pubhlth 222a: week 7 - health care delivery

1/35

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

36 Terms

hospital data & trends

Hospital care accounts for $1.5 trillion

1/3 of National Health Expenditures

among private hospitals…

71% are non-profit

national hospital care expenditures

1/3 - hospitals

1/5 - physicians & clinics

1/4 - other health

year-over-year growth spending on healthcare (2016-2024)

mostly + growth spending on care since there's only are facing downward in 2020 & 2022

solutions to hospital spending growth reaching 2 digits in 2023-early 2024

hospital operating margins

policy focus on reducing healthcare & hospital spending

KFF analysis of RAND Hospital data examines

margins ((revenues – expenses)/revenues)

operating margins vs. total margins: focus on patient care/operating activities

non-federal general short-term hospitals

short-term hospital operating margin KFF graph

drops in 2020 & 2022

hospital operating margins in 2023

operating margins

for-profit hospitals w/ high commercial discharge shares, & system-affiliated hospitals operating margins were higher than avg.

hospitals w/ low market shares operating margins were lower than avg.

rural hospital operating margins were lower than avg.

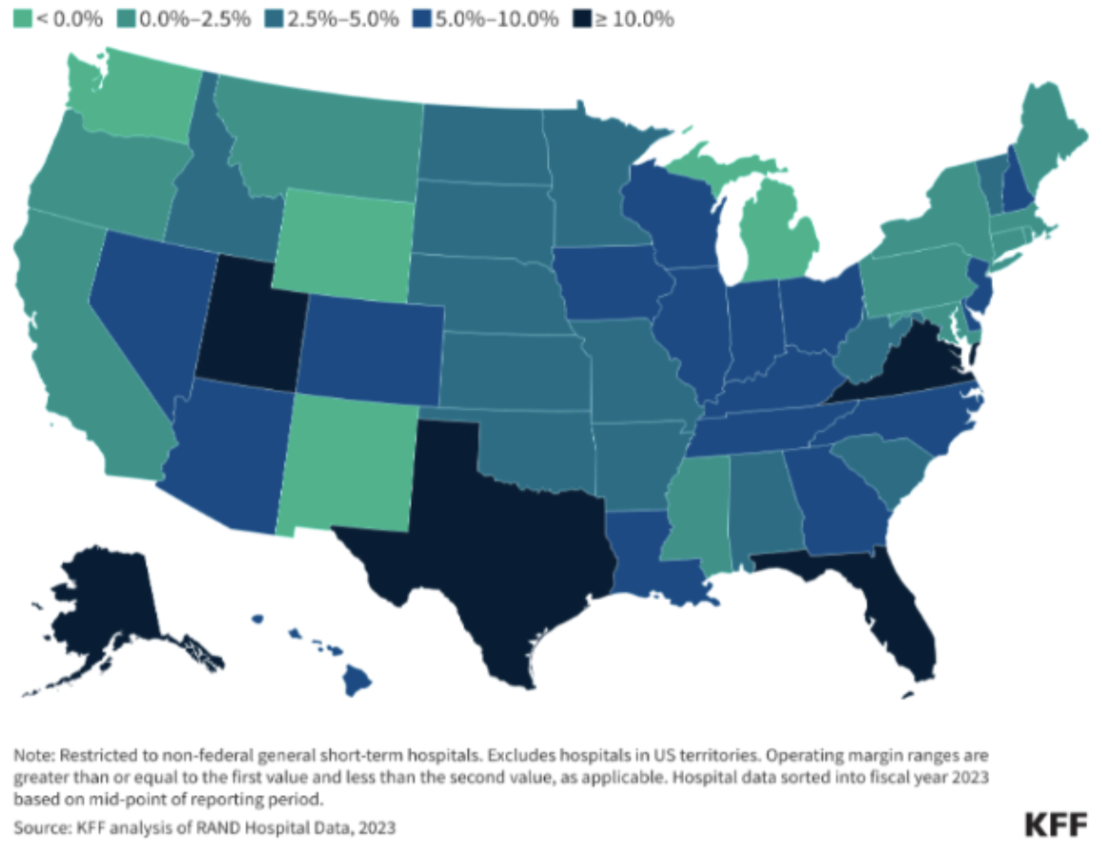

operating margins varied across states, 2023 map

hospital utilization 2000-2023 KFF

hospital inpatient utilization has decreased

hospital outpatient utilization has increased

hospital market is highly concentrated & increasingly consolidated

concentrated —> there are few large hospitals

trends in US have been toward higher market concentration as hospital & physician org mergers become more common

by 2016, 90% of all metropolitan areas had highly concentrated hospital markets

“As Hospitals Grow, So Does Your Bill,” Wall Street Journal, June 6, 2024

consolidation across the hospital has contributed to the higher cost of healthcare

“Corporate Giants Buy Up Primary Care Practices at Rapid Pace”, NYT, 2023

large health insurers & other companies are interested in doctors’ groups that care for patients in private medicare plans

