Markets and Regulations

1/57

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

58 Terms

Economic analysis of law

application of economic theory to predict effects of legal sanctions on behavior

Legal sanctions function like prices that influence behavior

Laws as incentives and prices

traditional definition: laws are obligations backed by state sanctions

economic perspective: laws create implicit prices for behaviors

Core principles of economics

efficiency

welfare

transaction

Efficiency

A change is efficient if total benefits are greater than total costs

pareto efficiency: at least one person is made better off while making no one worse off (win-win)

kaldor-hicks efficiency: an allocation can be efficient even if someone loses, as long as the winners could compensate the losers (potential win-win)

limitations of efficiency as a goal:

efficiency is not equity: focuses on total welfare, not distribution

efficiency is not fairness: considers outcomes, not process

efficiency is not maximizing happiness: based on willingness to pay, not utility

Welfare

Welfare = utility = satisfying desires

monetoary or non-monetary

subjective (similar phenomenon increases welfare for some, decreases for others)

indifferent (we don’t judge people’s desires)

Transaction

transfer of property rights

simultaneous economic and legal change:

physical/digital transfer of good or service

economic transfer of money

legal transfer of property rights

Transaction costs: information, bargaining, decision-making, monitoring, enforcement costs

Measuring costs-benefits

consider opportunity costs: the value of the next-best alternative foregone

ignore sunk costs: costs that will be incurred whether or not an action is taken

use marginal analysis: focus on additional costs and benefits

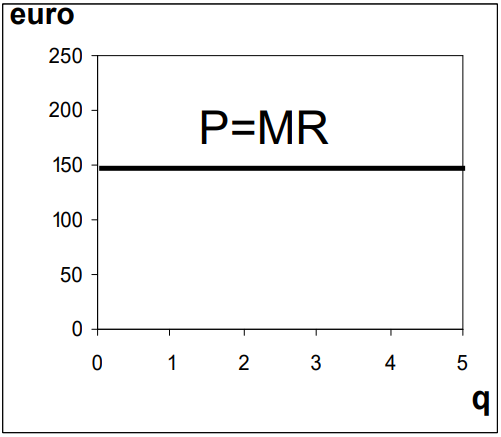

perfect competition

many suppliers and consumers

homogeneous goods

no transaction costs:

perfectly transparent

(property) rights defined

free entry and exit

Price is given because it is based on what people are willing to pay/supply and demand

P=MR because in perfect competition, MR would only equate to the price someone pays for the good (MR is also equal to MC in perfect competition)

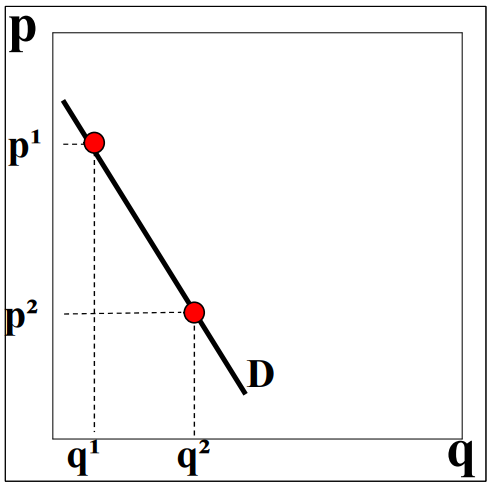

Demand

Demand = consumers

Demand curve = willingness to pay

Demand curve decreases (the higher p, the lower q)

price elasticity

how much the quantity demanded of a product changes in response to a change in its price.

elastic demand: effect on q is large (> -1%) → price increases but demanded quantity decreases strongly

inelastic demand: effect n q is small (< -1%) → price increases and demanded quantity hardly decreases

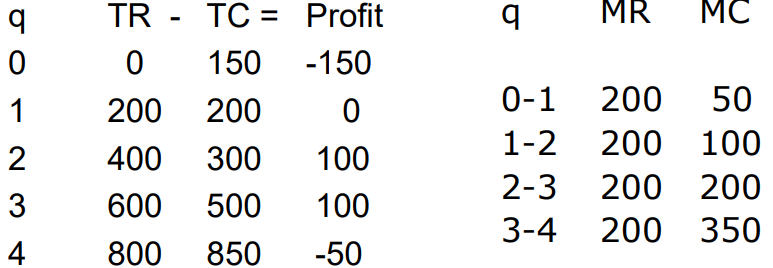

profit

revenue - cost

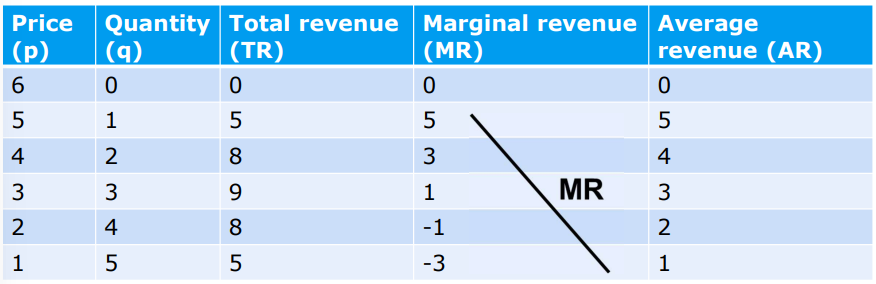

Revenues

price x quantity

Total Revenue = price x quantity

MR = Marginal revenue (the revenue you get if you sell one more good)

