IA Quiz

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

28 Terms

Equity Valuation Models

Equity just means ownership in a company, specifically shares of stock. When you own a stock, you own a small piece of “equity of that company”

Valuation means figuring out what something is worth

So Equity Valuation = figuring out what a company’s stock is actually worth

Fundamental Analysis

Using information about a company’s current and future profitability to determine its fair market value (figuring out a stock’s true value)

The goal of fundamental analysis is to identify stocks that are mispriced relative to their “true” or “intrinsic” value.

Fundamental Analysis is a method of equity valuation that uses a company’s current and prospective financial data to determine its intrinsic value to determine if the stock is mispriced and worth purchasing

Every stock has two prices that matter:

The Market Price - is what investors are currently paying for a share in the market — driven by supply, demand, emotions, news, and speculation.

The Intrinsic Value - is what a share is actually worth based on real financial data — the company's earnings, assets, growth potential, and future cash flows.

Market Cap and Valuation Ratios

Market Capitalization - is the total market value of a company. This is what makes using valuation ratios possible. It is the Stock Price x Total Shares Outstanding

Valuation ratios are ratios commonly used to access the valuation of one firm compared to others in the same industry using Market Cap. It turns raw numbers into proportions so you can compare companies of different sizes within the same industry. They take the market value and divide it by something meaningful: earnings, sales, book value, or growth so you can compare one company to another one fairly.

P/E, P/B, P/S, and PEG are the valuation ratios used to make these comparisons

P is the price of one share

Shareholder’s Equity

Shareholders’ Equity: Assets minus Liabilities. It is what remains for shareholders after all obligations are paid, this is why it is called residual claimants.

Shareholders don’t get paid first — credits, suppliers and debtors all have priority.

Book Value vs Market Value

Book Value: is the net worth of a company as reported on the balance sheet, based on historical cost. It records assets as the price the company originally paid for them, not what they’re worth today.

Market Value: is the current value of the company’s assets and liabilities. It is what the company is worth right now

Market value is forward-looking, it reflects what investors believe the company is expected to earn in the future. Growing, profitable companies will almost always have a market value far above their book value.

Floor For Stock Price

A floor is the lowest reasonable price a stock should ever fall to. Even if a company is struggling, its stock shouldn’t trade below what the company is fundamentally worth in the most basic sense, because than at that point it would be cheaper to just buy the whole company and sell it off for parts than just buy the stock. The floor is that boundary

Liquidation Value (A Floor Price Measure)

Liquidation Value is the net amount that could be realized (cash you actually walk away with) by selling all of a firm’s assets after paying off its debt

Liquidation Value (conceptual formula) = Asset Sale Proceeds - Total Debt

Liquidation Value is the worst case scenario value.

Liquidation value per share is considered floor for a stock price because if a stock ever traded below this number, investors could theoretically buy the whole company, shut it down, sell everything off, and walk away with more money than they paid. That opportunity would drive the price back up so the stock rarely stays below the liquidation value per share

If a stock’s market price ever fell below the liquidation value per share, that would mean you could buy one share for $10 but your share would be worth $15, you’d be getting $15 worth of value for $10. This opportunity would cause investors to immediately buy the stock and drive the price back up. The stock price shouldn’t stay below the liquidation value per share.

Replacement Cost (A Floor Price Measure)

The Replacement Cost is the cost of rebuilding or replacing all of a firm’s assets from scratch, minus its liabilities.

Replacement Cost is another floor price measure because if a company’s price ever fell below what it would cost to simply recreate that company, it would be cheaper to buy enough shares to own the existing company than build a new one.

“if a company’s price fell below what it would cost to recreate it, it would be cheaper to buy the entire company than build a new company similar”

How companies actually get acquired is investors or companies buy up all the shares until they own it entirely.

Tobin’s Q (A Valuation Ratio Using Replacement Cost)

Tobins Q is the ratio of the market value of a firm to its replacement cost

If Q > 1 the market value the firm is above the replacement cost. Investors believe the company generates more value than it would cost to rebuild it.

Q = 1 the market value equals replacement cost, perfectly in line

Q < 1 Market values the firm below replacement cost, potentially undervalued, cheaper to buy than to rebuild

A Tobin’s Q trends towards 1 in the long run as competition and market forces push a company’s market value back in line with its replacement cost

Balance Sheet vs Expected Future Cash Flows

The balance sheet is helpful for determining liquidation value and replacement cost, but expected future cash flows are more important for estimating a firm’s value as a going concern (as a living, functioning business)

