CFA Level I - Formulas

1/460

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

461 Terms

MAD

Mean Average Deviation =

|xi - xbar| / n

Employee share-based compensation (stock option/stock grant): how is it recorded on P&L? How are the values estimated?

Recognised as an expense on P&L over the vesting period. (Ie period between grant date and vesting date)

The value of a stock option must be approximated using a valuation model.

A stock grant → value depends on mkt value of a share

Employee: Stock options - how are they valued (what is a vesting date?)

Stock option is valued using valuation models (different from normal stock options).

Vesting date is first day employees can exercise

CV

Coefficient of Variation, aka. “relative dispersion”

= sd / mean

Harmonic Mean (And when to use it?)

Geometric Mean formula?

Now rank harmonic, geometric, and arithmetic by size.

Sum all the observations using 1/x

Take the number of obs, n, and divide by the previous result

Use this in case of needing to find “average price per share”. E.g. 1000$ invested in stock market every year, but stock market is priced differently every year, so greater weight need to be placed on cheaper years.

Geometric mean = [(1+r1)(1+r2)…]1/n -1

The arithmetic mean is largest, followed by geometric, then harmonic (follows the alphabet A, G, H)

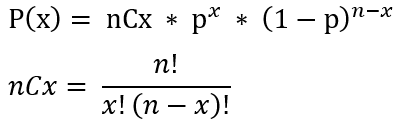

Binomial Probability

NOTE: 2nd + is the nCr function on TIBA

SE of Sample Mean

sd(x) / sqrt(n)

IQR and Location of Percentile

Q3-Q1 ; (Percentile)(n+1)

e.g. 12th percentile of 900 observations would occur on the 108th position

Multiplication Rule of Probability

P(AnB) = P(A|B)P(B)

If independent, P(AnB)=P(A)P(B) since P(A) = P(A|B)

Standard deviation formula

sqrt(sum(x-xbar)²)/n-1)

Variance of a portfolio

Varp = w1² var1² + w2² var2² + 2* w1w2 cov(1,2)

z-score formula

z = x-bar - mu / sigma

F statistic formula

“Master of Real Estate”

MSR/MSE

MSR = SSR/k-1

MSE = SSE/n-k

Correlation formula

cov(a,b) / σaσb

Covariance formula

sum(xi - xbar)(yi - ybar) / n-1

PED

%dQ / %dP

GDP Deflator

Nominal/Real *100

Fisher eqn

nominal = real + inflation

Balance of payments

BoP = Current Account + Capital Account + Financial Account

Forward rate from spot rates (And what does it imply?)

Fwd/Spot = 1+rspot / 1+rbase

(Implies: You cannot make risk-free profit by choosing:

investing for the longer maturity at the spot rate, versus

investing for the shorter maturity, then reinvesting at the implied forward)

Remember that rbase goes in the base!

Double-declining balance

1/number of years uselife life * 2 is the percent multiplied to the carrying value each year to get the depreciation value. STOP once you reach the salvage value

e.g. asset with value $1000 and disposal value of $200 useful life of 4 years, under straight line depreciation would be charged $200 per year. under DDB, ¼ = 25%, therefore first year depreciation expense is 50%, i.e. $500

Basic EPS

Net Income - Pref. Dividends / WA Shares Outstanding

Diluted EPS (If-converted method)

Diluted EPS is used when there are potentially convertible shares, or debt interest. NOTE that the denominator adds any common shares from CONVERSION. You do NOT add preferred shares.

ALSO NOTE: always calculate basic EPS as well. If Basic EPS < Diluted EPS, use Basic EPS as the reported Diluted EPS. Basically, Basic EPS forms a ceiling on Diluted EPS.

Debt Ratio

Total Debt / Total Assets

Leverage Ratio

Total Assets / Total Equity

Quick Ratio (Acid Test)

Cash and equivalents + Marketable securities + Receivables / Current Liabilities

Cash Ratio

Cash and equivalents + Marketable securities / Current Liabilities

FCFF and FCFE (Write both; Compare the two)

Free Cashflow to Firm = NI + Noncash Charges - Capex - Change in WC + interest(1-t)

Equivalently… FCFF = CFO – Capex + Int(1-t) .