1 or 2 health systems controlled the entire market for inpatient hospital care in nearly half of metropolitan areas in 2022

1 healthcare system controls a given share for more than 25% of the market

health system in the west vs east

dense 1-3 health system is more common in the east

sparse 3-4+ health system is more common in west & middle

share of hospitals & physicians affiliated w/ health systems

increasing share of hospitals are affiliated w/ health systems

share of hospitals affiliated w/ health systems increased from 56% in 2010 to 67% in 2022, w/ the share growing in both rural & nonrural areas

increasing share of physicians are affiliated w/ hospitals or health systems

traditional care

illness

acute care

inpatient

individual health

fragmented care

independent institution

service duplication

patient-centered care

wellness

primary care

outpatient

community well-being

managed care

integrated settings

continuum of services

payment models

fee-for-service

capitation (per member, per month fee for each enrollee assigned to provider)

global budget (budget covered by payer)

facility costs vs. professional services (hospitals & doctors are paid separately, typically w/o coordination)

attempt to align incentives in the system

higher cost → volume-driven healthcare

changes in healthcare use associated w/ the intro of hospital global budgets in maryland

matched 8 maryland counties w/ hospitals in the program (94,967 beneficiaries)

assuming parallel trends, we estimated a differential change in maryland

associations of maryland global budget revenue w/ spending & outcomes related to surgical care for medicare beneficiaries w/ cancer

medicare beneficiaries undergoing cancer surgery in control states had a statistically significant reduction

hospital payment under medicare

since october 1983, medicare has paid for inpatient care according to the hospital inpatient prospective payment system (PPS)

hospital receives a fixed payment based on the patient’s Diagnosis-Related groups (DRG), regardless of the cost of treatment

incentives limit to length of stay & resource utilization

created volume-driven healthcare

hospital reimbursement outside of medicare

varies by insurer & negotiating entities

DRGs are often used, but the medicare fee schedule may not be used

per diem is used especially in commercial contracts. medicaid programs have tried to shift from per diem to DRG

bundling has become increasingly popular

reimbursement for Outpatient Care

Professional Fees

How are they determined?

Fee-for-Service Fee Schedules (like Medicare)

Encounter/Visit Based Fees

Capitation for a set of services

Facility Fees can still apply

In Ambulatory Surgery Centers, for example

Scope of Practice Laws

Determined by state law (dictate what NPs, PAs can do)

2012-2013 veterans affairs data

cohort of medically complex patients w/ diabetes to compare health services use & costs depending on whether the primary care provider was a physician, NP, or PA

case-mix-adjusted total care costs were 6-7 percent lower for NP & PA patients than for physicians' patients, driven by more use of emergency & inpatient services by the latter

NP State Practice Environment, 2023 (AANP)

full —> very northeast & midwest

reduced —> northeast & southeast

restricted —> ca, tx, & southeast

physician Associate State Practice Environment, 2025 (AAPA)

reduced —> southeast

moderate —> ca, tx, east midish

advanced —> “w” us states

optimal —> northwest

nurse practitioner scope of practice & the prevention of foot complications in rural diabetes patients

expanding np practice authority may be effective solution for preventing complications from diabetic foot ulcers in rural communities

what are the trade-offs b/w more stringent & more flexible scope of practice laws?

pros

increase supply of care in underserved areas

shorter wait times

optimize workforce

cons

over-prescribing

fragmentations if mid-level providers don’t coordinate w/ specialists

accountable care orgs (ACO)

provider-led orgs w/ a mission to manage the full continuum of care & be accountable for overall costs & quality of care

physicians & hospitals at shared financial risk w/ the payer for a global budgetary target for a defined patient population

overall, ACOs reduce costs w/o reducing care quality

growth of accountable care orgs (ACO)

positive growth

medicare shared savings program ACO

allows providers to form accountable care entities w/ goal of delivering high quality care while reducing medicare costs

voluntary

different participation options (tracks)

promotes accountability for a patient pop

max 75% risk sharing

realizing equity, access, & community health (REACH) ACO

Advanced ACO model launched by Biden administration in 2023

First to offer a global risk track (100%)

Waiver flexibilities related to SNF admissions, home visits, & telehealth

Includes track dedicated to high-needs Medicare beneficiaries (e.g., one or more chronic conditions that impact mobility, unplanned hospital admissions)

REACH ACO – High Needs ACOs (HNACOs)

When examining performance in 2023, HNACOs performed better than other REACH ACOs, representing the top 5 performers

disparities in telemedicine:

age

limited english proficiency

rurality

income

telehealth

increased since covid & simultaneously decreased ED visits

In 2024, 71.4% of physicians reported using telehealth in their practices weekly,

79% who reported doing so in 2020

25.1% who reported doing so in 2018

Among psychiatrists, 85.9% reported having used telehealth in the previous week