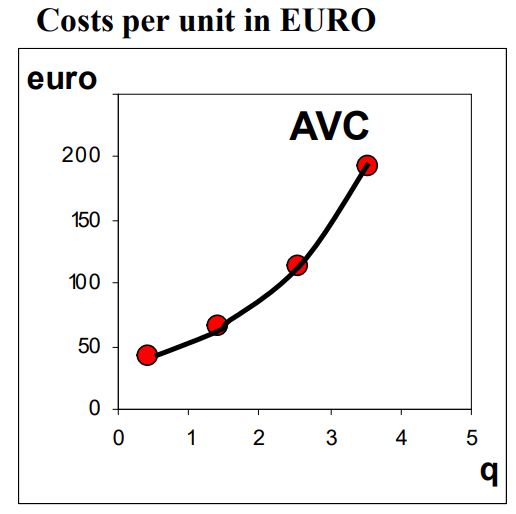

Costs

fixed costs: machines or land costs that are given

variable costs: labor or other factors that can change

Average variable cost curve (AVC)

Total variable cost (TVC) = average wage rate x number of workers

Average variable cost (AVC) = TVC/quantity

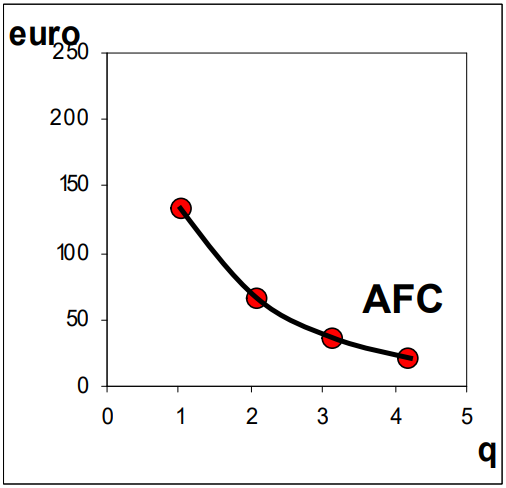

Average fixed cost curve (AFC)

TFC = total fixed costs

independent of production level

average fixed costs (AFC) declines

AFC = Fixed Costs (FC)/quantity

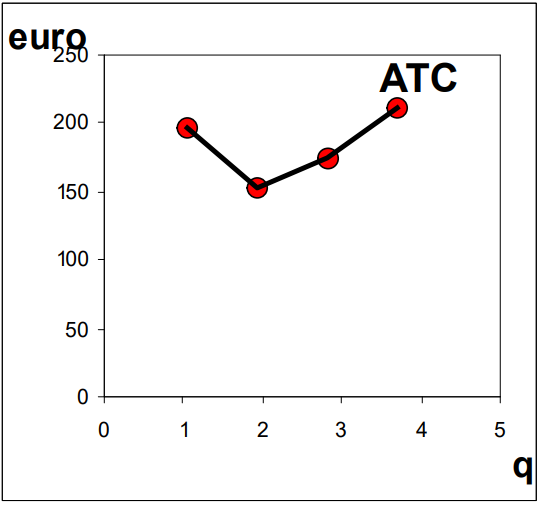

Average total cost curve (ATC)

Total costs (TC) = Total Variable Costs + Total fixed Costs

Average Total Costs = Total Costs/quantity

Average Total Costs = Average Variable Costs + Average Fixed Costs

ATC curve includes payment to shareholders and/or banks (hence profit)

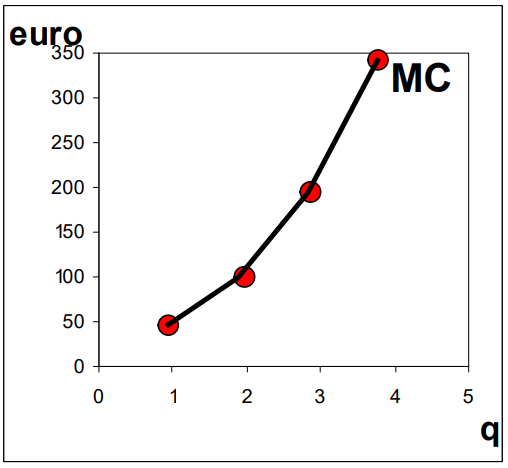

Marginal Cost Curve (MC)

Marginal costs = extra costs when production is expanded with 1 unit (exactly the inverse of MR)

When is profit maximized?

