Acc 212 Exam 1

1/40

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

41 Terms

Managerial Accounting

Focuses on internal accounting processes and generates reports that are referenced by management

Provides financial and nonfinancial information to an organization’s managers

Current performance

Financial Accounting

Involves collecting data to create financial statements for both internal and external use

Past performance

Planning

Process of setting goals and making plans to achieve them

Build a new factory?

Develop new products?

Expand into new markets?

Control

Process of monitoring and evaluating an organizations activities

Are costs too high?

Are services profitable?

Are customers satisfied?

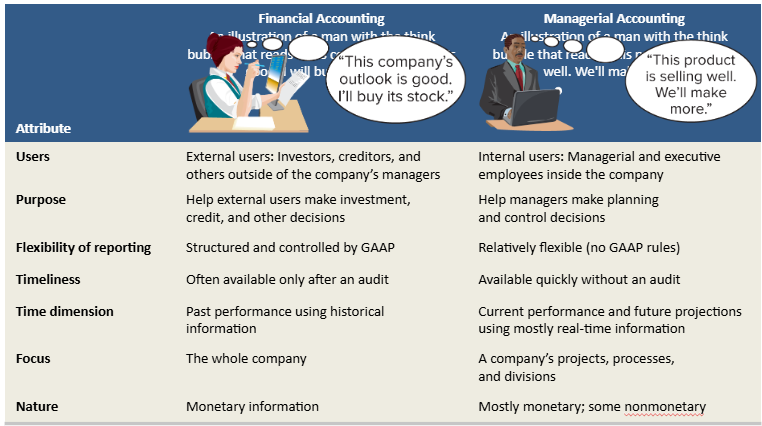

Financial Accounting comparison

Users: External users (investors, creditors, others outside of the company’s managers)

Prupose: Help external users make investment, credit, and other decisions

Flexibility of reporting: structured and cotnrolled by GAAP

Timeliness: Often available only after an audit

Time dimension: Past performance using historical information

Focus: The whole company

Nature: Monetary information

Managerial Accounting comparison

Users: Internal users (managerial and executive employees inside the company)

Purpose: Help managers make planning and control decisions

Flexibility of reporting: Relatively flexible (no GAAP rules)

Timeliness: Available quickly without an audit

Time dimension: Current performance and future projections using mostly real-time information

Focus: A company’s projects, processes, and divisions

Nature: Mostly monetary; some nonmonetary

Fraud

Affects all business and it is costly

The Association of Certified Fraud Examiners (ACFE) estimates the average US business to lose 5% of its annual revenues to fraud.

An internal control system is procedures managers use to:

Ensure reliable accounting

Protect assets

Uphold company policies

Promote efficient operations

The institute of managemetn accountants requires that managemetn accountants be

Competent, maintain confidentiality, act with integrity, and communicate information in a fair and credible manner

Managerial accounting is used in many careers

Marketing staff need sales and cost data to decide whcih products to promote

Managemetn needs sales force details to evaluate perfomrance

Entrepreneurs use costs, budgets, and financial statements

Decision makers in both for-profit and non-profit organizations use accounting data to make informed decisions and secure financing from donors

Direct costs

Cost-effectively traceable to a cost object

Indirect costs

Cannot be cost-effectively traced to a cost object

Direct materials

Costs for direct materials that can be cost-effecitvley traced through the manufacturing process to finished goods.

Ex. Tires, seats, frame, pedals, brakes, and cables

Direct labor

Wages and salaries for direct labor that are cost-effectively traced through manufacturing process to finished goods

Ex. Wages paid to bike assembly worker

Factory overhead

All manufacturing costs that are not direct materials or direct labor and cannot be cost-effectively traced to finished goods

Ex. Indirect labor (maintenance workers), indirect mateiral (screws, nuts, staples), indirect other costs (factory utility costs)

Manufacturing costs

Prime cost

Conversion cost

Prime cost

Direct material

Direct labor

Conversion cost

Direct labor

Factory overhead

Product costs

Direct labor

Direct material

Factory overhead

Production costs necessary to create a product

Period costs

Nonproduction costs linked to a time period (not products)

Selling expenses: costs to obtain orders and to deliver finished goods to customers

General and administrative expenses: costs of staff support and administrative functions

Nature of Managerial Accounting

Fraud triangle

Opportunity

Rationalization

Pressure

Artificial Intelligence

Artificial Intelligence (AI) uses software and can be used to complete repetitive tasks such as entering invoices and transaction data.

Managerial accountants are vital to evaluating AI generated reports and in making key business decisions.

