Ch 7: Financing and Settlement (National)

1/58

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

59 Terms

Conventional Loan

a mortgage loan without any type of government insurance or guarantee- the lender may be protected by private mortgage insurance (PMI)

Non-conventional loan

a federally back mortgage loan with special features such as insurance, guarantees and relaxed lending guidelines to encourage and enable more buyers to purchase a home.

(FHA, VA, USDA)

Conforming Loan

a standardized loan that meets the purchase requirement of the secondary mortgage market

non-conforming loan

a residential mortgage loan that does not meet the purchase requirements of the secondary mortgage market. These loans are typically funded by private portfolios/investors money or sometimes local banks who have the flexibility to do this/

note

the instrument for the debt- the personal promise to pay

Mortgage

A document used to pledge real property as security for a note (Given by the borrower – the mortgagor, to the lender – the mortgagee). The mortgage will be recorded to create a lien.

PITI

borrower’s monthly payment of principal and interest, plus 1/12 of the annual property taxes and 1/12 of the annual homeowner's insurance premium.

Qualifying Ratios

Front ratio (typically 28% for conventional loans) the amount of monthly gross income that can be used for the PITI payment. Back ratio (typically 36% for conventional loans) the amount of monthly gross income that can be used for all consumer debt including the PITI.

Equity

The amount of cash that an owner has in their property (market value – debt)

LTV

The loan to value ratio – the loan amount as a percent of either the price or the appraised value, whichever is lower.

point

1% of the loan

Amortization

repayment of a debt in installments. A loan can be fully amortized – when the last payment is made the debt is zero; partially amortized – when the last payment is made there is still a balance owed – a balloon loan; zero amortization – when the last payment is made the full balance is still owed – a term or straight loan.

which are the most common mortgage loans for financing the purchase of real property?

conventional loan

non-conventual loan

conforming loan

non-conforming loan

Contract for Deed

is also an instrument for financing the sale of real property

seller financing that does not transfer legal title immediately

title retention protects the seller

if buyer defaults w payment, ownership goes back to seller (eviction is cheaper then foreclosure)

vendor (seller)

vendee (buyer)

if vendor or vendee dies, passes on to heirs

is a installment sale (buyer pays over time)

what type of Contract is a Contract for Deed?

it is an executory contract (a contract that has not been fully executed)

lien theory

a mortgage loan is used for the purchase of real property, at closing the buyer receives the title, and the lender has a lien.

Title theory

at closing, the lender receives the title and will hold it until the lien is satisfied or paid off.

Deed of Trust

some states use a Deed of Trust instead of a traditional mortgage. The deed of trust contains a “power of sale” clause. Power of sale results in a quick, inexpensive, non-judicial foreclosure. This non-judicial foreclosure is preferred by lenders. The deed of trust involves three parties - the borrower or trustor, the lender or beneficiary, and the trustee.

Deed of trust

trustee acts in a fiduciary relationship with the beneficiary (lender). The trustee has two functions in accordance with the Deed of Trust. He or she will release the lien when the note is paid or will foreclose in the event of default.

Primary Market

where consumers go to borrow money. It includes mortgage bankers, mortgage brokers, banks, credit unions, etc. It also includes seller financing.

The Secondary Market

where lenders go for money

this market exist fro the purchases and sale of existing mortgages to investors

is designed to provide greater liquidity to the residential real estate market by providing a steady supply of funds

Lenders sell their loans and thus recover cash for originating more loans.

Loans qualified to be purchased in the secondary market are called conforming loans.

What loans meet the purchase requirements of Fannie Maw and Freddie Mac?

conforming loans- a standardized loan

Fixed-Rate Amortized Loan

Equal, regular payments of Principal and Interest (P&I)until the loan is repaid. Interest is paid in arrears – At the end of each payment period. With each payment, the amount toward the principal INCREASES and the interest DECREASES.

most popular loan

Term Loan

Interest Only (IO) until the end of the term, when the entire principal is repaid. This is a Zero-Amortization Loan. This is also called a Straight Loan.