When MR=MC in perfect competition

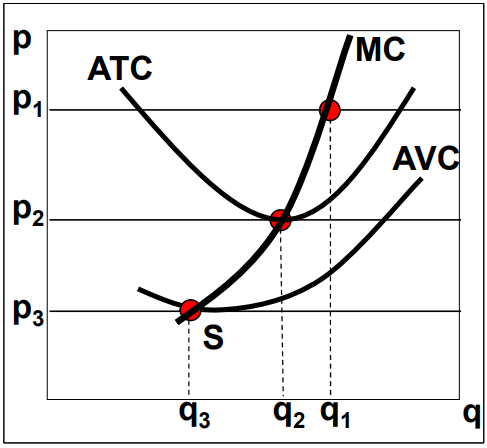

MC curve as supply curve

MC until S = supply curve for producer

price lower than ATC: loss

price below S: shutdown point

Line of reasoning:

P = MR with perfect competition

profit is maximized at MR = MC

MC = supply curve

Optimal production level

MR is greater than MC: expand → more profit

MR is less than MC: expand → less proft

Optimal: MR = MC

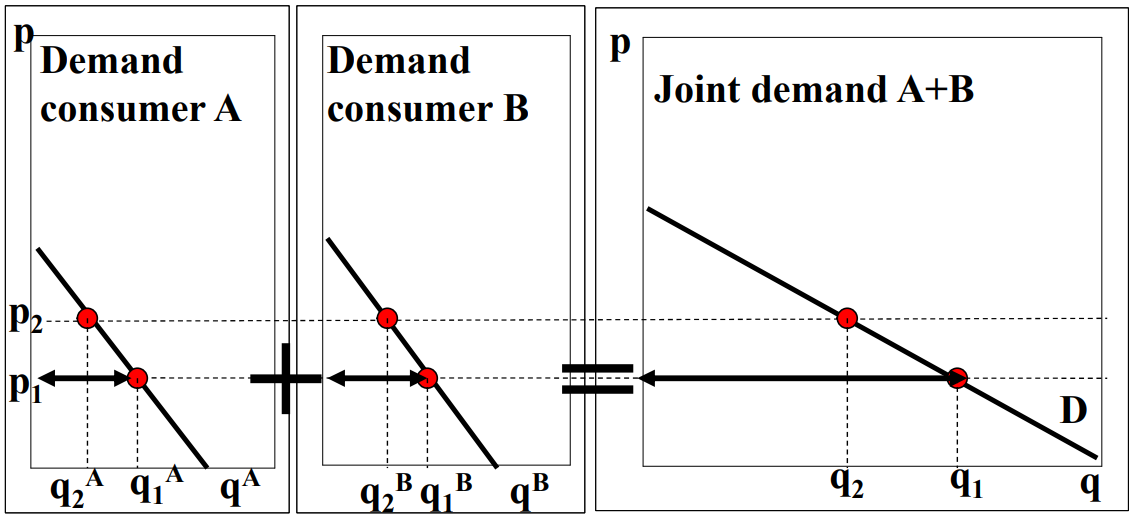

Market demand curve

add up all demand curves

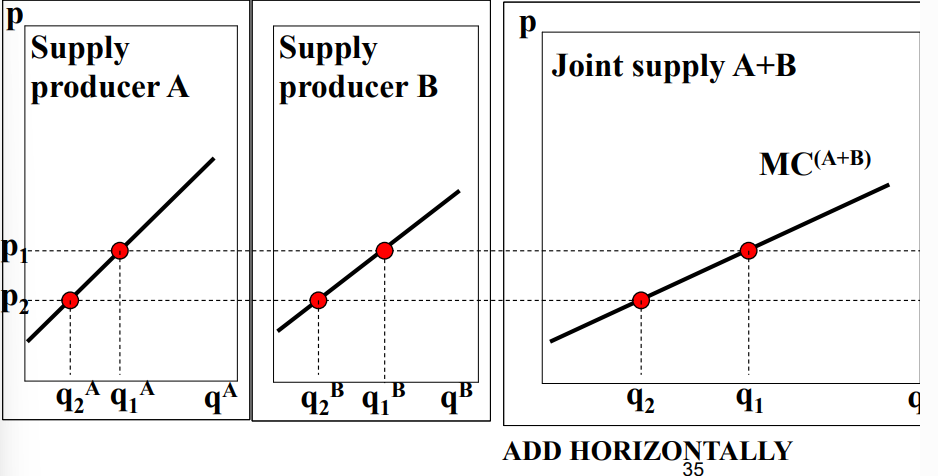

Market supply curve

shows the relationship between price and the total quantity producers are willing to supply.

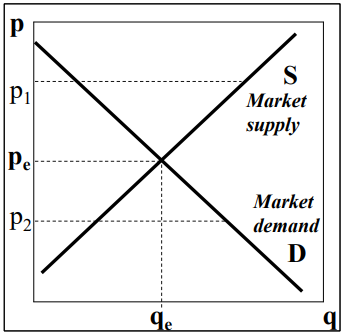

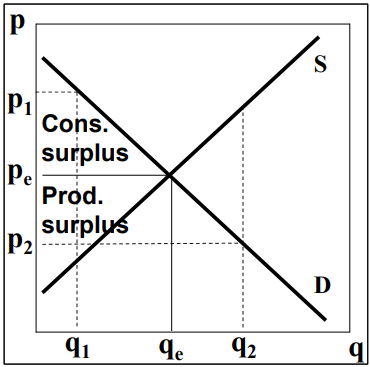

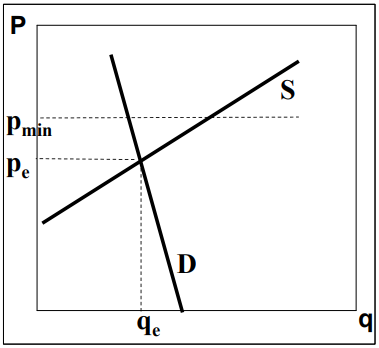

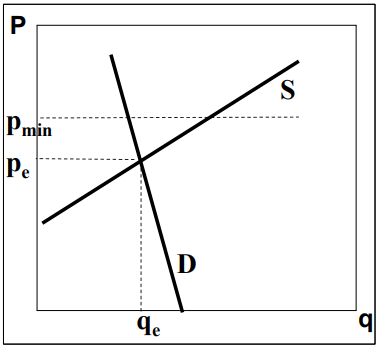

Market equilibrium

Pe = equilibrium price

Qe = equilibrium quantity

(p > Pe → impossible)

