Drafting and Interpreting Financial Statements

1/186

Earn XP

Description and Tags

All 8 chapters combined

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

187 Terms

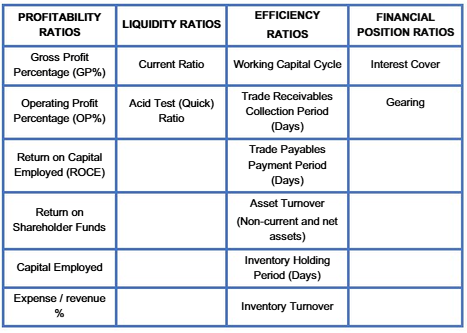

Financial Analysis

Profitability

Liquidity

Efficiency

Financial Position

Profitability

Measures looks at how successfully the business has made money during the period

Liquidity

Ability to meet its financial obligations

Efficiency

How well is business managed - and how successfully it uses resources

Financial Position

How well structured - financed by debt / equity holders

Ways of calculating financial measures

As a ratio - How the figures relate to each other.

As a percentage - One number is expressed as a proportion of another.

Making comparisons

Our own performance in previous years

Our performance this year against our own targets or benchmarks

Our performance this year against the performance of our competitors

Profitability Ratios - profits are required for;

Shareholders expect to receive a reward for the risk they have taken in investing their money in the business - this reward is the dividends.

Re-invest in new assets, or pay dividends in the future if it doesn’t perform well.

Gross Profit %

Gross Profit / Revenue

Shows how much gross profit a business makes for every £1 of sales revenue it earns.

Rising GP% = Increase in prices without an increase in COS, or reduced COS

Falling GP% = reverse of the above.

Operating Profit %

Operating Profit / Revenue

Gross Profit% but factoring in overheads

Rising OP% = Increase in GP% / Better control on expenses

Falling is the reverse of the above

Expense / Revenue

Wishing to compare how well entities control their expenses

Return on Capital Employed (ROCE)

Operating profit / (Total Equity + Non-current liabilities)

Higher the % the better, it means increasing profits whilst maintaining size.

Return on Shareholder funds %

(Profit after tax - (preference share / non con-trolling interest dividends)) / Total Equity

Used to compare existing or potential investments in different companies

Efficiency Ratios

Efficient business uses its resources on a day-to-day basis. Concerned with the management of its working apital

Inventory

Inventory Holding days = Inventory / Cost of Sales * 365

Inventory Turnover (times) = Cost of Sales / Inventory

This shows the efficiency of selling products, how long it takes on average to shift product, average number of times inventory has been sold in the period

Receivables Collection Period (in days)

Receivables / TUrnover * 365

Should match credit period offered to customers

Payables Collection Period (in days)

Trade Payables / Cost of Sales *365

The longer the better - to long may cause supplier issues

Working Capital Cycle (days)

Inventory Days + Receivables Days - Payable Days

This reflects the period of time that must be financed for when they first pay for goods or materials to the time when they receive payment from customers for sales made to them. The shorter the better

Asset Turnover (times)

Revenue / (Total Assets - Current Liabilities)

Revenue (Non-Current Assets)

The Liquidity Ratios

Current Ratio

Quick Ratio

The Current Ratio

Current Assets / Current Liabilities

This shows you how many times the company will be able to pay its current liabilities using its current level of short-term assets (Inventories, Trade Receivables, Bank and Cash Balances). Ideally sitting at 1.5-2:1

Quick Ratio (Acid Test)

(Current Assets - Inventory) / Current Liabilities

Inventories are removed as in most businesses there is a significant delay from inventory being converted into cash

Thus making this a more robust measure

A ratio less than 1:1 is often seen as a sign of as a risky level of liquidity.

Financial Position Ratios

Gearing

Interest Cover

Gearing

Non-Current Liabilities / (Total Equity + Non-Current Liabilities)

This calculates how much of the total value of the business is financed through debt

Interest Cover

Profit from Operations / Interest

How many times an entity is able to ‘cover’ its interest charges out of its profits.

Limitations of Ratio Analysis

Ratio analysis is looking at the past and not the present

Ratio analysis does not consider external factors, such as economical factors and the business environment for that industry, recession and inflation.

Ratio analysis does not measure the human element of an organisation (e.g. product quality, customer service, employee moral).

Ratio Analysis can be only truly useful when comparing with other businesses of the same size and type.

When does a group exist?

