AP microecon unit 2

1/92

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

93 Terms

Law of Demand

If ↑ price then ↓ quantity demanded

If ↓ price then ↑ quantity demanded

market =

forms when multiple parties exchange things of value

strong property rights =

exclusively owned

enforceable against thieves

transferrable

demand =

all demand in the economy, the entire downward sloping curve

quantity demand =

# of goods demanded at a certain price point on demand curve

factors affecting demand

expectations of future price

income

population

preferences

substitution

normal good =

w/ more money ppl buy more, w/ less money ppl buy less

inferior good =

more money ppl buy less, buy more of another better good

market graph (draw)

expectations of future price (D)

expect to be higher = demand inc

expect to be lower = demand dec

income (D)

income inc = demand inc

income dec = demand dec

*only for normal goods

population (D)

pop inc = demand inc

pop dec = demand dec

preferences (D)

preference/popularity inc = demand inc

preference/popularity dec = demand dec

substitution

other products prices go up = demand inc (ours is cheaper)

other products prices go down = demand dec (theirs is cheaper)

substitution effect

people may not actually want more of a good, it might be a better deal compared to other goods

law of supply

If price inc → quantity supplied inc

If price dec → quantity supplied dec

factors affecting supply

price of input

price of related goods

# of suppliers

technology

expected future prices

taxes/subsidies

price of input aka land,labor,capitol (S)

price of inputs inc = supply dec

price of inputs dec = supply inc

price of related goods (S)

price of related good inc = supply dec (more lucrative to produce other good)

price of related good dec = supply inc (more lucrative to produce our good)

number of suppliers (S)

number of suppliers dec = supply dec

number of suppliers inc = supply inc

technology (S)

tech devolves = supply dec

tech evolves = supply inc

expected future prices (S)

prices expected to inc = supply dec (sell later at higher price)

prices expected to dec = supply inc (sell now at higher price)

taxes/subsidies (S)

inc taxes/dec subsidies= supply dec

dec taxes/inc subsidies = supply inc

*subsidies mean govt gives money

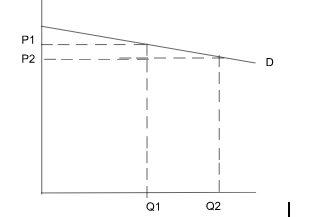

Elastic (D) =

small price change → big quantity change

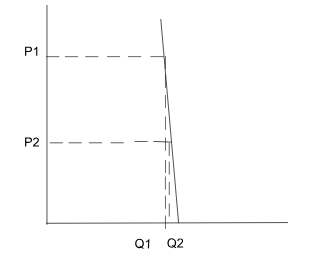

Inelastic (D) =

big price change → small quantity change

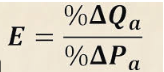

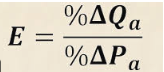

price elasticity of demand =

measuring how sensitive quantity is to price changes (very sensitive = elastic, not sensitive = inelastic)

high elasticity =

more horizontal demand curve

low elasticity =

more vertical curve

determinants of price elasticity of demand

substitutes

timeframe

income share

luxury v. necessity

narrowness do the market

substitutes (PEoD)

Many = more elasticity

Few = less elasticity

timeframe (PEoD)

Short time frame = less elasticity

Long time frame = more elastic

income share (PEoD)

Lower income share (less of ppl’s budget) = less elastic

Higher income share (more of ppl’s budget) = more elastic

luxury v. necessity (PEoD)

Necessity = less elastic (b/c need it so always need similar amount like prescriptions)

Luxury = more elasticity

narrowness of market (PEoD)

Narrower definition of market (apples) = more elasticity

broader definition of market (food) = less elasticity

perfect inelasticity

(within reason) any change in price will not change the quantity purchased

perfect inelasticity =

0

perfect elasticity =

infinity (∞)

constant unit elasticiy

% dec/inc in price = % inc/dec in quantity

Ex. 10% dec in price → 10% inc in quantity

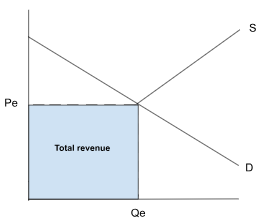

total revenue =

price * quantity

When elastic, a change in price means

Price dec = total revenue inc

Price inc = total revenue dec

When inelastic, a change in price means

price dec = total revenue dec

Price inc = total revenue inc

When unit elastic, a change in price means

total revenue stays the same between the 2 prices

region between 2 numbers is unit elastic

midpoint =

unit elastic

above midpoint =

elastic

below midpoint =

inelastic

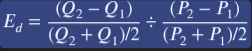

Price Elasticity of Demand formula (write =

Q = quantity demanded

inelastic situation =

|E| < 1

elastic situation

|E| > 1

unit elastic situation

|E| = 1

% change =

(new-old)/old *100

explanation for elasticity

when price of inc/dec by %, quantity demand of dec/inc by %

elastic & taxes

producers assume most of the burden (b/c quantity demanded dec but price stay the same)

some DWL, but only from producerse

inelastic & taxes

consumers assume most of the burden (b/c have to buy same amount but more expesnive

no DWL

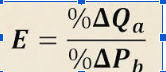

Price Elasticity of Supply (write) formula

Q = quantity supplied

Price elasticity of supply determinants

time frame

time frame (PEoS)

long run = more elastic (b/c can get more resources)

short run = less elastic (b/c can’t get more resources)

