AGOV Midterm Exam Copy

1/189

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

190 Terms

Dr. Investment Property, Land 10,065,000; Cr. Cash-Modified Disbursement System (MDS), Regular 10,065,000

Which of the following is considered an investment property?

A building held by the entity under a finance lease and leased out under one or more operating leases on a commercial basis

Which of the following would not be reported as investment property?

Property owned by the entity and leased out to another entity under a finance lease

Which of the following costs may properly be included in the carrying amount of an investment property?

Accrued taxes prior to acquisition date that the entity assumes an obligation to pay

During the period, Entity A, a government entity, decides to use as an office one of its buildings that has previously been leased out under various operating leases on commercial basis. Information on the investment property is as follows:

Investment property- Building - 1,000,000

Accumulated depreciation - 800,000

At the date of change in use, the fair value of the investment property is 250,000. How much is the gain (loss) on the transfer?

0

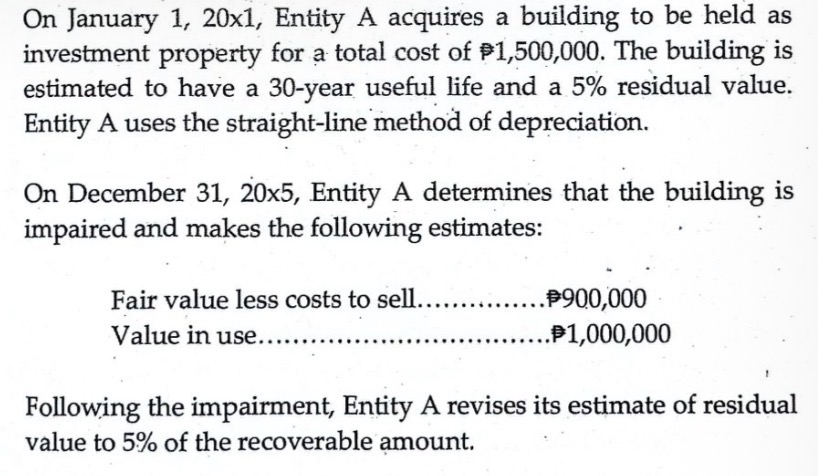

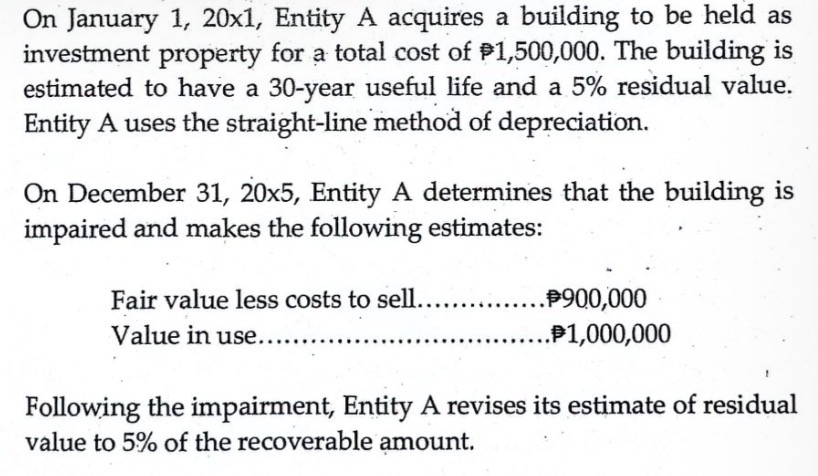

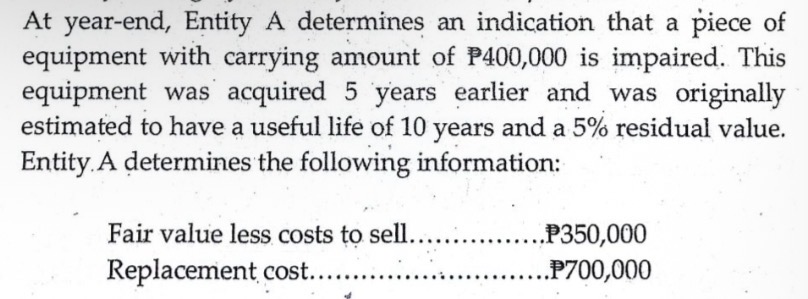

On January 1, 20x1, Entity A acquires a building to be held as investment property for a total cost of P1,500,000. The building is estimated to have a 30-year useful life and a 5% residual value. Entity A uses the straight-line method of depreciation. On December 31, 20x5, Entity A sells the building for P1,300,000. How much is gain (loss) on the sale?

37,500

How much is the impairment loss?

100,000

How much is the annual depreciation after the impairment?

85,500

Five years after the impairment, Entity A determines an indication that the impairment may no longer exist. Entity A makes the following estimates and computations:

Fair value less costs to sell - 800,000

Value in use - 750,000

The investment property would have a carrying amount of 600,000 by now if no impairment loss had been recognized in the past

How much is the gain on the reversal of impairment?

127,500

