Cost Exam 3

1/37

Earn XP

Description and Tags

CH 10,14,12

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

38 Terms

Budget

A detailed plan for the acquisition and use of financial and other resources over a specified period of time

Operating Budget

Plans for all phases of operations, including production, purchasing, personnel, and marketing budgets (on income stmt)

Financial Budget

Identify sources and uses of funds for budgeted operations and capital expenditures

master budget

A comprehensive financial plan that consolidates all individual budgets and outlines an organization's overall financial goals and objectives.

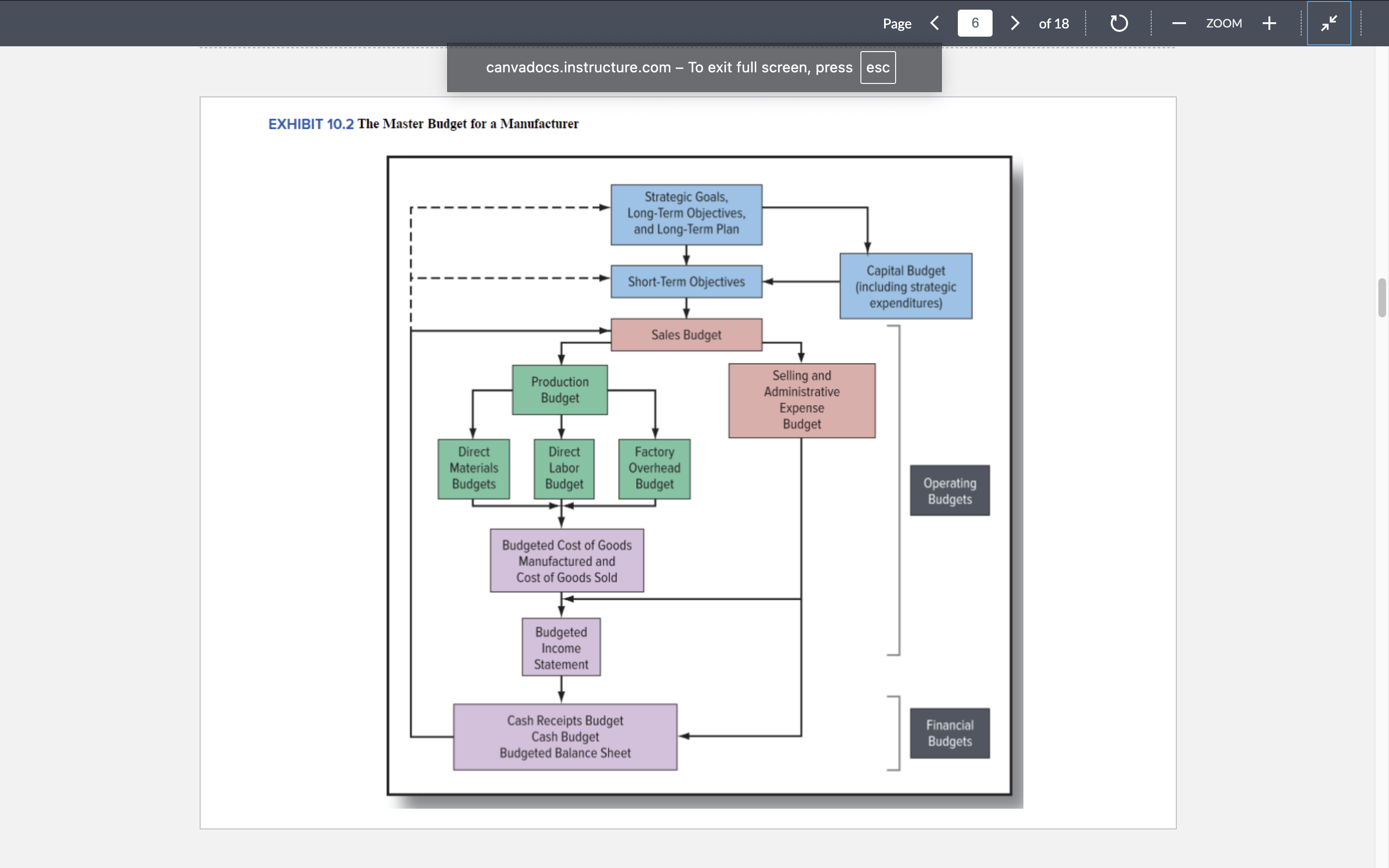

The Master Budget

Sales Budget =

SALES

+ Ending Inventory

=total needed

-beginning inventory

=to produce

Factory Overhead Budget

includes all production costs other than direct materials and direct labor. Some firms separate factory overhead into variable and fixed costs.

