IDP lecture set 2 4-6

1/23

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

24 Terms

Gross Domestic Product (GDP)

is the total monetary or market value of all finished goods and services produced within a country's borders during a specific period

Piketty’s argument

The golden age of growth in Western Europe occurred in the last century, after the two World Wars. During the 1950-1970 period (the "Glorious Thirty"), the GDP growth rate in Western Europe reached a record high of 4% per year. In contrast, U.S. growth remained more stable throughout the period

extreme wealth inequality is not an accidental flaw, but an inherent feature of free-market capitalism. His central thesis is that the rate of return on capital consistently outpaces economic growth, allowing the wealthy to accumulate assets much faster than the average person can earn wages

europe 1500-1700 The Malthusian mechanism

In a Malthusian economy:

Agricultural productivity increases.

More food becomes available.

Mortality falls and population increases.

The larger population divides the additional output.

Income per capita moves back toward a subsistence level.

Therefore, technological progress tended to increase population rather than permanently increase living standards.

The Key Role of Productivity in Economic Growth

One of the most important lessons in economics is that productivity drives economic growth. • Defined as the ratio of output over input, productivity determines how efficiently resources are utilized.

Productivity is mainly influenced by 4 key factors:

Innovation: the creation of new technologies (Investments in R&D) •

Education: adoption of new technologies and enhancement of workforce capacity •

Efficiency: Helps optimize production across different sectors •

Infrastructure: Also includes intangible infrastructure (creativity, good governance, macroeconomic stability)

human development index

long and healthy life

knowledge

a decent standard of living

The neoclassical and new growth traditions

argue that long-term growth is mainly supply-driven. Growth depends on the productive capacity of the economy: capital KKK, labor LLL, human capital, technology, and productivity

The Keynesian tradition

gives a larger role to demand. Investment, public spending, and aggregate demand affect whether productive capacity is actually used and whether future capacity is created.

Investment has a double role:

It is part of aggregate demand today.

It creates productive capacity for tomorrow.

Investments’ decisions are exposed to uncertainty (animal spirits)

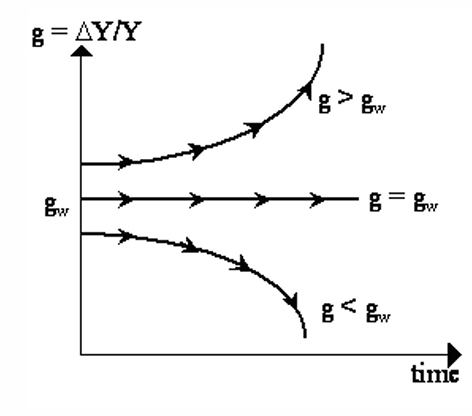

The Harrod- Domar Model

Solow models

The aggregate production function defines the relationship between total output and the inputs used in production: Y F K N = ( , ) Y= aggregate production; K= Capital: The total stock of machinery, buildings, infrastructure, and equipment N= Labor: The number of employed workers. F = State of Technology: The set of innovations and methods that determine both the range of goods an economy can produce and the techniques used for production.