ACC 403 Chapter 11

1/24

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

25 Terms

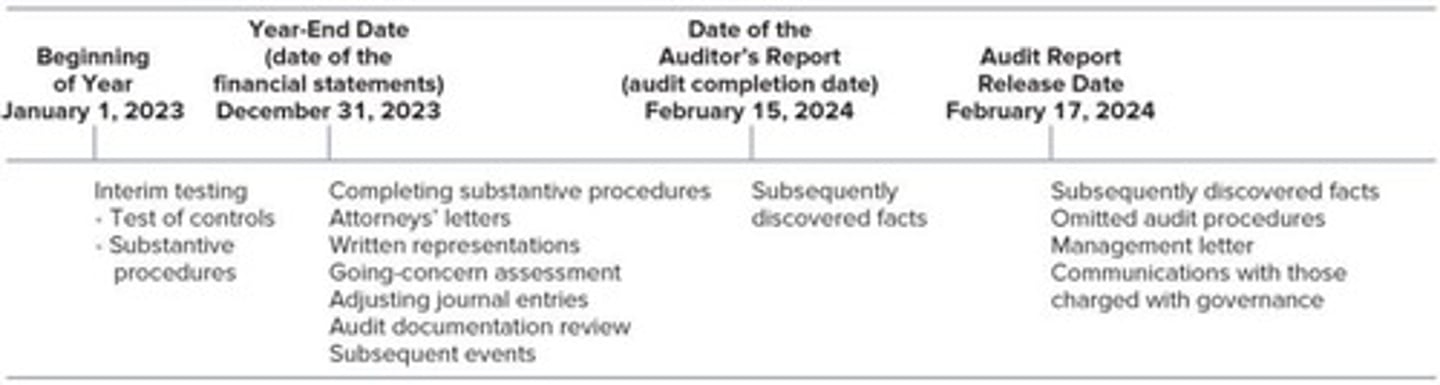

What are the four major periods in the audit timeline?

1. Prior to the date of the financial statements 2. Between the date of the financial statements and the date of the auditor's report 3. Between the date of the auditor's report and the audit report release date 4. Following the audit report release date

What are roll-forward procedures in auditing?

Procedures that extend conclusions from an interim date to the date of the financial statements.

What is the purpose of attorney letters in auditing?

To account for and disclose all material contingencies, including pending or threatened litigation.

What should be included in an attorney letter?

A list of pending litigation, a description of each item, an evaluation of the likelihood of an unfavorable outcome, and an estimate of the range of potential loss.

What is a written representation in auditing?

A written assertion provided by management to auditors regarding the entity's financial statements and internal control over financial reporting.

What are some indicators of a client's ability to continue as a going concern?

Negative trends, indications of financial difficulties, internal matters like work stoppages, and external matters like legal proceedings.

