econ exam

1/46

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

47 Terms

Market power

The ability to influence the market price of the product sold. Ex a firm in a perfect competitive market has none and a monopoly has it all

Monopoly

Sole seller of a product with No close substitutes and a price maker

Barriers to entry to the market, why mono arises

A single firm owns a key resource- like debeers n diamonds (not as common these days), gov gives a single firm the exclusive right to produce good- like patents (encourages research) and copyright (authors to write even better books), natural mono where a single firm can produce the market quantity at a lower cost than multiple firms- like supplying water or electricity (regulated so that the gov sets max price because it is normally a necessity)

Natural monopoly

Average total cost slopes downwards due to the huge initial cost to build the infrastructure and small marginal cost because the cost to add another unit is low because the up front cost was so high, basically the more you produce the smaller the average total cost gets

Natural mono ex

Bridge w toll but as population grows n that bridge becomes congested the market might expand into a comp market.

Natural mono ex

Bridge w toll but as population grows n that bridge becomes congested the market might expand into a comp market.

Mono vs comp: demand curve

Marginal revenue equals price for a competitive firm because they can increase quantity without lowering the price

Mono vs comp: demand curve

Marginal revenue is less than price in a mono because they have to reduce the price to sell a larger quantity and the only curve is the downward sloping demand curve and marginal revenue can even be negative