(p < Pe → impossible)

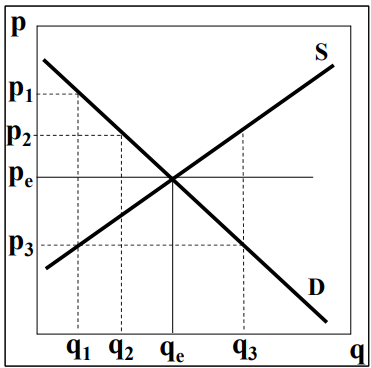

Pareto-efficient market equilibrium

only one equilibrium price: Pe

at P1 & q1 (and P2 & q2) both producer and consumer can increase welfare

continues until pe & qe: consumer and producer surplus is maximal

At p3 & q3 welfare decreases for both

Surplus

Consumer surplus: difference between price that consumers are willing to pay and equilibrium price

Producer surplus: difference between equilibrium price and price that entrepreneurs want to receive

Total surplus: consumer surplus + producer surplus

trading implies that both consumers and producers are better off (both welfare gain)

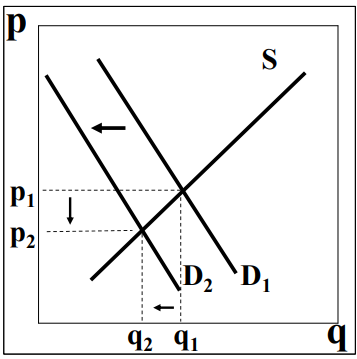

Changing demand

Demand curve D1 shifts:

preferences change

number of consumers changes income distribution changes

price of another good changes

less demand: D-curve to the left)

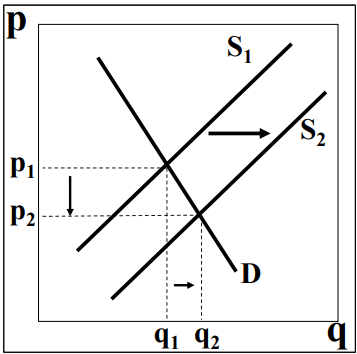

Changing supply

Supply curve S1 shifts:

price of some production factors changes

technology changes

(more supply or lower costs: S-curve to the right)

(MC decrease or: producing more at similar cost level)

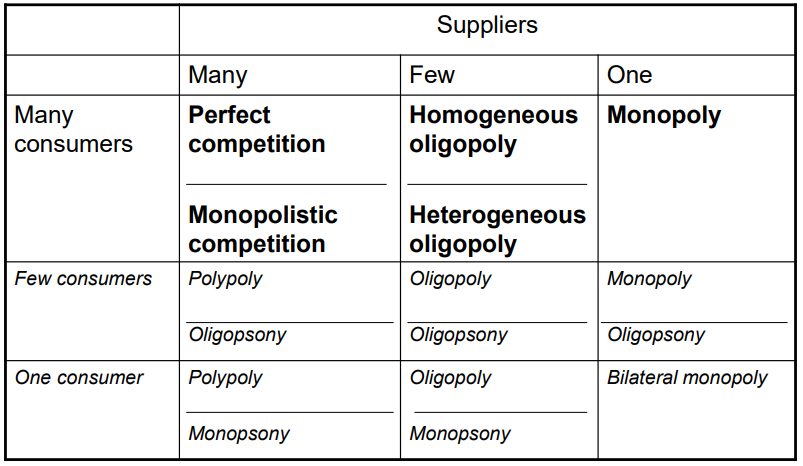

Market structure

the amount of suppliers and consumers dictates whether the market will have perfect competition, monopoly, oligopoly, oligopsony or others

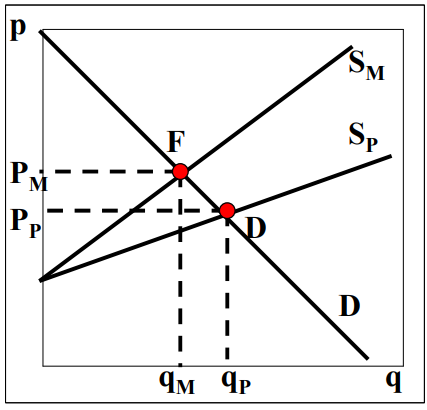

Monopoly

1 supplier: price setter

reasons for monopoly:

technical monopoly

legal monopoly

natural monopoly

advantage: low production costs

disadvantage: high price

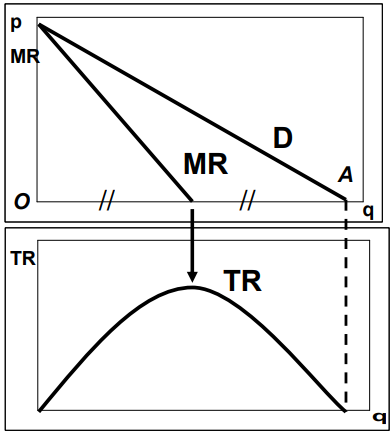

Monopolist’s revenues

demand curve = price

MR downward sloping (MR curve hits horizontal axis between O and A)