When one entity controls anothers shares by 50% or more

Goodwill

“THe difference between the amount paid by the parent for the shares in the subsidiary, and the value that has been acquired

How to measure the value acquired (goodwill)

Share Capital + Other Reserves + Retained Profit

Post acquisition profits

Post acquisition profits belong not only to the subsidiary, but also to the group.

Non-Controlling Interest

The equity in a subsidiary not attributable, directly or indirectly, to a parent.

Non-Controlling Interest must be show in the equity section

This will reflect the value of the subsidiary company which is owned by shareholders outside of the group.

Fair Values in Consolidated Financial accounts

The consolidated Financial Statements reflect the cost of the business acquired at the fair values of all of the assets and liabilities as at the date of acquisition.

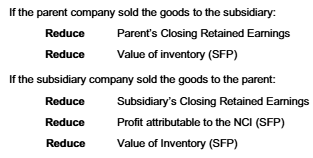

Intra-Group Transactions

Loans from one company to another

Sales of Goods or services from one company to another

Payment of dividends paid by one company to another

Loans from one company to another

There is no obligation (liability) between the group and the outside world, and so there is no need to record the loan in the consolidated accounts and we must remove it.

Sales of goods or services from one company to another

Intra-Group transactions do not affect the level of obligation to the outside world, and therefore must be removed in the consolidated statements.

It may be necessary to make an adjustment to the individual company balances at the year end to reflect items in “transit” - this could be cash or goods which have been accounted for in one entity’s accounts but not the other.

So long as the goods have all been sold to the outside world there there is no problem. The profit element of an intra-group sale is recorded in the selling company’s SPL and retained earnings in the SFP, but this is effectively cancelled out by the purchasing company recording the cost of these goods in its cost of sales computations

Unrealized profit must be removed from the consolidated statements. THerefor, a provision for unrealized profit (PUP) must be made. This provision reduces the progit and the value of the closing inventory.

The consolidated Statement of Profit or Loss

The adjusted profit of the group belongs primarily to the shareholders of the parent company. However, where there is a non-controlling interest (NCI) in the subsidiary, the NCI is entitled to receive a percentage share of the subsidiary’s profits only. this proportion of the group’s profits which ‘belonds’ to the NCI should be caculated first, with the proportion ‘belonging’ to the parent company then being calculated as a balancing figure.

ELimiate intra-group transactions from the revenue and cost of sales figures

Eliminate unrealized profits on goods still in inventory at the year end.

nifty cheat sheet

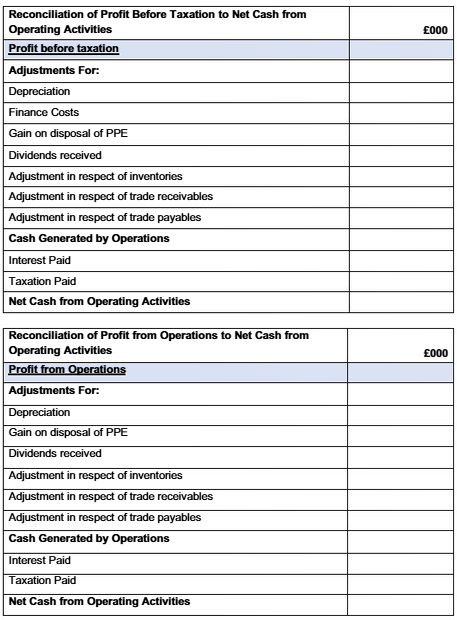

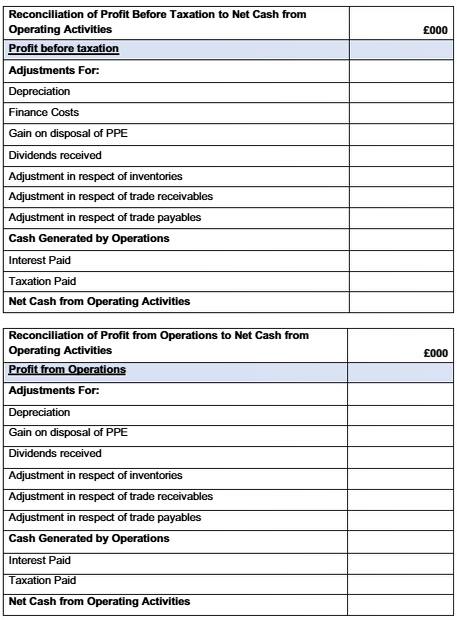

Starting point of a Statement of Cash Flows

To reconcile the profit for the year to the net cash that has been generated during the year.

What do we need to start then?