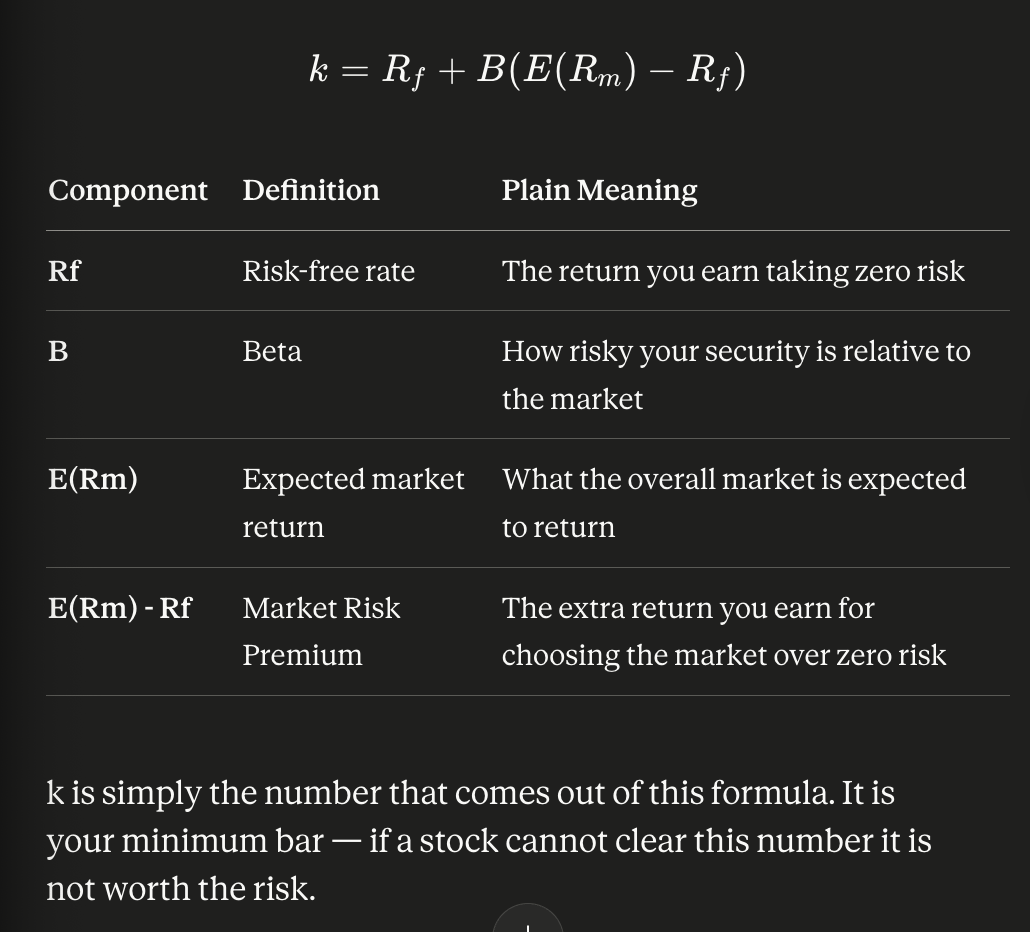

CAPM gives you k (Required Rate of Return)

The minimum return an investor needs to earn on a security to justify taking on it’s risk using the CAPM formula

What is the required rate of return?

What return does this investor require?

What should this stock return?