Free Cashflow to Equity = NI + Noncash Charges - Capex - Change in WC + Change in debt

Equivalently … FCFE = CFO - Capex + Change in Debt

FCFE = FCFF - Int(1-t) + Change in Debt

Interest coverage ratio

= EBIT / Interest payments

Reinvestment ratio

CFO / Cash paid for long term assets

Real exchange rate

(Nominal exchange rate)*(Pf / Ph)

Where nominal exchange rate is expressed in home ccy/foreign ccy

Change in real exchange rate

dReal Exchange Rate = dNominal Exchange Rate + dP foreign - dP home

Debt Payment Ratio

LT Debt Repayments / CFO

Dividend Payout Ratio

Common-share dividends / Net Income (attributable to common shares)

Investing & Financing Ratio

CFO / CFF + CFI

Receivables Turnover

Revenues / Avg Receivables

Payables Turnover

Credit Purchases / Avg Payables

Which should be approximated as… COGS+dInventory / Avg Payables

DSO

Days Sales Outstanding

= 365 / Receivables Turnover

= 365 * (Avg Receivables / Revenues)

DOH / DIH

Days on Hand (Days Inventory on Hand)

= 365 / (Inventory Turnover)

= 365 * (Avg Inventory / COGS)

Days Payables

365 / Payables Turnover

= 365 * (Avg Payables / Credit Purchases)

i.e. 365 (Avg Payables / COGS + dInventory)

Inventory Turnover

COGS / Avg Inventory

Cash Conversion Cycle

DSO + DIH - DP

(Acronym: CCC = S+I-P)

ROE (State the simple formula, along with the 3 and 5-part breakdown)

ROE = Net Income / Avg Equity

ROE = (Net Income / Revenue) * (Revenue/Assets) *(Assets/Avg Equity)

(Net profit margin)*(Asset Turnover)*(Leverage Ratio)

ROE = (NI/EBT)*(EBT/EBIT)*(EBIT/Revenue)*(Revenue/Assets)*(Assets/Avg Equity)

(Tax Burden)(Interest Burden)(Operating Margin)(Asset Turnover)(Leverage Ratio)

Asset Turnover

Revenue/Total Assets

List the DTA/DTL formulae (wrt to tax paid/tax expense? wrt to income tax expense vs tax payable? and also the change in DTL/DTL formula)

DTA is generated when Tax expense < Tax paid ; DTL when Tax expense > Tax paid.

DTA is generated when income tax expense < tax payable. DTL is generated when income tax expense > tax payable.

DTA is generated when carrying amount < tax base. DTL is generated when carrying amount > tax base.

Tax Expense = Tax Paid + dDTL - dDTA

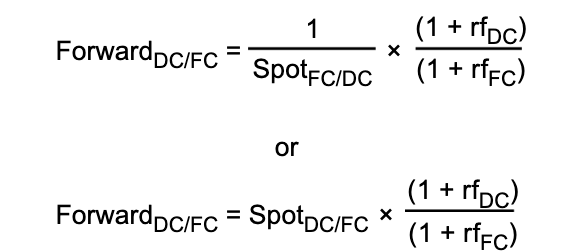

Forward/Spot rate relation for FX

(1+rhome) = Spothome/foreign * (1+rforeign) *Forwardforeign/home

Therefore,

Note in the image all the ‘home’ terms are in the numerator

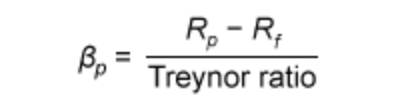

Systematic risk calculation

Systematic risk is defined as BETA

it is also known as market risk.

Beta = Cov(Rm,Rasset)/Varm = Corrm x SDasset / SDm

Alternatively, you can derive it from Treynor:

See image. Rp-Rf/Treynor = BETA

Macaulay Duration for FRNs

A FRN is a floating rate note, i.e. at each ‘reset date’, a new floating rate is calculated and that rate is used to pay the interest (+ a margin)

MacDurFRN = (Days Between Resets - Days Since Last Reset) / Days Between Resets

Ethics Standard I(A) - Knowledge of Law

Means you must comply with legislation. In conflicts of different laws, apply the stricter one.

The ‘applicable law’ is always the stricter of: law in place of residence or place of business.

If the applicable law is less strict than CFA guidelines, always choose CFA guidelines. If CFA guidelines are less stringent, choose the applicable law.

Standard I(B): Independence and Objectivity

DO NOT offer/accept G&E that could compromise independence/objectivity

Standard I(C): Misrepresentation

Do not spread untrue information, omit information, misrepresent your firm, or give misleading recommendations.

