

Fuzzy Matching

A technique used to find potential equivalents when there is less than an exact fit.

Were there any close or fuzzy matches of employee, vendor, or customer names?

If there were fuzzy matches among employee, vendor, or customer names and addreses, why did it occur?

What was the nature of the transactions?

Was it due to fraud, error, or just a coincidence?

Tolerances can be set to note how close of a mathc is close enough - 50, 70, or 80%

Tolerances too low - Type 1 error

Tolerances too high - Type 2 error

Sequence check

An analysis to see if the key number field i the record is in the correct ascending or descending order.

Were there any sequence gaps?

If there were sequence gaps, why did they occur?

What was the nature of the transactions?

Was it due to fraud, error, or just a coincidence?

Bank reconciliation

A type of diagnostic analytics for identifying anomalies is reconciling the cash account in the general ledger to the bank statement. Helps identify transactions on the bank statement that do not correspond with the company’s general ledger and vice versa.

Potential reconciling items include:

Outstanding checks → checks written by the company but not yet processed by the bank

Outstanding deposits → deposits recorded by the company but not yet processed by the bank

NSF checks → checks reported as received by the company, but the bank does not recognize them becasue the check writer has insufficient funds

Electronic funds transfer (wire transfer) → transfers received by the bank but not yet reflected by the company

Notes (loans made to customers collected by the bank) and interest (owed on notes from the customers and collected by the bank) → the company may nt be aware of the amounts of these items until it receives the bank statement

Bank service fees → fees the bank charges for its services and checking accounts. the bank deducts these fees directly from the company’s checking account. The company may not account for the fee until it receives the monthly bank statement

Errors → sometimes made by the company ro the bank in recording a transaction. Accountants find these errors by comparing the amounts for each transaction on the general ledger and each transaction on the bank statement

Expectation and anomaly

Cash balance at the bank is te same amount as cash balance in the general ledger

The cash balance at the bank is not the same amount as the cahs balance on the company’s general ledger. Why?

Variance analysis

Management accountants need to perform this to identify and explain the difference between a budget amount (or standard costs) and actual performance. The anomaly would be the difference or variance form what was expected.

Price variance

Variance due to the changing price of materials

Quantity (or usage) variance

The company used too many mateirals to produce each product than it budgeted to use.

Labor rate variance/quality

Labor rate being lower or higher than expected, hours worked higher or lower than budgeted

Fixed manufacturing overhead variances/variable manufacturing overhead variances

Consider the impact of overhead costs that are different from expectation.

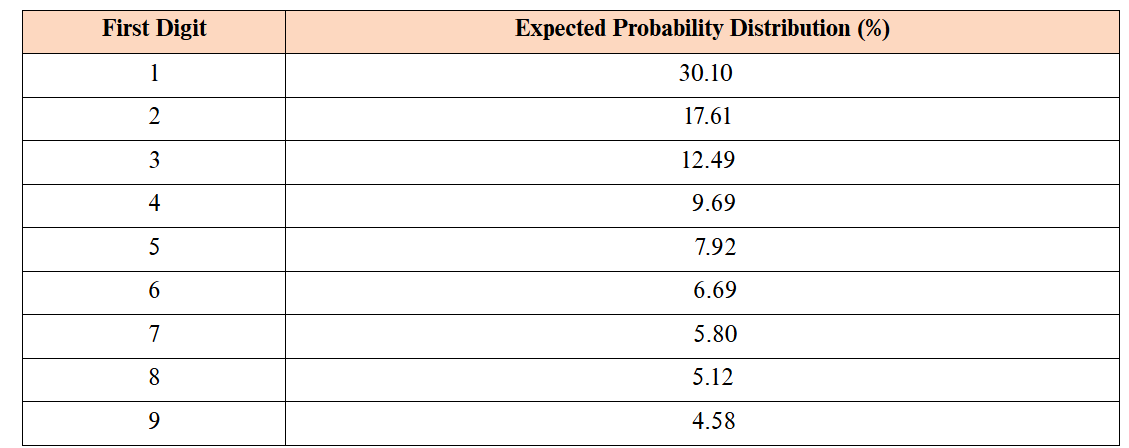

Benford’s law

The principle that in any large, randomly produced set of natural numbers, there is an expected distribution of the first, or leading, digit.

More numbers in a population of numbers start with 1 than any other digit, followed by those that begin with 2, then 3, and so on.

Any time there is a limitation placed on naturally occurring datasets, the dataset will usually violate Benford’s law

Examples of accounting based data that in general conform with Benford’s law

Earnings per share

Earnings

Sales

Forecasts of earnings by financial analysts

Total assets of the fortune 500 or russell 3000, etc.