During the period, one of the buildings of Entity A, a government entity, was completely destroyed by fire. The building has a historical cost of P1,000,000 and an accumulated depreciation of P400,000. The building is insured for P700,000. Which of the following statements is correct?

Entity A shall treat the loss event and the insurance claim as separate events.

Which of the following is an investment property?

Property that is being constructed or developed for future use as investment property.

Which of the following is not an investment property?

Equipment held to be leased out under one or more operating leases on a commercial basis to external parties.

According to the GAM for NAs, government entities shall measure an investment property as follows:

Initial. cost; Subsequent. Cost Model

Investment property acquired through donation is initially measured

at fair value on acquisition date

An entity acquires investment property in exchange for a long-term noninterest-bearing note. Assuming of the following are determinable with sufficient reliability but differ in amounts, which of them is most likely to be used in the initial measurement of the investment property?

cash price equivalent of the investment property.

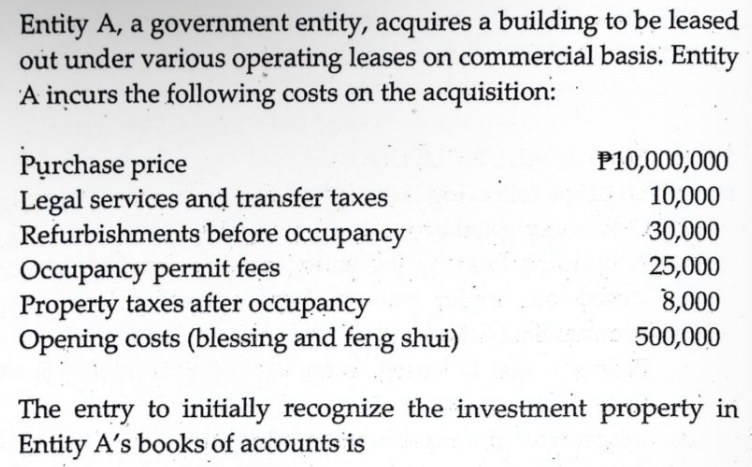

Entity A acquires an investment property for P1,000,000 cash. Additional costs incurred are as follows:

Repairs and remodelling before occupancy, P50,000.

Legal costs of transferring title to the property, P20,000.

Repairs after occupancy, P15,000.-

The investment property is estimated to have a remaining useful life of 10 years and a residual value equal to 5% of initial cost. Entity A uses the straight line method of depreciation. How much is the carrying amount of the investment property after one year?

968,350

According to the GAM for NGAs, transfers to or from investment property shall be made only when there is a

change in use

During the period, Entity A decides to lease out under various operating leases on commercial basis one of its buildings that has previously been used as office building. Information on the building is as follows:

Historical cost - 1,000,000

Accumulated depreciation - 800,000

At the date of change in use, the fair value of the building is 250,000. Which of the following is the correct reclassification entry?