Data analytics

Data analytics is a process of analyzing data to identify meaningful relations and trends.

There are four basic types of analytics:

Descriptive – summarizes and describes events from the past.

Diagnostic – reveals causes of events from the past.

Predictive – predicts likely events for the future.

Prescriptive – creates action plans to achieve a desired future.

Data visualization

Data visualization is a graphical presentation of data to help people understand their significance and make informed business decisions.

A popular tool to create data visualizations is a Tableau dashboard.

A dashboard is a data visualization that includes charts, graphs, and other imaging to help users see important trends and relations.

Cost concepts for service companies

The cost concepts described are generally applicable to service organizations.

Service companies can classify costs as direct materials, direct labor, overhead, selling, or general and administrative costs.

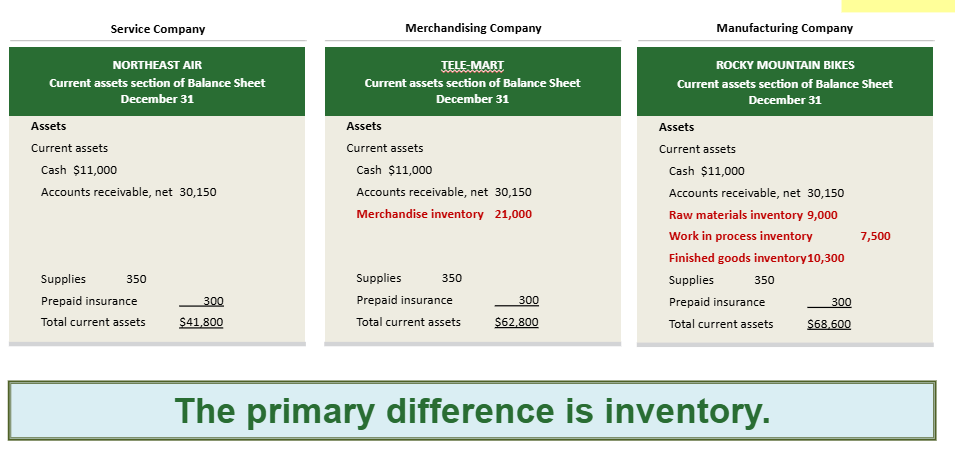

Reporting inventory on the balance sheet

Raw materials inventory: materials waiting to be processed

Work in process inventory: partially complete products, some materials, labor and/or overhread have been added

Finished goods inventory: completed products ready for sale

Balance sheets for manufacturers, merchandisers, and servicers

The primary difference is inventory

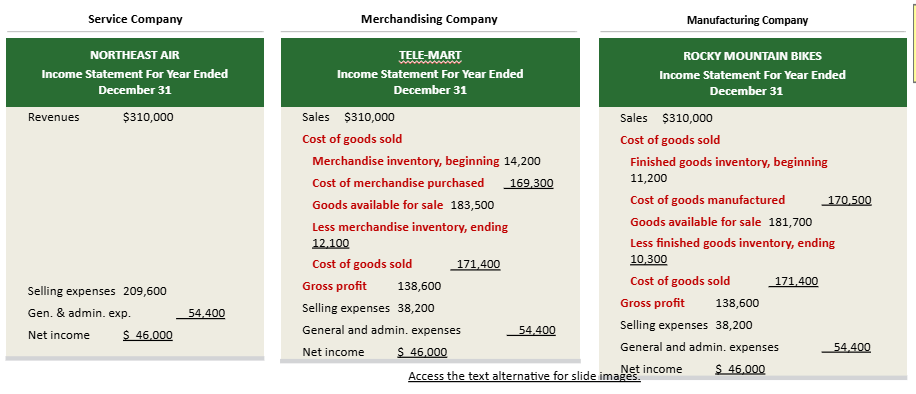

Merchandiser COGS equation

Beginning merchandise inventory + cost of merchandise purchased - ending merchandise inventory = COGS

Manufacturer COGS equation

Beginning finished goods inventory + cost of goods manufactured - ending finished goods inventory = COGS

