ECO2023 - Microeconomics UF Midterm 1

1/120

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

121 Terms

Every point inside or on the PPF is

attainable (possible)

Any point that is on the PFF is

efficient (product efficient)

Any point outside of the PPF is called

unattainable (with the resources given to us)

One best point on the PPF is not only production efficient but is

allocatively efficient

What causes us to be inside of the PPF versus on the PPF?

misallocation of resource (example: unemployment)

opportunity cost

The next best alternative foregone; Loss/Gain

with a straight line PPF, OC are

constant along the entire PPF

with a bowed-out PPF, the OC are

always increasing in both directions; law of increasing opportunity costs

it is possible but unlikely that a nation's PPF could be ___________; this will be evident if the OC's are ___________ as we move along the PPF

bowed inward; decreasing

change in the factors of production cause a

shift in the PPF - due to: land, capital, labor, and entrepreneurial effort/entrepreneurship

a change in technology; if the technology for the production of ONE good changes, this will cause a

rotation in the PPF

a change in technology; if the technology for the production of BOTH goods changes, this can cause a

shift in the PPF

parallel shift of the PPF

won't change OC

rotation of the PPF

would change OC

quantity demanded

at a given price, how much stuff people are willing to buy

law of demand

the idea that as the price of something goes up, the quantity you demand goes down

income effect (demand)

spending what is in my pocket

substitution effect

queso or guac

demand

marginal social benefit

when there is a change in the price of a good, it is referred to as a change in the ____________ ________________

quantity demanded; this does NOT shift the demand curve, just move along the curve

shifts in demand: normal good

everyday life; as your income increases, demand ↑ (right)

shifts in demand: inferior good

things you buy if you have limited income; as income increases, D ↓

shifts in demand: anything that make a product less desirable

D↓(preferences)

shifts in demand: anything that makes a product more desirable

D ↑

shifts in demand: two goods that are consumed together (ex: hot dogs and hot dog buns)

complements; when the price of one goes up the demand for the other goes D↓

shifts in demand; two goods that are consumed instead of the other (ex. pepsi and coke)

substitutes; when the price of one goes up the demand for the other D↑

shifts in demand; when the population of consumers increases

D ↑

shifts in demand; when the population of consumer decreases

D↓

shifts in demand; when you expect a price in the future your demand changes TODAY! w/ an increase

expected future price; your demand today ↑

shifts in demand; when you expect a price in the future your demand changes TODAY! w/ a decrease

expected future price; your demand today ↓

shifts in demand; expected future income - more money in the future

D↑ TODAY

shifts in demand; expected future income - less money in the future

D↓ TODAY

shifts in demand; sanctions imposed on buys of a good

if it is illegal to buy a good, the demand ↓

quantity supplied

at a given price, how much stuff firms are willing to sell; as price increases, firms sell more stuff

law of supply

the idea that as price of something goes up, the quantity supplied goes up; example: low-hanging fruit

supply

marginal social cost

when there is a change in the price of a good, it is referred to as a change in the _________ __________ of that good

quantity supplied; this does NOT change the supply curve, just move along the curve

shifts in supply; as input prices increase

firms S ↓ - cost of inputs (things used to produce a good)

shifts in supply; as input prices decrease

firms S ↑ - cost of inputs (things used to produce a good)

shifts in supply; if there is a technological advancement (easier to make a good) in the production of a good, firms will product

more of that good; S ↑

shifts in supply; price of production substitute (example: using wood to make paper or furniture)

S ↓

shifts in supply; price of production complement (example: making steaks and leather)

S ↓ (by-products)

shifts in supply; if a firm expects the price to increase in the future,

S ↑ (expected future prices)

shifts in supply; if a firm expects the price to decrease in the future,

S ↓ (expected future prices)

shifts in supply; when the # of firms (sellers) increases

S ↑

shifts in supply; when the # of firms (sellers) decreases

S ↓

shifts in supply; natural disaster

state of nature - S ↓

shifts in supply; sanctions (penalties) imposed on sellers of a good

if it is illegal to sell a good, the supply ↓

A market is in equilibrium when

it is producing the efficient quantity

Quantity demanded > quantity supplied

surplus

Quantity demanded < quantity supplied

shortage

with a surplus present, if the market is left unregulated, the price will ________ until EQ is reached

drop

with a shortage present, if the market is left unregulated, the price will ________ until EQ is reached