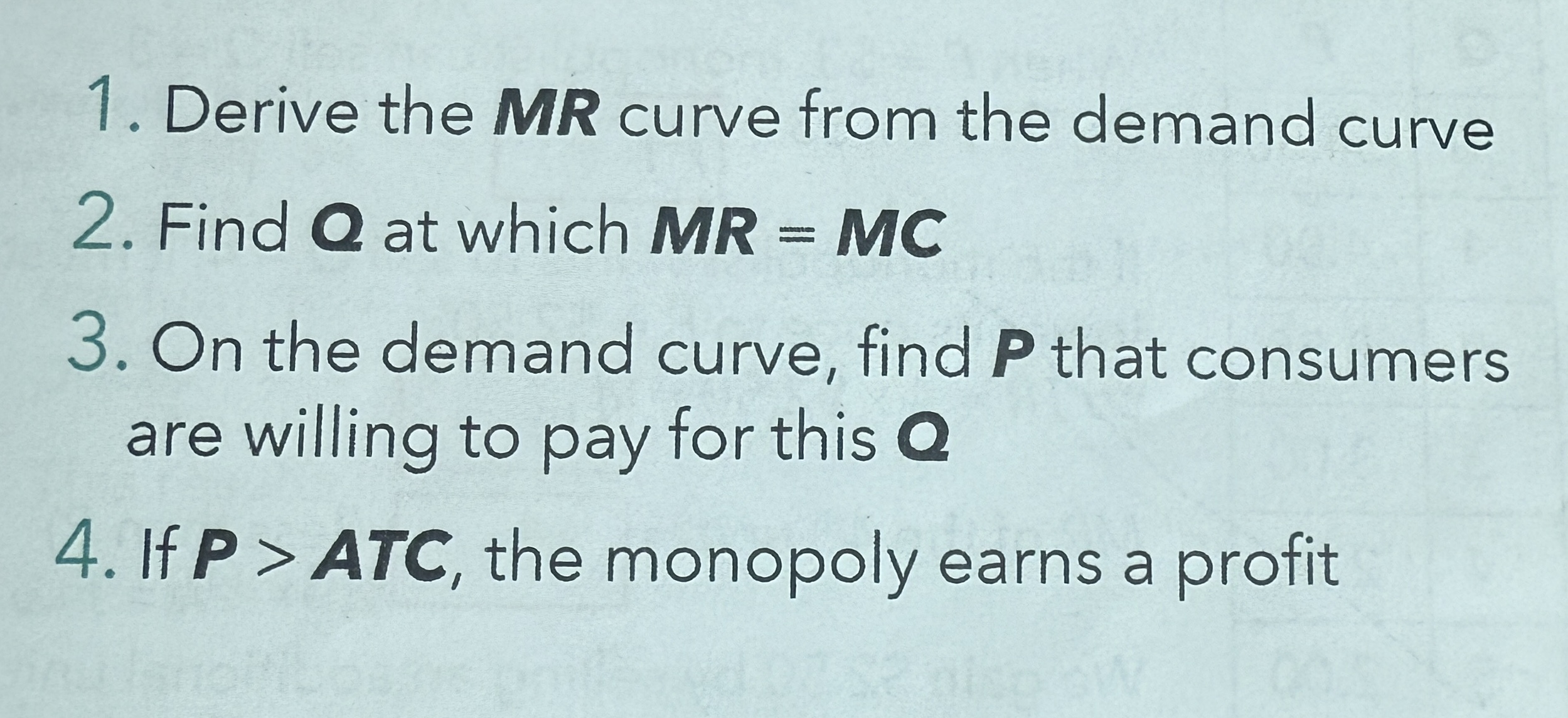

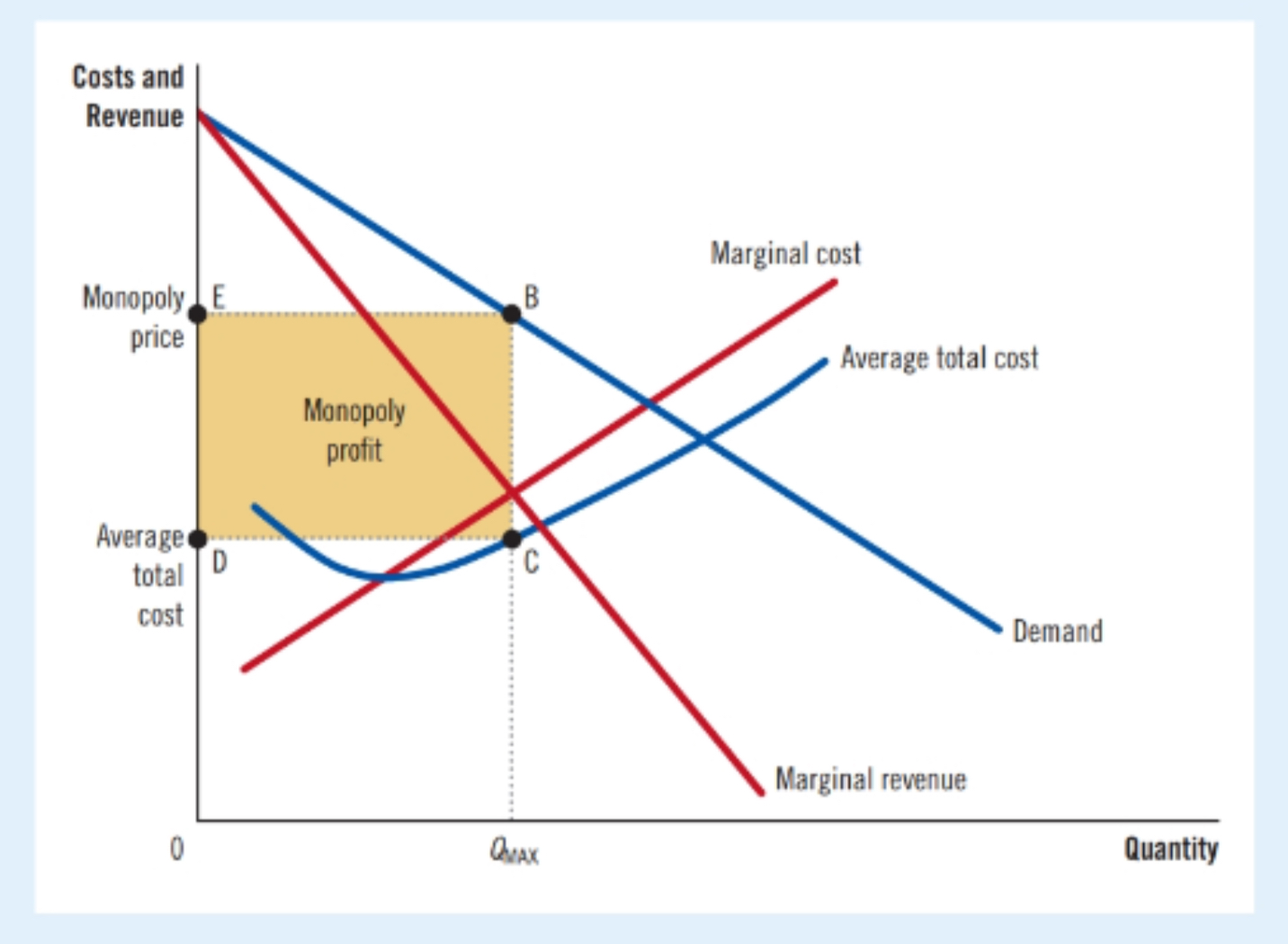

Profit max for mono

They will produce the quantity where marginal revenue equals marginal cost then set the highest price that consumers are willing to pay found on the demand curve