TR is maximal when MR = 0

this is not maximum profit

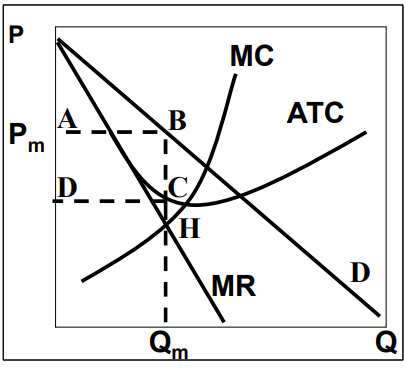

Monopolist’s costs

assumption: cost curves identical to firm under perfect competition

profit is maximal where MR = MC (in point H)

Point H gives ATC of point C and price of point B

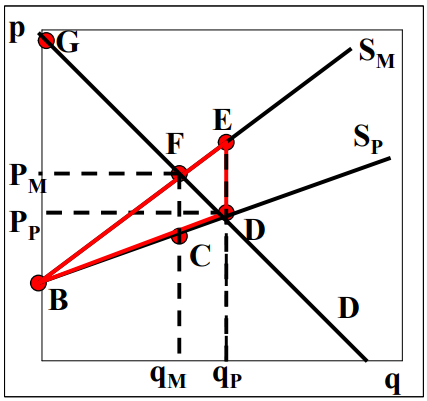

Monopolist’s profit

profit per unit is BC

costs pre unit is QmC

Sales is OQm

total (excess) profit: ABCD (namely profit per unit x sales)

Additional welfare costs of monopoly

rent-seeking: welfare costs of maintaining monopoly position

X-inefficiency: relatively weak incentive to control costs

Dynamic inefficiency: relatively weak incentive to innovate

Oligopoly

Few suppliers

Homogeneous oligopoly (identical products)

Heterogeneous oligopoly (non-identical/differentiated products

Cartel

oligopolists acting together as monopolist

unstable because:

free riding: produce more than illegally agreed

collective-action problem: cartel only enforceable in a small group or firms

entry: cartel’s excess profits attract new competitors

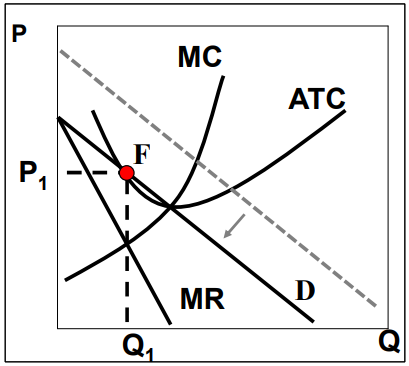

Monopolistic Competition: long term

excess profit attracts newcomers that may take away demand from existing firms

individual demand curve shifts to the left and ends in point F; P1 = ATC and MR = MC

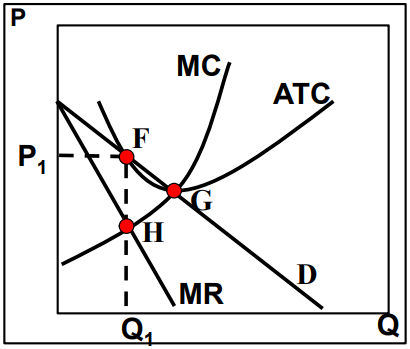

Monopolistic competition: welfare effect

prices above MC while perfect competition has P = MC

production does not occur at minimal cost (and quantity less than under perfect competition) which would be in point G

Deadweight loss FGH

Sources of market failure

imperfect competition

public goods

external effects

information asymmetries

government regulation is needed

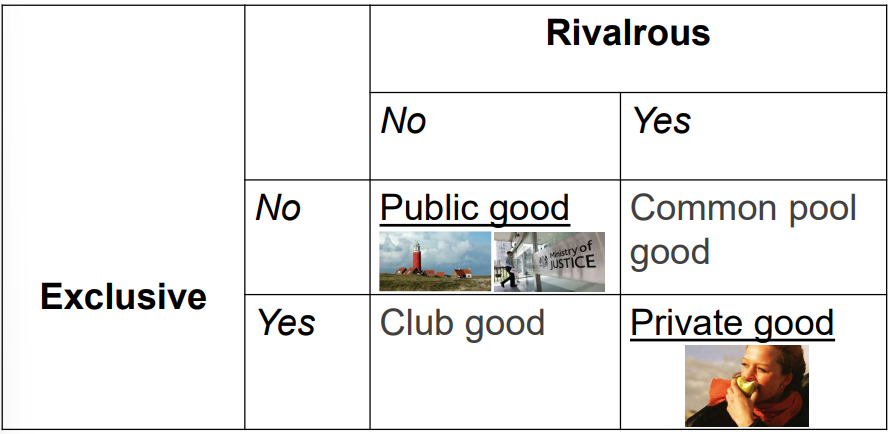

Types of goods

Can be rivalrous and/or exclusive

What are public goods?

non-exclusive and non-rivalrous goods (no individual can be excluded from its use and the use by one individual does not reduce the availability to others

causes free-riding (why pay?)