Blanket Loan

Covers more than one piece of property (several lots on one note). This loan may contain a Release Clause allowing the borrower to obtain partial releases of specific lots by making required lump sum payments.

done by builders

Blanket Loan

if you disturb a lot you must…

pay it off

Package Loan

Includes real property plus personal property (a furnished condominium)

Budget Loan

Includes Principal, Interest, Taxes, and Insurance in the monthly payment (known as PITI). Many loans, including FHA, VA, and most amortized fixed-rate loans, are budget mortgages.

in a budget loan where are the Taxes and Insurance keeped?

Taxes and insurance are placed in an Escrow Account. (An escrow account can also be called an impound, trust, or reserve account.)

Loan Servicers (Budget Loan)

The party managing the escrow account is referred to as the Loan Servicer.

Balloon Loan

is the first 3-5-7 years of fully amortized 30 year fixed loan

banks make max interest, get a slightly lower interest rate

Participation Loan

Two or more lenders invest in one loan. This allows the lenders to share the risk.

Open-End Mortgage

Permits additional borrowing on the same note. This is sometimes called a Credit Card Mortgage, or a Home Equity Line of Credit (HELOC).

Adjustable Rate Mortgage (ARM)

An ARM is a loan with an interest rate subject to change as conditions in the market change.

This loan would be a poor choice for those on a fixed income.

Construction Loan

Short-term loan with funds advanced periodically during the stages of construction. This is a Term Loan – Interest Only. The interest rate on this loan is higher than the rate on a permanent loan.

Reverse Annuity Mortgage

Allows homeowners 62 years of age or older, for all borrowers involved, to borrow against their equitywithout making any payments on the amount borrowed.

still paying taxes and insurance

lots of penalties

Wraparound mortgage

A new mortgage is placed in a secondary or subordinate position: it includes the unpaid balance of the first mortgage + added sums provided by the lender. Mortages combine in hope of get one loan with a lower interest rate

alienation clause in a mortgage would prevent/prohibit this kind of loan

Acceleration Clause

falling behind on payment

accelerating all your payments and making them due immediately

alienation clause

if you transfer your mortgage (sell your property) your mortgage is due

defeasance clause

lien is defeated when the mortgage is repaid

escalation clause

adjustable rate mortgage allows interest rate to rise in your payment, thus to use over time

subordination clause

Allows a lender to move to or take a lower lien position. This clause would be found in a second mortgage, a home improvement loan, or a home equity loan.

straight assumption

takes over someones payments and liability on the loan

This will not negatively impact a seller’s credit rating.

assumption clauses

allows someone to to take over the payments on an existing loan under specified terms and conditions.

assumption “subject to”

the buyer takes over the payments, but is not liable for the loan. The original borrower remains liable. In the event of a future foreclosure, this can have a negative effect on the seller's credit rating.

Truth in lending (LAW)

implanted by regulation Z

“tell Z true about lending”

Truth in Lending

what 2 types of terms?

trigger terms

exempt terms

trigger terms

enforce release of all the terms of the loan in your advertisement

exempt terms

advertise without advertising all the terms of the loan

Annual Percentage Rate

interest rates plus the fees rolled together

which of the following would be considered a trigger term under truth in lending?

interest rate

RESPA

-Real Estate Settlement Procedures Act

-law that regulates the settlement process, implemented by Regulation X

prohibit kickback, referrals without their notice

community reinvestment act

prohibited lenders from redlining

redlining- the illegal practice of not making loans in a certain area, particularly the minority areas

Banks and Insurance companies can't …..

redine- the illegal practice of not making loans in a certain area, particularly the minority areas

cannot discriminate on location

proration

division of ongoing expenses between the parties (seller and buyer expenses)

Setttlement during closing

Debit is Debt

If I owe it, I get the debit

if I receive, it I get the credit

when asked a question about closing and the splitting of property taxes for the year?