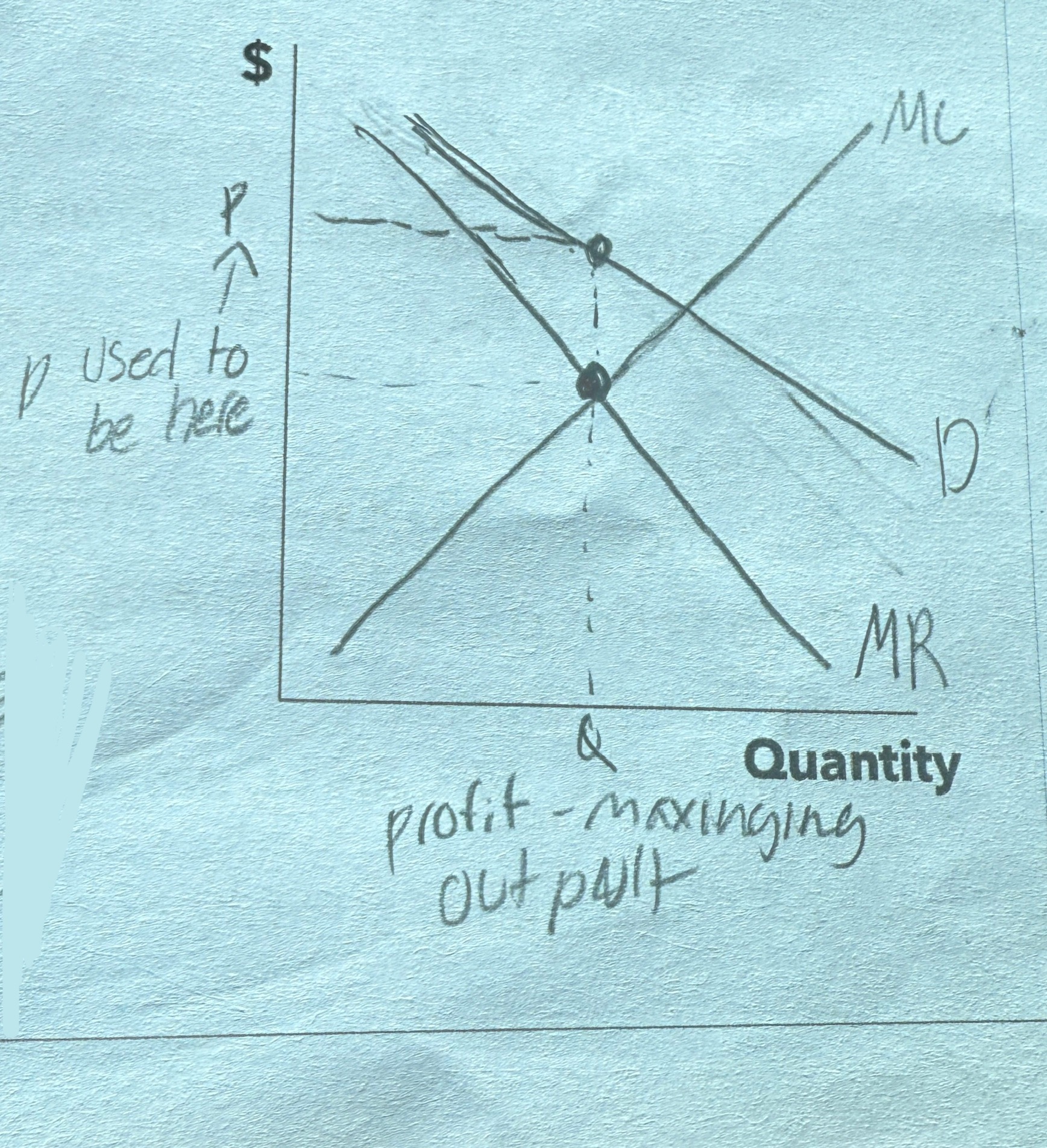

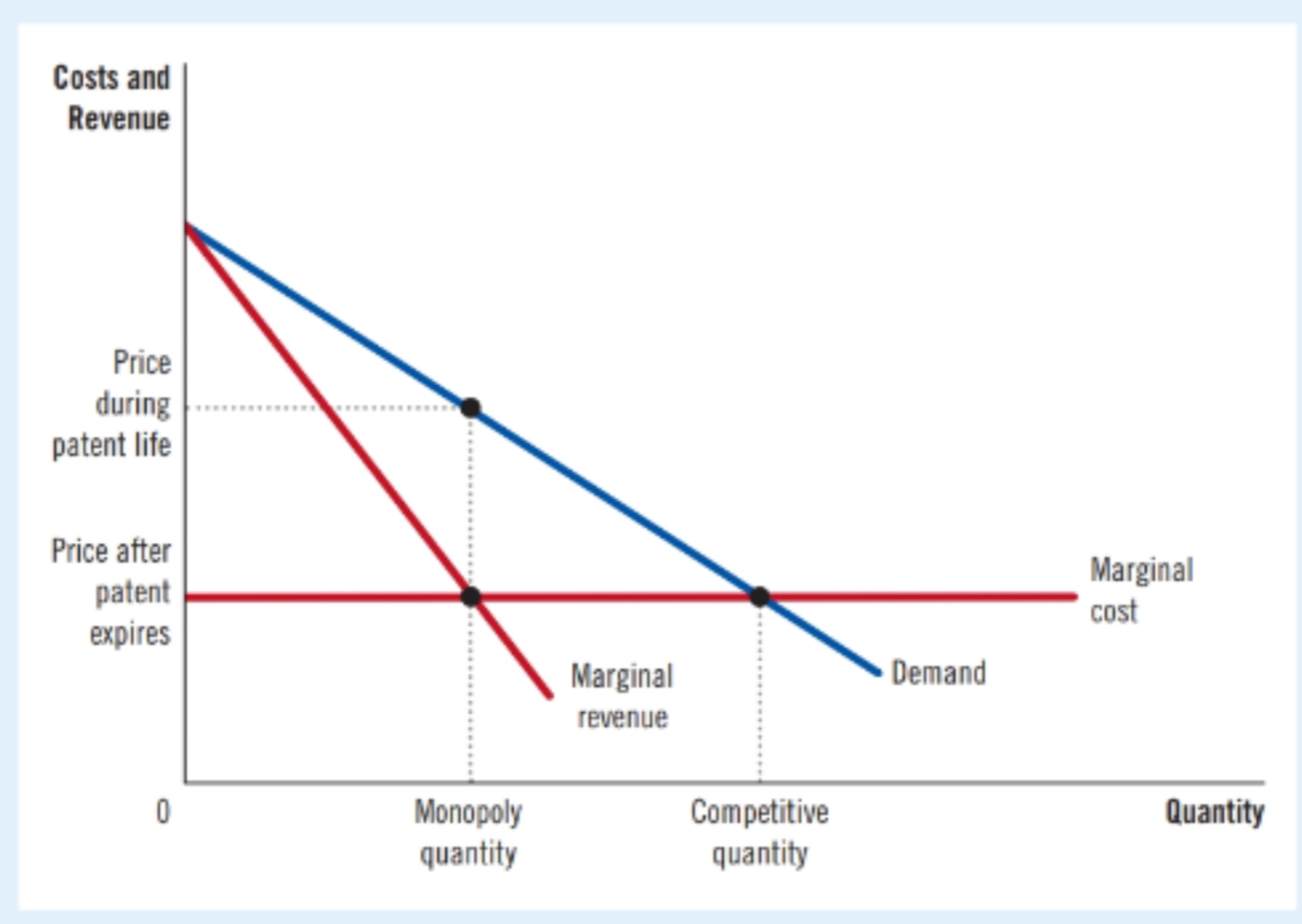

Mono turned comp

When new firms overcome the barriers of entry, the og mono market becomes comp and the price falls to the marginal cost. Basically quantity increases and the price lowers