Plagiarism: Not permitted to claim authorship of others’ work. However, you can use and distribute research reports as long as it is cited - this includes not only emails but also in-person and video communication

Work completed for employer: Past employee’s research may be used (do not claim authorship); it is the firm’s proprietary work

Standard I(D): Misconduct

Do not lie, cheat, steal, or act dishonestly - this differs from I(A) as it governs all ‘misconduct’ beyond legal matters.

In essence, act in a professional manner that reflects the profession best. Some violations may be breaching both I(A) and I(D).

e.g. While it is legal to have alcohol, being under the influence and making investment decisions reflects poorly on professionalism.

Standard I(E): Competence

Members/candidates have a responsibility to update their knowledge to remain competent. A ‘negative’ outcome from an investment recommendation does NOT imply failure to adhere to I(E)

This one is more about staying relevant to ensure delivering best advice to clients.

Geometric Mean Return (and when/why do we use it?)

[(1+r1)(1+r2)(1+ …)]1/n - 1

→ allows for compounding of return and accounts for different amounts invested each year

Standard II(A): MNPI

Do not act on, inform others on MNPI to use for trading (are allowed to, however, in CDD or loan underwriting or other contracted duties). This includes failing to prevent others from gaining access to and acting on MNPI when they do not need it.

Information considered material when the equity price or valuation is likely to be affected by such info - incl. earnings, M&A, major developments…

Information considered nonpublic when it has not been released in a press release or on company website.

Mosaic theory: You may use all public information, along with nonmaterial nonpublic information, when conducting research. It is not a violation to pay for or be paid for such research - and such research does not need to be made public before acted upon in trading.

Money Duration (formula from ModDur)

ModDur * Full Price

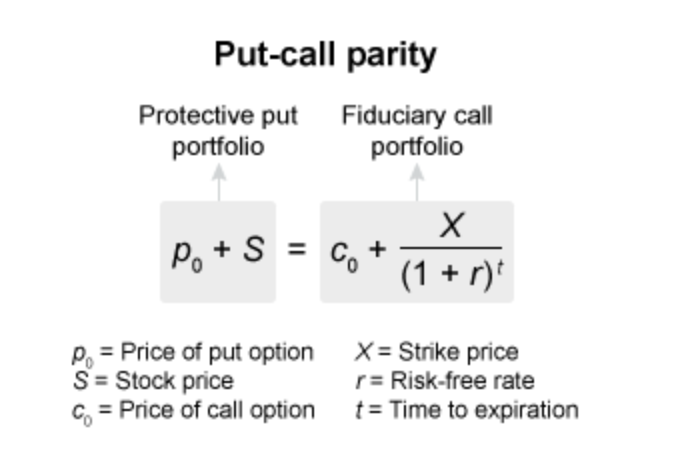

What is put-call parity? Write the formula too.

Put-call parity applies only to European call options. A protective put (a put + a share) should always have the same strike price and expiration as a fiduciary call (a call + a bond)

CML properties

Capital market line

> Relates only to portfolios on efficient frontier. X-axis is the standard portfolio deviation, measuring total risk

SML properties (Assets plotting below the SML are considered … undervalued or overvalued?)

Security market line

> Relates to ALL security portfolios, regardless of efficiency. X-axis is the systematic risk (Beta) it is the graphical representation of the CAPM line!

Assets plotting above SML are undervalued. Plotting below SML are overvalued

Porter’s five forces

threat of new entrants

barg power of suppliers

barg power of buyers

threat of substitutes

rivalry among existing competitors

Portfolio ModDur/MacDur steps?

Find the market value of each bond in the portfolio (Par value * Price)

Find the total market value of the portfolio

Divide MVbond by MVportfolio to find the weight of each bond

Multiply the weight by the ModDur/MacDur

Standard II(B): Market Manipulation

Do not pump and dump, do not manipulate markets by disseminating false info

The key is whether there was an intent to deceive. By disclosing, you can usually mitigate the “deceit” argument.

Standard III(A): LPC

Loyalty, prudence, and care to customers - remember that this standard only pertains to clients.

PUT CUSTOMERS INTERESTS FIRST, above employers and self interest

more responsibility required in custody-type relationships

any direct client instructions should be followed - albeit important to discuss the details if it conflicts with mandate - seek best price available

act in client interest in proxy votes

Standard III(B): Fair dealing

Do not discriminate against any client. It is permitted to set-up different ‘service levels’ provided this is disclosed

Material changes, such as revisions, shd be disseminated to all clients at best-effort time

Oversubscribed securities: Attempt to pro-rate available slots

Standard III(C): Suitability

Always consider client needs. Think about whether an investment suits the IPS (investment policy statement) and whether an investment decision fits the mandate.

