Micro ch 12 Perfect Competition

1/31

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

32 Terms

What is perfect competition?

A market where:

Many firms sell identical products

There are no restrictions to enter the industry

Established firms have no advantages over new ones

Sellers and buyers are well informed about prices

What is a price taker

A firm that cannot influence the price of a good/service and must accept the market price as given.

Why is demand perfectly elastic for a perfectly competitive firm?

Because all firms sell identical products (perfect substitutes), so consumers can switch instantly to another seller.

Define Elastic

Responsive to change

Demand elasticity = How much buyers respond to price changes.

Supply elasticity = How much sellers respond to price changes.

What is the goal of firms?

To maximize economic profit

Economic Profit

total revenue - total cost

Opportinity cost of production

everything the firm gives up to produce the product

Why is normal profit included in total cost?

Because normal profit is an opportunity cost—the minimum profit needed to keep the firm in business.

What is normal profit?

The minimum profit needed to keep a firm in business; it is treated as a cost because it is an opportunity cost.

Total Revenue formula

P x Q

Marginal revenue

The change in total revenue that results from a one-unit increase in the quality sold

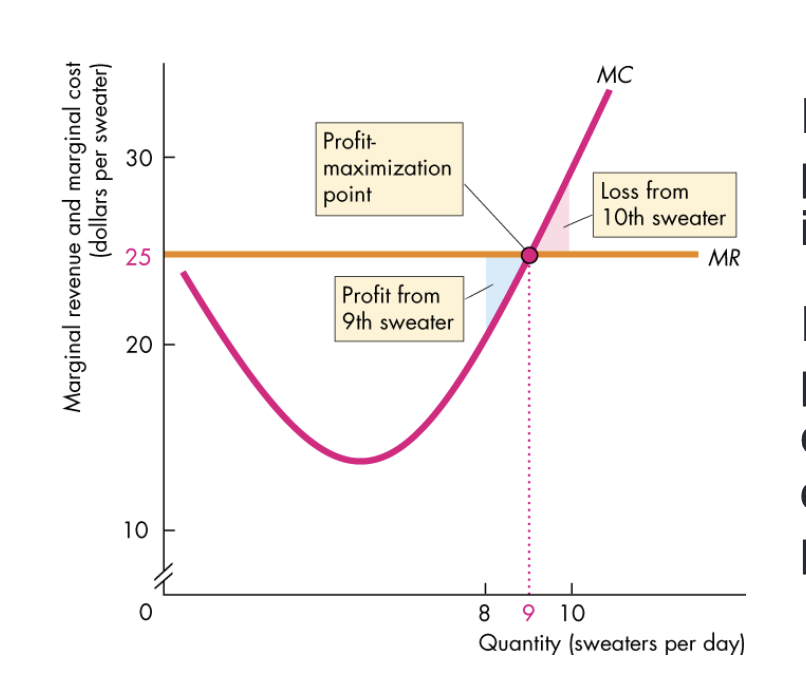

Profit maximization

when marginal revenue equals marginal cost (MR = MC)

