2. Parameter stability and structural change

1/24

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

25 Terms

What does CLRA1 mean?

What does βj interpreted as?

What are non constant parameters

We have n observations and that for the first set we have n1 observations and the second set has n -n1 observations and the β are not the same

What does it mean if we have a structural break/change?

βj1 =/ βj2 - 1 and 2 indicate subsets

the parameter is not constant

OLS estimater βjhat will be biased

It will be be some unbiased estimators of βj2hat and βj2 hat - overestimatye for one and underestimate for the other

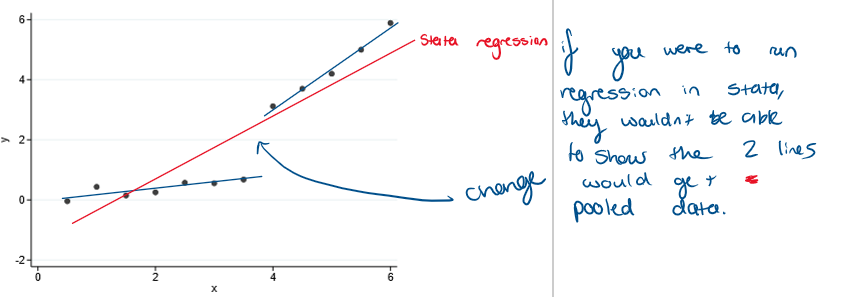

What can a sructural break look like?

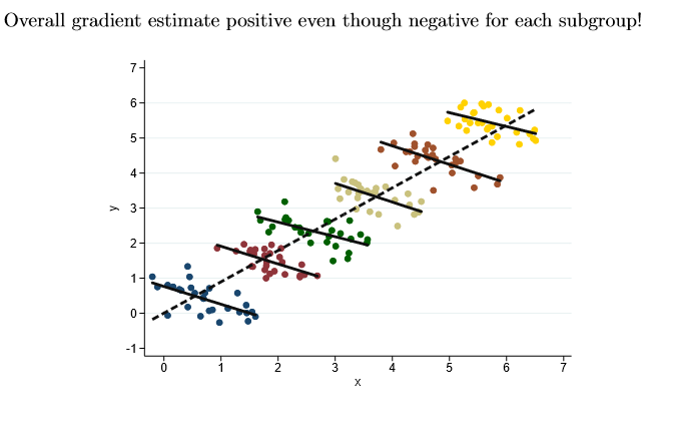

What does the Simpsons paradox look like

Why can structural change be problematic?

breaks assumption of constant parameters

May lead to misleading parameter estimates

How does structural change problems arise in cross-sectional data?

Cross-sectional data, relationships between variables may vary across different subgroups

determinants of wage may be different for men and women

determinants of life satisfaction may differ by age

How does structural change problems arise in time-series data?

Time-series data, relationships between variables may vary across different subperiods

relationships between macroeconomic aggregates change due to shocks

Determinants of aggregate excess mortality change due to Covid

What are the tests for structural change?

formal test:

Chow Test

Predictive Failure test

Informal diagnostic to idnetify potential structural breaks

recursive Least squares

What are we testing in the Chow test?

The null hypothesis is that the model 1 is correct: Yi = β0 + β1X1i + β2X2i + … + βkXki + ei

Alternative hypothesis is that any parameter is non-constant

H0: β01 = β02, β11 = β12, …. , βk1 = βk2

H1: βj1 =/ βj2 for atleast one j

How is the Chow test an F-Test

What are the 5 easy steps to do the F stat of a Chow test?