Tragedy of the commons

Refers to the tendency for a resource that has no price to be used until its marginal benefit falls to zero

solution: regulation

Quasi-public goods

private goods that are partly financed by the government

health care

education

External effects

advantages or disadvantages associated with the consumption and/or production of a good that fall on or accrue to other people than the direct users of that good without financial compensation

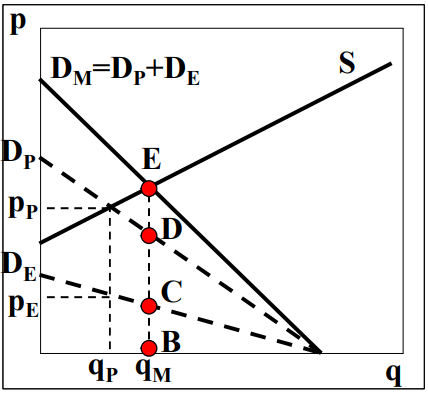

Positive externalities

Dp = demand curve paying consumers → quantity qp

qp has monetary value Pe for non-paying consumers with demand curve De (Free riding)

total social demand is Dm = Dp + De and optimal quantitiy is qm

Too little is produced ( qp instead of qm)

direct (paying) consumers versus indirect consumers (free-riders)

too low production, because supply is only tuned to direct consumers’ demand

achieve social optimum by adding demand of indirect consumers

consumer subsidy to direct users

producer subsidy

force free-riders to pay

Negative externalities

Sm = MC society costs

Sp = MC producers costs

Producers take into account Sp instead of Sm because they do not include the social costs (damage) in their MC

Too much production (qp vs qm) at a price that is too low (Pq vs Pm): socially sub-optimal

including social cost hence Sm:

consumer surplus: GFPm

Producer surplus BFPm (if production based on Sm)

No negative external effect but firms only consider Sp:

consumer surplus: GDPp

Producer surplus: BDPp

total welfare: BDG minus negative external effect

size of negative external effect

production according to Sp (instead of Sm): equilibrium D

at qp social costs of E

negative external effect: BDE

total welfare at Sp: BDG - BDE

Welfare loss at Sp: FDE

Is government regulation always necessary?

No - Cosean (market-based) approach: if property rights are clear, parties can negotiate so that the efficient outcome will emerge

Coase theorem

Bargaining leads to the (same) efficient outcome - damage is prevented or compensated irrespective of who has (or receives) the property rights. Must have:

no or low transaction costs

no public good

parties have sufficient means to compensate

clear property rights

Asymmetric information

Seller has more/better information than potential buyer = information asymmetry. Consequences:

the reservation price of potential buyers falls

lower prices than if there was perfect information

owners of quality goods have an incentive to keep them rather than sell for less than they’re worth

