Economics: Market Structure

1/43

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

44 Terms

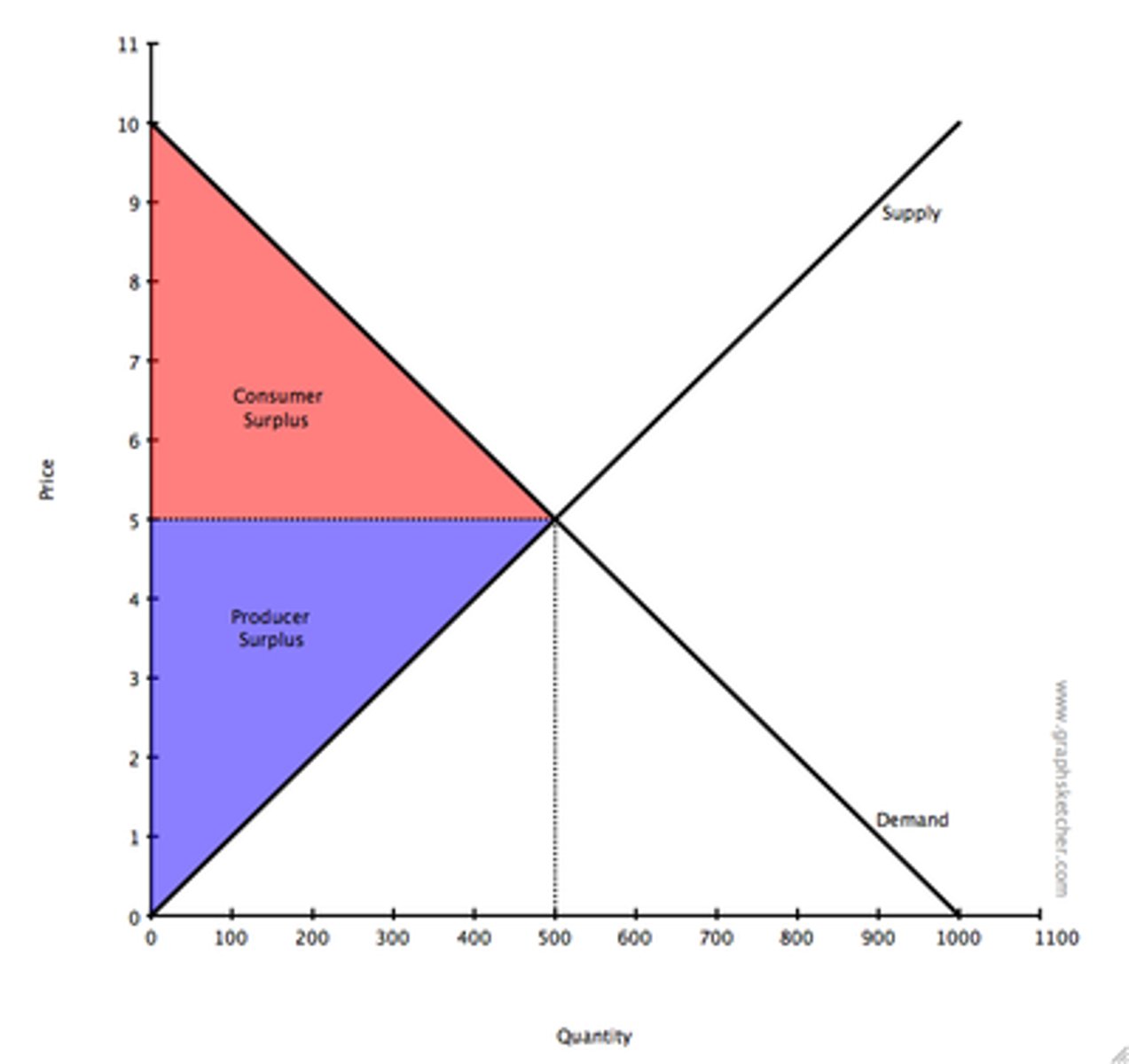

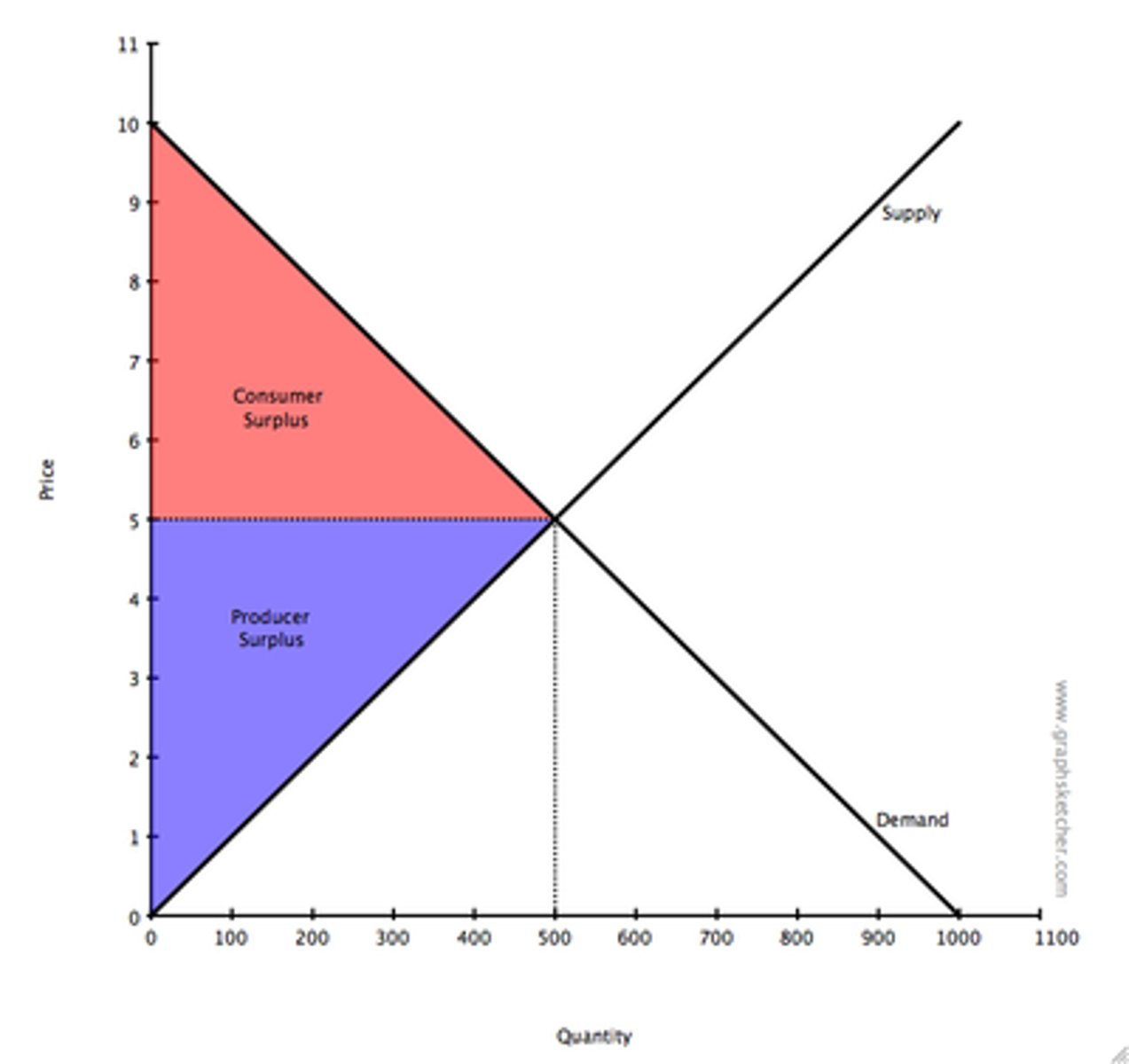

Consumer surplus

The total amount in excess of the market price that consumers would have been willing to pay to get the good.

Producer surplus

The total amount in excess of revenue in excess of the marginal cost of production that firms get at the market price (excess profits).

Perfect competition

Infinite number of small firms selling homogeneous products.

Perfect competition features

- Many buyers and sellers

- Homogeneous products

- Perfect information

- Free entry & exit to market

- Firms are price takers

Close examples of perfect competition

- Agricultural markets - milk, oats, wheat etc.