Total surplus in a comp

Maximized at→ price= marginal revenue = marginal cost

Total surplus in a comp

Maximized at→ price= marginal revenue = marginal cost

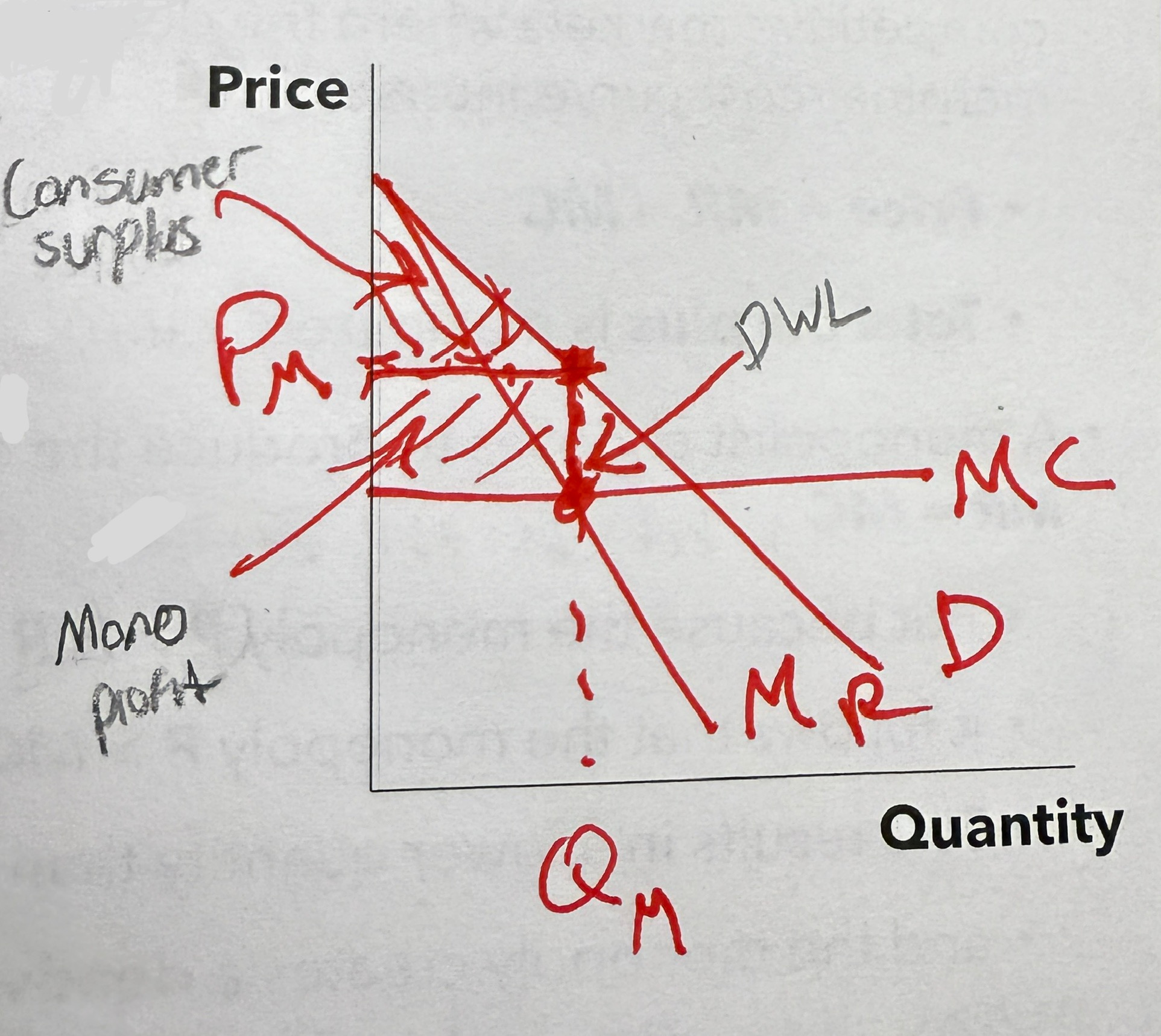

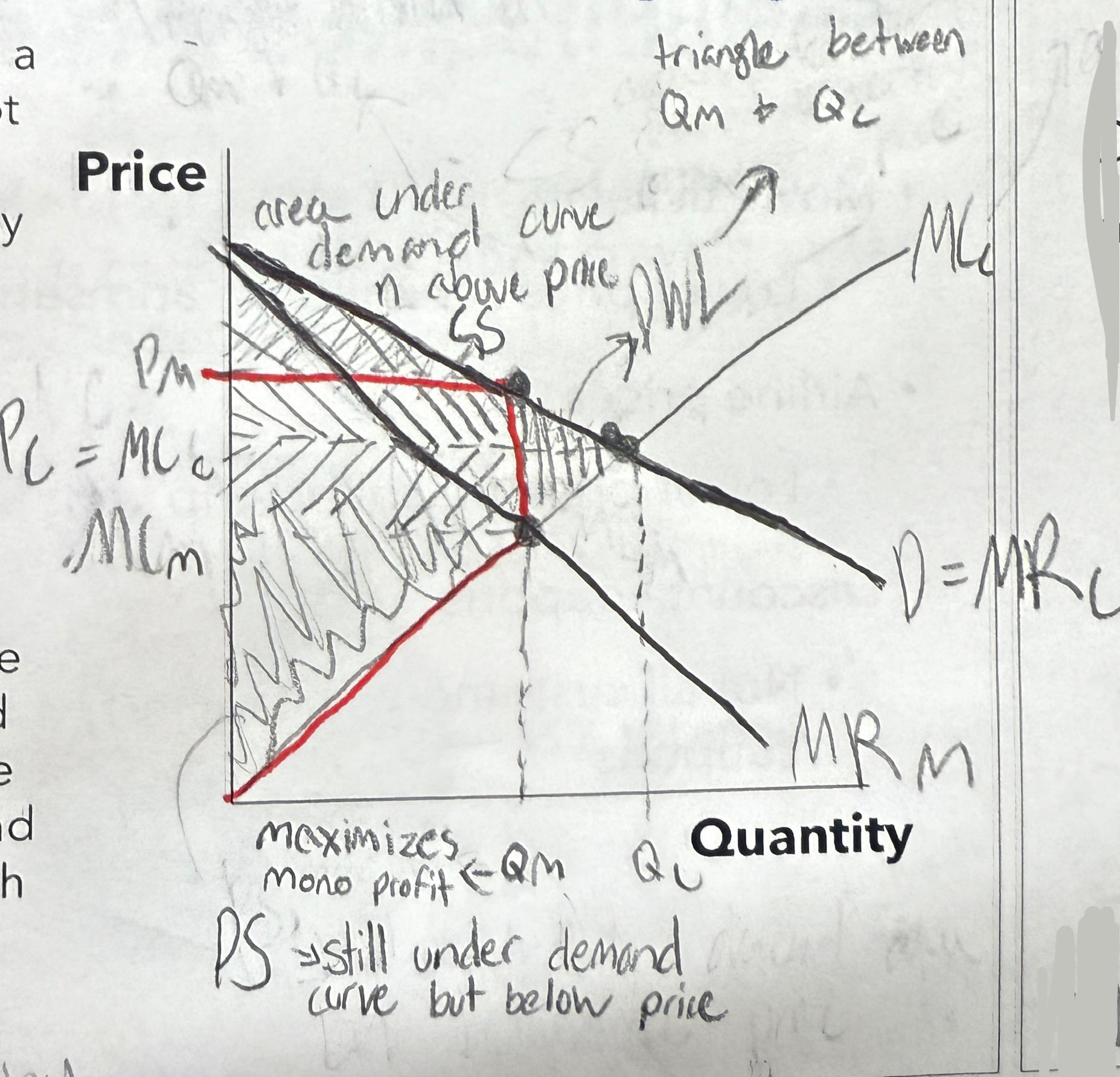

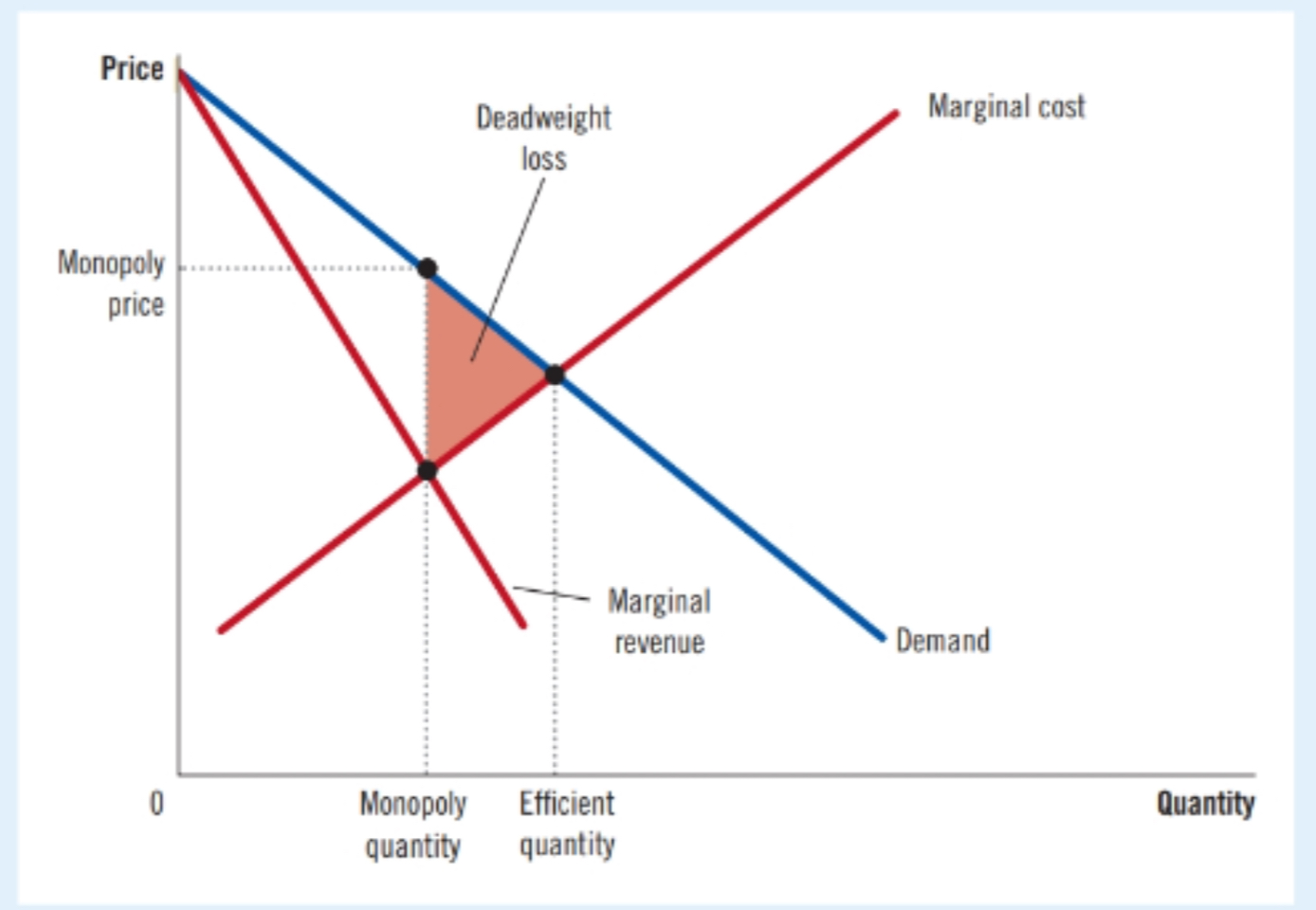

Total surplus in a mono

Mono produces the quantity where marginal revenue = marginal cost, but the price is more than marginal revenue and marginal cost. So this results in a lower quantity even though they could produce more and meet the demand

Deadweight loss (DWL)

Inefficient because willing customers are not able to get the product because of the price, total surplus is less then what it would be under a perfect comp

Deadweight loss (DWL) textbook

producing a quantity that is inefficiently low is equivalent to charging a price that is inefficiently high. When a monopolist charges a price above marginal cost, some potential consumers value the good at more than its marginal cost but less than the monopolist’s price. These consumers don’t buy the good. Because the value they place on the good exceeds the firm's cost of providing it to them, this result is inefficient.