Standard III(D): Performance presentation

Present performance information credibly and reliably. Do not alter calculation methodologies without disclosure and only do so with reason.

NEVER exaggerate returns and NEVER imply that past results lead to future earnings. Phrases like “you can expect to earn…” is misleading and against the policy

Standard III(E): Confidentiality

Keep info confidential unless client explicitly allows sharing. Or if required by law. Or if client is breaking the law.

Standard IV(A): Loyalty

Be loyal to employer by acting in their benefit.

Always inform employer if doing side hustles.

If switching jobs, do not contact existing/potential clients to solicit for business until AFTER you have left.

Whistleblowing: Always, always follow the law in whistleblowing. Then, the next priority is of clients/markets - whistleblowing should not be for personal gain!

Why are forward/futures priced different to spot?

Convenience yield: When the asset is expected to earn above the riskfree return, the amount ‘extra’ is the convenience yield. This reduces a forward/future price as it makes spot more valuable.

Storage costs: Make it more attractive to buy forward/future than spot - since you need to pay for storage on spot after receiving the item.

Standard IV(B): Addtl Compensation Arrangements

Always disclose / receive permission from employer before receiving or giving G&E which may impede on objectivity and independence

other clients DONT need to be informed..

Standard IV(C): Responsibility of superiors

Supervisors have the responsibility for their subordinates to uphold the CFA Code and Standards, along with applicable company regulations and local laws

Ensure that compliance procedures are easy to follow and well-documented. Keep subordinates trained and up-to-date on such procedures.

Standard V(A): Diligence

Exercise diligence, independence, thoroughness in analysing and creating research theses

i.e. Do your homework! On the things you are recommending.

Make sure you understand the model. And its assumptions and risks.

Do due diligence on external advisers/research, if used

Standard V(B): Communications with Current/Prospective Clients

This standard applies only to client-facing members/candidates

Remain transparent about services provided - along with costs

Disclose cost structure changes

Disclose general format/principles that are used to form investment recommendations

Disclose limitations and risks to clients

Distinguish fact from opinion

Standard V(C): Record retention

CFA recommends (NOT requirement) keeping records for at least 7 years, unless local laws say for longer.

Retain records that pertain to buy/sell/hold, research, or investment conclusions

Capture and forward digital media to firm (all work related content)

Standard VI(A): Avoid/disclose conflicts

Where possible, avoid conflicts of interest (COI)

If unavoidable, make the disclosure. Do not use COI for personal gain.

COI may exist within a firm between departments. Make sure what you are doing is not a COI.

Stock ownership: Owning a stock as an investment manager may be a COI if you intend to market that stock to clients

Directorship: Definite no-no, because your duty as a director (reporting to shareholders) differs from your duty as a investment manager (reporting to clients)

Diluted EPS (Treasury stock method)

Treasury stock method: for stock options. ie usually employee stock options - when a strike price is breached…

you must calculate how much cash inflow the company receives when the options are converted, and then how much the company buys back - the assumption is they use all proceeds to buy back.

The net new shares is added to the denominator.

Treasury stock

…Is treated as a negative equity in accounting. It is when a company buys back common shares issued.

Therefore when calculating equity remember to subtract treasury stock away.

Debt to capital ratio

Debt/(Debt+Equity)

CAPM (write formula and name each component)

Capital asset pricing model - calculates the expected return based on market risk premium, systematic risk, and riskfree rate

CAPM = Rf + B(Rm - Rf)

Pricing vs valuation (For bonds? For swaps?)

bonds: pricing is done at issuance, means setting the coupon rate which makes par=price

valuation is done after issuance, coupon is fixed, market yield (YTM)changes - evaluating whether the bond has gone up or down in value

swaps: determining the fixed for floating /vice versa rate that makes the swap value=0 at inception. valuation is done after the swap begins, the rate is predetermined - valuation helps to calculate who owes who what

price-weighted index vs value-weighted index vs equal-weighted vs fundamental index?

price-weighted: higher stock priced companies are weighted higher. if stock A trades at $90 and stock B trades at $10 then A is 90% and B is 10% of the portfolio. never requires rebalancing! only adjustment for when stocks split.

value-weighted: higher market cap companies are weighted heavier. (ie adjusts price by shares outstanding). so it creates a momentum effect - winners are weighted heavier and losers have less exposure

equal-weighted: all companies weighted the same-overweights small cap and underweights large cap. requires freq rebalancing, contrarian effect

fundamental index: companies not weighted by share price but instead on fundamentals like sales, earnings, book value, cash flow. If share prices rise but fundamentals don’t … then value tilt

When forward FX rate > spot rate (for price currency)

What happens (appreciation or depreication? forward discount or premium? is the interest rate lower or higher in price country vs home country)?