this causes the average quality of used goods to decline eve further

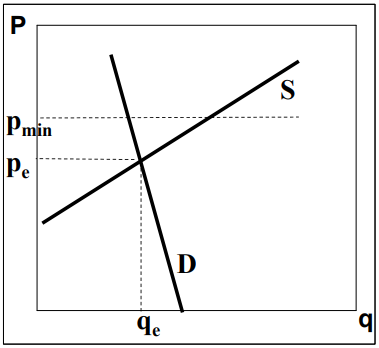

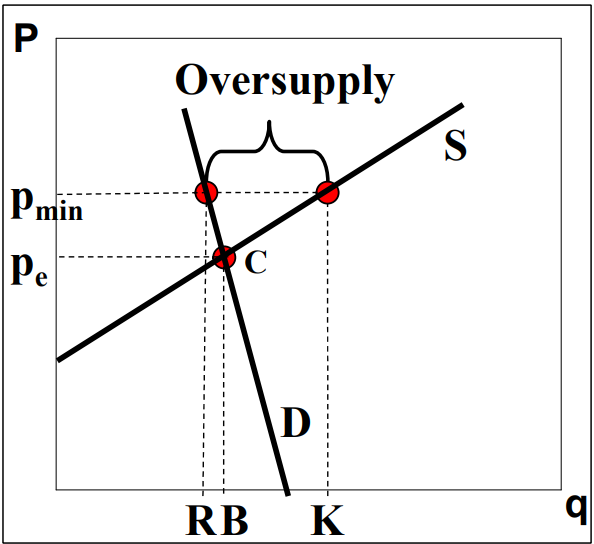

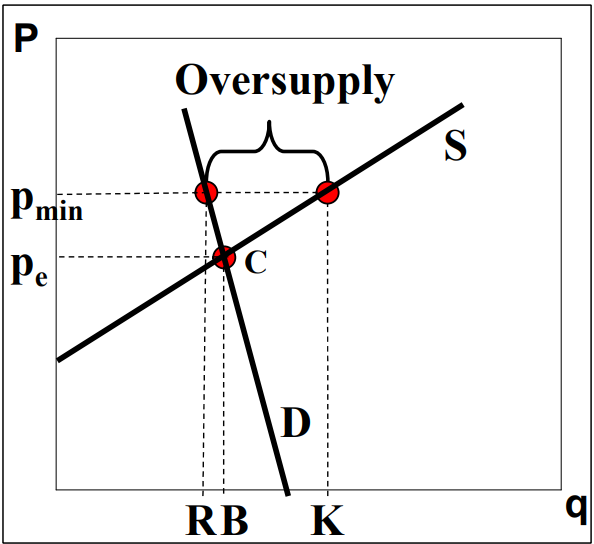

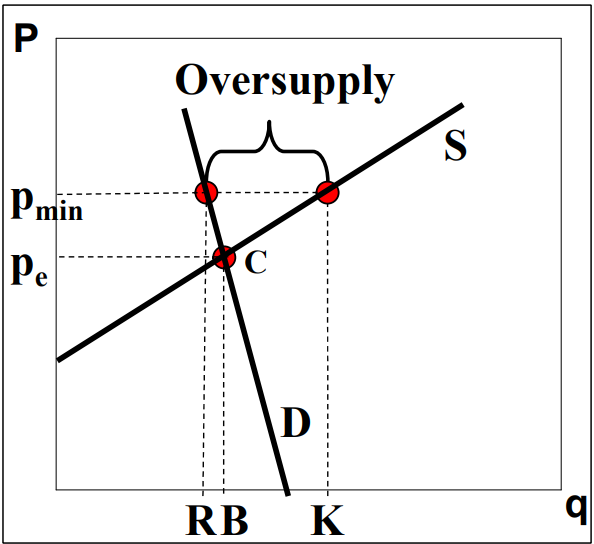

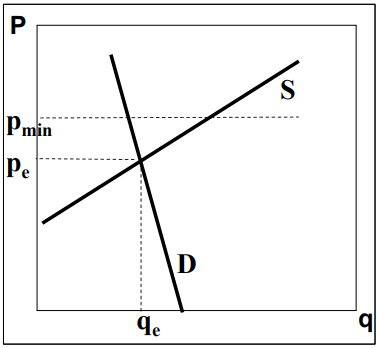

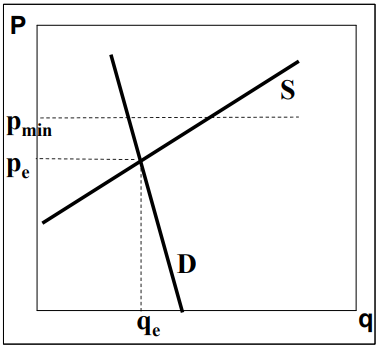

What is the effect of the minimum price Pmin on the quantity supplied and the quantity demanded?

Effect minimum (or: floor) price Pmin:

supply = q(K)

demand = q(R)

Oversupply q(RK) = milk lake

should the government buy it up?

What is the effect of the minimum price on milk producers’ revenues?

effect minimum price on producers’ revenues:

in equilibrium revenue = Pe x q(B)

now higher revenue: Pmin x q(R)

Do milk consumers gain or lose from a minimum price?

Consumer pays twice:

higher price for milk (smaller consumer surplus)

Extra tax money needed to buy up milk lake

Would a minimum price for milk be efficient or inefficient for society at large?

at Pmin demand is at qmin

consumer surplus is EFPmin

producer surplus is HKFPmin

Welfare loss is KCF, hence: (Pareto) inefficient

Minimum price for milk could be seen as fair (for producer) or as unfair (for consumer); but: consumer pays twice…