Cost of Goods Manufactured Budget and COGS Budget

prepared after FOH budget and the IS and BS use this information

Budgeted Income Statement (IS)

describes the upcoming net income for the upcoming period

Budgeted Balance Sheet (BS)

the last budget in the budget preparation process, incorporates the effects of all operations and cash flows during the budget period and shows projected ending balances in asset, liability, and equity accounts

Zero Based Budgeting (ZBB)

is a budgeting process that requires managers to prepare budgets from a zero base

– This type of budgeting allows no activities or functions to be included in the budget unless managers can justify their needs

– In-depth reviews and analyses of all budget items make managers aware of activities and functions that have outlived their usefulness

– Can be a difficult and time-consuming process

Kaizen (continuous improvement budgeting)

A budgeting approach that incorporates continuous-improvement expectations in the budgets

– Can be used as a complement to both traditional and activity-based (ABB and TDABB) systems

Behavioral Issues in Budgeting

-budgetary slack

spending the budget

goal congruence

Authoritative or participative budgeting

Top-down budgeting is referred to as authoritative budgeting

– Bottom-up budgeting is referred to as participative budgeting

Difficulty level of the budget target

An easy budget may fail to encourage employees to give their best efforts, while a very difficult target can discourage managers from even trying

– A “highly achievable target” is suggested with incentives for exceeding the budgeted figures

Linkage of compensation and budgeted performance

Problems with “fixed performance contracts”

– Gaming the performance measure

– Suggested improvements to basing incentive compensation on the basis of a fixed performance contract:

• Use of linear compensation plan, “rolling forecasts”, and relative performance

control

A set of procedures, tools, and systems that organizations use to monitor activities and to reach their goals

management accounting and control system

an organization’s core performance measurement system

operational control

Part of the control system that focuses on short-term operational performance

– Relates to the control of basic business processes (or activities)

short-term financial control

Comparison between actual and budgeted financial results

– Create Flexible Budget Schedule

Variances

Differences between budgeted amounts and actual financial results

Actual Results

Prepared at the end of the period (after actual activity is known)

– Actual sales volume is used, along with actual selling price per

unit, actual variable cost per unit, and actual total fixed costs

Flexible Budget

Prepared at the end of the period (actual activity is known)

– Actual sales volume is used, but with

• budgeted selling price per unit

• budgeted variable cost per unit

• budgeted total fixed costs

– Key to performing variance analysis at the end of the period

DM Price/Rate=

Actual Quantity (Actual Price - Standard Price) or AQ(AP-SP)

DM Qty/Efficiency =

SP(AQ-SQ)

DL Rate=

AH(AR-SR)

DL Efficiency =

SR(AH-SH)

DM Price Variance

= Actual Quantity Purchased (AP-SP) if different use AQP for price variance

DM Quantity Varience=

SP(AQU-SQ) if different use AQU

DM Variance common causes

Price Variances:

– Purchase of materials of different grades

– Quantity discounts

– Freight/delivery expediting cost (“rush orders”)

• Usage Variances:

– Purchase of non-standard quality materials

–Poorly trained or poorly supervised workers

–Poorly maintained machinery (not calibrated properly)

DL Variance common causes

Rate Variances:

– Labor substitution

– Out-of-date standards (e.g., new labor contract)

• Efficiency Variances:

– Poorly trained workers

– Poor quality raw materials used in production

– Poorly maintained equipment

– Poor supervision of workers

– Out-of-date standards

Standard Costs

costs that should be incurred under efficient operating conditions

Standard Cost System

an accounting system in which standard, not actual, cost flow through the formal accounting records

Type of Standards

– Ideal (Perfection) Standards

– Continuous-Improvement Standards

– Currently Attainable Standards

Standard Setting Procedures

Authoritative Standards and Participative Standards

Standard Cost Sheet

Contains both price and quantity components of each cost

Production Budget =

sales + end inv = total needed - beg inv = to produce

DM Purchases Budget=

Unit to produce x dm/unit = qty needed + end inv - beg inv of dm = qty to purch x cost/unit