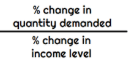

Income Elasticit of Demand (formula)

determins normal v. inferior goods

pos v. neg elasticity (IEoD)

positive elasticity = normal good

negative elasticity = inferior

elastic & positive (IEoD)

normal luxury

inelastic & positive (IEoD)

normal necessity

Cross Price Elasticity of Demand

determines if substitutes, complements, or unrelated

perfect substitutes (CED)

E = infinity/ E>0 = near perfect substitutes

complements (CED)

E<0 & negative

demand of A and price of B are inverse

no relation (CED)

E = 0

midpoint elasticity formula

works for all types of elasticity

* use ALL THE TIME

Total Revenue Test (check elasticity)

elastic = P & TR are inverse

inelastic = P & TR go in same direction

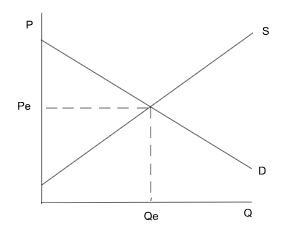

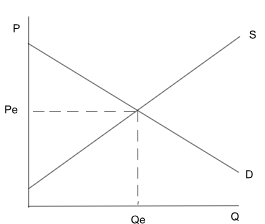

market equilibrium (draw)

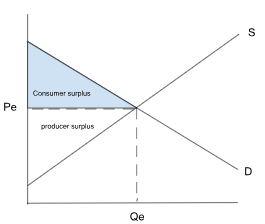

consumer surplus

total marginal benefit that consumers get above price paid (equilibrium)

b/c you could have paid higher (willingness) but you paid less (equilibrium price) so you “save money” so you have a benefit

producer & consumer surplus formula

½(b*h)

producer surplus

total marginal benefit above supply line (below supply curve = marginal cost) & below price

Needed certain price to produce a certain quantity (supply line) but are getting paid more to produce same quantity (b/c of equilibrium) so get more money aka benefit

consumer & producer surplus graph

total revenue graph

shifting supply & demand

changes P or Q

if inc/dec on both graph = inc/dec

one will always be indeterminate (on one graph inc, on another dec)

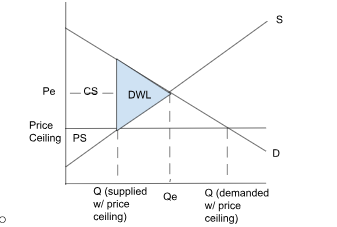

Price Ceilings =

max price set by government

*usually below equilibrium

Dead Weight Loss (DWL)

surplus loss b/c of price control (not efficient)

non-binding v. binding price ceilings

non-binding = doesnt prevent market from reaching equilibrium

binding = prevents market from reaching equilibrium

Price ceiling graph

shortage =

Qd > Qs

shortage amount =

Qd - Qs

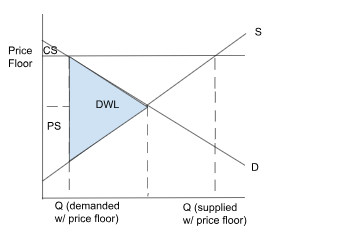

price floors =

minimum price set by govt

*usually above equilibrium (has no effect below)

price floor graph

surplus =

Qs > Qd = surplus

surplus amount

Qs - Qd

who suffers in price floor/ceiling

price ceiling = most producers suffer b/c sell at lower price

price floor = all consumers suffer b/c high prices

*ASK GPT

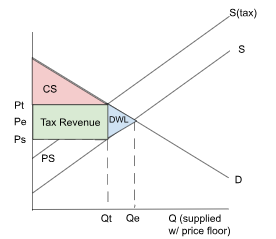

Tax Graph

Pt = price consumers pay

Ps = price suppliers pay

Qt = quantity supplied q/ tax

CS & PS dec

total tax revenue =

size of tax * Qt

tax incidence (burden of tax on market)

(old price - new price) * quantity

shared by buyers & sellers, shows how much surplus dec from CS & PS to become tax revenue

tax on seller/buyer

ta on seller = supply curve move up/down

tax on buyer = demand curve move up or down

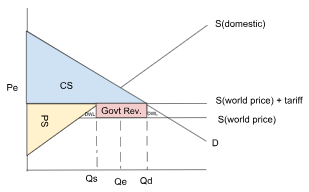

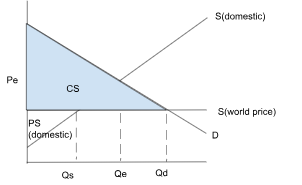

country exporting =

producers win, consumers lose (consumers pay higher price b/c new equilibrium, but producers sell more product)

country importing =

consumers win, producers lose (consumers pay lower price, producers don’t get as much revenue)

country import graph

beneficial to everyone except domestic producers b/c total surplus increases

shortage, so importing meets consumer demand

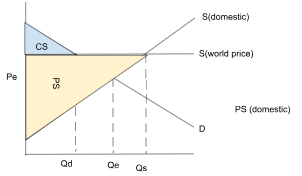

country export graph

beneficial to everyone except domestic customers b/c total surplus increases

surlus, so exporting meets producer needs

trade w/ tariffs graph

total tariff/govt rev. = size of tariff * import amount (Qd-Qs)