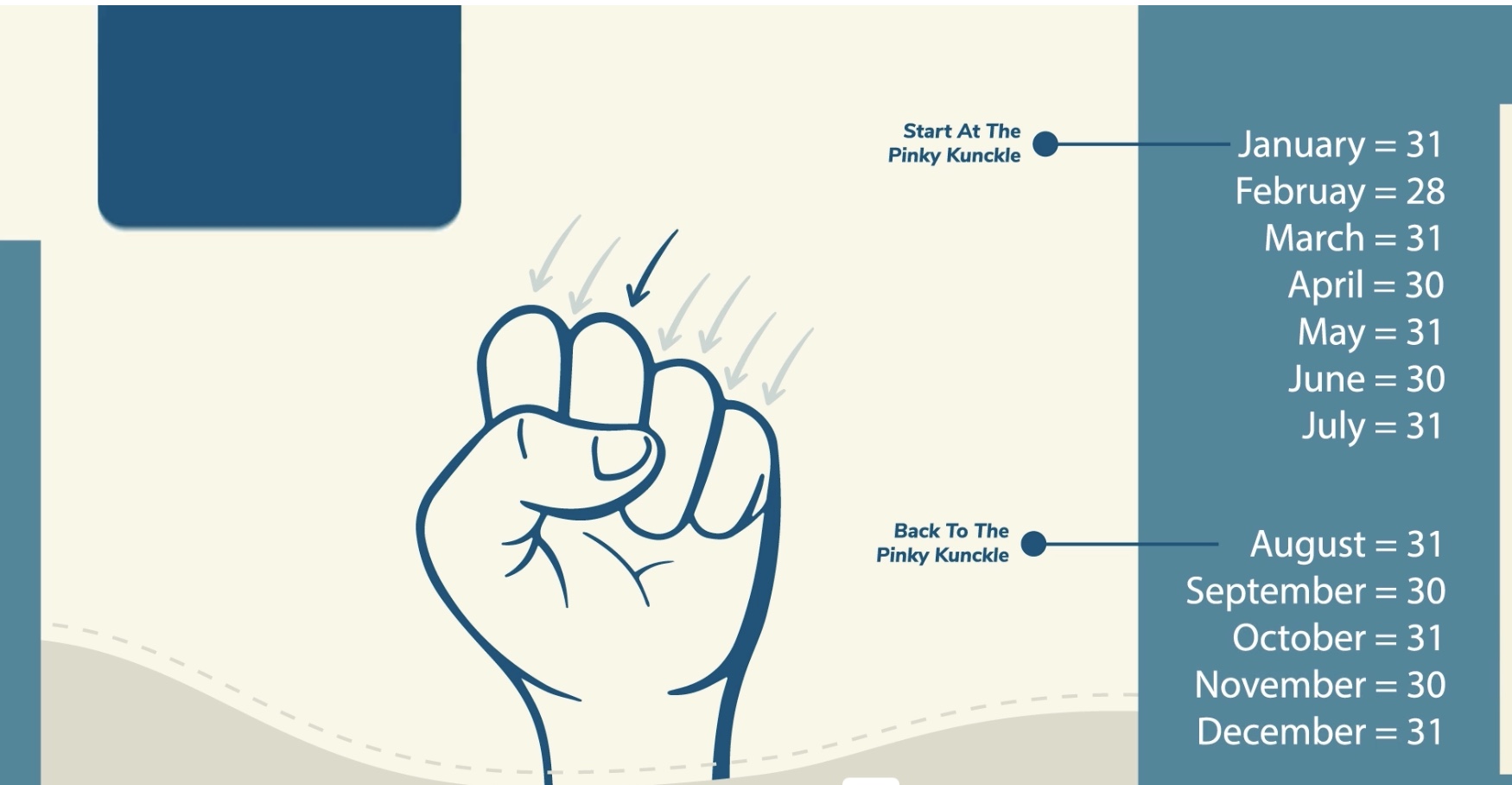

when 365 days are apart of the equation, how can we tell what # of days are in what month?

use fist

starting from pinky count the groves as months that have 30 days, knuckles have 31 days in the month

REMEMBER February has 28 days

a closing is occurring on November 1st, property taxes have already been paid, what is true?

the buyer owes for the remainder of the year

practice this question

answer: $550