It means that the

price currency is expected to depreciate against the base currency (i.e. base appreciates)

the base currency is trading at a forward premium to the price currency. (i.e. the price currency is trading at a forward discount to the base currency)

price country’s interest rate is higher than the home country’s.

What is an incurrence test

Negative covenant - basically means RATIOS that must be met before the company can issue more debt

What is limitations on liens

Negative covenant - restricts borrower from using the same asset as collateral in another facility

Pari passu

Means any additional debt issued by a borrower should have the same contractual rights as existing debt issued by that company with same seniority

What should you NOT consider during NPV/cashflow analysis?

Sunk costs

Financing costs

i.e. ask yourself: does including/not including this item cause cashflows to suffer/benefit?

Fiduciary call (And what is its value?)

Long European call option

Coupled with a long on a zero-coupon bond maturing on the option expiry date, face value = strike price of option

The value is equal the Call Option Premium+ Strike Price/Riskfree rate^t

Protective put

Long European put option

Long forward contract on underlying

Coupled with a long on a zero-coupon bond maturing when both the forward and put option expire, face vlaue = forward price

The value is equal the Put Option Premium + Fwd Price/Riskfree rate^t

How to convert from LIFO to FIFO?

Any LIFO reserves must be added to the inventory amount for the respective year. (This is because a LIFO reserve is exactly for this purpose)

An increase in LIFO reserve should be SUBTRACTED from COGS. (add any decrease to the LIFO reserve to COGS reported on the income statement.)

