ACCTG 414 CHP 1 & 2

0.0(0)

Studied by 1 personCard Sorting

1/36

Earn XP

Description and Tags

Last updated 4:39 AM on 9/9/22

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

37 Terms

1

New cards

Organizations and Reporting Standards in Canada

Canadian Accounting Standards Board (AcSB), International Accounting Standards Board (IASB), Financial Accounting Standards Board (FASB)< and Various Securities Commissions

2

New cards

Canadian Accounting Standards Board (AcSB)

Primarily responsible for setting GAAP in Canada, Develops standards for Canadian private Enterprises (ASPE), not for profit entities and pension plans. Adopts international standards (IFRS) into Canadian GAAP

3

New cards

International Accounting Standard's Board (IASB)

Major international standard setting body, IFRS used by public companies in Canada since 2011, Private enterprises have an option of using IFRS

4

New cards

Financial Accounting Standards Board (FASB)

FASB is the major setting body in the US, US GAAP affects Canadian companies too, as many Canadian companies are listed on US Stock exchange.

5

New cards

Securities Commissions

Provincial securities commissions, oversee/monitor capital marketplace in their province, ensure strict adherence to securities law/legislation.

6

New cards

Hierarchy of GAAP, Under IFRS GAAP includes

International Financial Reporting Standards (IFRS), International Accounting Standards (IAS), Interpretations (IFRIC or SIC). Alternative sources, pronouncements of other standard setting bodies, or other accounting literature.

7

New cards

Conceptual Framework

Main foundation for establishing a set of accounting standards, some advantages include; foundation for creating consistent standards overtime, reference for solving emerging problems in financial reporting more quickly

8

New cards

Objective of financial reporting

is to provide information that is useful for decision making, fundamental and enhancing

9

New cards

Fundamental Qualitative Characteristics

Relevance and Representational Faithfulness

10

New cards

Relevance

Relevant information is capable of making a difference in a user's decision, in order to be relevant information should have predicative and feedback/ confirmatory value, include all material information that would make a difference to the decision maker

11

New cards

Representational Faithfulness

information faithfully reflects the underlying economic substance of an event or transaction; it represents what it says it represents. To be representationally faithful info should be complete, neutral and free from error

12

New cards

Conservatism

means to require a greater degree of verification before recognizing good news compared to bad news, err on the side of understating rather than overstating net income and net assets

13

New cards

Conservatism and Neutrality

is somewhat inconsistent with the concept of neutrality, conservatism underlies some accounting standards e.g., recording an impairment on assets that have declined in value

14

New cards

Enhancing Qualitative Characteristics

Comparability, verifiability, timeliness and understandability

15

New cards

Comparability

information measured and reported in a similar way both from company to company and for same company from year to year

16

New cards

Verifiability

different individuals would come up with similar results

17

New cards

Timeliness

information is available to decisions makers before it loses it ability to make a difference in their decisions

18

New cards

Understandability

information has sufficient clarity such that a reasonably informed user can understand it

19

New cards

Trade-offs

not always possible to have all fundamental and enhancing qualitative characteristics at the same time, e.g. trading off verifiability for timeliness, to meet a deadline

20

New cards

Cost vs Benefit

Always have to weigh the costs and benefits of providing information

21

New cards

Assets - B/S

Have three key elements; represent a present economic resource entity has control over that resource and results from a past transaction or event

22

New cards

Liabilities - B/S

Have three key characteristics, represent a present duty or responsibility, entity is obligated to transfer an economic resource, obligation results from a past transaction or event

23

New cards

Equity - B/S

Represents the owner's residual interest in the assets, after all liabilities are deducted

24

New cards

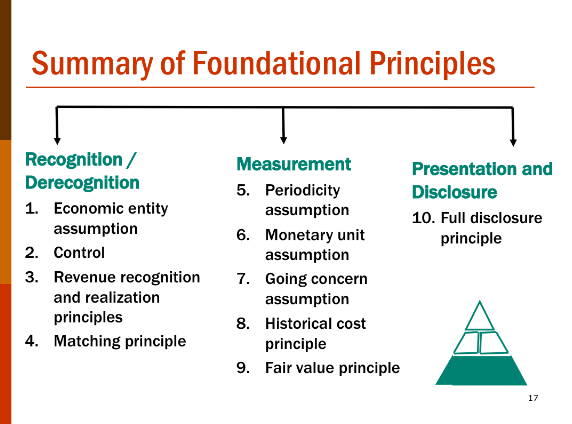

Foundational Principles

help explain which, when and how financial elements and events should be recognized/derecognized, measured and presented/disclosed by the accounting system

25

New cards

Recognition

act of including something on the BS or IS

26

New cards

Derecognition

Act of removing something from the BS or IS

27

New cards

Economic Entity Assumption

All economic events are identified with a particular economic entity, that economic entity is separate and distinct from its owners

28

New cards

Control

control is an important factor in determining entities to be consolidated and included in an economic entity, refers to having power over the investee

29

New cards

Revenue Recognition Principle

Determines when revenue should be recognized

30

New cards

Matching Principle

Expenses are recognized in same period as the related revenue, match expenses to related revenue

31

New cards

Measurement

all elements must be measurable to be recognized, some elements in statements require use of estimates which include uncertainty

32

New cards

Periodicity Assumption

economic activities of an entity can be divided into artificial time periods for reporting purposes, monthly, quarterly or yearly

33

New cards

Monetary Unit Assumption

Money is the unit of measurement for economic transactions, also make a stable dollar assumption whereby the effect of inflation and deflation are ignored in the financial statements

34

New cards

Going Concern Assumption

Assumption that a business enterprise will continue to operate in the foreseeable future

35

New cards

Historical Cost Principle

Financial statement item measured at the cost that was paid/received when the transaction took place

36

New cards

Fair Value Principle

the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date

37

New cards

Full disclosure principle

the practice of providing information that is important enough to influence an informed users decisions, should provide sufficient detail, but still be condensed enough to remain understandable