Accounting Final Chapters

1/94

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

95 Terms

Current Liability

a debt that a company expects to pay within one year or the operating cycle, whichever is longer

current liabilities inlcude

notes payable

accounts payable

unearned revenues

accrued liabilities - taxes payable, salaries and wages payable, and interest payable

notes payable

write a promissory note

frequently issued to meet short-term financing needs

requires the borrower to pay interest

issued for varying periods

accounts payable

typically just a vendor offering a customer 30 days to pay an invoice as a courtesy

sales taxes payable

sales taxes are expressed as a stated percentage of the sales price

selling company (vendor or retailer)

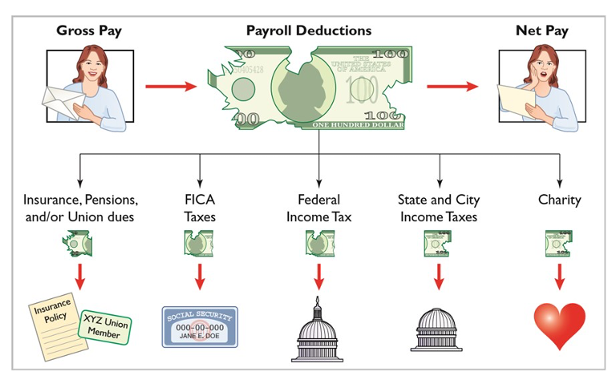

payroll and payroll taxes payable

similar to the requirement for collecting sales tax, employers (businesses) are requires to withhold certain taxes on behalf of their employees

The term “payroll” pertains to both

salaries and wages

salaries

managerial, administrative, and sales personnel (monthly or yearly rate)

wages

store clerks, factory employees, and manual laborers (rate per hour)

determining the payroll involves computing three amounts

gross earnings

payroll deductions

net pay

net pay =

gross pay - payroll deductions

payroll tax expense

results from additional taxes that governmental agencies levy on employers

payroll taxes include

employer’s share of FICA (social security and medicare)

federal unemployment taxes

state unemployment taxes

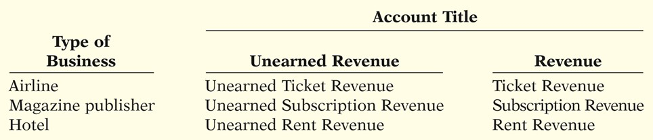

unearned revenues

revenues received by the company, delivers goods or provides services

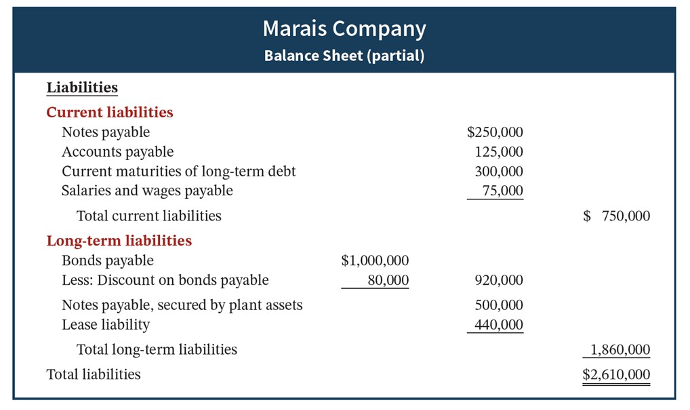

Current Maturities of Long-term debt

portion of long-term debt that comes due in the current year, no adjusted entry required

long-term liabilities

obligations that are expected to be paid more than one year in the future

bonds

a form of interest bearing notes payable - sold in small denominations, attract many investors, a corporation issuing bonds is borrowing money, the person who buys the bonds (bondholder) is lending money

types of bonds

secured, unsecured, convertible, and callable bonds

the board of directors must stipulate

the number of bonds to be authorized, the total face value, and the contractual interest rate

bond indenture

bond terms are set forth in a legal document

bond certificate

typically a $1,000 face value

represents a promise to pay

sum of money at the designated maturity date, plus periodic interest at a contractual (stated) rate on the maturity amount (face value)

bond trading

bondholders can sell their bonds on national exchanges, bond prices are quoted as a percentage of the face value

current market price (present value) is a function of three factores

dollar amounts to be received

length of time until the amounts are received

market rate of interest

market interest rate

the rate investors demand for loaning funds

determining the market value of a bond calculation

the current market price of a bond is equal to the present value of all the future cash payments promised by the bond

a corporation records bond transactions when it

issues (sells)