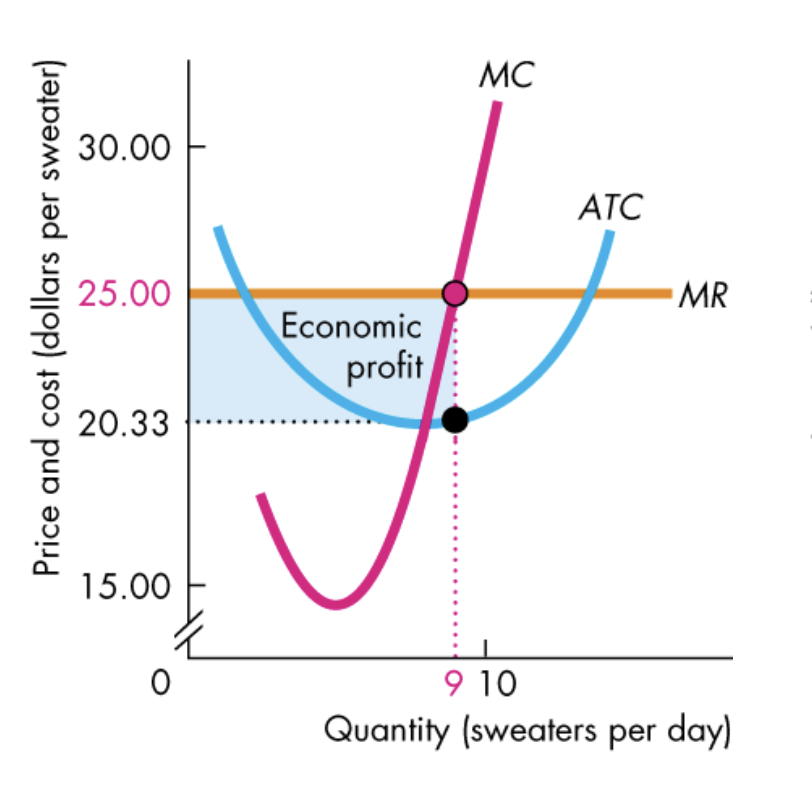

Profit Maximization Graph

In a perfect competition, MR = P, so P is horizontal

X-axis is quantity, Y-axis is MR and MC

MC is U because of diminishing returns

Profit is maximized when MR and MC intersect

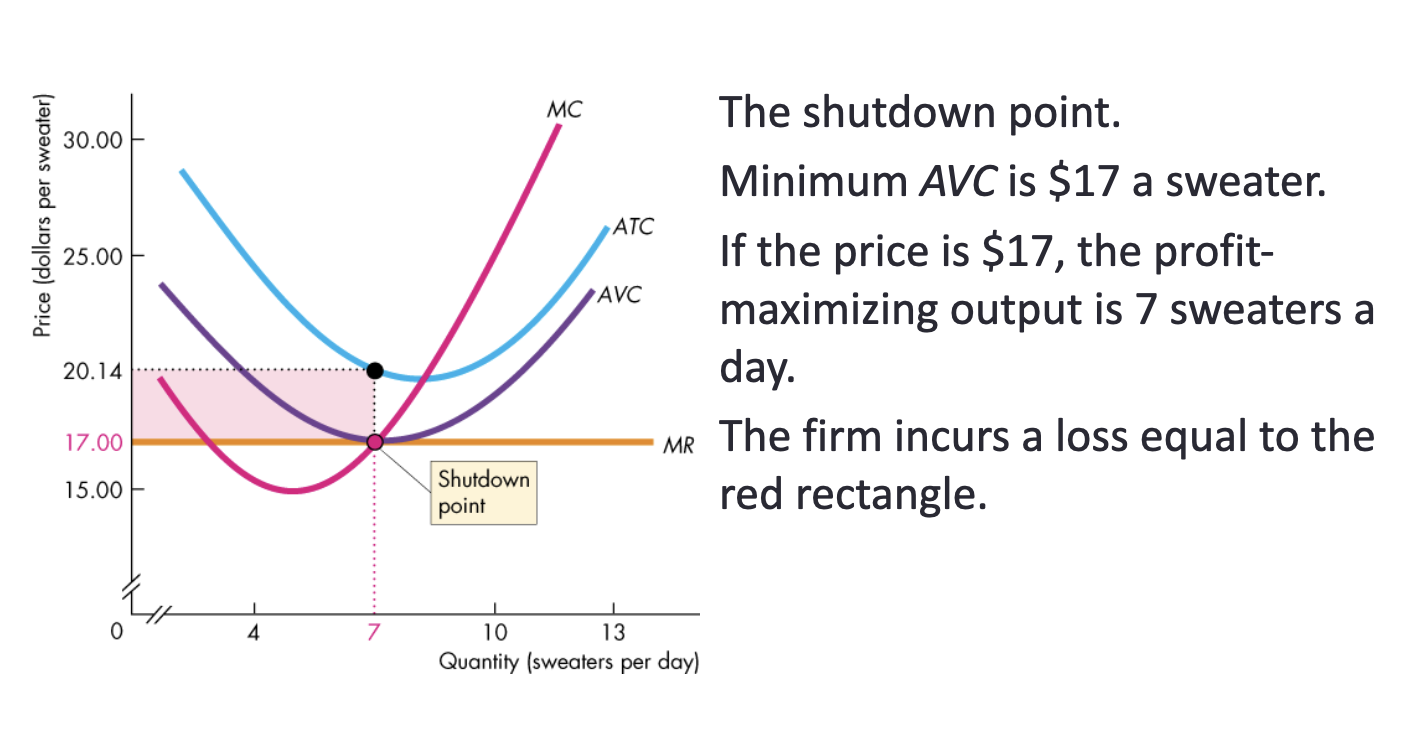

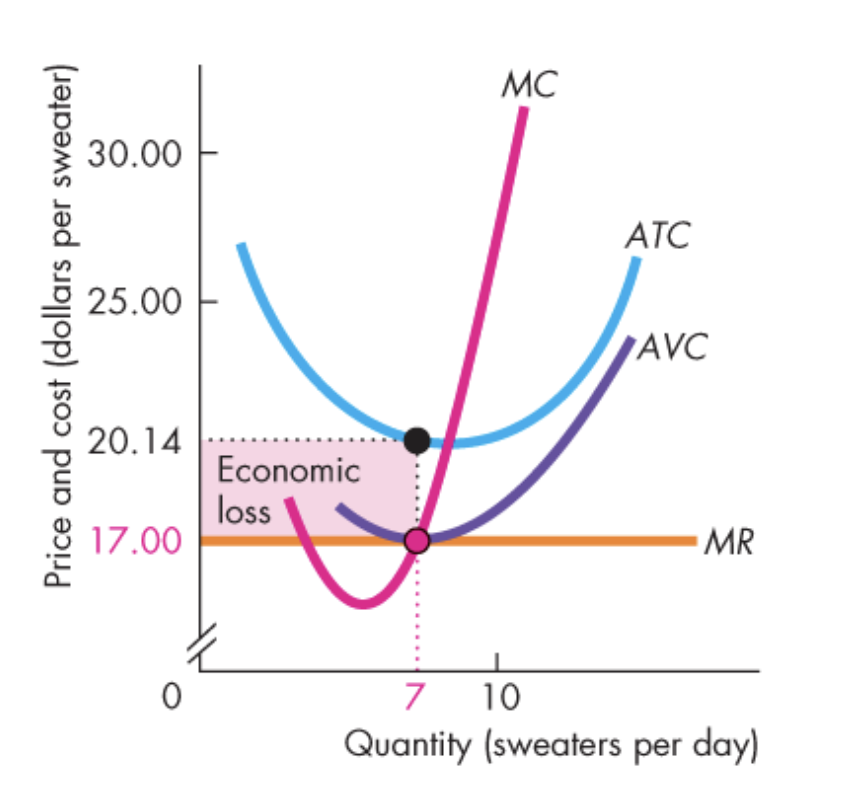

Whats the shutdown point?

The price and quantity at which a firm is indiferent between producing and shutting

AVC is at its minimum

MC curve crosses the AVC curve

MC always crosses AVC at AVC's minimum point.

MC always crosses ATC at ATC's minimum point.