Cr. Investment Property Buildings 200,000, Accumulated Depreciation- Buildings 800,000; Cr. Buildings 1,000,000

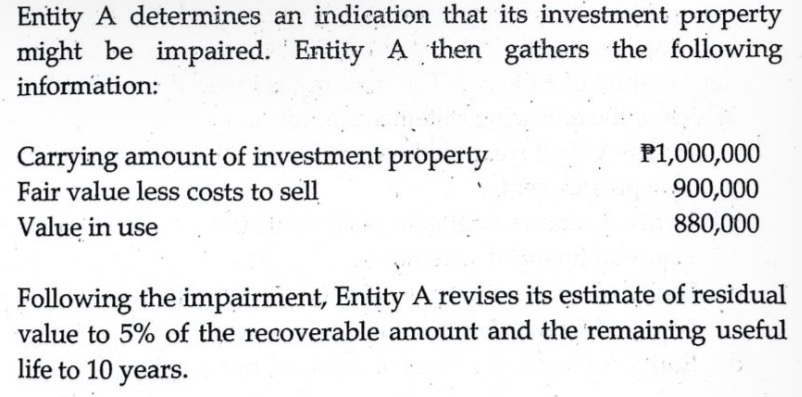

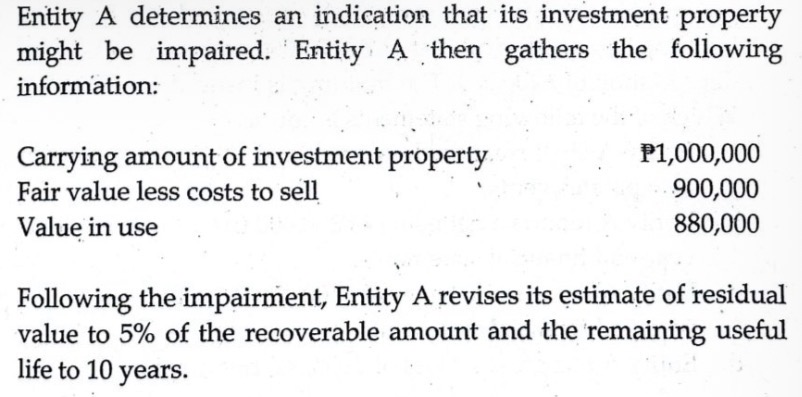

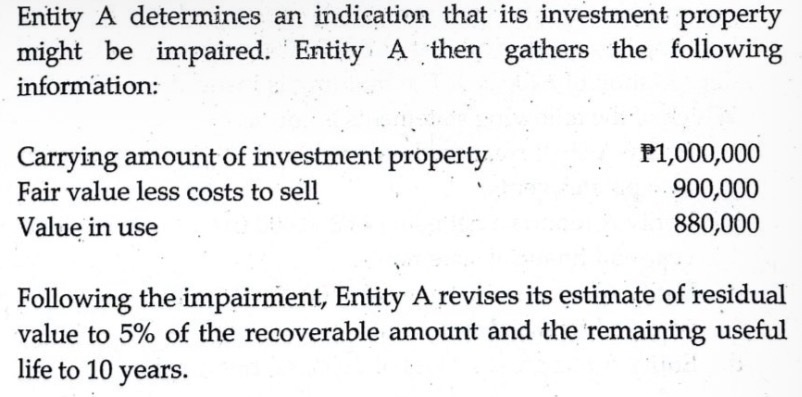

How much is the impairment loss on December 31, 20x5?

262,500

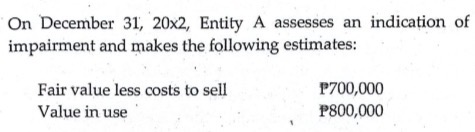

On December 31, 2x10, Entity A determines an indication that the impairment loss recognized in the prior period may no longer exist. Entity A makes the following estimates and computations:

Fair value less costs to sell - 1,100,000

Value in use - 1,050,000

How much is the gain on the reversal of impairment?