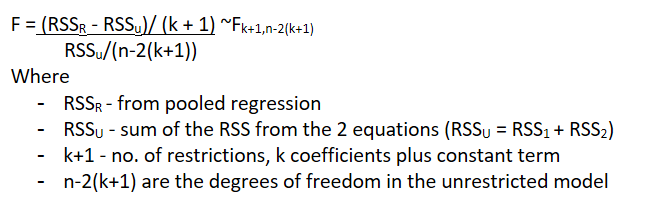

Run the pooled, restricted regression using the whole sample (1,…, n) and obtain RSSR

Run regression in group 1 using observations 1,…n1 obtain RSS1

Run regression in group 2 using observations n1+1,…,n and obtain RSS2

Calculated RSSu = RSS1 + RSS2

Calculate the F-stat and compare it to the relevant critical value of the F-distribution table - bigger values of F are rejected - if RSSR is much bigger than RSSU → more residual variation in RSSR than RSSU

What are the steps for a chow test

need critical components

need hypothesis

write F stat/ test stat

Need critical value

What are the drawbacks of the Chow Test

to calculate RSSu = RSS1 + RSS2 we require:

ei1 and ei2 are homoscedastic and independently distributed

The test does not tell us which parameter is unstable

only that any of them may be

Procedure requires us to know where structural break occurs

bc/ we need to specify where to split the sample - in practice we don’t know this exactly

May not have enough data to estimate both models seperately

esp if one sub-sample is relatively small

What’s different between the predictive failure test and the chow test

instead of estimating models for 2 samples and detecting differences We estimate the model for one sample and check whether it can accurately predict outcomes in the other sample

How does predictive failure test show there is a structural break?

If model cannot predict outcomes in the second sample → then structural break has occured

What are the hypothesis for a predictive failure test?

Null: the same model can be fitted to the second sample

H0: Yi = β0 + β1X1i + β2X2i + … + βkXki + ei i = n1 + 1, …. n1 + n2

If we impose the null on our unrestricted model what do we get

Yi = β0 + β1X1i + β2X2i + … + βkXki + ei i = 1,2,..n1+n2

How is the predictive failure test an F-test of multiple regressions

What are the steps for a predictive failure test

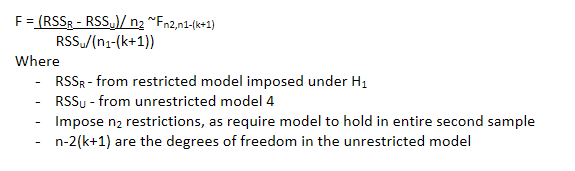

Run the full, restricted regression using the whole sample (inc all observations 1, .., n1, n1 + 1, …, n1 + n2) and obtain RSSR

Run regression in the first subgroup using only observations 1,…,n1 and obtain RSSU

Calculate the F-stat and compare it to the relevant critical value from the F-distribution table

How can we use the predictive failure test using dummy variables?

How can we know when where a break is?

differences btw/ groups in cross-sectional data

break after a major event in time-series

Data-driven way to identify potential breaks - recursive least squares

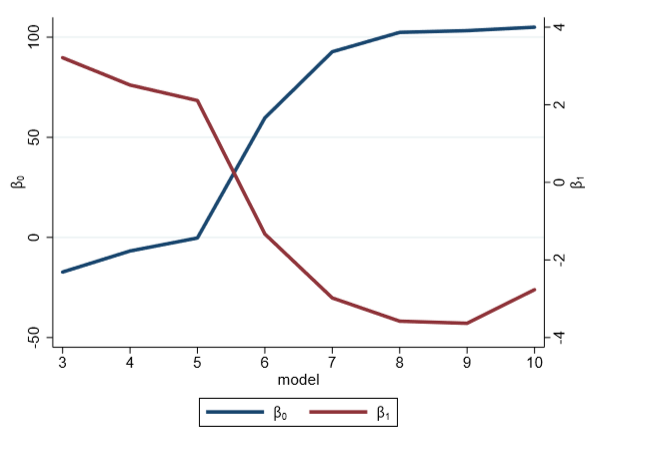

What is the procedure for Recursive Least squares

Fit model on smallest possible subsample (first k+1 observations)

Obtain βjhat

Extend sample by 1 observation and fit model again

Obtain another set for βjhat

Repeat adding one observation at a time, until entire sample used

Obtaining a sequence of sets for βjhat

Plot the sequence of values for each parameter

visual inspection will tell you where the break might be

What could it look like if there is a break using reclusive least squares