Shutdown Point Graph

Profit-maximizing output: MR = MC

Q = 7

P = AVC = 17

AVC is at its minimum

MC crosses AVC

Firm is indifferent between producing and shutting down

What is the short-run market supply curve?

The quantity supplied by all firms in the market at each price when the number of firms and plant sizes remain unchanged.

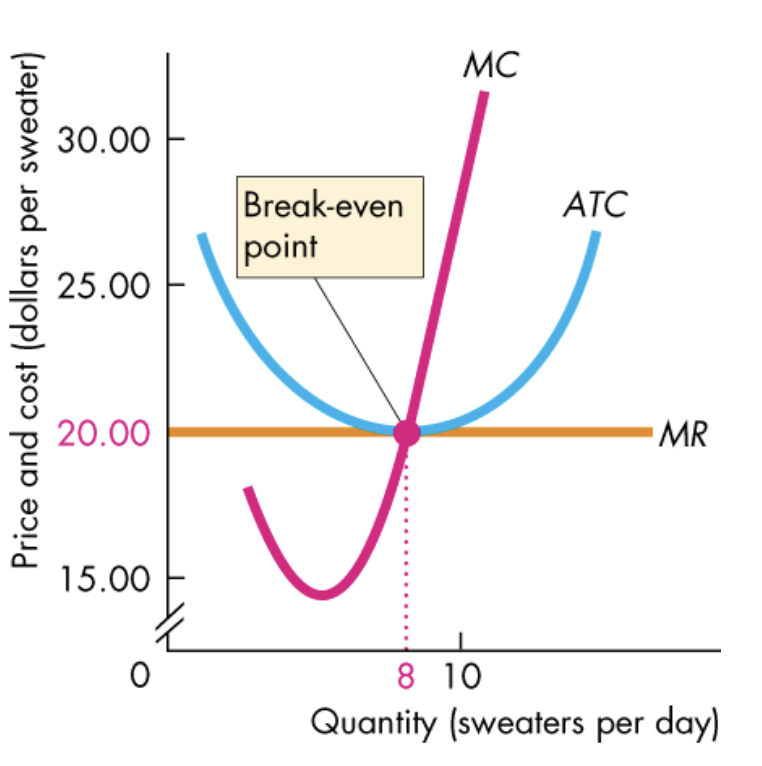

Break-even Graph

Price touches ATC

Economic Profit Graph

Price > ATC

Economic Loss Graph

Price < ATC

What happens when firms earn economic profit in the long run?

