Chapter 9

1/74

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

75 Terms

Master trusts

multi-employer pension scheme structure with board of independent trustees, cheaper than own with more protection

NEST has

public service obligation to accept all employers under Pensions Act 2008

Eligible jobholder

Between 22 and State Pension age (SPA) earning > £10k py MUST be enrolled but can opt out

Non-eligible jobholder

MUST be provided info on how to opt-in if between 16-21 or SPA-74 earning >£10k or 16-74 earning between £6,240-£10k

Entitled worker

between 16-74 earning less than £6,240 MUST be provided info on how to opt in, employers NOT obliged to meet min contribution requirements

Employers can delay the date they enrol employee into pension by

up to three months from deadline given by pensions regulator, must provide postponement notice

Exemptions from auto-enrolment

consist of a sole director

consist of a number of directors but no more than one has employment contract

Qualifying earnings

earnings (including bonuses etc) between £6,240 and £50,270

Key stages of retirement planning

current financial position (A+Ls)

aspirations in retirement

capital needed

income for intended lifestyle

risk profile

existing retirement plans

identify appropriate solutions

implement strategy and keep reviewing

Risk profile elements

tolerance

attitude

capacity

Uses of cash in pension

to fund PCLS and first few years income payments

Uses of bonds in pension

match the maturity dates of bonds to intended retirement date

Uses of equities in pension

real return after inflation, suitable for drawdown where funds need to achieve growth to maintain income payments

Uses of property in pension

diversification, ensure pension fund maintains value during market volatility, could provide rental income for regular income stream

Lifestyling option

moves away from equities and more into bonds and cash

Lifestyling works by

switching 5-10y before, locks in gains then reinvests in cash/bonds, assumes retiree will take PCLS so target mix is 75% gilts, 25% cash

Gilts in lifestyling

protect against annuity rates falling as annuity rates are calculated from gilt yields

Disadvantages of lifestyling

switching occurs automatically at pre-set times so could lock in lower values, stops further growth also

could retire early or later so could happen too early or too late

not suitable for phased retirement or drawdown

Lifestyling assumes member will

retire on predetermined date

take PCLS

purchase annuity with remaining funds

Common characteristics of target date funds

fund has target date (a year) at beginning focus on cap growth, then gradually shifts to preserve capital

typically multi-asset funds

likely to be more dynamic management

gives discretion over timing

Pension KID

key details, illustration of annual pension, effect of charges on growth using reduction in yield figure

Since 2010

don’t have to retire to take benefits

don’t have to take benefits by 75

can take benefits before 55 if retiring due to ill health

PCLS

For defined contribution schemes, up to 25% tax free up to £268,275

Other options

invest some of it to provide income or use it to pay for planned purchases

take it all as pension and have certainty of higher pension income

Small pension pot commutation

pension less than £10k, can take all as lump sum, max three non-oc schemes can be commuted this way

Trivial commutation

can take if all pension scheme benefits lower than £30k, must be taken within 12m

do tax rules (25%) still apply

yes

UFPLS

no limit to number of payments

max tax-free cash £268,275

Taking UFPLS triggers

MPAA which limits amount that can be contributed in all future tax years to £10k

Dangers of UFPLS

risk individuals will cash in too early

can force individuals into higher tax bracket

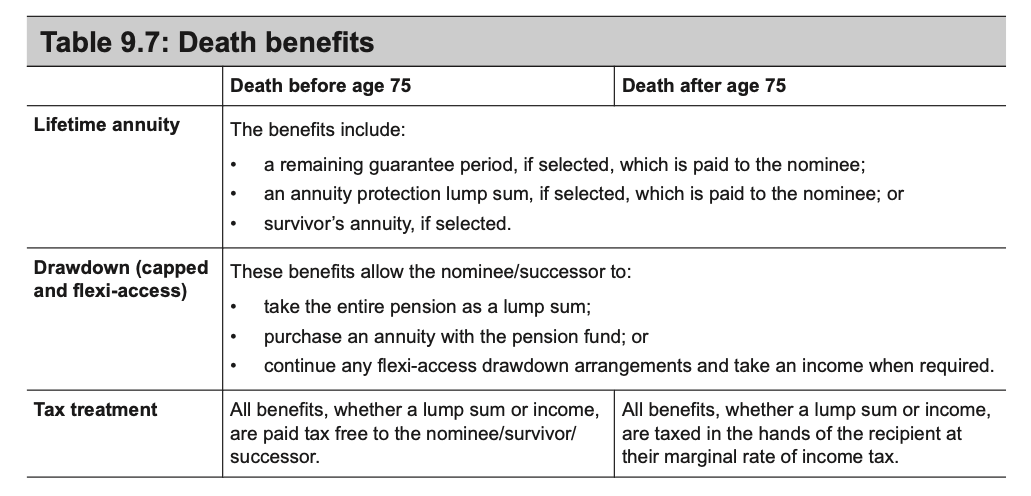

Lifetime annuity

payable by insurance company chosen

Drawdown pension

allows drawdown of income through flexible payments, can be capped or flexible

Annuity key features

monthly, quarterly, half-yearly or yearly payment

income is taxable

annuitant chooses if income stays same or increases (level or escalating)

can choose whether the income stops on death or continues to spouse, civil partner or dependant

