Chapter 2

1/12

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

13 Terms

What is a CPA firm and what do they do?

Legal rights to perform audits

Perform attestation/assurance services

Non-assurance services

What is a public accounting firm?

A business owned by certified accountants that provides services like auditing, tax preparation, and consulting to individuals, private businesses, and non-profits.

a proprietorship, partnership, incorporated association, corporation, limited liability company, limited liability partnership, or other legal entity that is engaged in the practice of public accounting or preparing or issuing audit reports; and (B) to the extent so designated by the rules of the Board, any associated person of any entity described in subparagraph

What is a registered public accounting firm?

A public accounting firm that has officially registered with the PCAOB (Public Company Accounting Oversight Board).

What are 3 factors that influence the organizational structure of CPA firms?

Need for independence

Importance of competence

Increased litigation risk

What is the SEC and who does it help?

Assist with providing investors with reliable information upon which to make investment decisions

Protects investors

Some SEC common forms (S-1,8-K,10-Q,10K)

S-1 - This is the initial registration form required for US companies planning an IPO (Initial Public Offering).

8-K - The unscheduled "material event" form. Companies must file this generally within 4 business days of an event that shareholders should know about immediately.

10-Q - Filed three times a year at the end of each of the first three fiscal quarters. Contains unaudited financial statements and a brief update on operations

10-K - A comprehensive annual filing that gives a complete snapshot of the company's financial health over the past year.

What is the Sarbanes-Oxley Act (SOX)

Came from Enron, WorldCom, etc. 2012

What is the PCAOB and where did it come from?

The PCAOB is a non-profit corporation established by Congress to oversee the audits of public companies (issuers) and SEC-registered broker-dealers. Its primary mission is to protect investors by ensuring audit reports are informative, accurate, and independent.

Created by section 101 of SOX

Overseen by SEC

SOX administrative provisions: Duties of the board

register public accounting firms that prepare audit reports (102);

establish auditing, quality control, ethics, independence, and other standards relating to the preparation of audit reports (103);

conduct inspections of registered public accounting firms (104);

conduct investigations and disciplinary proceedings (105);

improve the quality of audit services in order to protect investors, or to further the public interest;

enforce compliance with this Act, the rules of the Board, professional standards, and the securities laws relating to the preparation and issuance of audit reports

set the budget and manage the operations of the Board.

What is the role of the SEC in accounting and auditing?

By federal law, the SEC has the absolute legal authority to establish accounting and financial reporting standards for public companies.

Under Section 101 of the Sarbanes-Oxley Act (SOX), the SEC was tasked with overseeing the PCAOB.

The SEC ensures compliance through its Division of Corporation Finance and its Division of Enforcement.

What is the AICPA?

(American Institute of Certified Public Accountants) is the national professional organization for Certified Public Accountants (CPAs) in the United States.

it has no regulatory power over public companies, but it remains the dominant force governing private company accounting and the CPA profession as a whole.

Set professional requirements

Conduct Research

publish materials related services performed

Empowered to set standards (private companies and non-public audits)

auditing standards

complication and review standard

other attestation standards

Code of professional conduct

CPA Exam

U.S. and International auditing standards

IAASB - applicable to entities outside of the US

ASB (aicpa) - applicable to private entities in US

PCAOB - applicable to US public companies

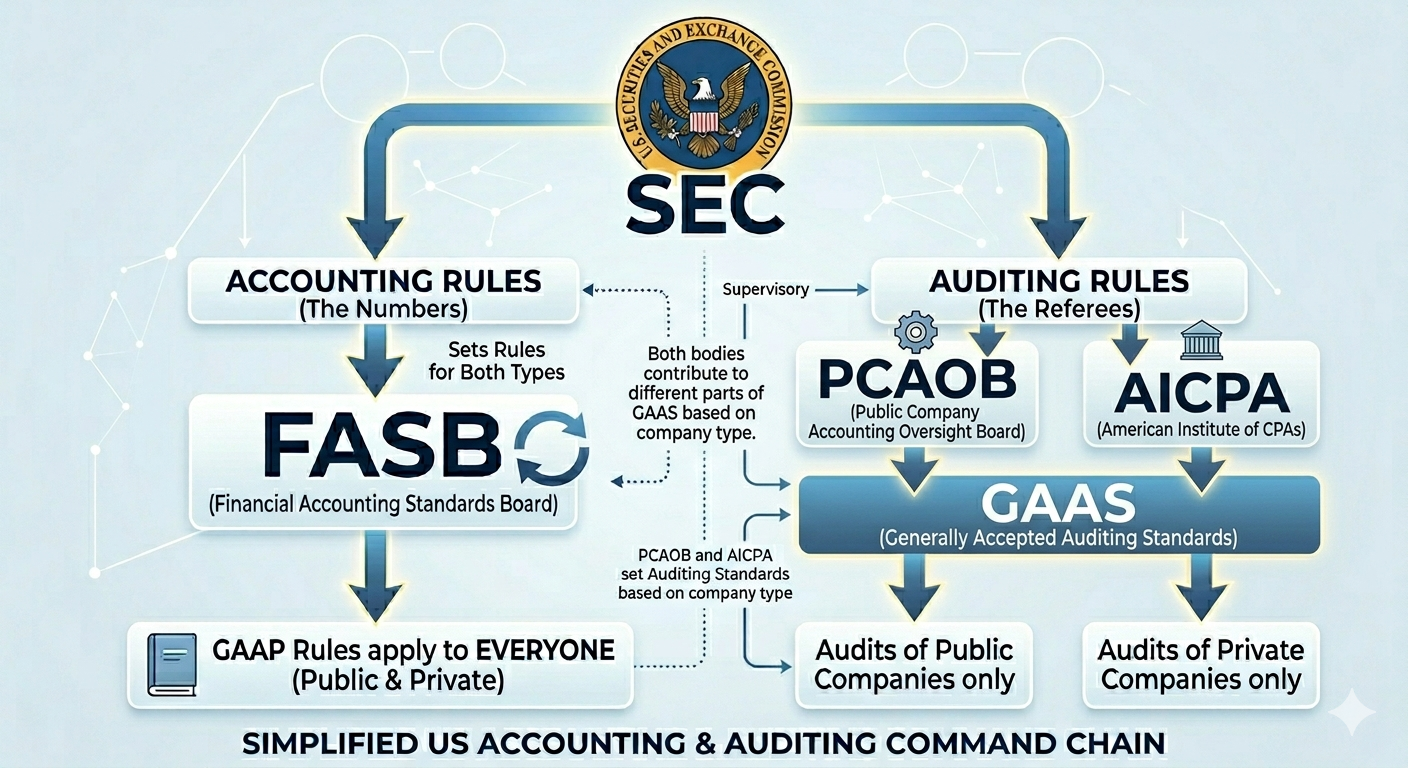

Image explaining all the acronyms

FASB - independent non-profit organization recognized by SEC to create GAAP rules (every us company must follow)

PCAOB - created by government in 2002 (SOX), directly overseen by SEC, they set GAAS for public companies

AICPA - private professional association, SEC has no control, they set GAAS for private companies