New firms enter the industry, increasing supply and lowering price until economic profit is zero.

What happens when firms incur economic losses in the long run?

Firms exit the industry, decreasing supply and raising price until economic profit is zero.

What is the long-run equilibrium condition in perfect competition?

Economic profit = 0

P = ATC

Resources are used effieicntly when…

No one can be made better off without making someone else worse off.

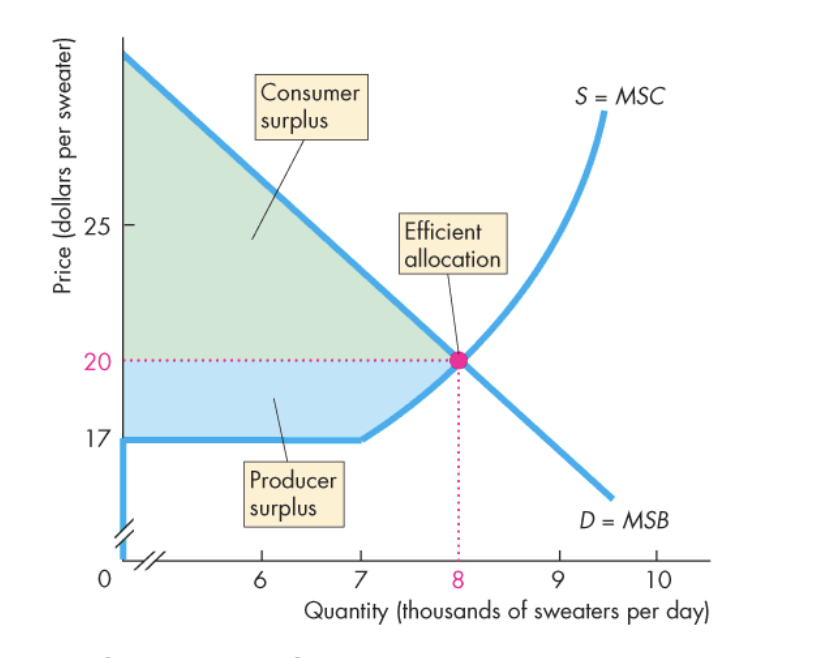

What does the market demand curve represent?

Marginal Social Benefit (MSB).

What does the market supply curve represent?

MSC Marginal Social Cost

When is the market supply curve equal to MSC?

When firms bear all the costs of production.

Perfect Competition and Efficiency

MSB = MSC

Consumer surplus in the graph

area above price line and below demand curve

Producer surplus in the graph

area below the price line and above the supply curve

Total Surplus in the graph

consumer suplus + producer surplus

Graph of Efficient Allocation

Market equilibrium where MSB = MSC and total surplus is maximized.

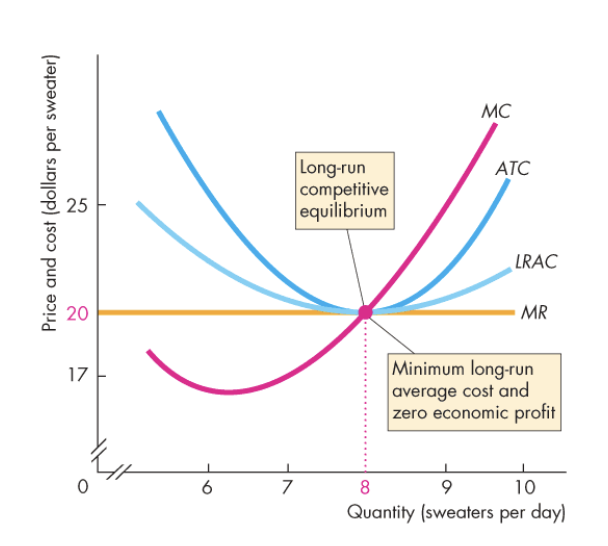

Long-Run Competitive Equilibrium

MR = MC

P = ATC

P = minimum LRAC

Economic profit = 0

Firm produces at the lowest possible cost

No incentive for firms to enter or exit