Trading Profit of the business

How do we calculate the Trading Profit from Profit before tax?

Profit before tax

+

Finance Costs

+

Depreciation

+

Loss on disposal of PPE

-

Dividends Received

=

Trading Profit

How do we calculate the Trading Profit from Profit from Operations?

Profit from Operations

+

Depreciation

+

Loss on disposal of PPE

-

Dividends Received

=

Trading Profit

Depreciation (Cash Flow)

Identify the depreciation charge for the year. It is a non-cash item that has decreased our profit and is not part of our ordinary trade, so we will need to add it back to our profit.

Dividends received (Cash Flow)

Dividends received are not part of profit from operations - they will be dealt with under investing activities

Gain/Loss on Disposal of PPE (Cash Flow)

A gain or a loss arising from the sale or other disposal of a non-current asset should not be included in the profit from normal trading/operations.

Finance Costs (Cash Flow)

This is not ordinary trade, and is thus added back. It is later deducted in the second half of the Cashflow Statement

Inventory (Cash Flow)

Calculate the difference between the start and end of the year, decrease in inventories = add, increase in inventories = deduct.

Receivables (Cash Flow)

Calculate the difference between the start and end of the year, decrease in receivables = add, increase in receivables = deduct.

Payables (Cash Flow)

Calculate the difference between the start and end of the year, decrease in payables = deduct, increase in payables = add.

Finance Costs (Interest) and Taxation

The amount of tax or interest actually paid during the period can be calculated from:

Balance at start of the year + Charge for this year - Balance at end of year = Amount paid.

Second half of the Statement of Cash Flows

Investing Activities

Financing Activities

Investing Activities

Purchase of non-current assets

Disposal of non-current assets

Receipts of dividends

Financing Activities

Repayment of bank loans

Taking out new loans

Issue of new share capital (including share premium)

Payment of dividends

Disposal of PPE

Carrying amount of PPE sold + Loss (Or Gain) on disposal of PPE

Purchases of PPE

PPE at start of the year - Depreciation Charge[Acc.dept at end-Acc.dept at Start] - Carrying amount of PPE sold - PPE at end of year = -Total PPE additions

Operating Activities Cash Flows

Add Depreciation

Less investment income

Changes in Inventories, receivables and payables

Less interest paid

Less taxes on income

Interest Activities Cash Flows

Inflows

Sale proceeds from sale of PPE and other non-current assets

Interest and dividends received

Outflows

Purchases of PPE and other non-current assets

Financing Activities Cash Flows

Inflows

Receipts from increases in share capital

Increases in long-term loans

Outflows

Repayment of share capital / loans

Dividends paid

IAS 10 Events After the Reporting Period

Events after the reporting period are those events, favorable and unfavorable, that occur between the end of the reporting period and the date when the financial statements are authorized for issue.

An adjusting event

Provides evidence of conditions that existed at the end of the reporting period

Non-adjusting evenet

Is indicative of conditions that arose after the reporting period

Typical Adjusting Events

Conclusion of a court case which had been ongoing at the financial year end

Impairment of assets

A reduction in value of inventories where net realisable value falls below cost

Insolvency of a major trade customer

Discovery of fraud by an employee

Typical Non-adjusting Events

A new business combination - purchase of, or sale to, another entity

THe major purchase of non-current assets

Damage to non-current assets or loss of production capacity to fire or flood

Issue of new share capital

Taking out a new (or increasing an existing) loan

Material Adjusting Events

Are accounted for by altering the amounts shown in the financial statements to reflect the event

Material Non-adjusting events

Are included as a note to the accounts giving, where possible, an indication of the likely financial effect of the event.

IAS 12 Income Taxes

The actual tax liability is usually not agreed until the financial statements are published - hence there will often be an under-provision or over-provision of taxation in any given financial period.

IFRS 15 - Revenue from Contracts with Customers

This introduced a new model of revenue recognition that is based on the transfer of control, at what point the transfer takes place and the amount to recognize

A Contract

An agreement between two or more parties that creates enforceable rights or obligations - written, oral or implied

A Customer

A party that contracts with an entity to purchase goods or services that are the output of the entity’s ordinary activities in exchange for consideration

Income

Increases in assets, or decreases in liabilities, that result in increases in equity, other than those relating to contributions from holders of equity claims

Revenue

The gross inflow of economic benefits during the period arising in the course of the ordinary activities of the entity, when those inflows result in increases in equity, other than increases relating to the contributions from equity shareholders

Difference between Income and Revenue

Revenue is only derived in the “course of the ordinary activities of the entity”

The five step model

Identify the contract with the customer

Identify the performance obligations in the contract

Determine the transaction price

Allocate the transaction price

Recognize revenue when (or as) a performance obligation is satisfied

Identify the contract with the customer

Be approved by both parties

Identify the rights of each party

Identify the payment terms

Have commercial substance

SHow that it is probable that the entity will collect the consideration when it falls due, in exchnage for goods and services

Identify the performance obligations in the contract

Performance obligation is a promise in a contract with the customer to transfer goods or services to the customer.