215,000

Entity A acquires equipment for P1M. The equipment is acquired not for active use in the production of goods but rather as standby equipment that will only be used if the main equipment needs to be repaired. Does this equipment qualify for recognition as property, plant and equipment?

Yes, all of the recognition criteria for a PPE are met.

For government entities, the capitalization threshold for PPE is

at least P50,000.

According to the GAM for NGAs, cash discounts not taken on purchases of items of PPE are

recognized as "Other Losses."

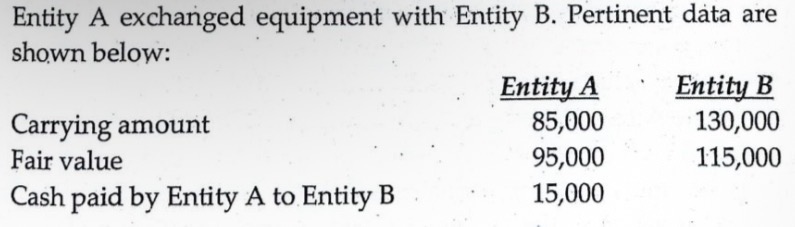

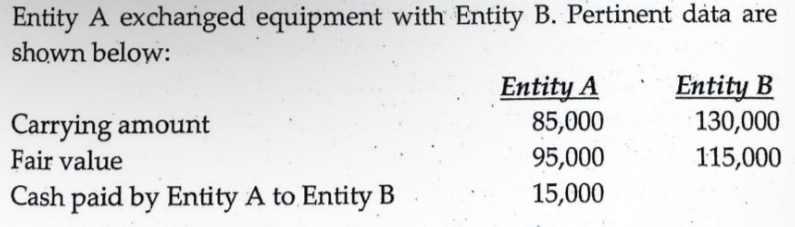

Entity A exchanged a piece of equipment with Entity B. Entity A, however, did not recognize any gain or loss on the exchange. Which of the following is a valid reason for this?

The exchange lacks commercial substance.

Entity A receives a donation of land with fair value of PIM.

The donor stipulated that the land shall only be used as a portion of a proposed highway. At the date of receipt of the donation, the construction of the highway is not yet started. When should Entity A recognize the land in its books of accounts?

Upon receipt of the donation.

According to the GAM for NGAs, estimates of decommissioning and restoration costs of an item of PPE are (choose the incorrect statement)

included in the initial cost of an item of PPE but not subject to subsequent depreciation, although subject to amortization using the effective interest method.

Which of the following costs is not added to the cost of an item of PPE?

Trade discounts

Entity A acquires a building through self-construction (construction by administration): The initial cost of the building will most likely be based on which of the following?

The costs of direct materials, direct labor and construction overhead, excluding wastages.

Entity A acquires a building through selt-construction (construction by administration). The construction costs incurred are

initially recorded in the "Construction in Progress" account.

Which of the following assets would most likely not be assigned a residual value by a government entity?

Infrastructure asset

Which of the following assets is generally not subject to depreciation?

Heritage assets

Which of the following is considered a heritage asset?

museum

Which of the following assets of a government entity is not subject to impairment?

None of these

A government entity derecognize an item of PPE that is

unserviceable

The national government receives a P10M grant from a foreign government conditioned on the construction of a highway. According to the GAM for NGAs; when shall the national government recognize revenue from the grant?