redeems (buys back) bonds

when bondholders convert bonds into common stock

if bondholders sell their bond investments to other investors, the issuing compnay recieves no further money on the transaction,

nor does the issuing company journalize the transaction

accounting for bond transaction

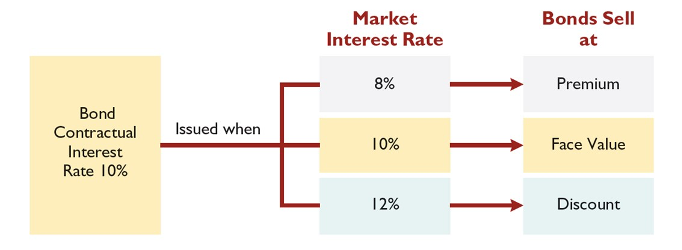

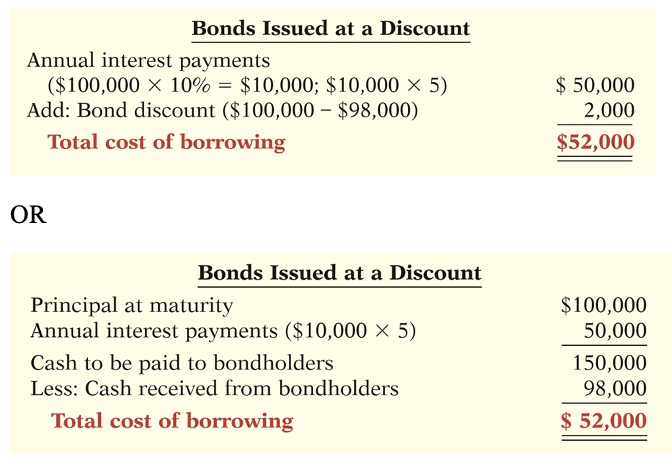

issuing bonds at a discount

sale of bonds below face value (discount) =

total cost of borrowing > interest paid

borrower is required to pay the bond discount at the maturity date

Therefore, the bond discount is considered to be an increase in the cost of borrowing

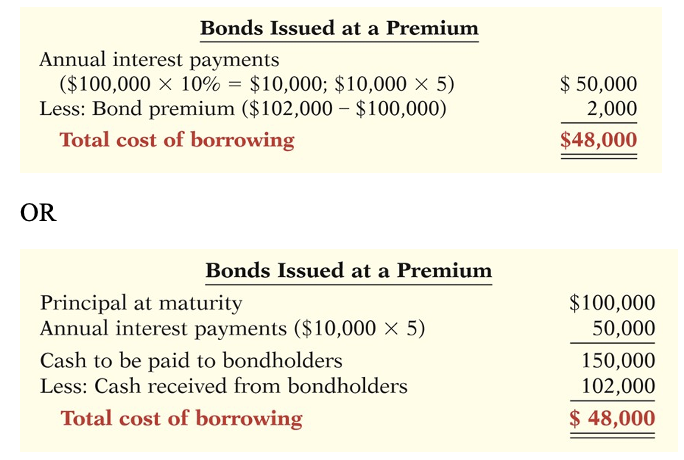

issuing bonds at a premium

sales of bonds above face value (premium) =

total cost of borrowing < interest paid

borrower is not required to pay the bond premium at the maturity date of the bonds

Therefore, the bond premium is considered to be a reduction in the cost of borrowing

When bonds are redeemed before maturity, it is necessary to

eliminate carrying value of bonds at redemption date

record cash paid

recognize gain or loss on redemption

the carrying value of the bonds

is the face value of the bonds less any remaining bond discount or plus any remaining bond premium at the redemption date

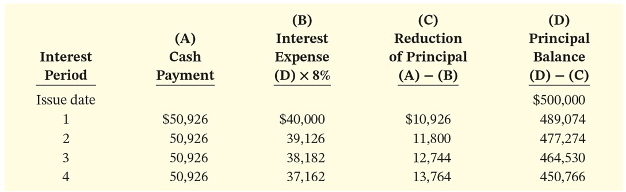

long term notes payable

may be secured by a mortgage that pledges title-specific assets as security for a loan

terms require the borrower to make installment payments over the term of the loan (interest on the unpaid balance of the loan and a reduction of the loan principal)

Companies initially record mortgage notes payable at face value

each payment on a mortgage note payable consists of

interest on the unpaid balance of the loan and a reduction of the loan principal

Balance sheet current liabilities and long term liabilities

liquidity

the ability to pay maturing obligations and meet unexpected needs for cash

the relationship of current assets to current liabilities is critical in analyzing liquidity we can express this relationship as

dollar amount (working capital) and ratio (current ratio)

working capital

the excess of current assets over current liabilities

current ratio

permits us to compare the liquidity of different sized companies and of a single company at different times

solvency

the ability of a company to survive over a long period of time

two ratios that provide information about long run solvency and the ability to meet interest payments as they come due are

debt to assets ratio and times interest earned

the higher the percentage of debt to assets

the greater the risk that the company may be unable to meet its maturing obligations

