4.9 - Task sensitive preferences

1/22

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

23 Terms

Task sensitive preferences

The idea that standard economic preferences are misleading because we assume preferences exist independently

TSP is where you don’t have preferences at all until you have a decision in front of you

Therefore preferences are only formed in light of this decision

‘Constructed preferences’

inherently comparative preferences

deeper sense of comparison required for the formulation of preferences

Cant calculate attractiveness of a lottery unless you have one to compare it to

cant formulate lottery value or its utility

Salience theory and inherently comparative preferences

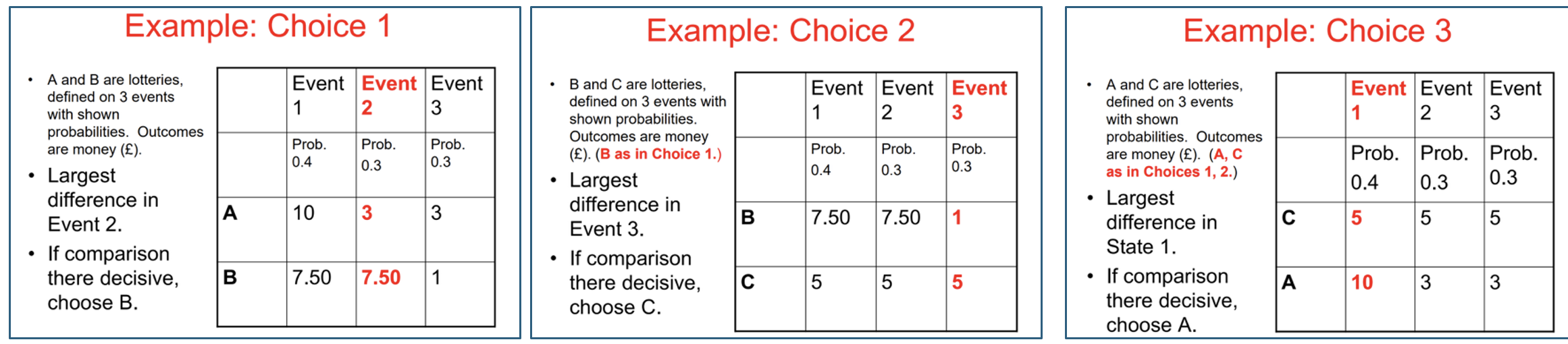

Agent chooses the option that has the best outcome in the event in which the outcomes of the options differ most

No option assessable without knowing the other option.

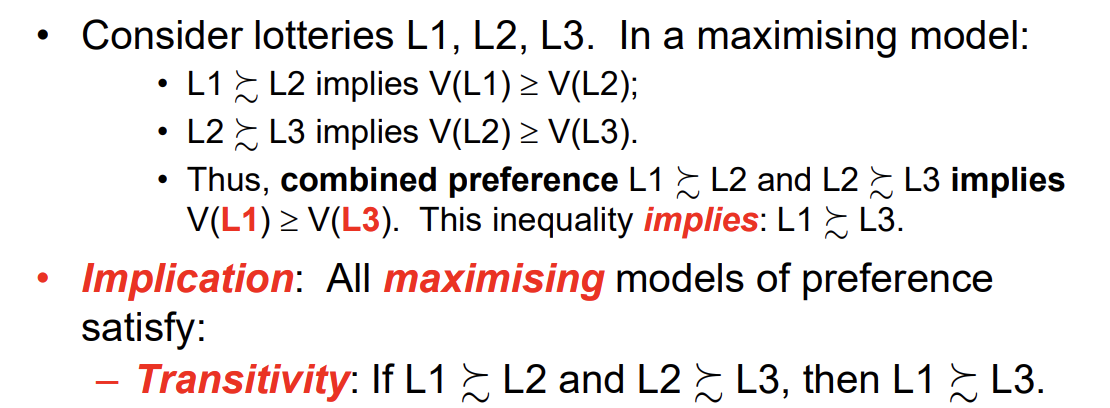

Transitivity & lotteries

inherently-comparative preferences & Intransitivity: Loomes et al. (1991) - OV

Agent is putting more weight on 1 event in each case but it’s a different one in each 3 choices - relative weights vary across choices even though probability doesnt