when the condition is satisfied

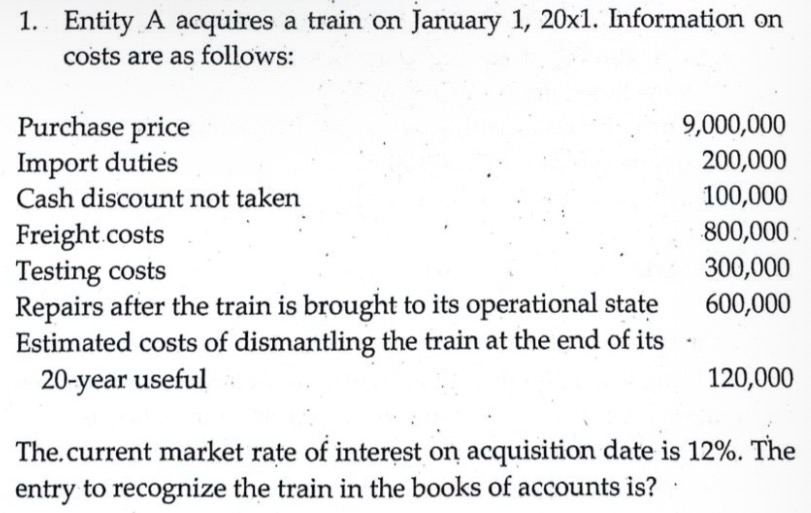

Dr. Trains 10,212,440, Other Losses 100,000; Cr. Cash-Modified Disbursement System (MDS), Regular 10,300,000, Other Provisions 12,440

Entity A acquires 5 motor vehicles for a package price of P10M. In conjunction with the purchase, the supplier provides Entity A a promotional item of 1 motor vehicle which is not of the same type as those acquired. The fair value the motor vehicle is P2M. Which of the following statements is correct?

For individual costing purposes, the cost of each of the 5 motor vehicles is P1,600,000.

During the period, Entity A starts the construction of a building by administration. Entity A acquires construction materials for P10M. The entry to record the transaction is

Dr. Construction Material s Inventory 10,000,000; Cr. Accounts Payable 10,000,000

Entity A, a government entity, acquires a piece of equipment for PIM on August 6, 20x1. The equipment's estimated useful life is 5 years. How much is the carrying amount of the equipment, on December 31, 20x1?

920,833

During the year, Entity A, an NGA, incurred interest of P200,000 on a loan taken to specifically finance. the construction of a building. The proceeds of the loan were temporarily invested and earned interest income of P20,000. Which of the following entries best reflects the recognition of the interest in the books of accounts of Entity A?

Dr. Construction in Progress - Buildings and Other Structures 180,000; Cr. Interest Payable 180,000

Which of the following is not one of the characteristics of property, plant and equipment?

It is intended for resale in the ordinary course of operations.

Which of the following does not result to the recognition of PPE?

Acquisition of a building for P10M intended to be leased out under various operating leases on commercial basis.

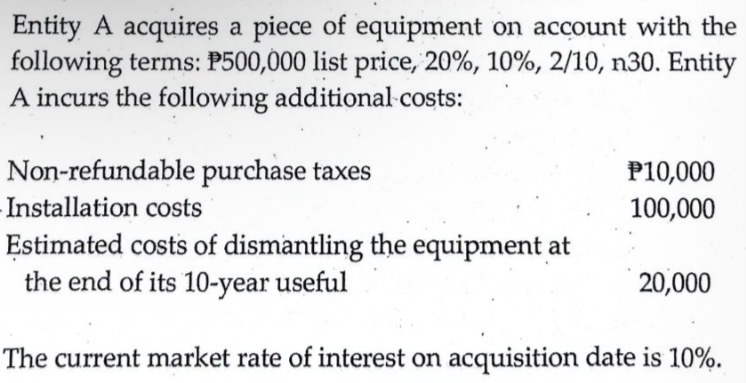

How much is the initial cost of equipment?

470,511

Entity A acquires 5 motor vehicles for a package price of P10M. In conjunction with the purchase, the supplier provides Entity A a promotional item of 1 motor vehicle which is the same as those acquired. The fair value the motor vehicle is P2M. Which of the following statements is correct?

For individual costing purposes, the cost of each motor vehicle acquired is P1,666,667.