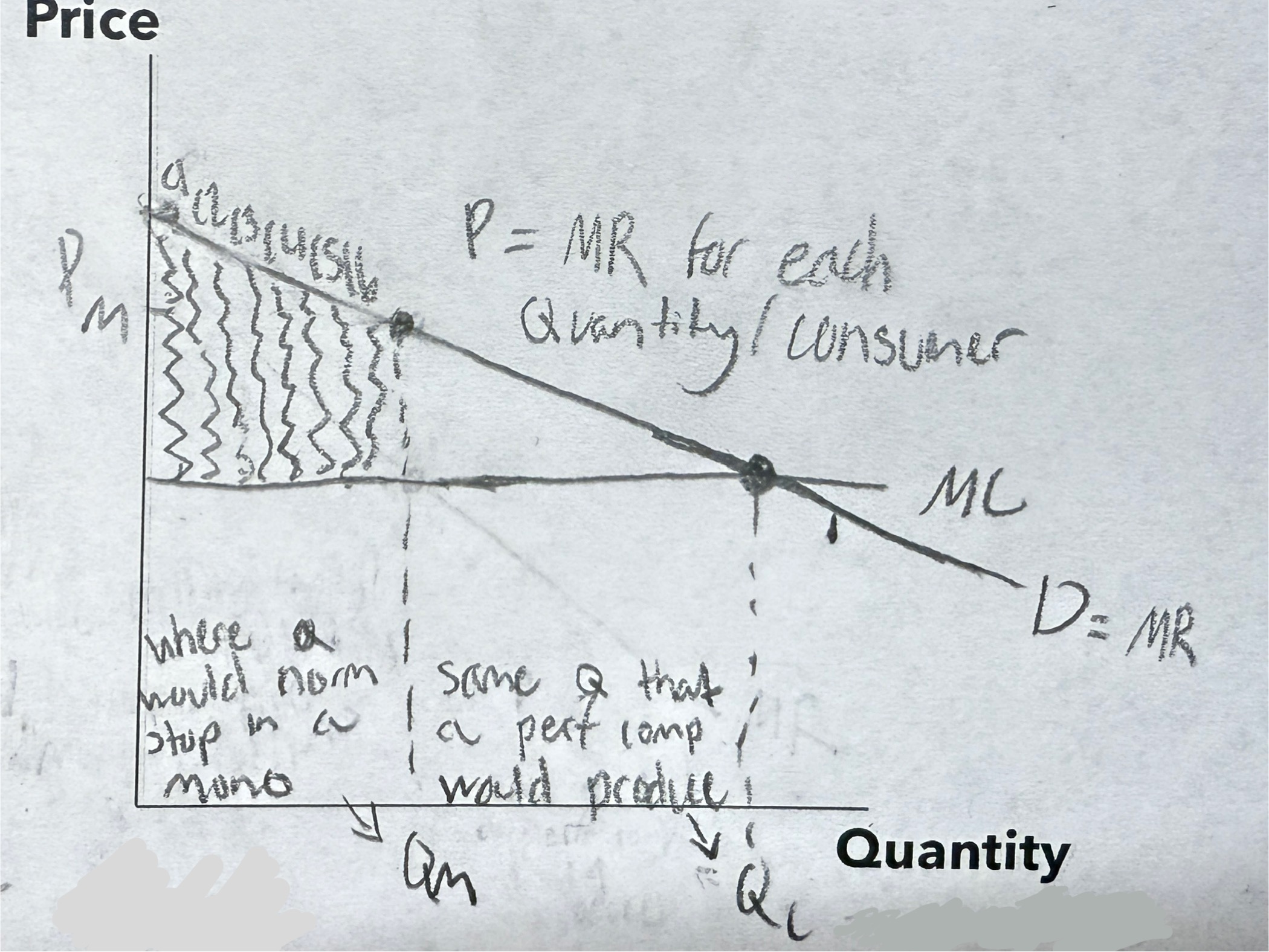

Non perfect Price discrimination, dividing up consumers into groups based on the a trait that reflects and is related to their willingness to pay, examples

Movie tickets, lower price for children and seniors- may fall asleep or not pay attention

Airline prices, lower price for round trip with Saturday night stay and higher price for people trying to buy a flight days before it departs- paying less for inconvenience and paying more because of desperation

Discount coupons, not all customers are willing to spend time to clip coupons- illusion of deals that are not guaranteed

Marginal revenue math with table

Q | P | TR

4 × 7 = 28

5 × 6 = 30

Marginal Revenue of the 5th quantity

30-28=2 dollars

Monopolies are inefficient because they produce less than the socially optimal quantity and charge prices above marginal cost. Governments have four main policy options to address this:

Antitrust laws – Promote competition by preventing mergers that would reduce competition (especially horizontal mergers) and breaking up large companies. However, some mergers create efficiencies (synergies), so regulators must weigh benefits against costs.

Regulation – Common for natural monopolies (e.g., utilities). Setting price equal to marginal cost would be efficient, but because natural monopolies have declining average total cost, marginal cost is below average total cost, so the firm would incur losses and exit. Subsidies could cover losses but require distortionary taxes. Alternatively, regulators can set price equal to average total cost (zero profit), but that creates deadweight loss. Also, regulation reduces firms’ incentive to cut costs.

Public ownership – Government runs the monopoly (e.g., postal service, some utilities). Supporters note it avoids private monopoly power, but critics argue that public enterprises lack the profit motive to minimize costs, and political processes may be captured by special interests.

Do nothing – Some economists (e.g., George Stigler) argue that political failures from imperfect policies can be worse than market failures. In some cases, the best solution may be to leave the monopoly alone.