Preference cycle only goes in 1 direction if intransitive

Wasnt set up to test salience theory (regret theory & preference reversal - PC in only 1 direction)

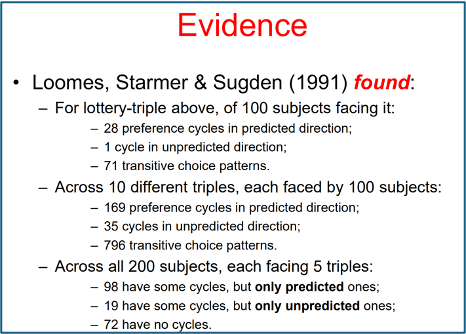

inherently-comparative preferences & Intransitivity LSS (1991) - Results

80% had transitive preferences

Of 20% intransitive, majority in predicted direction

of 200 subjects, most had at least 1 cycle of intransitivity

almost ½ of all subjects in predicted direction

inherently-comparative preferences & Intransitivity - LSS (1991) vs other studies

LSS just 1 study - other studies vary in how much intransitivity is found

depends on how decisions presented

LSS set up study to over emphasise events with large outcome differences

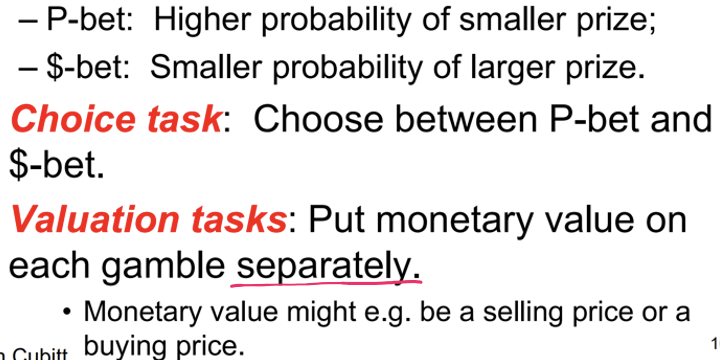

Preference reversal

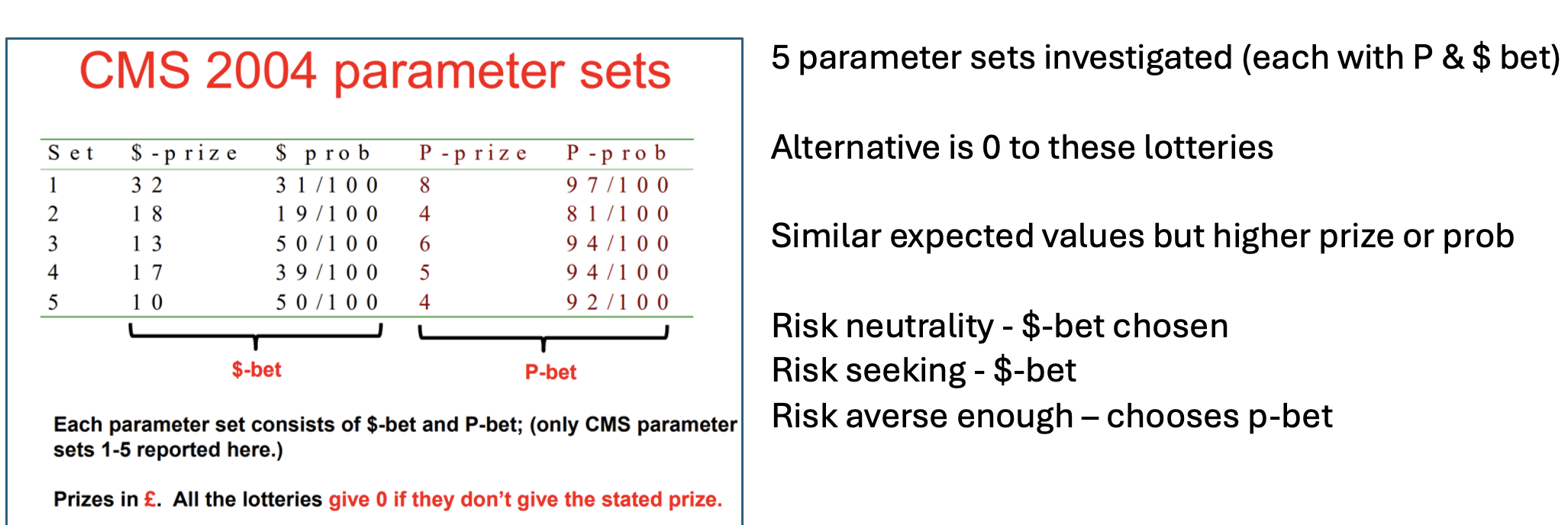

2 choices with similar expected value - Choice depends on risk aversion

Systematic tendency for subjects to choose P-bet in choice task but put higher value on $-bet in the valuation tasks (standard PR)