- Large markets - grand bazaar in Istanbul

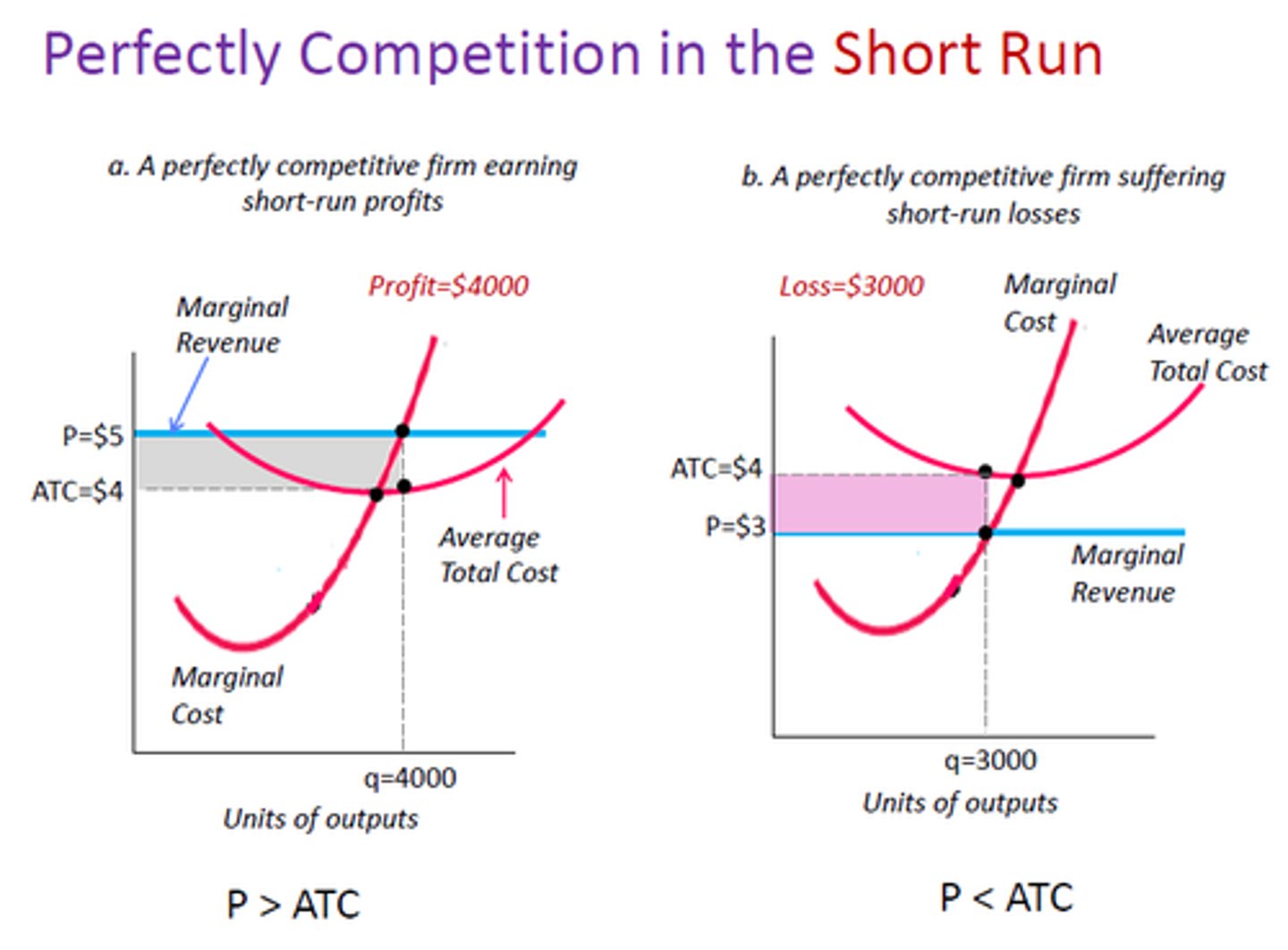

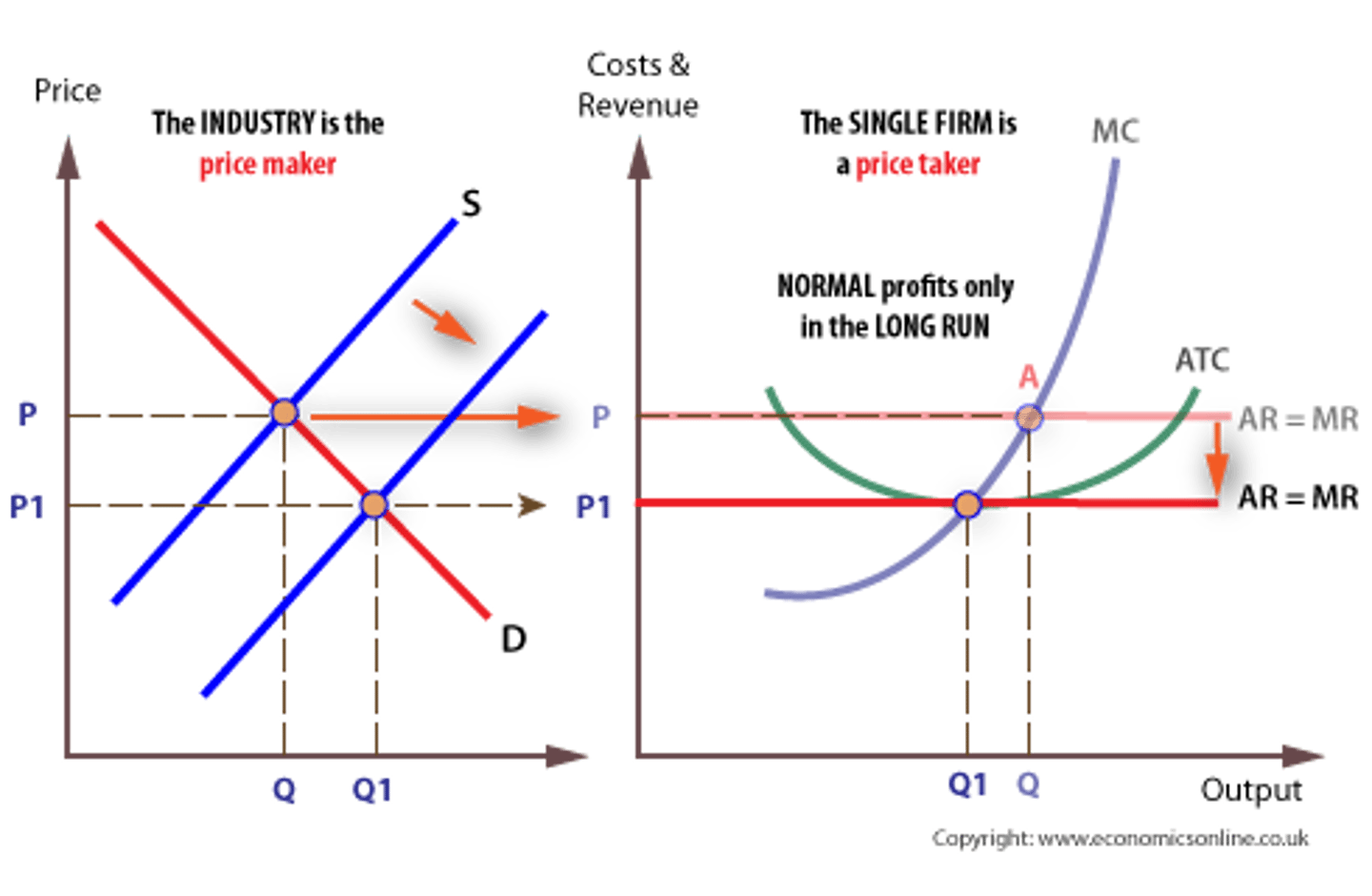

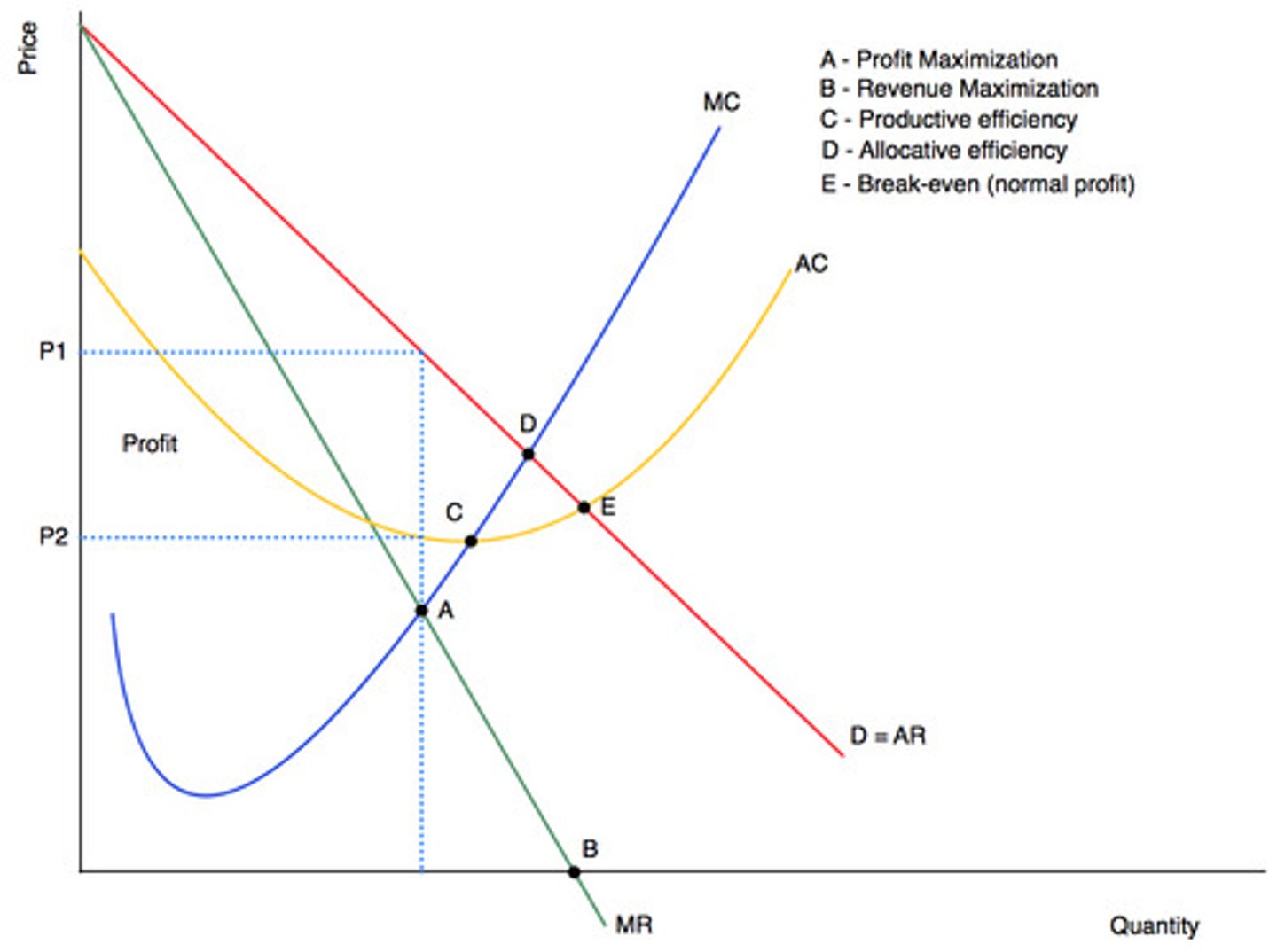

Short-run in perfect competition

A firm can earn 'abnormal' or 'economic profits,' BUT this makes the market attractive to other firms not within the market.

1. Given that there are no barriers to entry, businesses can easily begin production in the market

2. Industry capacity increases, shifting out the industry supply curve