Some government grants of monopoly power may be desirable if they

Provide incentives for invention and artistic creation

Some government grants of monopoly power may be desirable if they

Provide incentives for invention and artistic creation

For a profit maximizing monopoly that charges a single price, what is the relationship between price, marginal revenue and marginal cost?

Price is greater then (>) marginal revenue and marginal revenue is equal to marginal cost.

If a monopoly’s fixed cost increases, its price will _____, and its profit will ______.

Stay the same, decrease

Compared with the social optimum, a monopoly firm chooses

A quantity that is too low and a price that is too high

The deadweight loss from monopoly Aries because

some potential consumers who forgo buying the good value it more than its marginal cost

Price discrimination by a monopolist refers to charity different prices based on

the consumer’s willingness to pay.

When a monopolist switches from charging a single price to practicing perfect price discrimination, it reduces

consumer surplus

Antitrust regulators are likely to prohibit two firms from merging if

The combined firm will have a large share of the market

If regulators impose marginal cost pricing on a natural monopoly, a possible problem is that

the firm will lose money and exit the market

Concentration ratio

the percentage of the market’s total output supplied by its 4 largest firms, the higher the concentration ratio the less competition

Oligopoly

A market structure where only a few sellers offer similar or identical products. Bc these markets have only a few firms, each firm must be strategic when making supply decisions. The firms are keenly aware that each firm’s profit depends not only on how much it produces but also on how much each of the others produce. When setting production, a firm in an oligopoly needs to consider how its choices might affect the choices of other firms in the market. EX. Soft drinks, web browsers, batteries, credit cards

Collusion

An agreement among firms in a market about quantities of the good to produce or price to charge for the good. But this is difficult to firms to honor agreements due to self interest

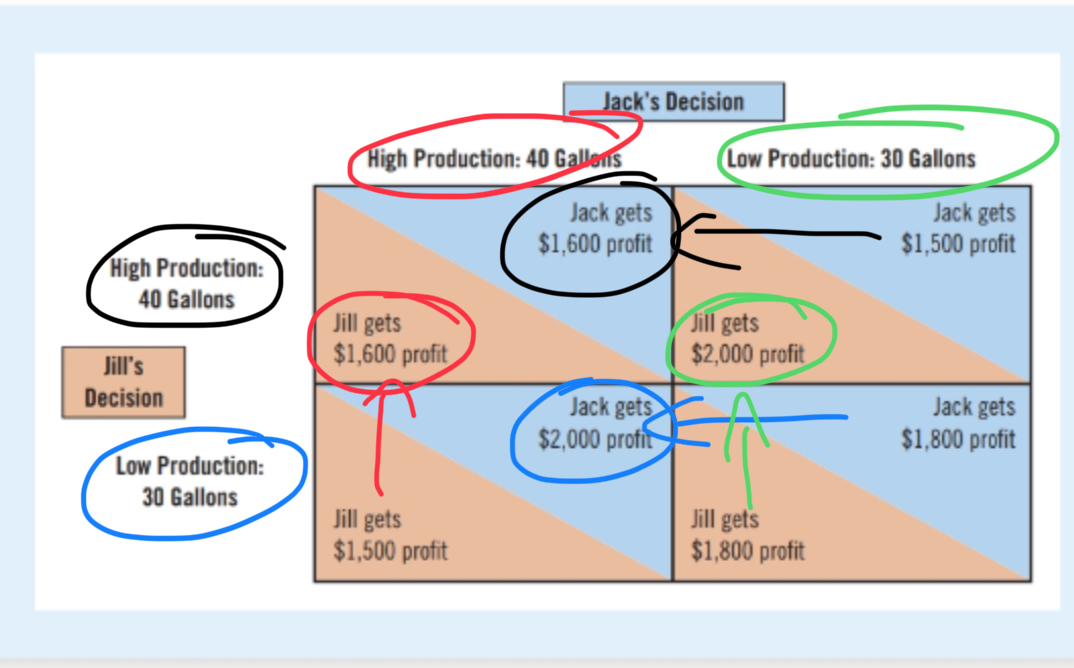

Maximum profits in oligopoly

Oligopolists can make the most profit if they cooperate and together act like one big monopolist producing a small quantity of output and charging a price well above marginal cost. Yet because each oligopolist cares only about its own profit, powerful incentives pull them apart, making it hard to maintain the cooperative outcome.

Cartel

A group of firms acting in unison

Cartel

A group of firms acting in unison

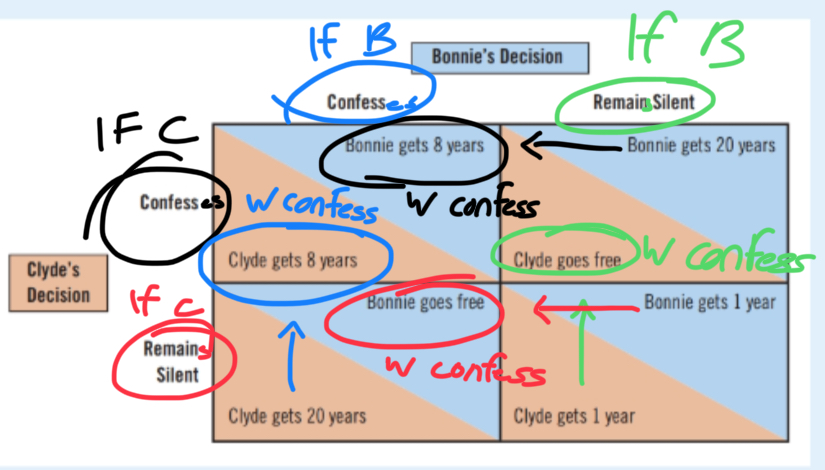

Dominant strategy

the option that is best for one player to choose regardless and no matter what the other players choose.