Entity A acquires a building by awarding a construction contract to a contractor. The initial cost of the building will most likely be based on which of the following?

The contract price.

If the exchange has commercial substance, how much is the initial measurement of the equipment received by Entity A?

110,000

If the exchange has commercial subtance, how much is the gain (loss) recognized by Entity A in the exchange?

10,000

Entity A incurs costs in repairing an item of PPE. It is not clear whether the repair is a minor or a major repair. Entity A shall

recognize the repair costs as expense.

Entity A, a government entity, acquires a piece of equipment for PIM on August 26, 20x1. The equipment's estimated useful life is 5 years. How much is the accumulated depreciation of the equipment on December 31, 20x1?

63,333

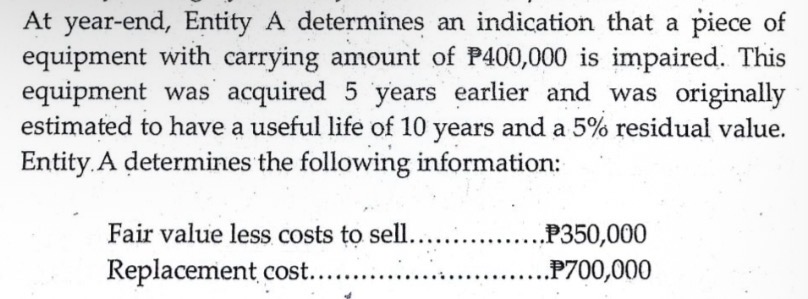

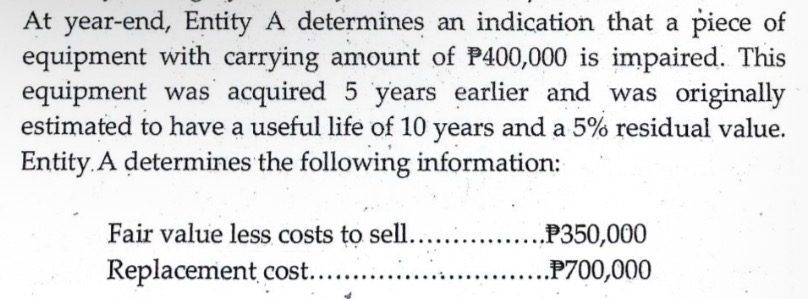

How much is the impairment loss assuming Entity A computes for the value in use using the Depreciated Replacement Cost Approach?

32,500

Assume the indication of impairment is physical damage to the equipment. Entity A estimates that it would cost P10,000 to restore the equipment's service potential to the level before the physical damage. How much is the impairment loss under the Restoration Cost Approach?

42,500

Assume the indication of impairment is a significant decline in the expected output of the equipment, which Entity A estimates to be 10%. How much is the impairment loss under the Service Units Approach?

50,000

Which of the following statements is correct?

Fully depreciated PPE are not derecognized.

Which of the following is derecognized?

Unserviceable PPE

How do government entities account for borrowing costs?

Choice (a) for national government agencies; choice (b) for the national government.

In which of the following instances is an asset not considered to be identifiable?

The asset can only be transferred if the entity is liquidated

Which of the following is most likely to be recognized as intangible asset by a government entity?

Publishing title acquired as a donation

Subsequent expenditures on recognized intangible assets are

generally expensed, unless they meet the definition of an intangible asset and the asset recognition criteria

According to the GAM for NGAs, government entities shall use this measurement model in subsequently measuring intangible assets.

Cost model

Intangible assets held by government entities are measured as follows:

Initial. cost; Subsequent. cost less accomulated amortization and impairment losses

The default amortization method for intangible assets with finite useful life is

straight line method

Which of the following statements is incorrect regarding the accounting for impairment of intangible assets under the GAM for NGAs?