3. Price received by each firm falls

4. Some firms exit the market

Long-run Perfect Competition

The long-run equilibrium is considered 'perfect' in the sense that each firm produces at the most efficient output possible.

Firms will earn normal profits that are only sufficient enough to keep them in the market.

Monopolistic competition

Large number of small firms selling differentiated products.

Monopolistic competition features

- Many buyers and sellers

- Heterogeneous products

- Close substitute products

- Perfect information

- Free entry & exit to market

Short-run in monopolistic competition

Abnormal profits / losses are possible

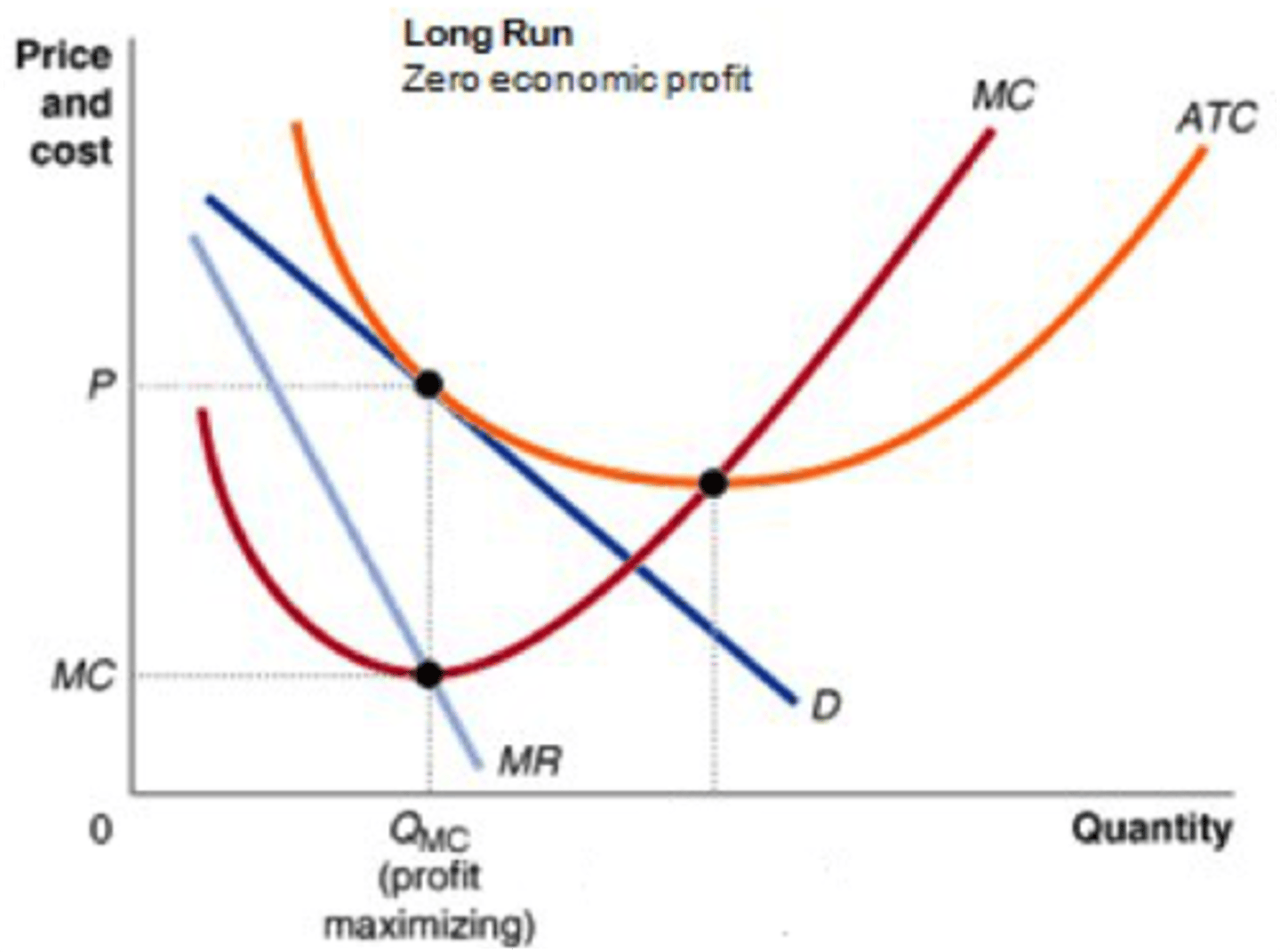

Long-run in monopolistic competition

Normal profits only exist in the long run due to the nature of the 'Tangency Equilibrium'

- Zero economic profit - P=AC

- Due to free entry/exist

Oligopoly

Few firms that share a large proportion of the industry.