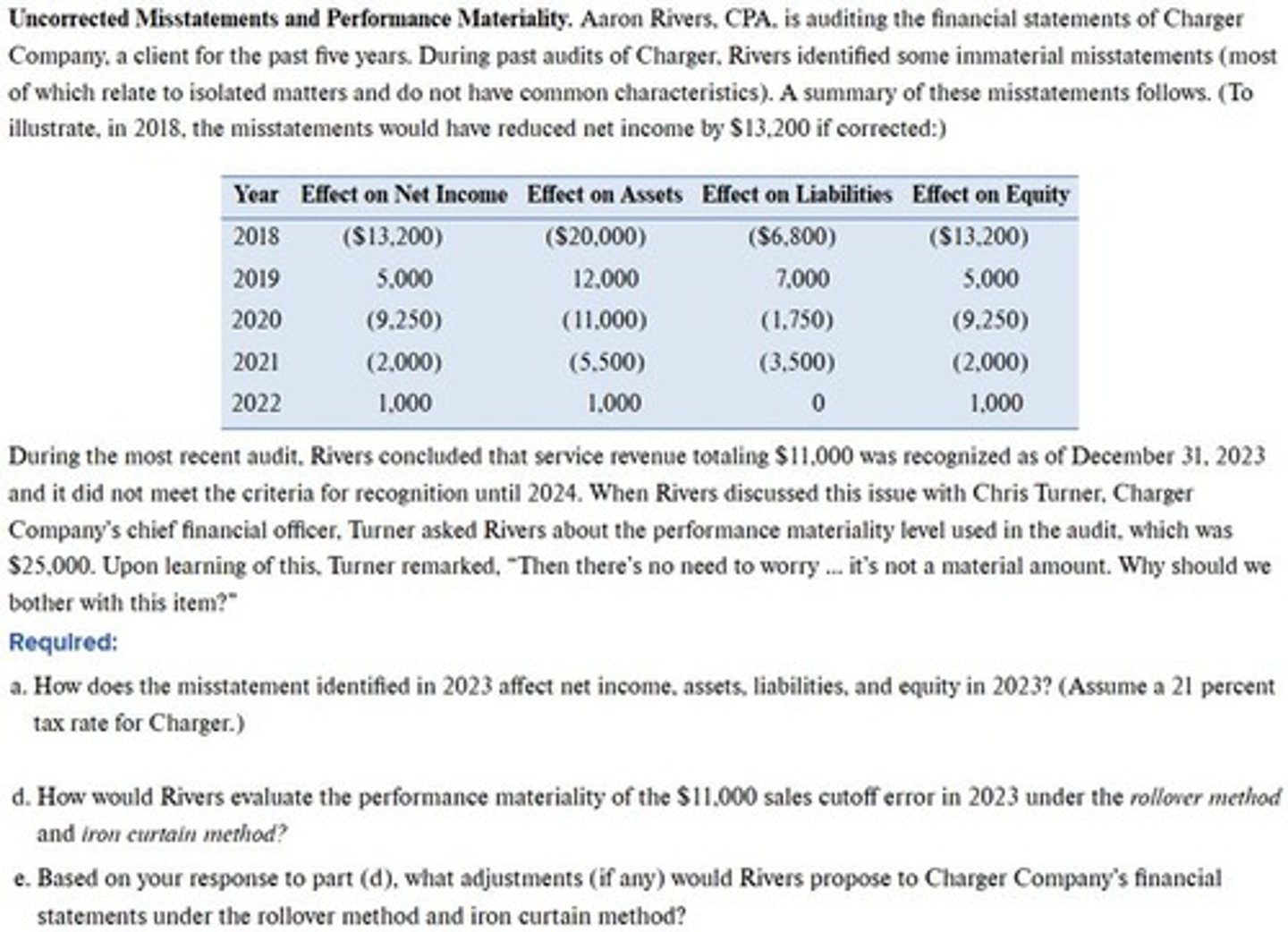

What are the two methods to evaluate the materiality of uncorrected misstatements?

1. Rollover method: considers only current-period income effects 2. Iron curtain method: considers the aggregate effect on the entity's balance sheet.

