Mod. 8 Capital Structure

1/15

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

16 Terms

Main Question

Does the choice of capital structure affect firm value???

capital structure

The relative proportions of debt, equity, and other securities that a firm has outstanding

the mix of debt and equity

unlevered equity

Equity in a firm with no debt

levered equity

Equity in a firm that also has debt outstanding

Perfect Capital Market (conditions)

•There are no taxes

•There are no transaction costs and no brokerage costs.

•The capital markets are competitive.

Conclusion

Modigliani-Miller I condition

question: does debt affect a firms value in a perfect capital market?

Answer: No, firm value is independent of capital structure in the perfect capital markets.

Modigliani- Miller I

leverage and firm value in a perfect capital market

MMI proposition

•In a perfect capital market, the total value of a firm is equal to the market value of the total cash flows generated by its assets and is not affected by its choice of capital structure.

•In the absence of taxes or other transaction costs, the total cash flow paid out to all of a firm’s security holders is equal to the total cash flow generated by the firm’s assets.

•Therefore, by the Law of One Price, the firm’s securities and its assets must have the same total market value.

Two identical firms except one has debt (with taxes)

Modigliani-Miller II conditions

based on firm having debt and additionally taxes

conclusion

question: does having taxes have a negative or positive impact on company value?

Answer: positive, due to tax shield, lowers taxable income, allowing more to go to investors (in form of dividends)

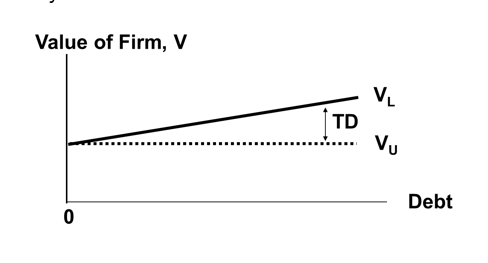

•MM show that the total CF to Firm L’s investors is equal to the total CF to Firm U’s investor plus an additional amount due to interest deductibility:

•CFL = CFU + rdDT.

•What is value of these cash flows?

•Value of CFU = VU

•MM show that the value of rdDT = TD

•Therefore, VL = VU + TD.

•If T = 40%, then every dollar of debt adds 40 cents of extra value to firm.

Modigliani-Miller II

leverage and firm value with corporate taxes

•Corporate tax laws allow interest to be deducted, which reduces taxes paid by levered firms.

•Therefore, more CF goes to investors and less to taxes when leverage is used.

•In other words, the debt “shields” some of the firm’s CF from taxes.

•CFU = $1,800 , CFL = $2,280,

•Tax shield on interest payment = 0.4*$1,200

•CFL ("$2,280")= CFU ($1,800 ) + rdDT (0.4*$1,200)

firm value and debt when corporate taxes are considered

under MM with corporate taxes, firm value increases continuously as more and more debt is used

tax shield

a reduction in taxable income achieved through allowable deductions, exemptions, or credits. By lowering your taxable income, it effectively "shields" a portion of your earnings from taxation, resulting in lower overall tax liabilities for individuals and businesses

debt lowers the total taxable income amount, meaning the firm pays less in taxes, increasing its cash flows

more cash flows goes to investors and less to tax

= tax rate * interest payment * debt

based on the tax and debt amount

with debt = lowers net income, but also lowers taxes

interest payments are not taxable

levered firms have larger firm value under this condition

exam Q for MMI

when does debt not/ cannot affect the firm value?

answer: in perfect capital markets

means no taxes, no friction, is competitive

generates similar cash flows even with different levels of debt use

idea that IN a IMPERFECT capital market, debt DOES affect firm value

next Q is if this is a good thing or bad thing MMII

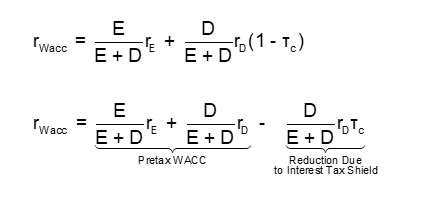

WACC with taxes

•With tax-deductible interest, the effective after-tax borrowing rate is and the weighted average cost of capital becomes

Exam Q for MMII

in environment with taxes and the company has some debt, given the tax rate, debt amount and interest rate, estimate the tax* shield

Answer: Tax debt interest rate (which is T * D *rd)

VL = Vu + TS (TS = TD in symbols, is the additional value)

the additional value created by debt according to MMII shows how the use of debt in taxed markets IS positive

next Q. what is the optimal level of debt (trade-off theory)

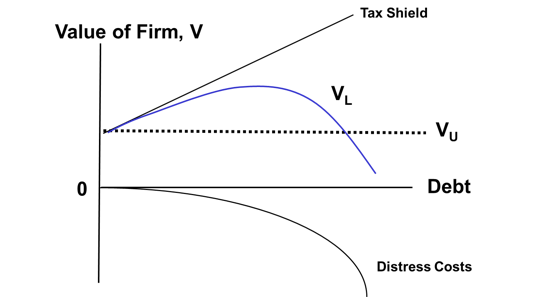

trade off theory

•MM theory ignores bankruptcy (financial distress) costs, which increase as more leverage is used.

•At low leverage levels, tax benefits outweigh bankruptcy costs.

•At high levels, bankruptcy costs outweigh tax benefits.

•An optimal capital structure exists that balances these costs and benefits.

can we maximize firm value with debt?

MMII is based on unrealistic expectations that the firm will be able to generate enough earnings to pay off the debt aka never go bankrupt (this is not realistic)

tax shiel v cost of financial distress

graphically shows how debt is beneficial up to a point

tied to trade off theory

VL = firm value

VU = optimal amount of debt

Hamada’s formula

used for finding the optimal capital structure/ amount of debt a company should use

•MM theory implies that beta changes with leverage.

•bU is the beta of a firm when it has no debt (the unlevered beta)

•bL = bU [1 + (1 - T)(wd/ws)]

beta: affects cost of equity, WACC, total and average risk of company

WACC used in firm valuation of DCF

maximizing firm value = minimizing WACC

this equation connects capital structure to cost of equity through the beta and WACC estimation