Mod. 5 Capital Budgeting

1/16

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

17 Terms

Capital Budgeting

•Lists the investments that a company plans to undertake

•Process used to analyze alternate investments and decide which ones to accept

determining if a project is worth undertaking

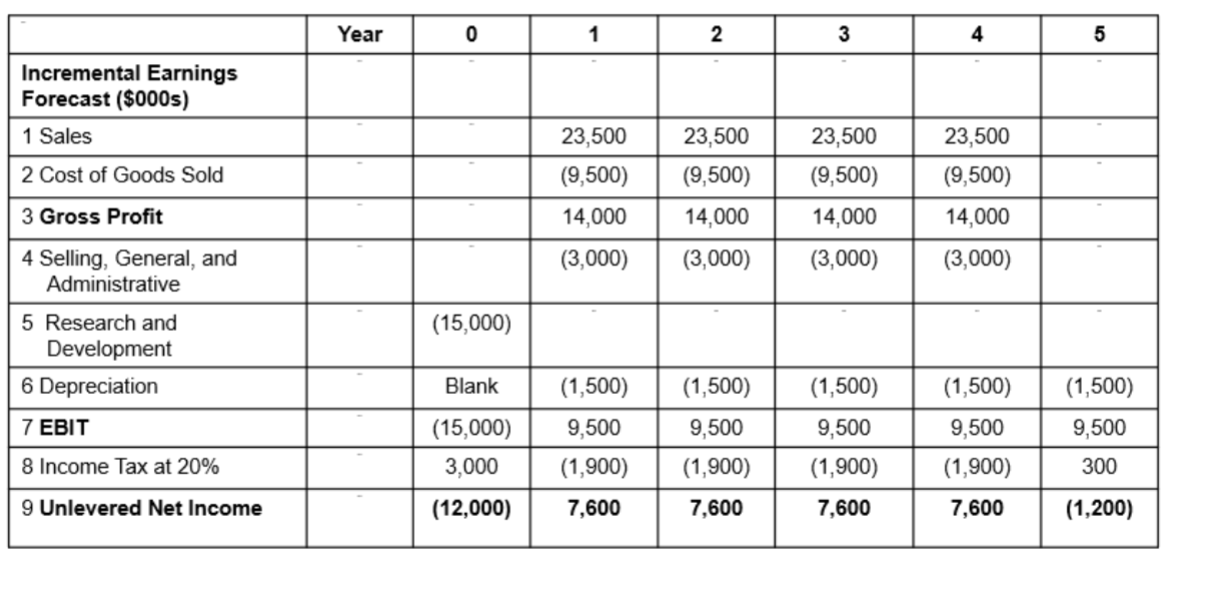

incremental earnings

•The amount by which the firm’s earnings are expected to change as a result of the investment decision

only the earnings generated by the project/ investment

the first step to capital budgeting

interest expense

•is typically not included for capital budgeting decisions

•The rationale is that the project should be judged on its own, not on how it will be financed.

Marginal Corporate Tax Rate

•on the marginal or incremental dollar of pre-tax income

•Note: A negative tax is equal to a tax credit

Opportunity Cost

•The value a resource could have provided in its best alternative use.

•Must be included in the incremental earning calculation.

ex: If you have $1,000 and you spend it on a vacation, this is whatever else you could have done with that money (investing it, buying something, etc.)

Project Externalities

Indirect effects of the project that may affect the profits of other business activities of the firm.

must be included in the incremental earnings calculation

cannibalization

when sales of a new product displaces sales of an existing product.

sunk costs

•costs that have been or will be paid regardless of the decision whether or not the investment is undertaken

should not be included in the incremental earnings analysis

Tax Expenses

are included in incremental earnings/ capital budgeting

is an additional expense on the incremental earnings (like interest expense)