Determine the transaction price

The transaction price is the amount to which the entity, in exchange for transferring the provided goods and services. Variable consideration can only be included if it is highly probable that there will not be a signifcant reversal of revenue in the future

Allocate the transaction price

Allocation is based on the relatie standalone (separate) selling price of each performace obligation. ANy overall discounts should also be proportioned evenly between each individual part.

Recognize revenue when (or as) a performance obligation is satisfied

Revenue is recognized in financial statements when an entity satisfies a performance obligation by transferring promised goods or services to a customer. This is the point that the control of the product is passed to the customer.

Performance obligation can be satisfie

Over time

The customer simultaneously receives and consumes all the benefits provided by the entity and the entity performs

The entity’s performance creates or enhances an asset that the customer controls as the asset is created

The entity’s performance does not create an asset with an alternative use to the entity, and the entity has an enforceable right to the payment for performance completed to date.

Point in time

The customer has legal entitlement to the asset

The customer has physical possession and has accepted the asset

The significant risks and rewards have passed to the customer

The entity has a present right to payment for the asset.

IAS 37 - Provisions, Contingent Liabilities and Contingent Assets

IAS 37 defines and specifies the accounting for and disclosure of provisions, contingent liabilities, and contingent assets.

Provision

A liability of uncertain timing or amount

When should a provision be recognized?

The company has a present obligation as a result of a past event

It is probable that there will be an outflow of economic resources required to settle the liability

A reliable estimate of the liability can be made

When should the value of provisions be re-assessed?

The value of all provisions should be re-assessed at the end of each financial year, and adjusted if necessary

Contingent Liability

Possible obligation arising from past events whose existence will only be confirmed by one or more uncertain future events not entirely within the entity’s control

Or

A present obligation that arises from past events. but which is not recognized because it is not probable that an outflow of economic benefits will be required, or that obligation cannot be measured with sufficient reliability

Difference between a Provision and Contingent Liability

The difference is based on the degree of certainty,

Provision is equal to or greater than 50% certainty.

Contingent Liabilities are between 20% and 50% certain - these are notes only.

Anything below 20% is known as a Remote Contingent Liability - which gets no disclosure at all including in the notes.

Contingent assets

A possible asset arising from past events which will only be confirmed by uncertain future events not wholly within the entity’s control

When are contingent assets declared in financial statements?

A contingent asset is never shown in the financial statements unless virtually certain.

If it is probable (greater than 50%) A note is included.

Otherwise, it is left out completely like a remote contingent liability.

Objective of the International Accounting Standards Board (IASB)

to develop, in the public interest, a single set of high quality, understandable and enforceable global accounting standards that require high quality, transparent and comparable information in financial statements and other financial reporting to help participants in the world's capital markets and other users make economic decisions.

Purpose of IASB's Conceptual Framework for Financial Reporting

IASB's Conceptual Framework for Financial Reporting provides us with

The Main users of Financial Statements

Investors, Lenders, Government, Suppliers, General Public, Management, Employees, Trade Unions, Competitors, and Customers

Most important users of financial statements

Current and potential investors are the most important due to being owners, thus they are put at the forefront, alongside lenders and creditors, as these three have the most to loose.

What are the underlying assumption on which financial statements should be prepared on

What is Going Concern

The financial statements are assumed to have been prepared on the basis that the entity will continue in business for the foreseeable future, and the enterprise as neither the intention nor the need to liquidate or curtail materially the scale of its operations.

What is the Accrual Basis

The effects of transactions and other events are recognised when they occur and not when the cash is received or paid.

Qualitative Characterists of useful financial information

What are the Fundamental Qualitative Characteristics of useful financial information

Relevance, and Faithful Representation

What makes information Relevant?

It is capable of making a difference in the decision-making process AND has one of the following:

What makes information have the quality of “Faithful Representation”

What are the Enhancing Qualitative Characteristics of useful financial information

Verifiable, Comparable, Understandable, Timely