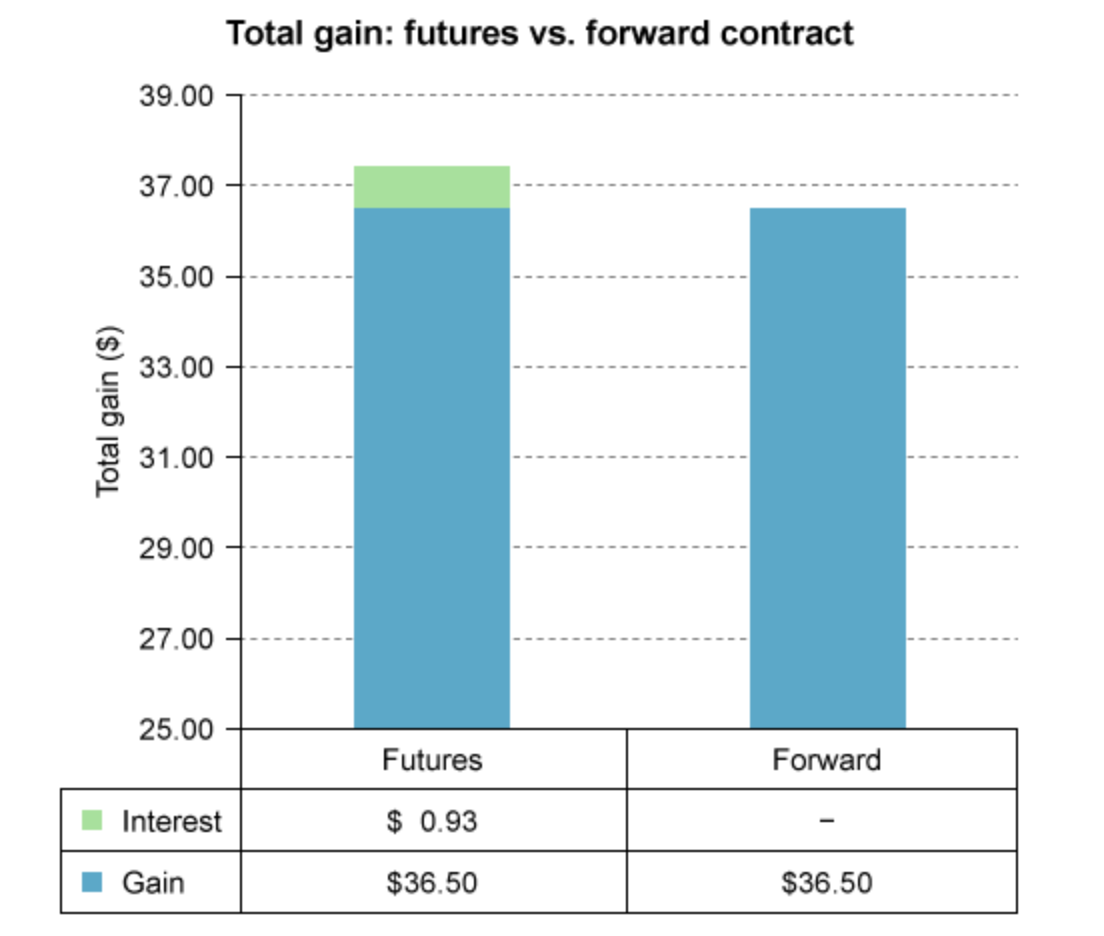

What is the key difference between futures and forwards? If interest rates are positively correlated with futures prices, which one is more advantageous?

Futures are settled daily and exchange-traded - therefore cashflows can be reinvested at a daily rate.

Forwards are not settled daily and OTC.

When interest rates and futures prices are positively correlated, futures are more advantageous as the daily CFs can be reinvested for more $ in the end.

A budget deficit = contractionary/expansionary?

Expansionary. This is because taxes are low / Govt spending high. i.e. expansionary

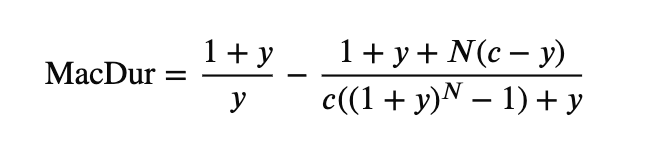

Closed form Macaulay Duration formula (ie how do we calculate MacDur?)

remember that y is the annual YTM. therefore for semiannual coupons, divide by two.

for N, use the number of periods of payment.

for c, use coupons per period. ie 3% if it is a “6% semiannual paid bond”

Add-on rate

is for money market instruments, especially commercial papers or bank deposits

AOR = (# Days in Year / # Days till Maturity) * (FV - PV / PV)

for a bond-equivalent yield, use 365 as days in year

Discount rate

For money market instruments, especially t-bills

DR = (# Days in Year / # Days till Maturity) * (FV - PV/FV)

for a bond-equivalent yield, use 365 as days in year

Nominal return formula

Nominal return means expected return.

1+Nominal Return = (1+riskfree rate)(1+inf rate)(1+risk premium)

treasury bills are considered the riskfree rate

Holding period return formula

when given two values and income?

when given rates?

and when leveraged?

[Income generated + (Final value - Initial value)] / Initial Value

Use geometric return. Ie [(1+r1)(1+r2)]^1/n

leveraged return = unlevered return + D/E(unlevered return - borrowing costs)

Approximate duration formula (when do we use it? what does it measure?)

Used for bonds without options

measures change in price due to change in YTM

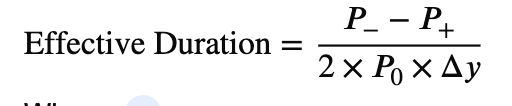

Effective duration formula (when do we use it? what does it measure?)

Used for bonds with options (EFFECTIVE = OPTIONS)

measures change in price due to change in yield curve

(dY is change in yield curve)

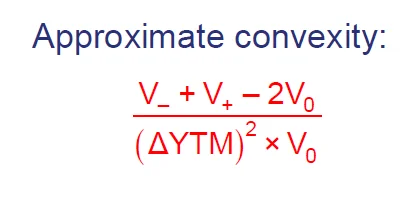

Approximate convexity (when do we use it? what does it measure?)

used for bonds without options

measures 2nd order (curvature) changes in price due to change in YTM

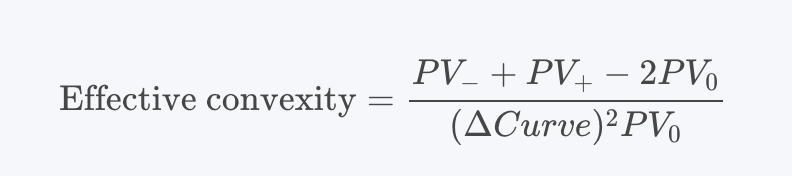

Effective convexity (when do we use it? what does it measure?)

Used for bonds with options (EFFECTIVE = OPTIONS)

measures 2nd order (curvature) changes in price due to change in yield curve