Observed preference differ when inferred from choice or valuation (buying OR selling L)

PR is highly robust / replicable

not incentive or inexperience cause

Cubitt et al. / CMS (2004) - OV

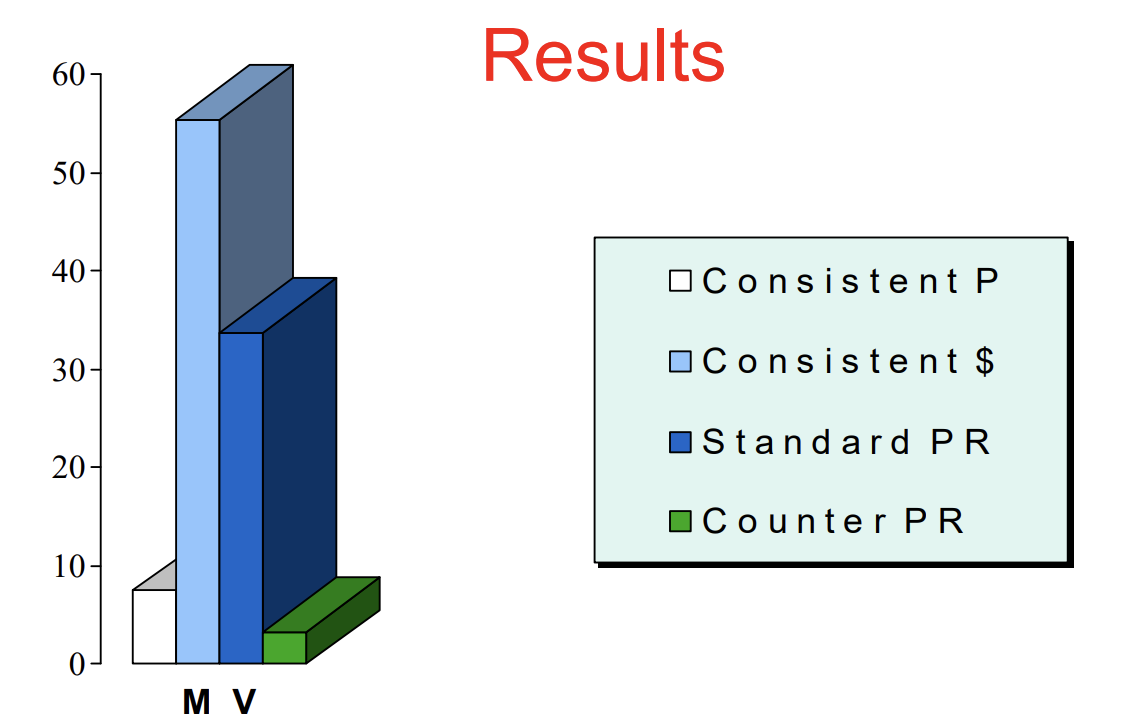

CMS (2004) - Results

MV - Monetary value

Sum of left 2 (consistent) – just over 60%

~40% committed either reversal - Standard PR more frequent

Almost no preference reversal if $-bet chosen in choice task

Extensive evidence that PR is robust

PR scepticism

PR first seen in 1960-70s by Slovic & Lichtenstein

Both lab + field (casinos in Las Vegas)

Economists initially sceptical – lots of criticism

Grether & Plott criticised a lot and tried to repeat on their own

Found PR in own experiment – overwhelming majority shown when choosing p-bet

“Taken at face value, the data are simply inconsistent with preference theory ….. . The inconsistency …. suggests that no optimisation principles of any sort lie behind even the simplest of human choices.”