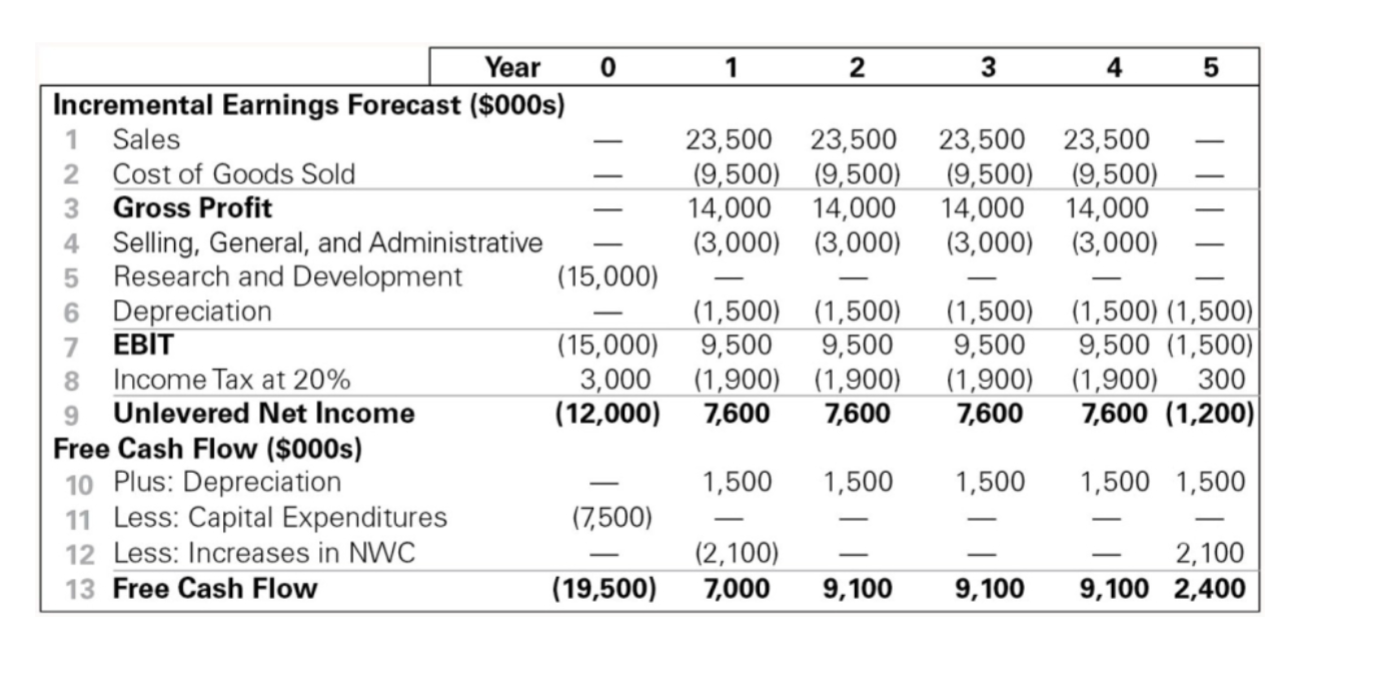

Free Cash Flow

The incremental effect of a project on a firm’s available cash

the second step of capital budgeting

is the unlevered net income + Depreciation - Capital Expenditures - changes in net working capital

Other Non-cash Items

• Amortization

• Timing of Cash Flows

• Cash flows are often spread throughout the year

• Accelerated Depreciation

• Modified Accelerated Cost Recovery System (MACRS) depreciation

Capital Expenditures and Depreciation

•Capital Expenditures are the actual cash outflows when an asset is purchased

•These cash outflows are included in calculating free cash flow

•Depreciation is a non-cash expense

•The free cash flow estimate is adjusted for this non-cash expense

part of calculating free cash flows

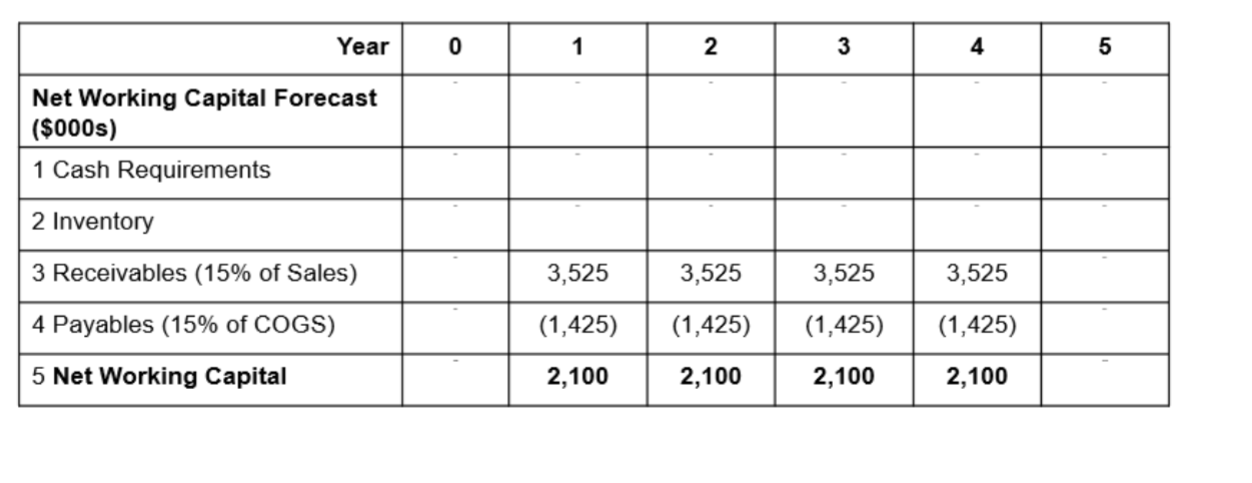

Net working capital (NWC)

= current assets - current liabilities

cash + inventory + receivables - payables

sometimes %’s are given as a total for revenue or incremental to

the % of sales (receivables)

the % of COGS (payables)

often requires investment such as trade credit

trade credit

•is the difference between receivables

and payables.

Analyzing the Project

break even analysis

sensitivity analysis

scenario analysis

ways the assumptions of the project may change in the future

Break-even analysis

•Which is the level of a parameter for which NPV = 0

•IRR is the break-even analysis of the cost of capital

•For each parameter, calculate the value at which NPV = 0

•It can be done in Excel using Goal Seek

is the individual results of changing assumptions to NPV = 0

Sensitivity Analysis

•Break the NPV calculation into its component assumption.

•Then, show how NPV varies as the underlying assumptions change

•It can be done using Data Table in Excel

the big picutre of how each assumption variable can change and impact NPV

the returns as a whole

Scenario Analysis

•Analyzing the effect on NPV of changing multiple project parameters.

•It can be done using Scenario Manager in Excel

things like best & worse cases

when multiple assumptions in the project change