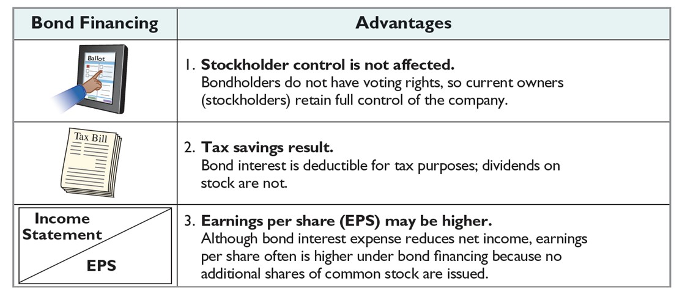

bond financing

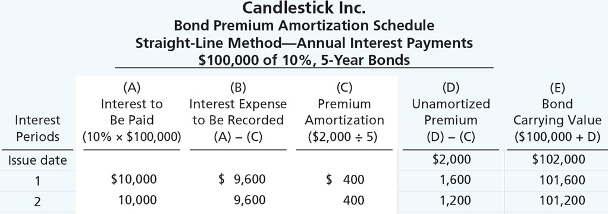

amortizing bond premium

Dec. 31 | Interest Expense | 9,600 | |

Premium on Bonds Payable | 400 | ||

Interest Payable ($100,000 x 10%) | 10,000 |

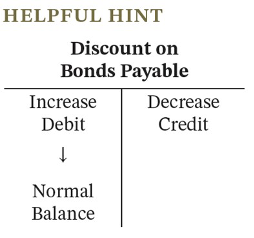

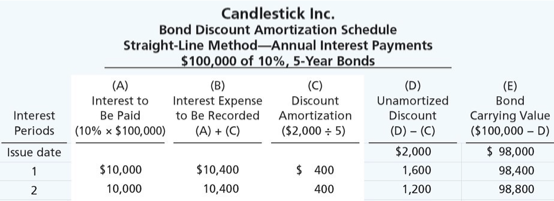

amortizing bond discount

Dec. 31 | Interest Expense | 10,400 | |

Discount on Bonds Payable | 400 | ||

Interest Payable ($100,000 x 10%) | 10,000 |

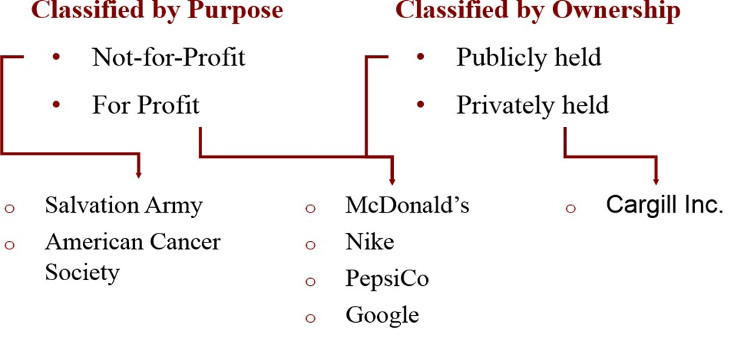

major characteristics of a corporation

an entity separate and distinct from its owners, privately held corporations are also referred to as closely held corporations

characteristics that distinguish corporations from proprietorships

separate legal existence

corporation acts under its own name rather than in the name of its stockholders

transferable ownership rights

shareholders may sell their stock

ability to acquire capital

a corporation can obtain capital through the issuance of stock

continuous life

continuance as a going concern is not affected by the withdrawal, death, or incapacity of a stockholder, employee, or officer

corporation management

separation of ownership and management often reduces an owners ability actively manage the company