Minimum price for milk is inefficient due to welfare loss for society at large

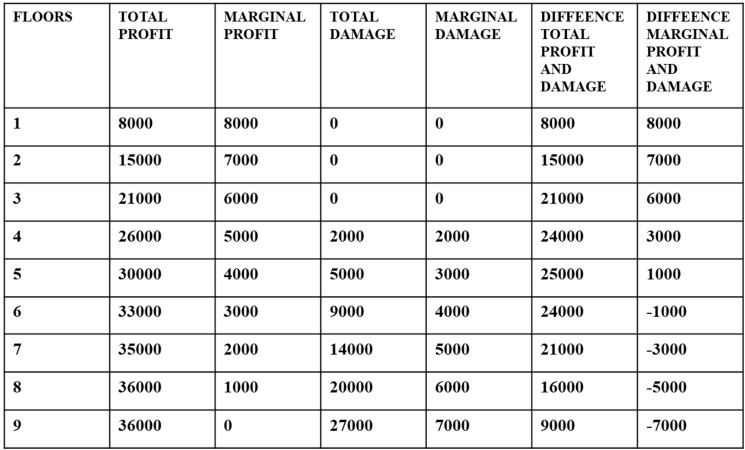

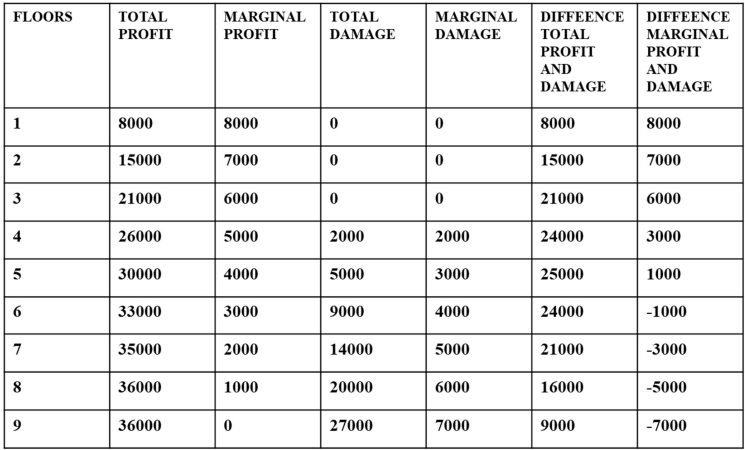

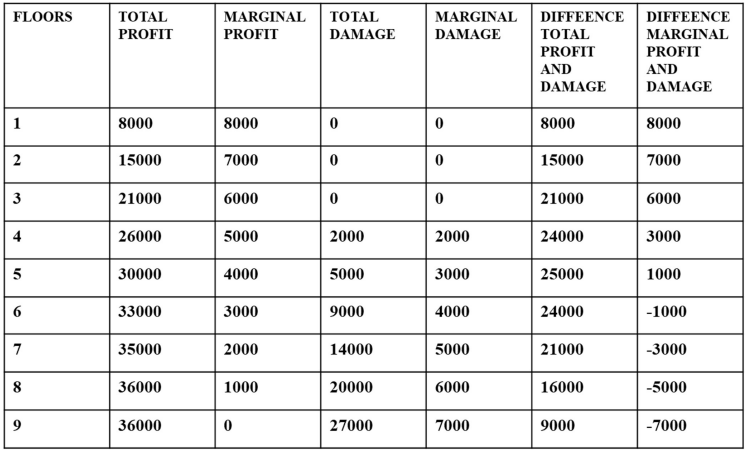

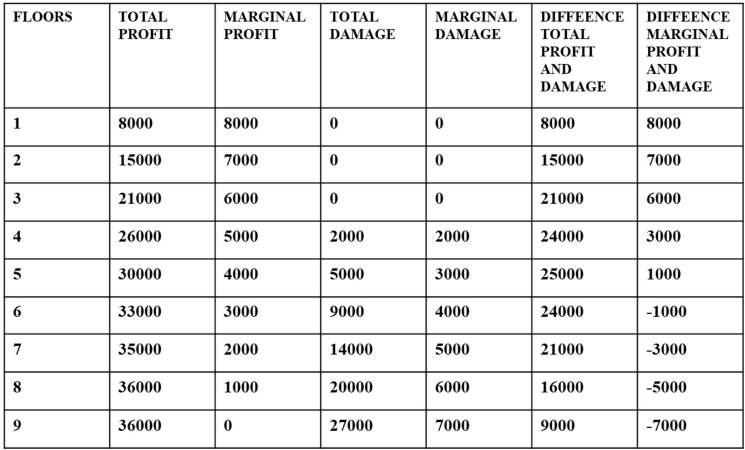

How many floors should the judge allow to ensure an efficient allocation of rights?

Efficient allocation is realized with 5 floors where MR=MC, namely where marginal profit is equal to or at least still higher than marginal damage (or: where the difference between total profit and total damage is the biggest)

Suppose the judge allows 3 floors: will the project developer comply or build more floors in case of a liability protection of local residents?

When the judge allows 3 floors, the project developer will still build 5 floors, because he can increase his profit by building 2 extra floors even though he has to compensate the damage for the local residents

Emissions trading is a market-based instrument to achieve an emission reduction target cost-effectively by allowing companies to buy and sell emission allowances. In the EU, companies are legally obliged to cover their yearly CO2 emissions with (an equal amount of) emission allowances.

Prior to 2013, electricity producers received their tradable emission allowances for free, but they passed through the market value of those rights in the electricity price.

Consumers then accused producers of making ‘windfall profits’ and argued in favour of more competition in the oligopolistic electricity market to stop or at least reduce those windfall profits.

Will more competition in the electricity market reduce or even make an end to those windfall profits from free allowances?

The opportunity costs of free emission allowances will be passed through to consumers irrespective of the electricity market structure.

However, more competition implies a bigger electricity price increase (hence a larger pass-through rate of the opportunity costs) which policymakers (non-economists) strangely refer to as higher “windfall profits”

Reason: in a (perfectly) competitive market, prices are more aligned with costs (P = MC)

More competition is good for consumers because the electricity price will be lower when competition increases

Passing through opportunity costs is economically correct. “windfall profits” are inherent to emission allowances being allocated for free, because their opportunity costs have to be passed on to consumers

Windfall profits can be avoided if politicians don’t like it: emissions allowances should then be auctioned to energy firms - which was actually done as of 2013

A higher electricity price as result of emissions trading is efficient if a previously unpriced externality, such as CO2 is not priced

What is a property right?

A bundle of rights:

right of use

right of enjoyment

right of exclusion

right of disposition

right to split this bundle of rights

3 key messages by Coase

1: social cost = externalities such as environmental pollution

problem: by negotiating over rights externalities can be internalized, so that social costs cannot exist in the classic, micro-economic model

extra assumption necessary for social cost: the existence of transaction costs

Irrelevance of the allocation of rights: to whom the rights are allocated does not matter for efficiency because without transaction costs, parties can negotiate to internalize the externality

Validity of Coase theorem is limited due to transaction costs such as:

finding information and searching for contract party

negotiating and drafting a contract

verifying behavior and, if needed, enforcing the contract