Oligopoly features

- High concentration ratio (less than 7 firms)

- Heterogeneous products (price makers)

- High barriers of entry & exit

- Interdependence

Mutual Interdependence

The strategic actions of each firm in the market will have an impact on rival's sales and profitability (vice versa).

- Unique feature of oligopolies

2 Options for oligopolists

1. Interdependence of firms may lead them to collude and act like a monopoly - jointly maximising profits

2. Interdependence of firms may lead to competition and rivalry - maximising their own profits

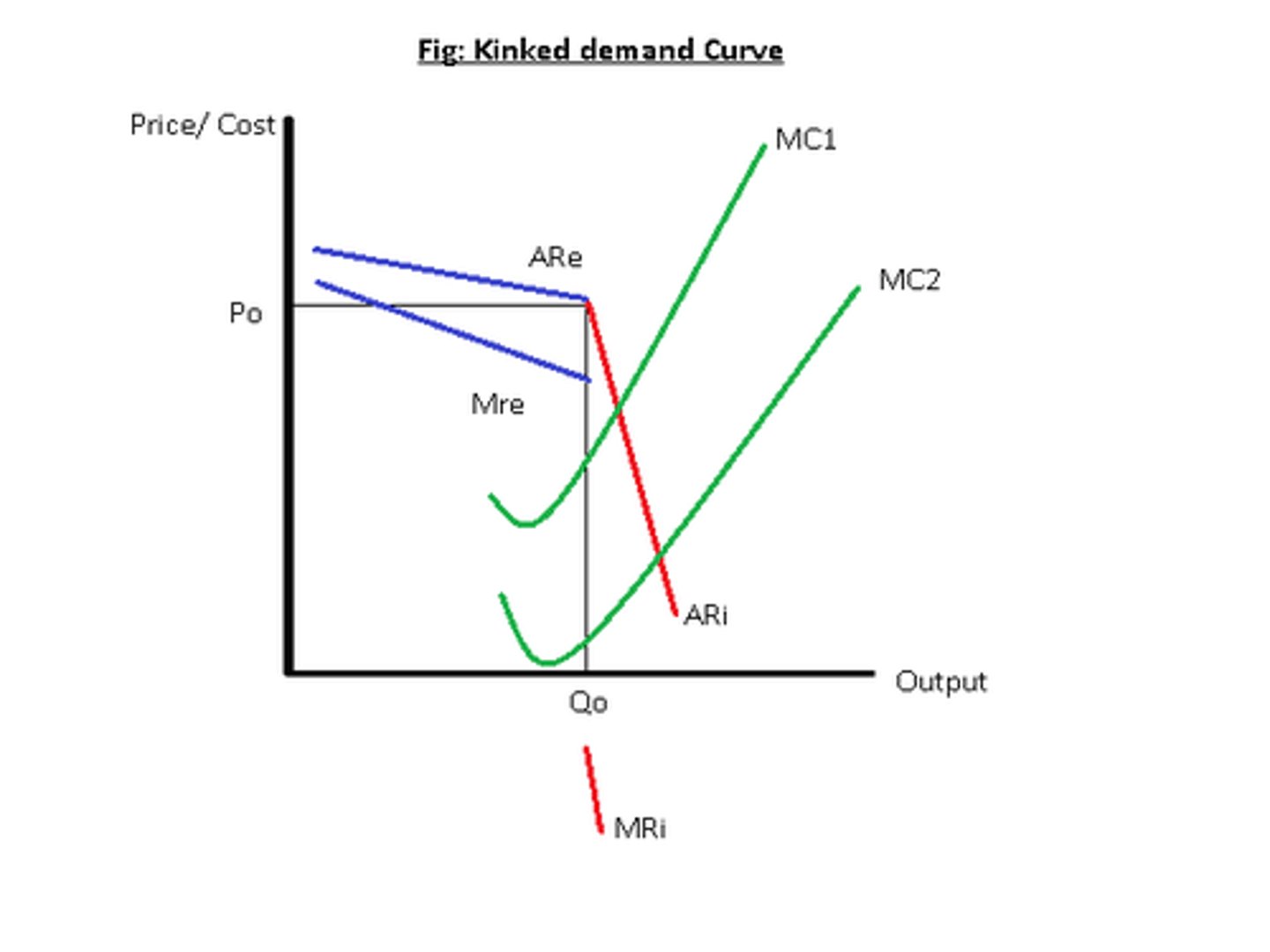

Kinked Demand Curve (Sweezy, 1939)

Built to explain price stability (sticky prices) in oligopolies.

- Price INCREASES from the prevailing market price will not be followed by competitors

- Price DECREASES from prevailing market price will be matched by competitors

Issues with the Kinked Demand Curve

- Price stability may be due to other factors

- The model lacks empirical observation

- Does not explain how prices are initially set - how does a firm arrive at P*?