PR causes

Incentives

Procedure invariance

Intransitivity - PR without PI violation

Regret aversion (Salience T sorta reason)

Loss aversion (Sugden 2003)

Scale-Compatibility hypothesis (Tversky et al. 1988)

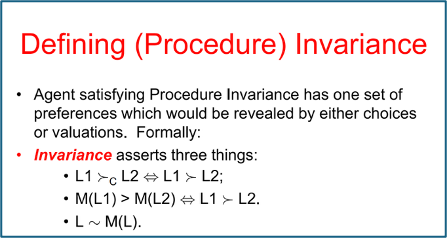

Procedure invariance

Preferences are unaffected by the procedures used to elicit them

Preferences are independent of the tasks they face

PR as Artefact of incentives

Within-subjects design usually used, so need to incentivise all tasks without distorting them

1 random round (RLIS) incentive or BDM mechanism

assumes independence axiom and subject will ignore the other tasks when making a choice

if PR found then D-Q problem says RLIS may have distorted choices (no clean explanation)

These incentive structures are valid experimental procedures if subjects rely on EUT → PR could just be regular Allais paradox interacting with incentive structure

use an OPS to get around this

PR as Violation of assumption of Procedure Invariance

Elicited preferences depend on how they are elicited

Valuation vs choices give different preference

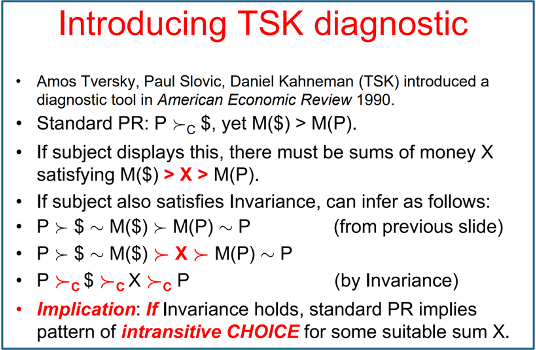

PI vs intransitivity test

>c = strict preference revealed by a choice

Standard PR: P >c $ BUT M($) > M(P)

If subject displays PR & satisfies PI then subject must have PC

P > $ ~ M($) > M(P) ~ P

Therefore PR caused by intransitivity

Tversky et al. (1990) - OV

use X as sum of money between M($) & M(P)

Then give agent option of X & M(…) or P/$

If subject satisfies PI but also shows PR then must be intransitive preferences

Used OPS to avoid independence axiom but Cubitt et al. showed that still requires it at the meta level

TSK (1990) - RESULTS

TSK find only 10% explained by this – intransitivity not main cause

preference cycle in majority predicted direction

Sugden (2003) - OV and results

Theoretical paper

In choice task preferences elicited with reference that subject owns neither lottery

in valuation the subject ‘owns’ one of the L - gives their WTA to sell it

losing $-bet is a bigger ‘loss’ than P-bet

Loss aversion causing the higher valuation of $-bet

Scale-Compatibility hypothesis (Slovic et al. 1990)

The way in which an individual is required to respond to a task can affect the weights that he or she places on particular dimensions of alternatives being evaluated

valuation tasks require a money amount as output → individuals place particularly high (low) weight on the money (probability) dimension

leads to inflated $-bets

Chu & Chu (1990) - OV and Results

Exposed preference reversers to ‘money pumps’

had their stated preferences implemented across a series of trades

Experimenter used arbitrage of their choice and valuation which ultimately resulted in monetary losses if PR chosen

Led to PR being avoided quickly

Market experience of 1 PR gamble also carried forward to other PR gambles → PR avoided

PR and monetary payoffs - Slovic et al. (1990)

Prevalence of PR is substantially reduced by using nonmonetary payoffs

more PR also found with real payoffs compared to hypotheticals

PR and time preferences

PR still found when looking at dynamic problems

Tversky et al. (1990) studied choices between delayed payments

found people chose the shorter delay option but valued the longer delay one higher