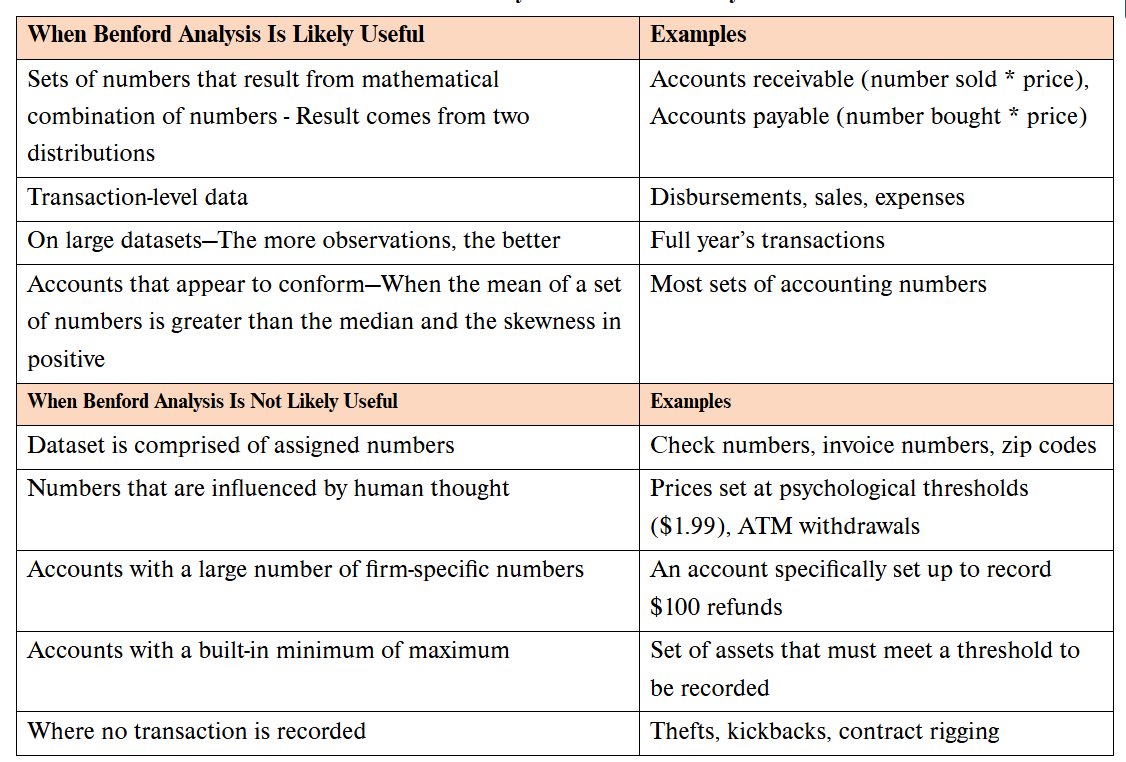

When Benford’s law is useful and when it isn’t

Drill down analytics

Looks for underlying patterns in the data by examining the data at a more detailed level.

Peeling each layer of an onion and deciding whether it is reasonable and/or feasible to go down one more layer to understand the pattern.

Analysts can identify potential correlations

Examples of drill down analytics

Analysis of the highest owning customer

By having more infroamtion about what individual customers owe, we will have a better idea of the deb’s collectability

Analysis of the most profitable customer

Company can better work and cater to these customers and work to make unprofitable customers more profitable

Analysis of the most profitable product

Company can bette prmote them to its customers

Analysis of the relationship between accounts payable clerks and its vendors

Looking to detect relationships within a data file that could be potential indicators of fraud

See if there is any unusual relationships between them

If an A/P clerk is paying one vendor more quickly, perhaps the vendor is also providing some favors back to the A/P clerk such as a kcikback scheme or side payment to the A/P clerk for this and other favors

Sunk cost fallacy

Commitment to past investments made escalates and makes it harder to abandon prior investments that may no longer be profitable even if it may not make rational sense.

Determining statistical linkages, patterns and relationships among variables using statistical tools and techniques

It is important to determine this.

Looking at events that identified anomalies may uncover hidden relationships

Correlation, tests of differences in means, regression analysis, cross-tabulations, filtering, and time-series data analytics can all be useful techniques for uncovering hidden or unknown patterns, or stories, in the data

Two-sample t-test difference of means

One way of uncovering causal relationships is to form hypothesis of what you expect will or will not occur.

Used to determine if the means of two different populations are the same or statistically different from each other.

Regression

A basic technique used in diagnostic analytics that allows the accountant to evaluate whether a specific dependent variable outcome value is related to independent variable inputs

Determining the relationship between two sets of variables when we believe that one variable is dependent on the other.

Diagnostic analytics summary

Attempts to address the question of why something happened

Break down into 2 broad categories

Exploring anomalies and outliers (including a discussion of how the expected amounts are determined)

Drilling in to the detail using various tools and techniques

Techniques:

Benford’s law

Bank reconciliations

Fuzzy matching

Sequence checking

Duplicate payments

Predictive analytics

Analytics performed to provide foresight by identifying patterns in historical data and assessing likelihood or proabability.