Nash equilibrium

The situation where players each choose their best strategy given that all the other players have chosen, basically what will end up happening in whatever situation, however not necessarily the best option that was available

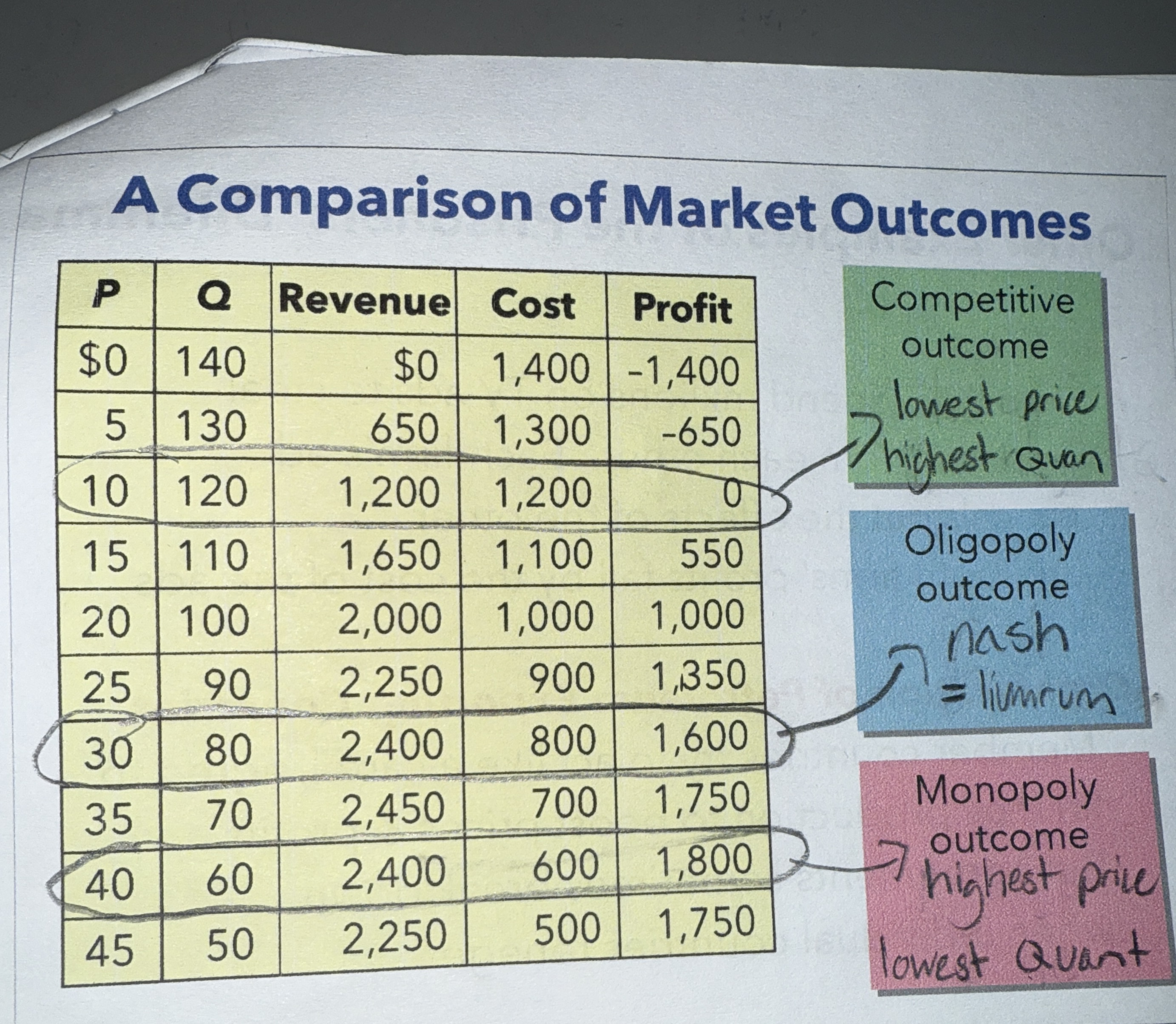

Comparison of market outcomes

Oligopoly QUANTITY greater than (>) monopoly QUANTITY

Oligopoly QUANTITY less than (<) monopoly QUANTITY

Oligopoly PRICE greater than (>) competitive PRICE

Oligopoly PRICE less than (<) monopoly PRICE

Prisoners dilemma

a particular “game” between two captured prisoners that illustrates why cooperation is difficult to maintain even when it is mutually beneficial

Other examples of the prisoners’ dilemma

Arms race between military superpowers:

-Each country would be better off if both disarm, but each has a dominant strategy of arming

Common resources:

-All would be better off if everyone conserved common resources, but each person's dominant strategy is overusing the resources

Ad Wars:

-Two firms spend millions on TV ads to steal business from each other. Each firm's ad cancels out the effects of the other,

and both firms' profits fall by the cost of the ads

Organization of Petroleum Exporting Countries:

-Member countries try to act like a cartel, agree to limit oil production to boost prices & profits. But agreements sometimes break down when individual countries go back on promises

Idk

Policymakers use the antitrust laws to prevent oligopolies from engaging in behavior that reduces competition. The application of these laws can be controversial because some behavior that can appear to reduce competition may have legitimate business purposes.

The key feature of an oligopolistic market is that

a small number of firms are acting strategically.

If an oligopolistic industry organizes itself as a cooperative cartel, it will produce a quantity of output _____ the competitive level and _____ the

monopoly level.

Less than , equal to

If an oligopoly does not cooperate and each firm chooses its own quantity, the industry will produce a quantity of output _______ the competitive level and _____ the monopoly level.

Less than, more than

As the number of firms in an oligopoly grows, the

industry approaches a level of output ______ the

competitive level and ______ the monopoly level.

Equal to, more than

Two people facing the prisoners dilemma may cooperate if they

Play the game repeatedly and expect no cooperation to be met with future retaliation

Two people facing the prisoners dilemma may cooperate if they

Play the game repeatedly and expect no cooperation to be met with future retaliation