Reporting costs and the income statement

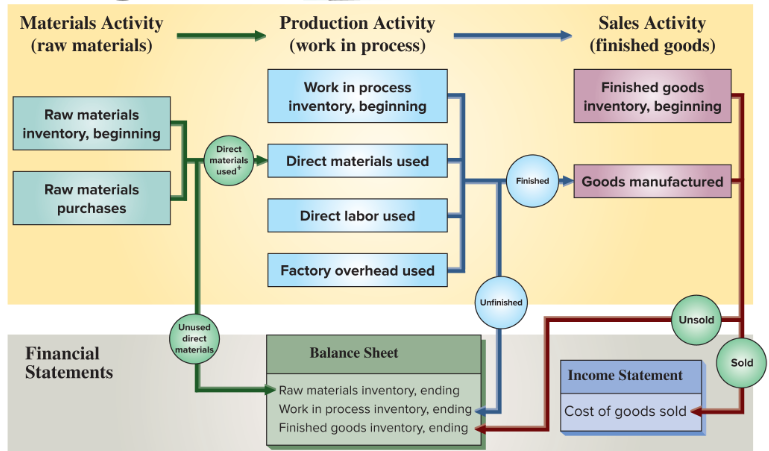

Flow of manufacturing activities

Materials activity (raw materials)

Production activity (work in process)

Sales activity (finished goods)

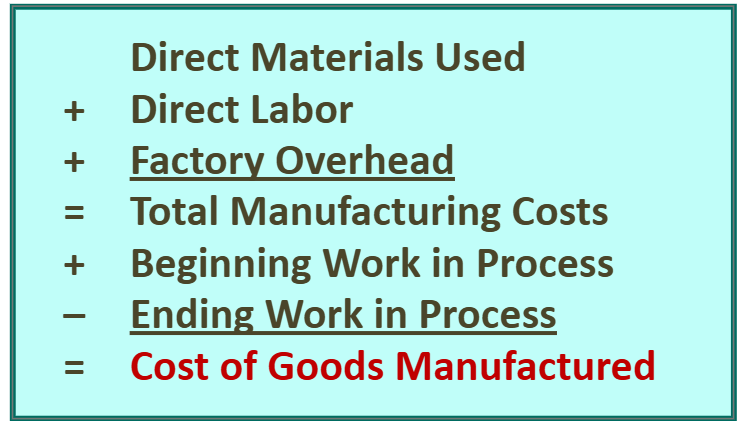

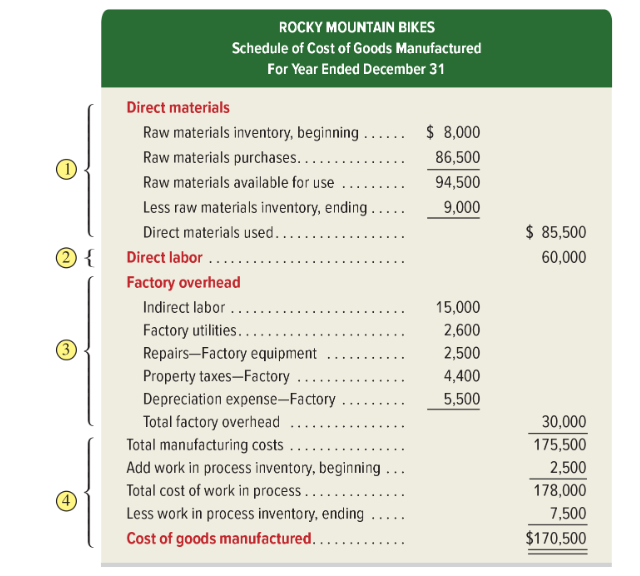

Schedule of cost of good manfactured

Summarizes the types and amounts of costs incurred in a company’s manufacturing process.

Manufacturing statement

Trends in managerial accounting

Digital manufacturing

Customer orientation

E-commerce

Lean practices

Global economy

Service economy

Value chain

Lean principles

The goal of a lean business model is to eliminate waste while “satisfying the customer” and “providing a positive return” to the company.

Continuous improvement rejects the notion of “good enough” and challenges employees and managers to continuously improve operations.

Total quality management

Quality improvement applied to its business activities

Seek and uncover waste

Constant focus on higher standards

Just-in-time (JIT) manufacturing

Receive customer orders → schedule production → receive materials just-in-time for production → complete parts just-in-time for assembly into products → complete products just-in-time to ship to customers

Value chain

Refers to the series of principles that add value to a company’s products or services. Companies can use lean principles to increase efficiency and profits.

Triple bottom line

Focuses on three measures:

Financial “profits”

Social “people”

Environmental “planet”

ESG insight: reporting and analysis

Environmental, social, and governance (ESG)

Framework that depicts how companies behave as responsible stewards of the environment, principled members of society, and accountable leaders.

Includes sustainable practices and socially responsible activities.

Sample metrics are shown in the graphic below.

Environmental

Social

Governance