ACIS 2115 ch4-8

1/14

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

15 Terms

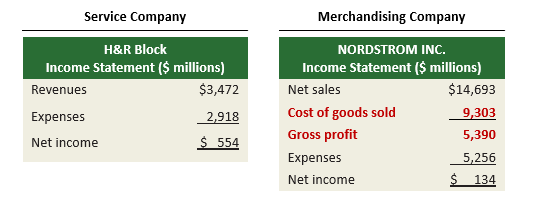

Service company vs. merchandising company

A service company sells services.

A merchandising company sells products.

The big difference is that merchandisers have inventory and cost of goods sold.

Merchandising company income statement

Net Sales - Cost of Goods Sold = Gross Profit

Gross Profit - Expenses = Net Income

Net sales

Sales - Sales Discounts - Sales Returns and Allowances = Net Sales

Operating cycle for a merchandiser

Cash → Inventory → Sales → Accounts Receivable → Cash

Business uses cash to buy inventory.

Business sells the inventory.

If sold on credit, the customer owes money.

Customer pays.

Business gets cash back.

Perpetual inventory system

This system updates inventory every time inventory is bought or sold.

It records:

Each purchase

Each sale

Cost of goods sold at the time of sale

Inventory balance after each transaction

Most companies use this now because technology makes it easier.

Periodic inventory system

This system updates inventory only at the end of the period.

Instead of tracking every sale immediately, the company counts inventory at the end.

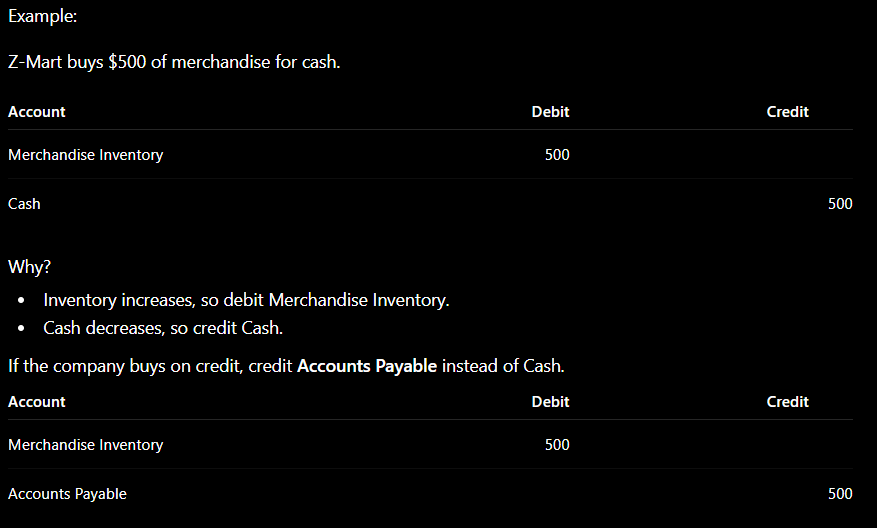

Buying merchandise

When a business buys goods for resale, it records the purchase in Merchandise Inventory.

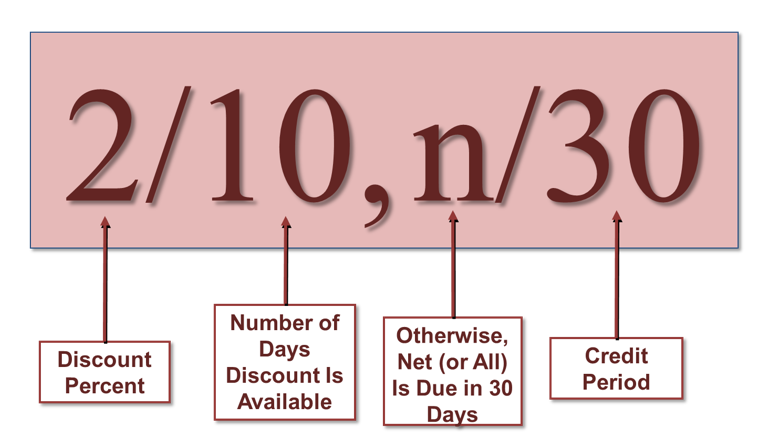

Credit terms

explain when payment is due and whether there is a discount.

Example:

2/10, n/30

This means:

2 = 2% discount

10 = discount available if paid within 10 days

n/30 = full amount due within 30 days

The buyer gets a 2% discount if they pay within 10 days. Otherwise, the full amount is due in 30 days.

Purchase return

The buyer sends merchandise back. These happen when the buyer is unhappy with the merchandise.

= we bought it and returned it.

Purchase allowance

The buyer keeps the merchandise but gets a price reduction because of defective or unacceptable merchandise. These happen when the buyer is unhappy with the merchandise.

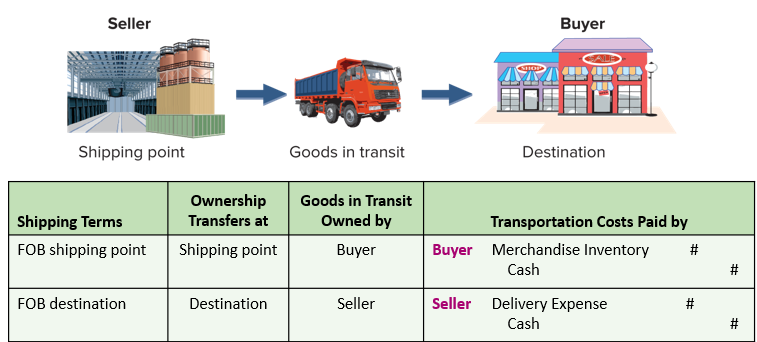

Transportation costs and FOB terms

FOB(Free on Board) tells who owns the goods during shipping and who pays shipping.

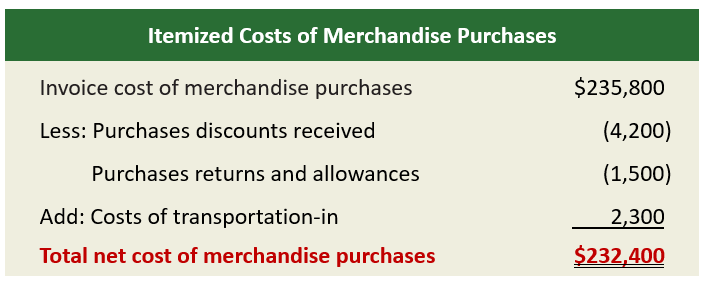

Net cost of purchases

Invoice cost of purchases

- Purchase discounts

- Purchase returns and allowances

+ Transportation-in(Transportation cost of a buyer)

= Net cost of purchases

Sales return

The customer returns the merchandise. These happen when customers are unhappy. contra revenue account.

Sales return = we sold it and the customer returned it.

Sales allowance

The customer keeps the merchandise but gets a price reduction. These happen when customers are unhappy. contra revenue account.