rise

if demand increases

P ↑ Q↑

if supply increases

P ↓ Q ↑

if demand decreases

P ↓ Q ↓

if supply decreases

P ↑ Q ↓

key words for demand

consumers/consumption, buyers, and demanders

key words for supply

producers/production, sellers, and suppliers

law of demand states when the price of a good increases

the quantity demanded of that good will decrease

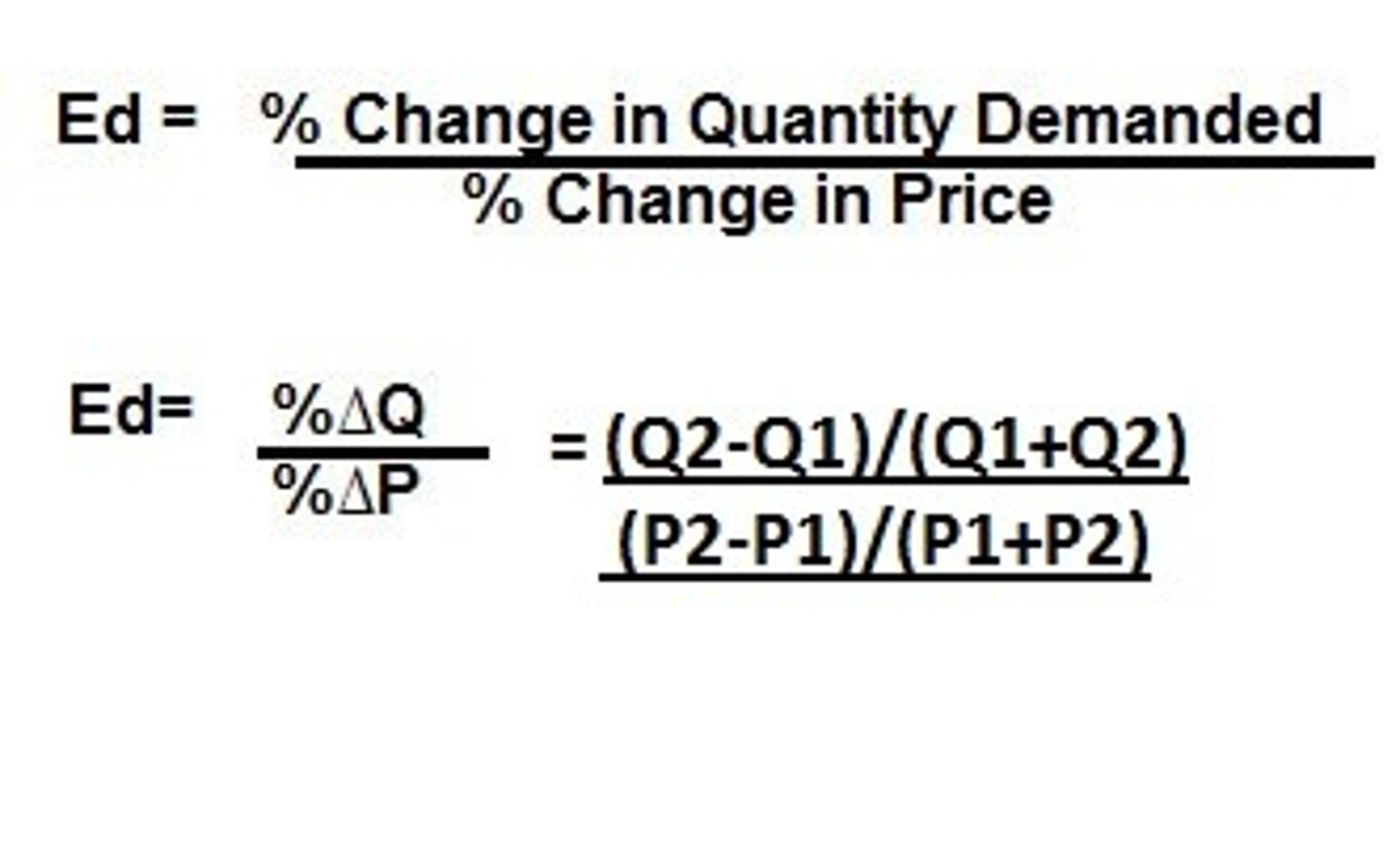

elasticity

the percent change in quantity divided by percent change in price

Elasticity synonym

responsiveness

price elasticity of demand formula

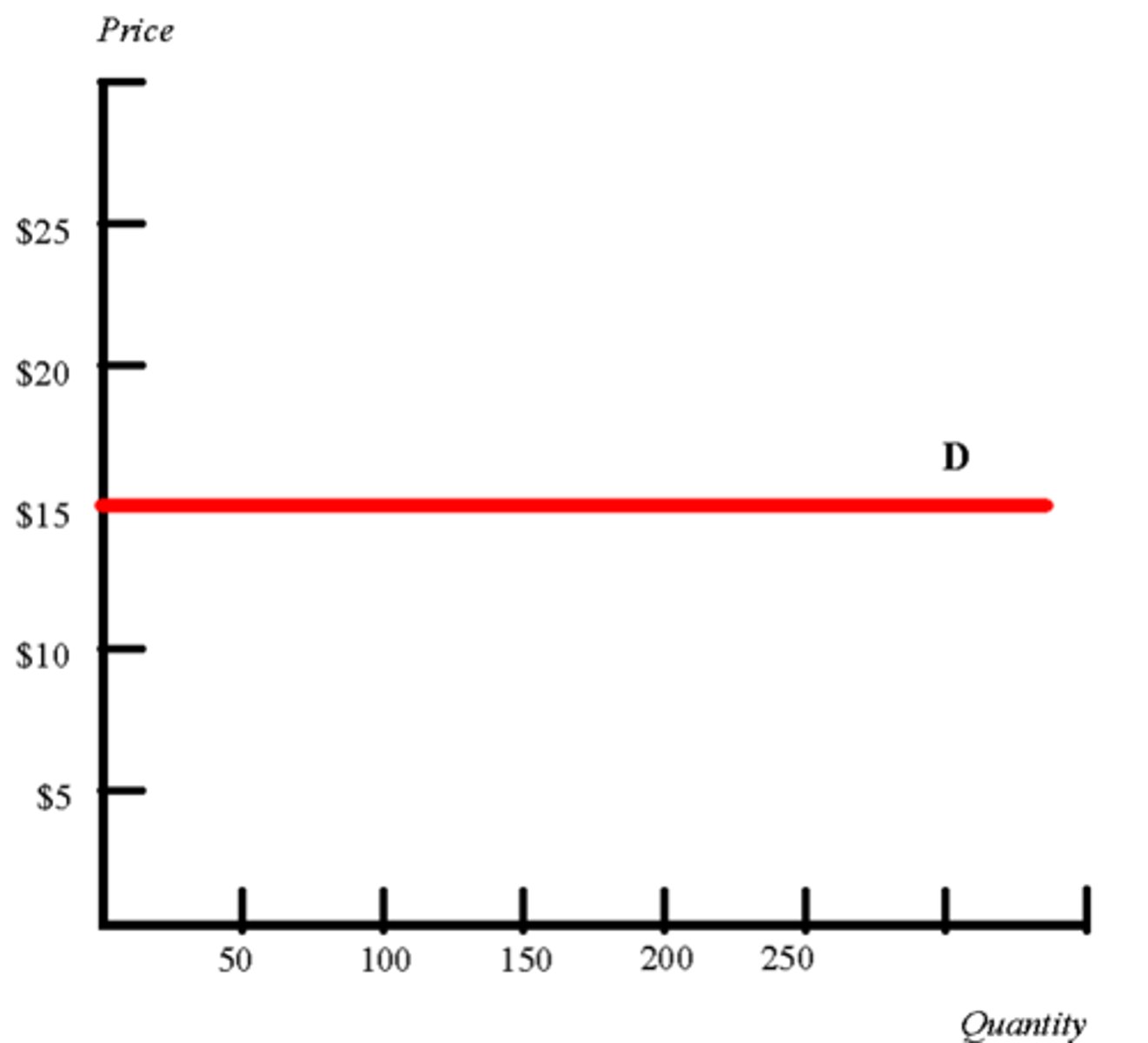

perfectly elastic

E = infinity

inelastic

E < 1

elastic

E > 1

unit elastic

E = 1

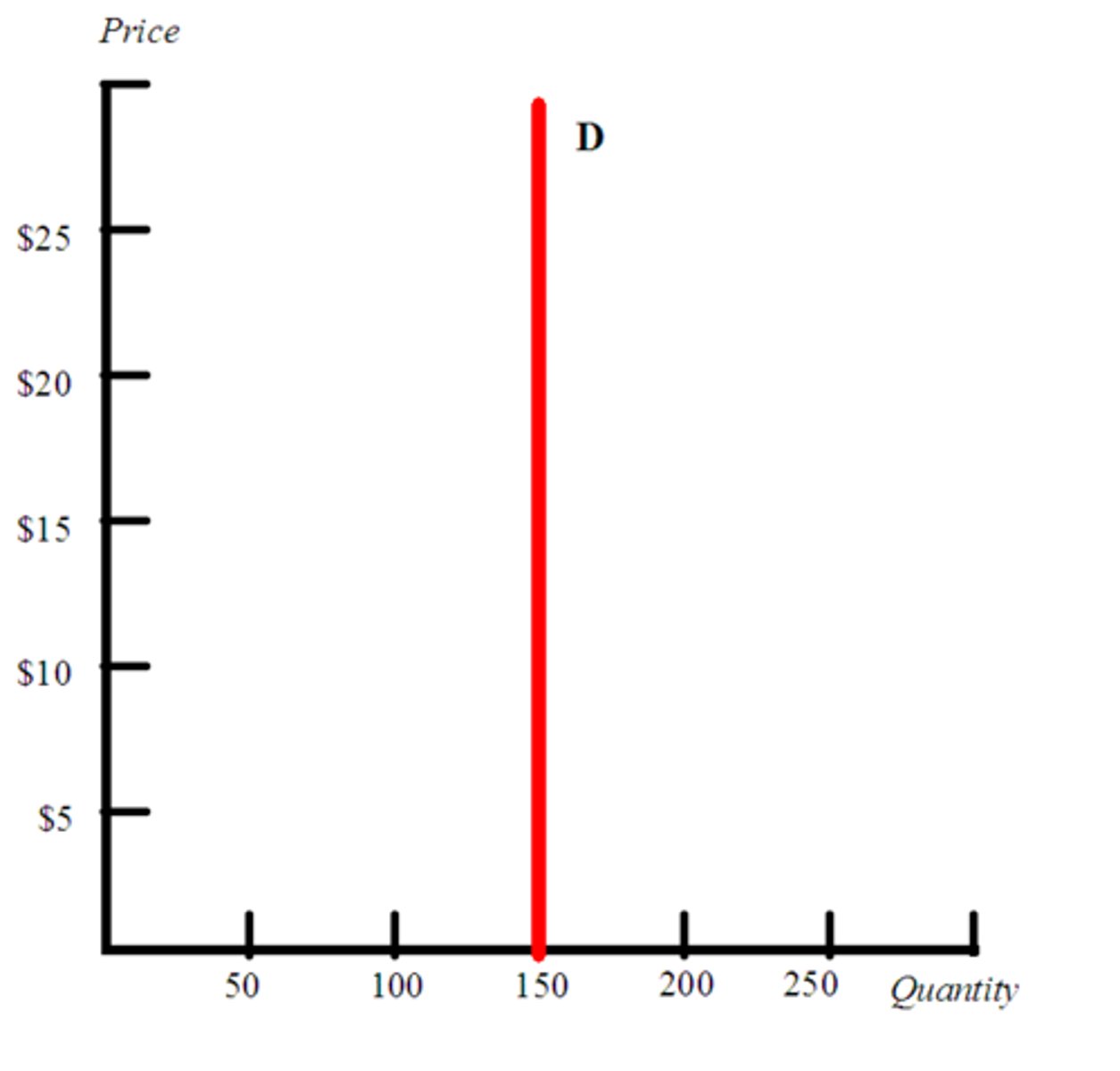

perfectly inelastic

E = 1

more elastic

flatter curve

portion of income spent on a good - higher proportion

more elastic - price decreases

Number of substitutes - more substitutes

more elastic

Luxury vs. Necessity

