IMPORTANT 228 EXAM FORMULAS ETC

1/36

Earn XP

Description and Tags

for last minute cramming and retention

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

37 Terms

variable cost (VC) formula

no. of labour hours * labour costs (considering that labour is the only cost that is varied)

average variable cost (AVC) formula

TVC/Q

fixed costs

any cost that stays the same! its a pretty obvious one. however, don’t forget that the fixed cost will most likely always exist (even when TP = 0)

average fixed cost (AFC)

FC/Q

total cost (TC) formula

FC + VC

average total cost (ATC) formula

TC/Q

what is marginal cost?

The additional cost incurred by producing one more unit of a good or service. It is calculated as the change in total cost / change in quantity produced. you calculate this for every value of Q lol.

what are short run costs?

the costs that a firm incurs when at least one factor of production is fixed. These costs include both fixed costs and variable costs.

what are long run costs?

the costs that a firm incurs when all factors of production are variable. In the long run, a firm can adjust all its inputs to optimize production, allowing for more flexibility in cost management.

how to identify the short run cost in a question

look for the question telling you how many units of capital the firm currently employs! this will be your fixed value. then, look for the cost indicated in the question (i.e. $263). Fixed costs stay constant, and variable costs fluctuate based on production outputs.

how to identify long run total cost in a question

just look at all the possible combos for the required cost for units (i.e. 263 units) and pick the cheapest one

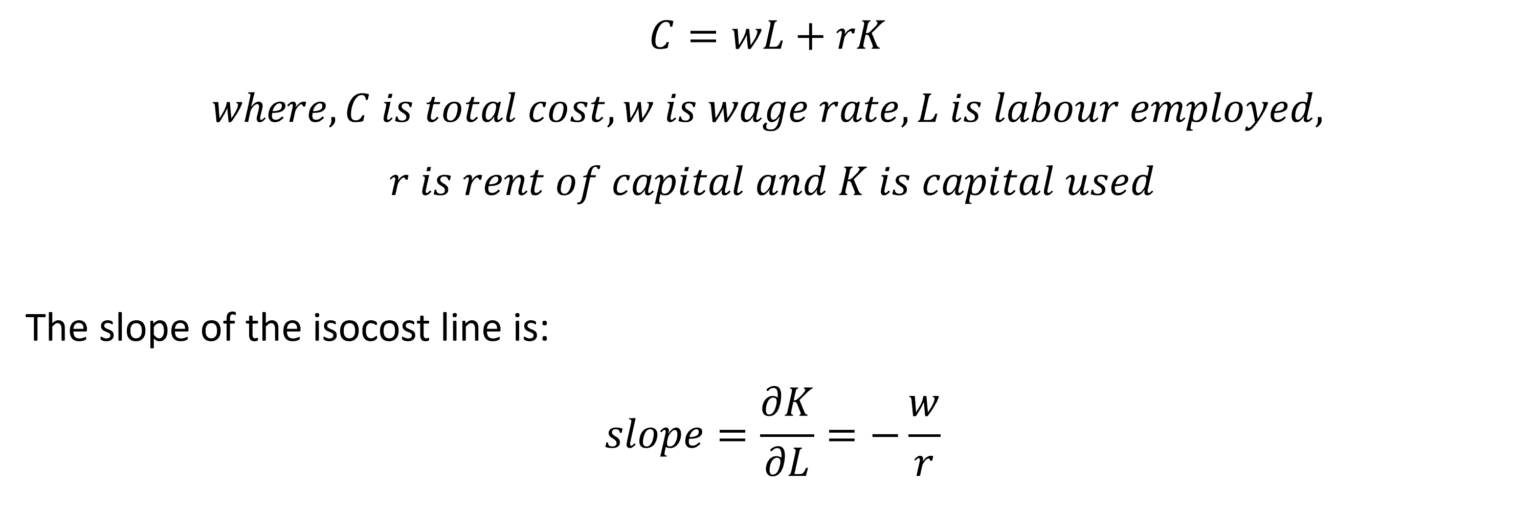

isocost line equation

dominant strategy (game theory)

A strategy that yields the best outcome for a player, regardless of what the other players choose.

On a payoff matrix, it looks like a single row (or column) of numbers that is strictly superior to the alternative rows (or columns) for that player in every single scenario

nash equilibria (game theory)

a state in a game or situation where no player can improve their outcome by changing their strategy alone, as long as everyone else keeps their strategy the same. It is a point where everyone's choice is the best response to everyone else's (basically two circles in the same box)

dominated strategy (game theory)

A strategy that is less effective than another strategy for a player, regardless of what the other players choose, resulting in a worse outcome in all scenarios (no options in row/column being higher than any alternate options in another column)

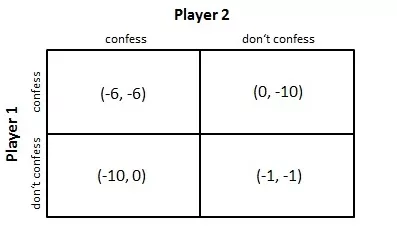

prisoners dilemma (game theory)

A standard example of a game in which two players must choose between cooperation and betrayal, where the optimal outcome for both occurs when they cooperate, but individual incentives lead to mutual betrayal, resulting in a worse outcome for both.

what is the sub-game perfect nash equilibria

a game theory concept used to analyze sequential (step-by-step) games. It requires players' strategies to be a Nash equilibrium in every possible subgame. This eliminates non-credible threats, ensuring players act rationally at every stage of the game

implicit costs

Costs that represent the opportunity cost of utilising resources, such as time and money, in a way that does not involve explicit monetary payment.

explicit costs

Direct, out-of-pocket payments for resources, including wages, rent, and materials.

marginal revenue (MR)

the additional revenue from selling one more unit

when does profit maximisation occur?

where MR = MC

key features of perfect competition (important for paragraphs too!)

many sellers and buyers

standardized (homogeneous) product

full information

equal access to resources

free entry into and exit from the market