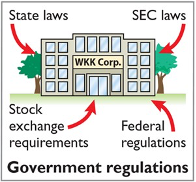

government regulations

additional taxes

corporations must pay income taxes as separate legal entity, and in addition, shareholders must pay taxes on cash dividends

forming a corporation initial steps

file an application with the secretary of state

the state grants a charter

the corporation develops bylaws

corporations engaged in interstate commerce must obtain a

license from each state in which they do business

stockholders rights

vote in election of board of directors at annual meeting and vote on actions that require stockholder approval

share the corporate earnings through receipt of dividends

keep that same percentage ownership which new shares of stock are issued (preemptive right)

share in assets upon liquidation in proportion to their holdings

residual claim

owners are paid with assets that remain after all other claims have been paid

charter indicates the maximum number of shares that a corporation is

authorized to sell

issuance of stock

companies issue common stock directly to investors or indirectly through an investment banking firm

factors in setting the price for a new issue of stock

the company’s anticipated future earnings

expected dividend rate per share

current financial position

current state of the economy

current state of the securities market

years ago par value determined the legal capital

per share that a company must retrain in the business for the protection of corporate creditors

no-par value stock

is fairly common today

in many states, the board of directors assigns a

stated value to no-par shares

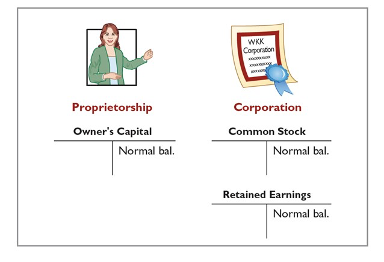

corporate capital - proprietorship versus corporation

comparison of owners equity (stockholders equity) accounts reported on the balance sheets of a proprietorship and a corporation

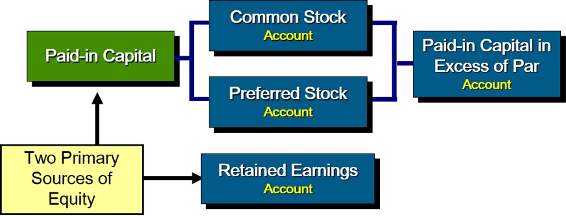

paid in capital

is the total amount of cash and other assets paid in to the corporation by stockholders in exchange for capital stock

retained earnings

is net income that a corporation retains for future use

accountings for common stock primary objectives

identify the specific sources of paid-in capital

maintain the distinction between paid-in capital and retained earnings

corporations also may issue stock for

services (attorneys or consultants)

non-cash assets (land, buildings, and equipment)

cost is either the fair value of the consideration given up

or the fair value of the consideration received, whichever is more clearly determinable

preferred stockholders have a priority as to

distributions of earnings (dividends)

assets in the event of liquidation

accounting for preferred stock

generally do not have voting rights

accounting for preferred stock at issuance is similar to that for common stock

preferred stock may have a par value or no-par value

Treasury stock

is a corporations own stock that is has reacquired from shareholders but not retired

corporations acquire treasury stock for various reasons

to reissue the shares to officers and employees under bonus and stock compensation plans

to enhance the stocks market value

to have additional shares available for use in the acquisition of other companies

to increase earnings per share

companies generally use the

cost method

debit treasury stock for

the price paid to reacquire the shares

treasury stock is a

contra stockholders equity account, reduces stockholders equity

treasury shares do not have

dividend rights or voting rights

sale of treasury stock

above cost

below cost

both increase total assets and stockholders equity

distribution

of cash or stock to stockholders on a pro rata (proportional to ownership) basis

types of dividends

cash divdends

property dividends

stock dividends

scrip (promissory notes)

cash dividends

retained earnings, adequate cash, and declared divdends

retained earnings

payment of cash dividends from retained earnings is legal in all states

holders of cumulative preferred stock

must be paid any unpaid prior year dividends and their current year dividend before common stockholders receive dividends

if stock is noncumulative

preferred stockholders are only entitled to receive their share of dividends declared in the current year (not prior years)

stock dividends

a pro rata (proportional to ownership) distribution of the corporations own stock to stockholders

reasons why corporations issue stock dividends

satisfy stockholders dividend expectations without spending cash

increase marketability of the corporations stock

emphasize a portion of stockholders equity has been permanently reinvested in the business

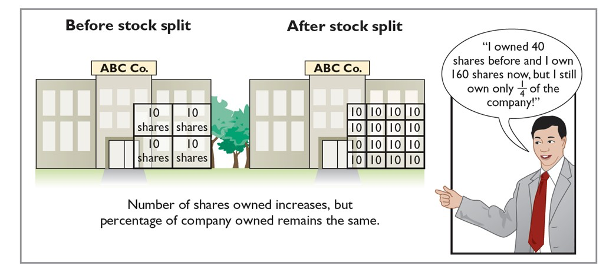

A stock split changes

the par value per share but does not affect any balances in stockholders equity

retained earnings is net income that a company retains in the business

part of the stockholders claim on the total assets of the corporation

debit balance in retained earnings is identified as a deficit

restrictions can result from

legal restrictions

contractual restrictions

voluntary restrictions