WK 6 finance

1/18

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

19 Terms

what are real options

discretionary opportunities that are embedded within firm’s investment projects.

they give firms the right but not the obligation to exercise the option

options can be optimally exercised to maximise project value by waiting until after receiving new information in future

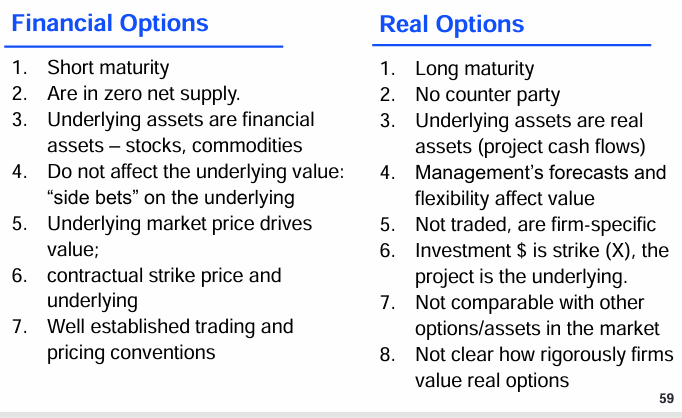

Limitation of standard NPV analysis

standard/static NPV analysis treats investment decisions as if they are now or never decisions with no alternatives when in reality managers tend to have flexibility in terms of the decisions they make in regard to projects. Hence, this flexibility provided by options should be accounted for in project evaluation and NPV analysis.

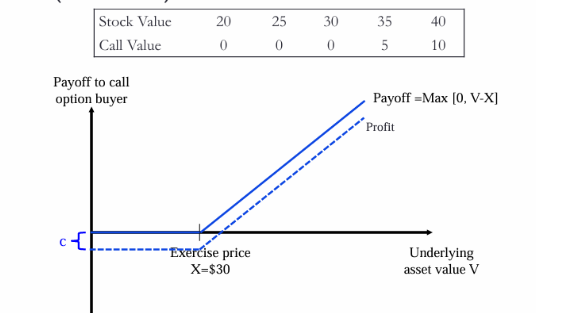

What is a call option (financial options)

it is a contract between a holder and writer that gives the holder the right but not the obligation to buy the underlying asset at a pre-specified exercise/strike price (X), even if the value (V) of the underlying asset changes

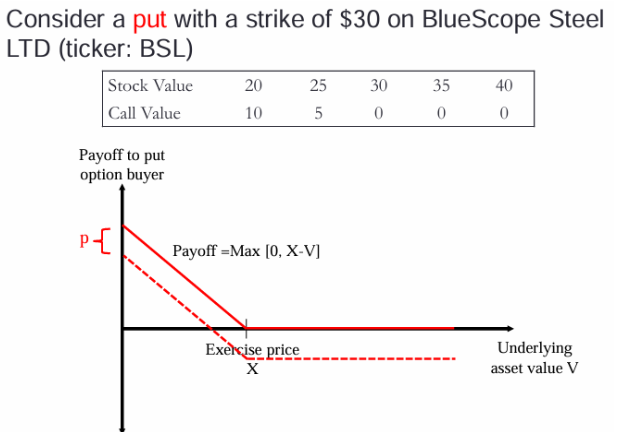

What is a put option

it is a contract between a holder and writer that gives the holder the right but not the obligation to sell the underlying asset at a pre-specified exercise/strike price (X), even if the value (V) of the underlying asset changes

What is T, c and p

T=time to expiration

c=euro call premium (diff between payoff and profit)

p=euro put premium (diff between payoff and profit)

Payoff from call option

V-X (you benefit when V increases, cuz you can buy for cheaper)

Payoff from put option

X-V (you benefit when V decreases, cuz you can sell for higher)