Intangible assets are subject to amortization using the straight line method over a period of 2 to 10 years but are not subject to impairment

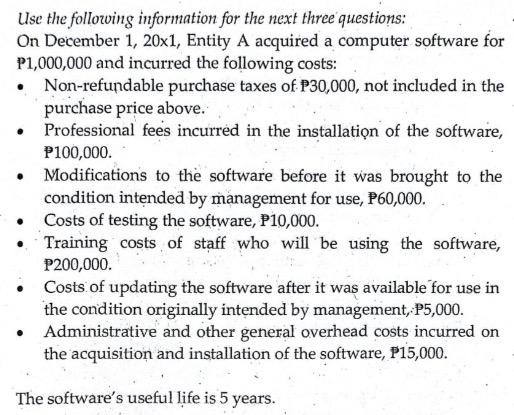

The entry to initially recognize the software is:

Debit. Computer Software 1,200,000; Credit. Cash-Modified Disbursement System (MDS), Regular 1,200,000

The entry to recognize the event is

Debit. Impairment Loss-Intangible Assets 140,000; Credit. Accumulated Impairment Losses - Computer Software 140,000

Which of the following is not one of the essential elements of an intangible asset?

Held for use in the production or supply of goods

An intangible asset is identifiable it is

a or b

Which of the following is an indicator of control?

all of these

Which of the following is most likely not an intangible asset

Computer

A purchased intangible asset is initially measured at

cost

The development costs of an internally generated intangible asset can be capitalized if certain conditions are met. Which of the following is not one of those conditions?

Existence of similar assets in the market or economic environment where the entity operates.

Internally generated brands, mastheads, publishing titles, lists of users of a service, and items similar in substance are not recognized as intangible assets because

these cannot be distinguished from the cost of developing the entity's operations as a whole.

Government entities normally assign their intangible assets a residual value of

zero

Which of the following intangible assets is not amortized?

Intangible asset not yet available for use

An entity shall test for impairment an intangible asset with finite useful life

only when an indication of impairment exists.

Financial liabilities, other than those that are classified to be subsequently measured at fair value through surplus or deficit, are measured as follows:

Initial. fair value minus transaction costs; Subsequent. amortized cost

Which of the following is not a financial liability?

Due to BIR

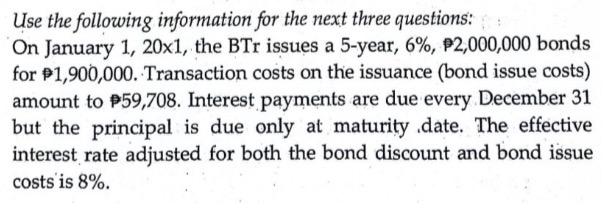

Transaction costs on issuing bonds are

deducted from the initial carrying amount of the bonds.

An entity issues term bonds at a discount. If the bonds are subsequently measured at amortized cost, which of the following statements is not correct?

The carrying amount of the bonds decreases each period.

The carrying amount of bonds payable in' the prior year's

financial statements. is P100,000. This year, the carrying amount of the same bond issuance is P102,000. Which of the following assumptions is least likely to be valid?

The interest expense during the period is P10,000, while the interest payment is P12,000.

Entity A issues 5-year bonds at a discount. At the beginning of the 3rd year, Entity A retires the bonds at a premium. Which of the following statements is correct?

Entity A recognizes loss on the retirement.

The entry on December 31, 20X1 to recognize interest expense is

Debit. Interest Expense 211,252; Credit. Discount on Bonds Payable-Domestic 61,252, Cash - Modified Disbursement System (MDS), Regular 150,000

The carrying amount of the bonds on December 31, 20X1 is

2,701,908

The unamortized bond discount on December 31, 20X1 is

231,939

A provision is measured at

the entity's best estimate of the settlement amount.

Which of the following may result to the recognition of a liability in Entity A's December 31, 20x1 statement of financial position?