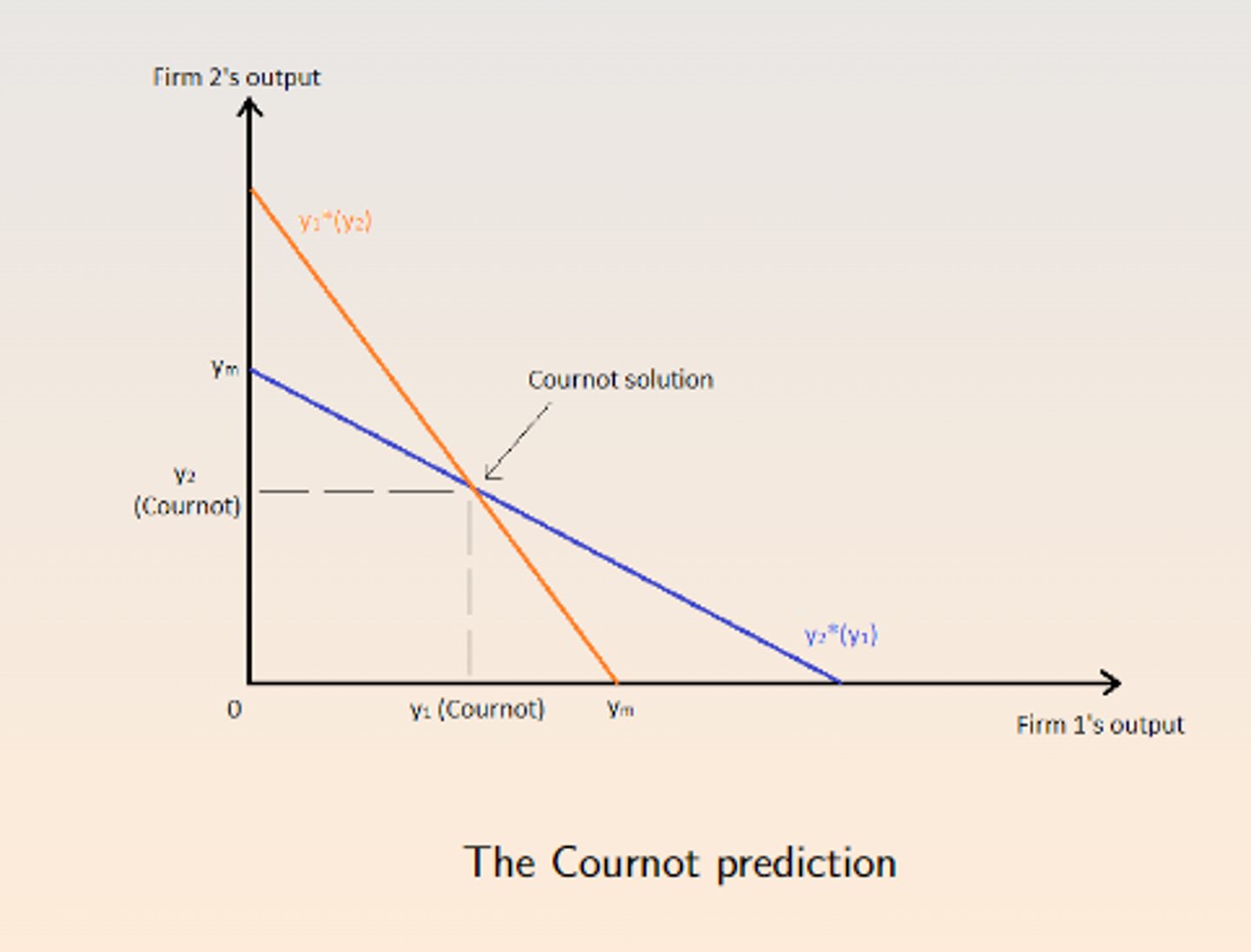

Cournot Oligopoly Model (Cournot, 1838)

A model of oligopoly that focuses output decisions of firms as the key strategic variable.

- Firms have to decide how much to produce

Assumptions made in Cournot Model

- Two firms (duopoly)

- Homogeneous products

- Equal marginal costs of production

Cournot Conjecture

Where each firm calculates its optimal output assuming that its rivals will not change its output from the previous period.

Residual Demand Curve (Cournot Model)

The amount of demand left for a firm once the other firm has sold its output.