Issues with real options

you must be able to identify options in the project and identify what type of options they are

need to be able value real options

need to know how to value diff types of options

Conditions that need to be met for real option to exist

news will arrive in future

when news arrives, it may affect managers decision making

How to identify real options

search for uncertainty managers may face

look for clues in project’s description: phases, strategic investment, scenarios

examine pattern of cash flows and expenditures : might occur in stages

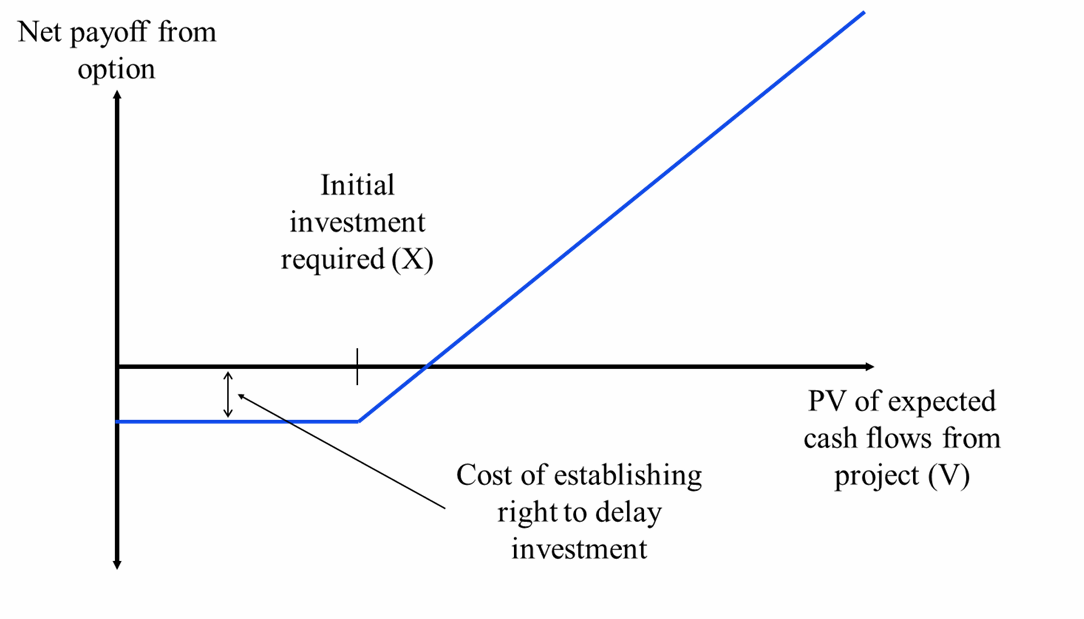

What does the exercise price represent in real options

what you pay/cost of the actual project

What does the premium represent in real options

The price of obtaining the actual option/keeping that form of flexibility

what does the underlying asset represent in real options

the project whose value the option depends on ie the present value of cash flows

Types of real options

Option to delay

allows you to delay making the investment

Option to expand: allows company to see how things are going before expanding

Option to abandon: allows firm the opportunity to abandon the project if it turns out to be unsuccessful

Option to vary

Option to delay (making an investment)

pros: gives you the chance to respond and react to new market information before making your decision

Cons: delaying can reduce the PV of cash flows from the early cash flows the business missed out on from delaying, or gives competitors the chance to dominate the market

may not be costless as you may need to pay for a license or patent so you can act in future