luxury good = more elastic

time passed since price change

more time passed = more elastic

total revenue

TR = P x Q

if demand is inelastic

revenue follows price

if demand is elastic

revenue goes against price

if demand is ELASTIC and a firm RAISES its prices, total revenue

↓

if demand is ELASTIC and a firm LOWERS its prices, total revenue

↑

if demand is UNIT ELASTIC and a firm RAISES its prices, total revenue

=

if demand is UNIT ELASTIC and a firm LOWERS its prices, total revenue

=

if demand is INELASTIC and a firm RAISES its prices, total revenue

↑

if demand is INELASTIC and a firm LOWERS its prices, total revenue

↓

income elasticity of demand - +

we have a normal good

income elasticity of demand - -

inferior good

cross price elasticity of demand - +

substitutes

cross-price elasticity of demand - -

compliments

marginal

one more unit

MB > MC

Q ↑ (deal)

MB < MC

Q ↓ (no deal)

consumer surplus

willingness to pay - price (demand - P*)

producer surplus

price - willingness to pay

total surplus

total surplus = consumer surplus + producer surplus

efficiency happens when we

maximize total surplus (producing at capacity)

if demand is more elastic than supply

flatter = more elastic; CS < PS

if supply is most elastic than demand

PS < CS

the more elastic curve will have _____ of the total surplus

less

when a competitive market is at equilibrium

MB = MC

Adam Smith, Wealth of Nations, 1776

each person in a competitive market, acting only in their own self-interest, is led to promote the efficient use of society's resources

invisible hand

a competitive market will reach the efficient point of production (the point that best uses society's resource) on its own accord, as if the market were being guided to the point by

if a market is not producing the efficient quantity then the market will have

deadweight loss