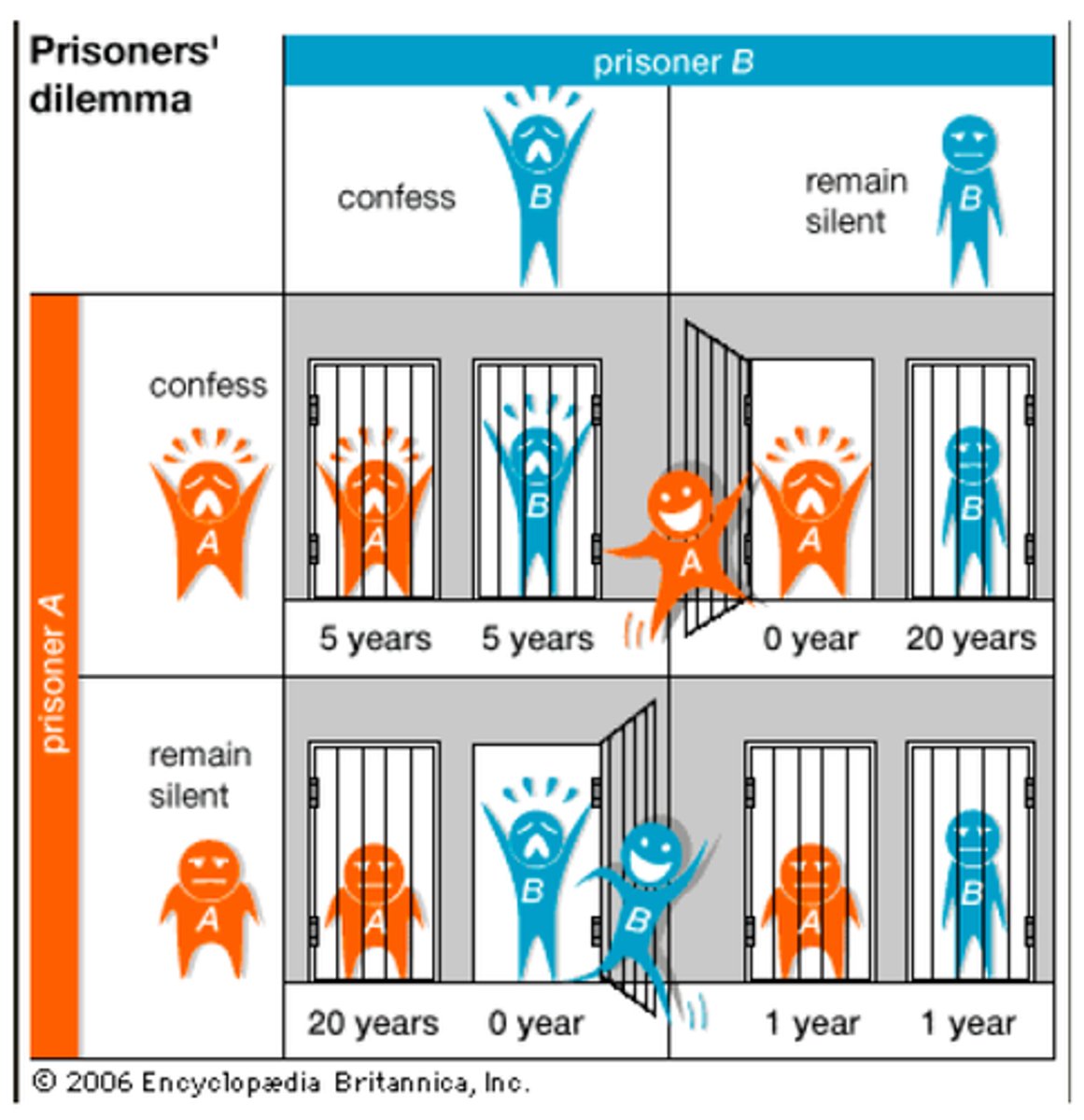

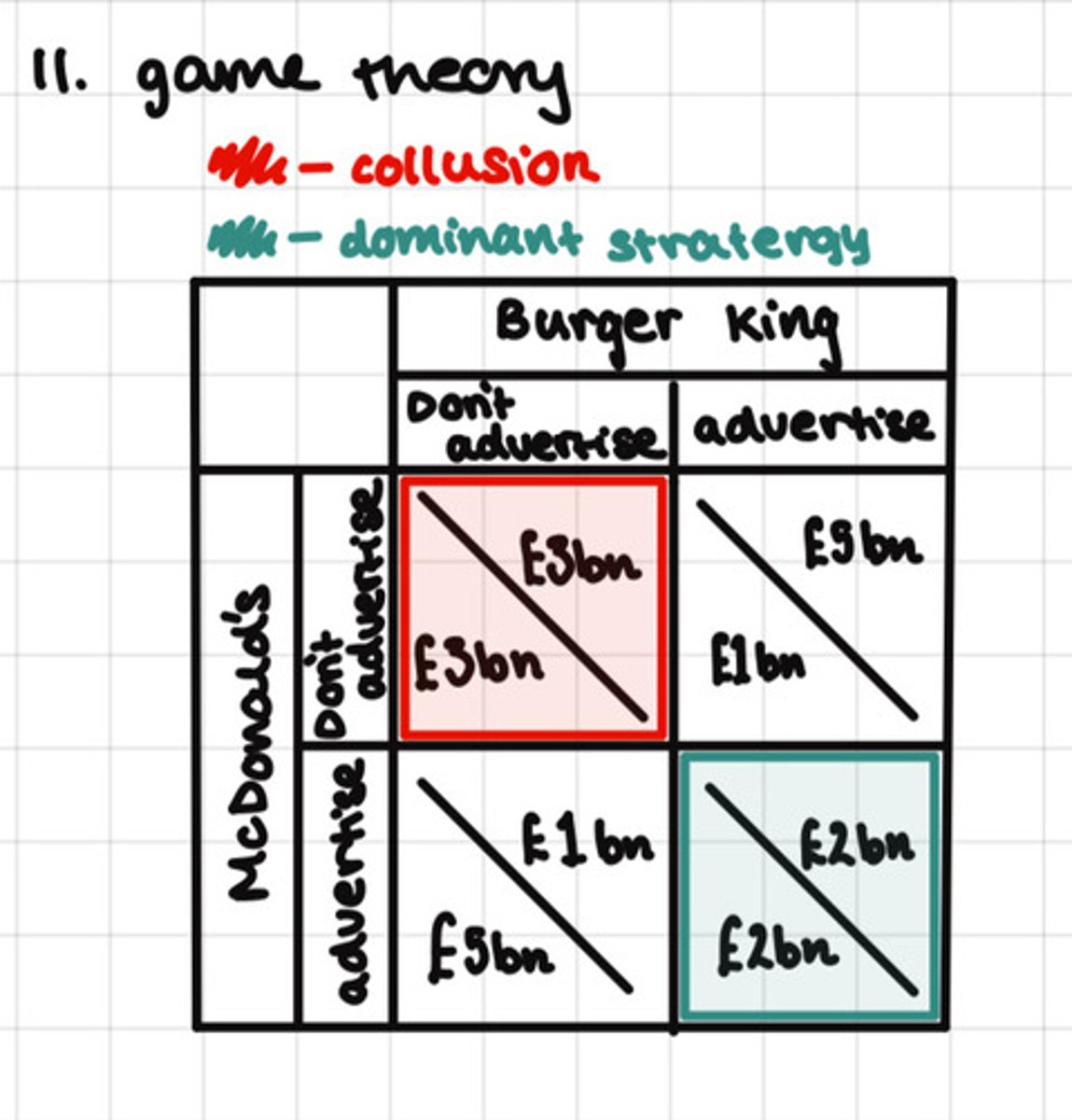

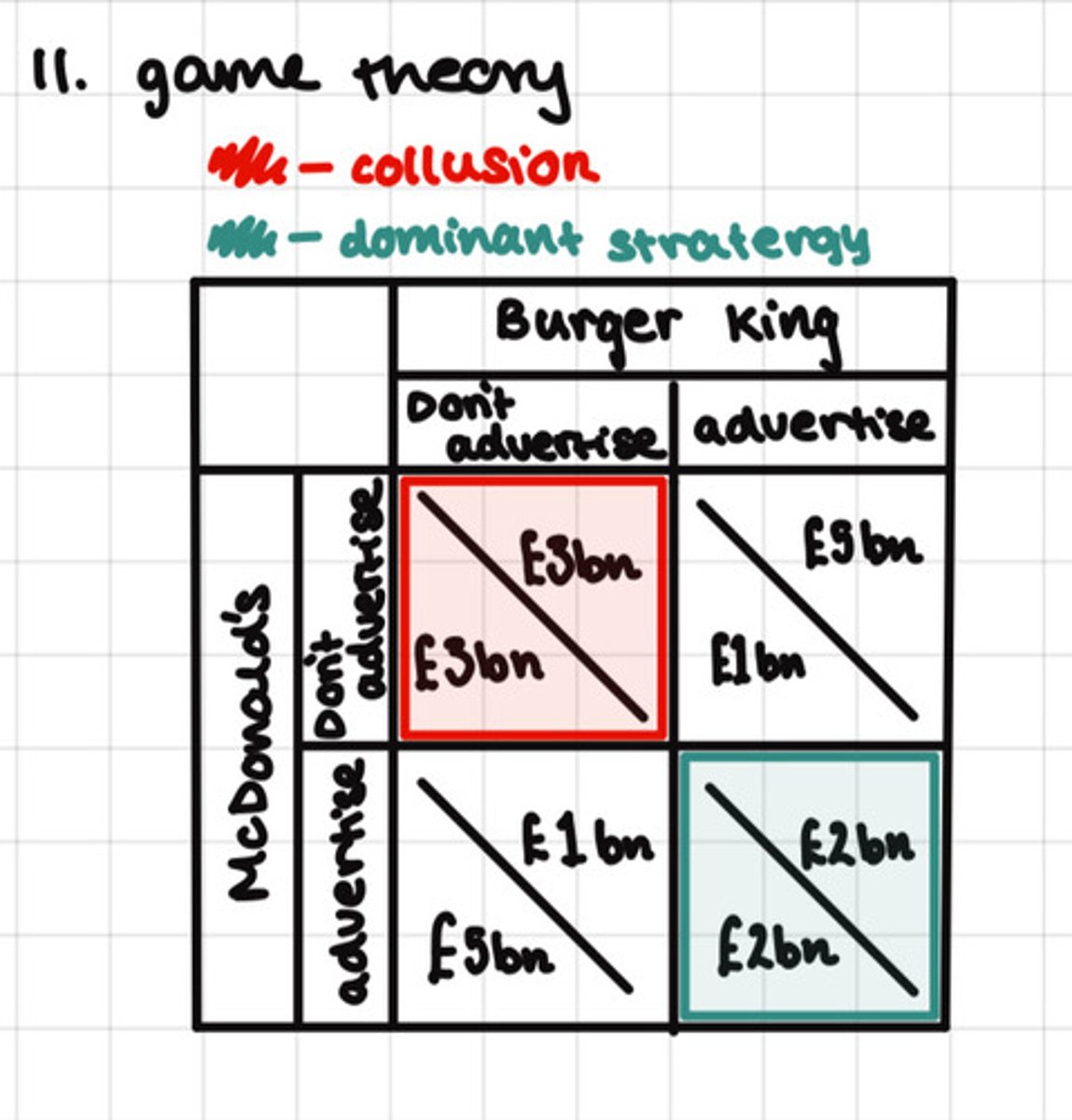

Game Theory (Dresher & Flood, 1950)

Explores the implications of self-interested (strategic) behaviour where individual decision-making entities are interdependent - focusing on equilibrium outcomes.

Prisoner's Dilemma

Conditions of the dilemma:

Each prisoner may either betray or stay silent to involvement in the crime

No communication is allowed between the two prisoners

Independent decision-making with no collusion

The prisoner's chosen strategy affects the pay-off of the other

One-shot game

There is only a single chance for the prisoner to decide how to behave in this scenario

Nash Equilibrium (Nash, 1950)

The point at which a competitor is pursuing the best possible (dominant) strategy, given the likely strategies of the other competitors in the game.

- No sole incentive for either competitor to move away from this point

Dominant Strategy

A strategy that is best for a player in a game regardless of the strategies chosen by the other players.

Collusion

Co-operative behaviour exuded by firms.

Collusive behaviours

- Price fixing

- Controlled output

- Restricting aggression on non-price / quantity variables

Overt / Explicit Collusion

A written agreement between firms to collude.

Tacit / Implicit Collusion (Conscious Parallelism)

No explicit agreement but each firm mutually recognises (through repeated interaction) that collusion is rewarded by profits.

Stability of Collusion

Collusion is unstable as there is always an incentive to cheat.

One-Shot / Finite Settings for Game Theory

It is expected that players use their dominant strategy with the same outcome in each round as all firms expect the other to cheat.

- Collusion is impossible

- E.g. Auctions, government invites for tenders to government contracts etc.

Grim Trigger

Punishment strategy in Infinite Game Theory Setting:

If a rival firm cheers on a firm, they will NEVER CO-OPERATE together again.