generally viewed as call option

Option to expand/grow

generally viewed as call option

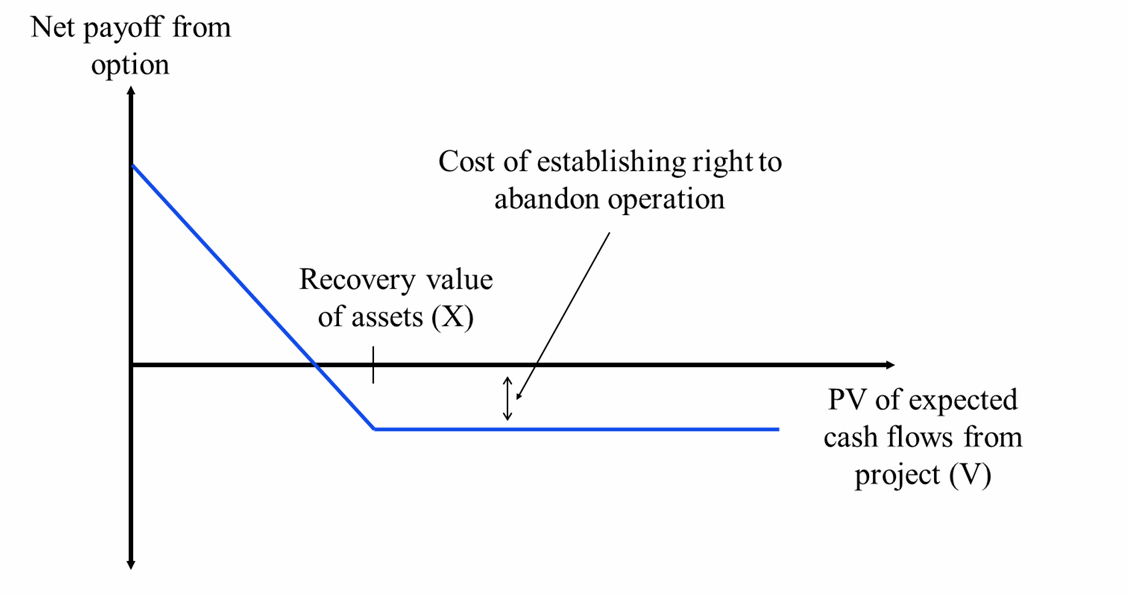

Option to abandon

can use if there is a get out clause

or if firm can abandon the project and realise the salvage value

X=money associated with getting out ie. salvage value of assets

viewed as put option

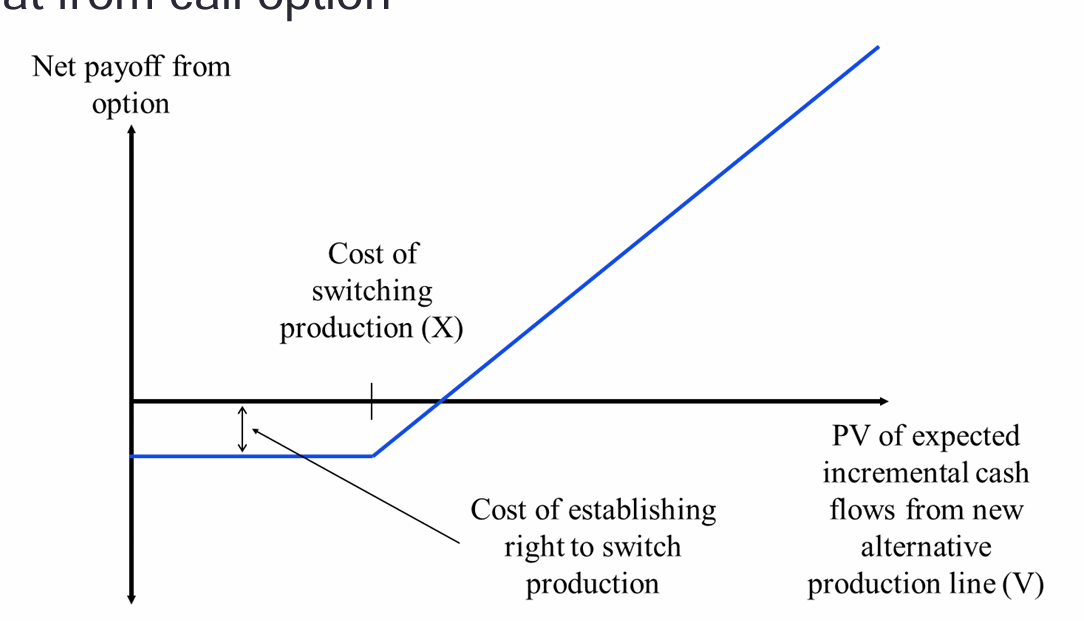

Option to vary

allows firm to revise its operatin decisions for a fixed cost in response to market conditions

eg. option to alter production rate, option to switch inputs

treated as call option

Financial vs real options