Income provided depends on

annuity rates and pension pot

annuity rates depend on life expectancy and gilt yields

life expectancy increased and gilt yields fallen, so reductions in annuity rates

depends on the options selected

A guaranteed annuity

pays for a minimum period even if the annuitant dies during period but reduces income provided, usually 5-10y term

impaired life or enhanced annuity

impaired life pays higher cos will live less (cancer), enhanced pays higher cos of lifestyle features like smoking or obesity

Does lifetime annuity trigger MPAA

no

Capped drawdown

subject to a maximum income level (150% of income from GAD tables), but no minimum

not available now

not subject to MPAA

Flexi-access drawdown

can withdraw any amount over any period they choose

MPAA only triggered once individual takes income from the arrangement

Phased retirement

allows individual to access pension benefits while still in some form of employment, with a portion crystallised each year combining tax-free cash and taxable income

Tax benefits of phased retirement

level of taxable income can be tailored to fit in a low tax bracket

benefits of phased retirement

leaves unused funds invested in pension for potential investment growth

tax-free cash available to take in future years

annuity rates tend to get better the older an individual gets

Delayed retirement

leave their pension benefits uncrystallised when they reach their retirement age, can use other sources (ISA) and leave pension to family on death tax efficiently

Nominees

nominated beneficiaries, individuals who pension member has formally requested to receive pension benefits on their death

Survivors

refers to the individual(s) who continue to receive annuity income from a joint annuity on death of the annuitant

Successors

individuals who have been subsequently nominated, by the nominee, to receive pension benefits on the death of the nominee

Dependents

scheme pensions, those who qualify, within the scheme rules, to receive death benefits on the death of the member.

SIPPs can invest in

collective funds authorised or recognised by FCA

securities listed on stock exchanges

commercial property

bank deposits

SIPPs can be used as a

wrapper to manage a directly invested portfolio of shares and bonds

means of investing in commercial (not residential) property

structure through which to operate drawdown pension

way to finance the member’s business

Small self-administered schemes (SSASs)

occupational defined contribution schemes aimed at company directors and senior employees

How many members will a SSASs have

twelve members and all of them must be trustees

What do SSASs provide

greater control over investment of funds, ability to lend 50% of assets to sponsoring employer

Key features of ISAs

allow individuals to hold cash deposits, bonds, UK and overseas shares and certain life assurance policies

investments can be held directly or through collective investment schemes

can only be operated by HMRC approved account managers

Tax benefits of ISAs

interest on cash ISAs can be paid free of tax

dividends received from an ISA are free of income tax

there is no additional tax liability for higher- and additional-rate taxpayers

all gains are free of CGT

Eligibility rules for ISAs

only individuals

must be over 18

must be resident in UK

must not exceed subscription limit

Can ISAs be held in trust

no

Returns for innovative finance ISAs

larger than cash ISAs as its available for others to borrow

Lifetime ISAs

18-40 to open

for first home or retirement

can contribute till 50

LISA subscriptions

own limit of £4k a year

LISA early withtdrawals

25% charge even on transfers to another ISA

LISA first home

less than £450k and purchased with mortgage, can combine LISAs if home in joint names

Are ISA managers obliged to accept transfers in

no

When the investor dies, how long will the tax advantaged growth continue

earliest of

closure of ISA

completion of the administration of the deceased’s estate

three years and one day after the death

If a life insurance policy inside an ISA triggers a gain at death

that gain is also treated as tax‑free

When someone dies, any interest, dividends, or capital gains that happened before the date of death

keep their ISA tax exemption

Annual Permitted Subscription

additional allowance from deceased’s ISA benefits being passed to their spouse or civil partner (either value of ISA on death or transfer)

Can transfers be made from CTF to JISA

yes

Investment bonds are unique in that they are set up as

single premium whole of life policies, but focus primarily on investment

Do investment bonds have a min/max like ISAs

no

Tax-deferred income withdrawals

5% of the initial investment up to a maximum of 20 years after it has been made

The value of all tax-deferred withdrawals is

added to the gain on encashment to determine whether the withdrawals will attract income tax

Tax treatment of onshore bond

20% tax has been paid within the underlying investment funds so only further liability if higher-rate or additional-rate

Tax treatment of offshore bond

no tax paid, so benefits from gross roll up with investment growing at faster rate because no tax deducted, but then has to pay full income tax on gains

top-slicing relief

spreading the tax liability on a bond over its lifetime