- Nash equilibrium will be sustained.

Tit-for-Tat

Punishment strategy in Infinite Game Theory Setting:

If a rival firm cheats on a firm, they will retaliate by cheating in return until they feel satisfied by the repayment.

- Does not pay in the long-term - therefore collusion is possible again

Monopoly

A single firm supplies the entire market.

Monopoly features

- No close substitutes

- Heterogeneous product (price makers)

- High barriers to entry & exit

- Firm faces the entire demand curve

Sunk cost

Costs that have already been incurred and cannot be recovered - regardless of future decisions.

Outcomes of monopolies

- High prices

- Lower levels of production

- Economic profit for monopolists

- Allocative inefficiency

- Production inefficiency

Redistribution of welfare in monopoly

- Consumers lose out due to higher prices & lower production

- Monopolists gain via abnormal profits

Natural monopoly

When a single firm can supply the entire market at a lower costs than multiple competing firms - due to significant economies of scale.

- High fixed costs & low marginal costs

- Average costs fall as output increases - making it inefficient for multiple firms to operate

Benefits of monopolies

- Monopoly profits provide resources for investment / innovation

- Monopoly profits reward innovation

Preferred market structure

Intuition suggests that PERFECT COMPETITION is societies best option.

Concentration ratios

A measure of seller concentration in a market.

Concentration Ratio Cn

The percentage of the value of sales accounted for by the n largest firms in the industry.

- Values between 0%-100%

- High percentage = high concentration & little competition

- Low percentage = low concentration & plentiful competition

DOES NOT TAKE ACCOUNT OF THE SIZE DISTRIBUTION OF FIRMS!

Herfindahl-Hirschman Index (HH)

The sum of squares of the market shares of each firm (xi).

- Values between 0-10,000

- 0 = perfect competition

- 5,000 = duopoly

- 10,000 = pure monopoly

TAKES ACCOUNT OF ALL FIRMS IN THE MARKET