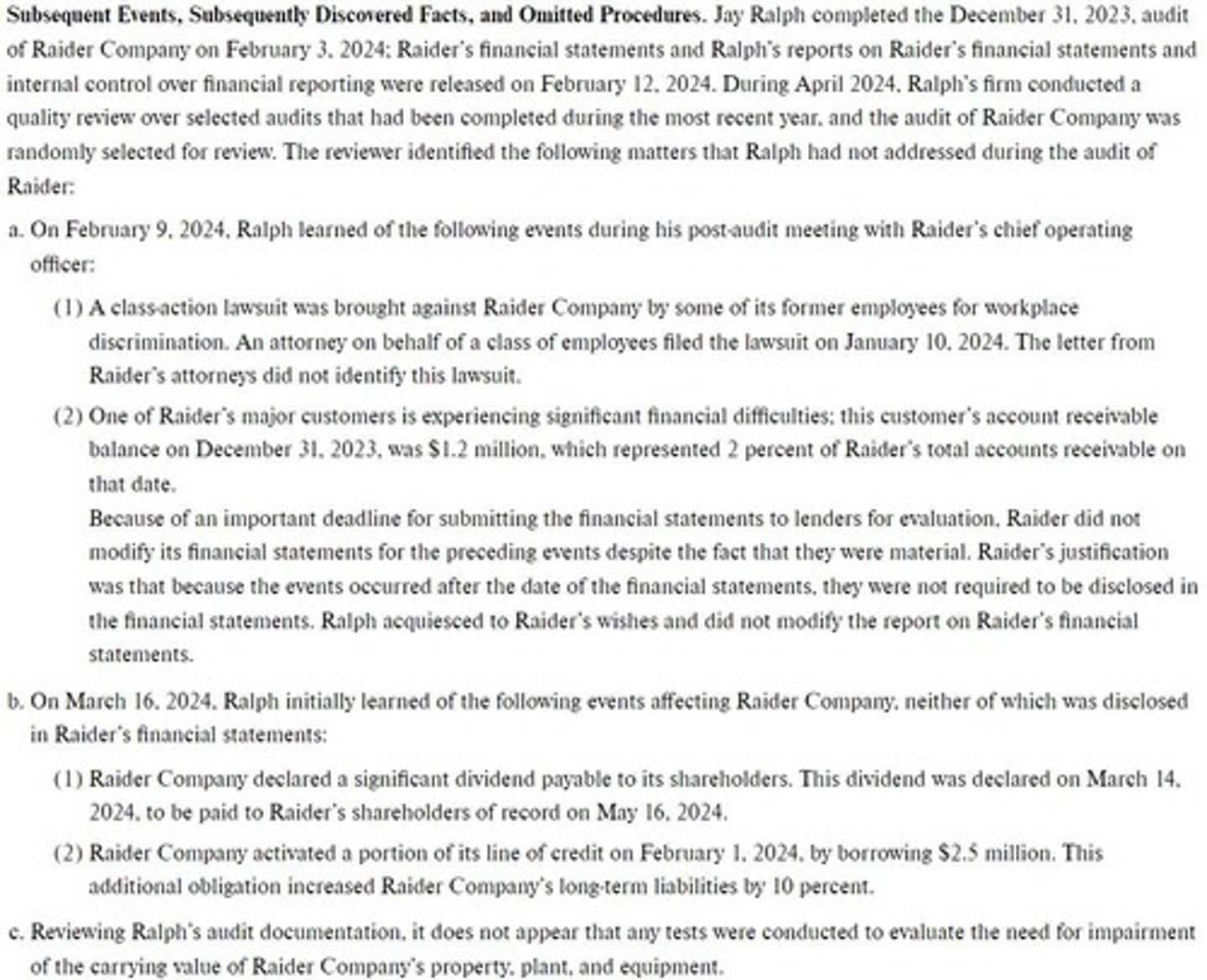

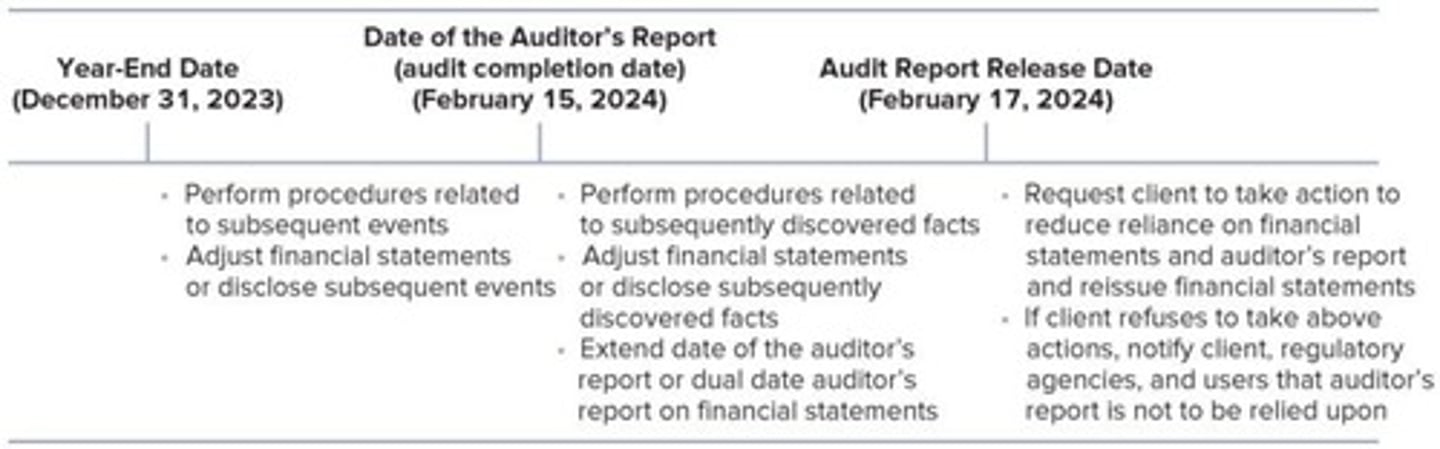

What is the auditor's responsibility regarding subsequent events?

To ensure that material subsequent events are properly identified and disclosed in the financial statements.

What are Type 1 subsequent events?

Conditions that existed at the date of the financial statements.

What are Type 2 subsequent events?

Conditions that arose following the date of the financial statements.

What should auditors do if they discover subsequently discovered facts?

If discovered after the report release date, the client should notify individuals relying on the financial statements and issue revised financial statements.

What are omitted procedures in auditing?

The inadvertent failure of auditors to perform necessary audit procedures prior to the audit report release date.

What should auditors do if omitted procedures yield results that do not support the previously issued opinion?

Issue a revised opinion and inform persons currently relying on the financial statements.

What is the purpose of audit documentation review?

To ensure all appropriate audit steps were performed and that documentation is clear and understandable.

What is the significance of GAAS in audit reviews?

GAAS requires the review of significant judgments by a second partner not involved with the audit.

What should auditors evaluate regarding accounting estimates?

For reasonableness, consistency with historical data, and potential effects of events after the financial statement date.

What is the role of communications with individuals charged with governance?

To communicate significant internal control deficiencies and material weaknesses in writing.

What is the importance of evaluating unusual account balances during an audit?

To assess whether they were previously identified and to ensure adequate evidence has been gathered.

What is the role of analytical procedures in the audit fieldwork?

To review accounts and evaluate relationships among account balances.

What is the significance of the audit report release date?

It marks the end of the audit process and the point at which certain responsibilities arise for auditors.

What happens if an auditor encounters substantial doubt about a client's ability to continue as a going concern?

The audit report should be modified to reflect the uncertainties.

What is the purpose of reviewing meeting minutes during an audit?

To inquire about the existence of subsequent events.

What is the significance of the written representation being dated?

It should be dated as of the date of the audit report, serving as a final confirmation before completion.

What is the responsibility of the client regarding financial statement adjustments?

It is the client's responsibility to adjust the financial statements, even if they do not accept auditor's proposed adjustments.

What should be communicated to the audit committee regarding misstatements?

All non-trivial misstatements should be communicated, especially if they are material.