A lawsuit is filed against Entity A on January 3, 20x2. Apparently, Entity A's geodetic engineer miscalculated the area of the lot where Entity A has started constructing an office building in December 20x1. This resulted to the encroachment of an adjacent lot owned by a private individual. Entity A has offered to settle the case out-of-court for PIM; however, the defendant wants payment of P1.2M. Both parties agreed to a settlement of P1.050M on January 31, 20x1.

Entity A purchases office supplies and receives delivery thereof. Entity A recognizes a liability from this transaction because of which of the following obligating events?

Legal obligation

Entity A obtains a 6%, 5-year, P10M face amount loan. Entity A pays transaction cost (service charge) of 3%. How much is the carrying amount of the loan payable on initial recognition?

9.7M

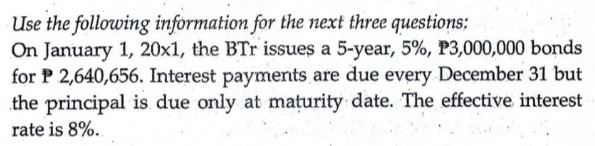

How much is the carrying amount of the bonds on initial recognition?

1,840,292

How much is the interest expense for 20X1?

147,223

How much is the carrying amount of the bonds on December 31, 20X1?

1,867,515

Which of the following distinguishes a provision from other types of liabilities?

A provision necessarily needs to be estimated because it is a liability of uncertain timing or amount.

A present obligation whose cost can be measured reliably but with improbable outflow of resources embodying economic benefits or service potential is most likely to be

disclosed only

Which of the following is correct regarding contingent assets?

Contingent assets are only disclosed if probable.

Which of the following statements is correct regarding reimbursements of provisions?

The expense related to the provision may be presented in the statement of financial performance net of the reimbursement.

At the commencement date, a government entity lessee recognizes the asset acquired under a finance lease and the related lease liability at

the lower of a and b

Entity A acquires an asset under a finance lease. The lease does not transfer ownership or contain any purchase option. Which of the following statements is correct?

Entity A will depreciate: the leased asset over the shorter of the asset's useful life and the lease term.

In accounting for finance leases, lease payments are discounted using

if this is determinable; if not, then b.

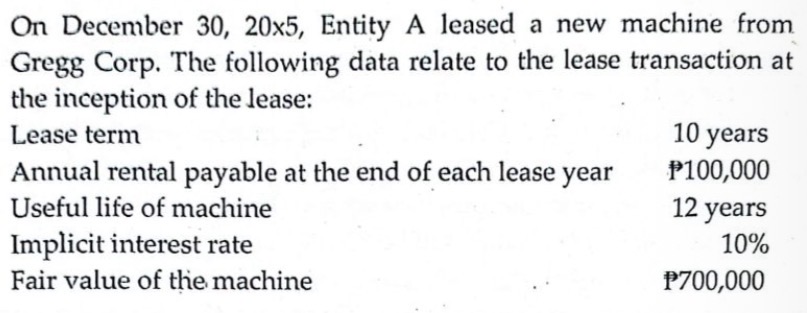

The lease has no renewal option, and the possession of the machine reverts to Gregg when the lease terminates. At the inception of the lease, Entity A should record a lease liability of

615,000

On January 2, 20x6, Entity A entered into a ten-year. non-cancellable lease requiring year-end payments of P100,000. Entity A's incremental borrowing rate is 12%, while the lessor's implicit interest rate, known to Entity A, is 10%. Ownership of the property remains with the lessor at expiration of the lease. There is no bargain purchase option: The leased property has an estimated economic life of 12 years. What amount should Entity A capitalize for this leased property on January 2, 20xG?

614,500

Entity A entered into a nine-year finance lease on a warehouse on December 31, 20x1. Lease payments of P52,000, which includes real estate taxes of P2,000, are due annually, beginning on December 31, 20x1, and every December 31 thereafter. Entity A does not know the interest rate implicit in the lease; Entity A's incremental borrowing rate is 9%. What amount should Entity A report as finance lease liability at December 31, 20x1?

280,000