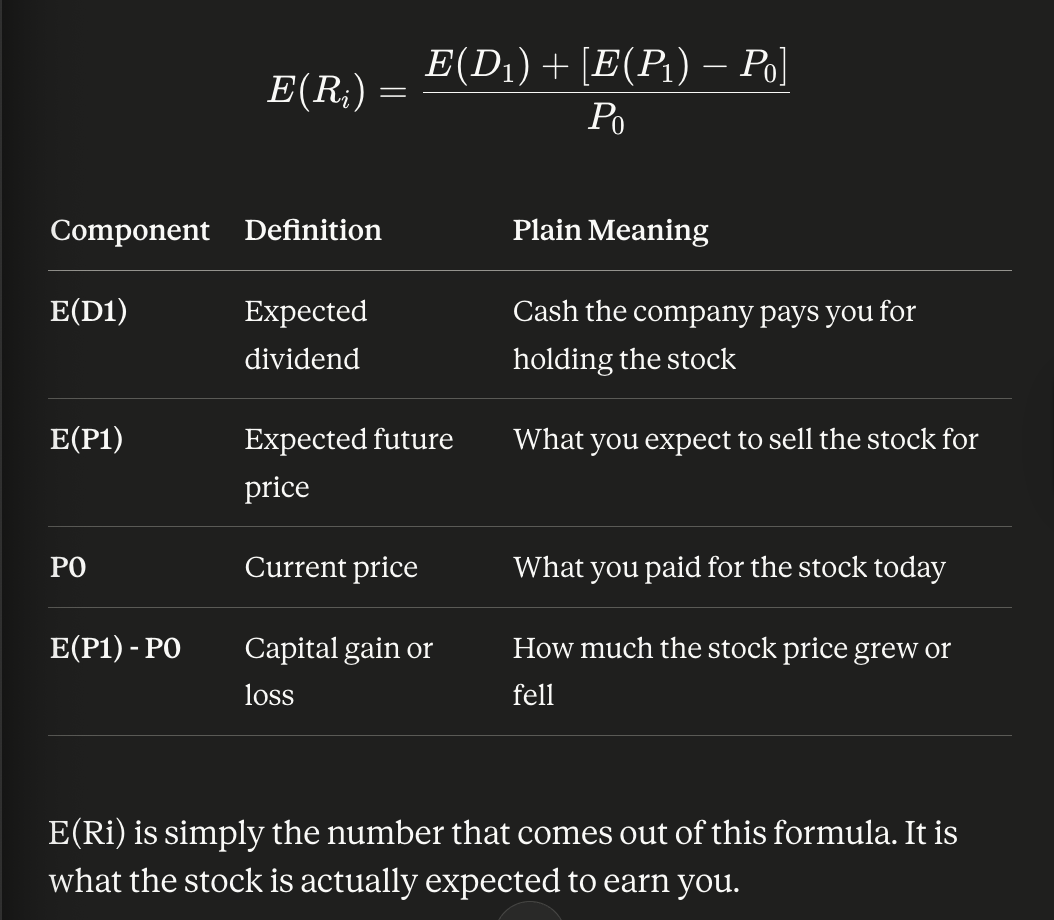

HPR gives you E(Ri) (Expected Return)

The total return earned on a stock over the period you hold it, composed of dividends and capital gains or losses

What is the expected return on this stock?

What is the holding period return?

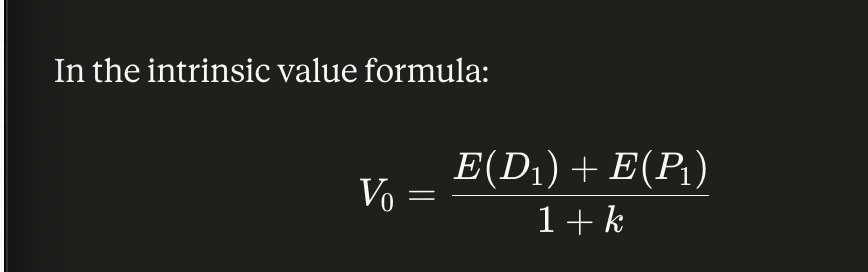

Intrinsic Value V0.

V0 is the label for intrinsic value. The zero in V0 means as of right now, the value today.

Intrinsic Value is the true value of a stock based on a model. It represents an investor’s estimate of what a stock is actually worth calculated as the present value of all future cash payments on a per share basis. You use intrinisc value when you plan to collect dividends for a set period of time and then sell the stock at an expected future price.

Intrinsic Value captures two sources of cash a stock will pay you: dividends (cash payments the company makes to you while you hold the stock) and final sale proceeds (the price you eventually sell the stock for)

Both dividends and final sale proceeds get discounted back to today using k - the risk adjusted rate calculated from CAPM

If a stock’s intrinsic value is greater than it’s market value it’s a GOOD INVESTMENT

Now if a stock’s intrinisic value was less than it’s market value than it’s not worth buying

If they’re equal its fairly priced

Our market value is also simply the current stock price trading in the market right now, it doesn’t need to be calculated you just observe it through Google Finance, Bloomberg etc

Intrinsic Value is the goal of fundamental analysis, you calculate it to find stocks where the market price does not reflect the true value (the intrinsic value), meaning the stock is mispriced.

Present Value PV is the value today of cash you expect to receive in the future, adjusted for the fact that money received in the future is less than money received today.

Market Capitalization Rate

Important Distinction:

Market Capitalization: The total market value of a company (share price x total shares outstanding)

Market Capitalization Rate is the required rate of return based on the market. It is the rate of return that the market as a whole agrees a stock should earn given its risk

Equilibrium and Market Capitalization Rate: Equilibrium is where a stock’s price fully reflects its intrinsic value, meaning the market has correctly priced the stock based on all available information. Equilibrium is where a stock’s intrinsic value is equal to it’s market value.

Market Capitalization Rate is k, but it is the k across the entire market.

k is the market capitilization rate. If you plug in your own personal k you may get a different V0 than the market does. On top of that if an investor thinks the expected future dividends will be different or the expected future price of a stock than they will get a different intrinsic value of a stock.

“If an investor disagrees with the market's consensus estimate of E(D1), E(P1), or k, they will arrive at a different intrinsic value than the market price.”

Determining That a Stock is Undervalued

Given:

ED1 = $4, the stock is expected to pay $4 dividend

P0 = the stock is currently trading at $48

EP1 the expected future price of the stock is $52

Rf = 6% is the risk free rate

ERM = 11% the expected market return

Beta = 1.2 the stock is 1.2x more risky than the market

Step1: Use HPR to find ERi - what the stock is expected to return

4 + (52-48)/48 = 8/48 = 16.67% expected return

Step 2: Use CAPM to find k - the minimum return

.06 + 1.2(.11-.06) = 12%

The expected return was greater than the minimum return so the stock is a good buy or is undervalued

or use V0 and P0

V0 = (4+52)/(1+.12) = $50

P0 = $48

Since the intrinsic value V0 is greater than the market value P0 you should buy the stock

This stock is positive alpha. It is a stock that provides a better return than what is fair given its risk level.

To determine if a stock has a positive alpha it’s expected return (ERi) must be greater than it’s minimum return (k) and it’s intrinsic value (V0) must be greater than it’s market value (P0)

You expect the price of IBX stock to be $59.77 per share a year from now. Its current market price is $50, and you expect it to pay a dividend of $2.15 per share one year from now.

What is the stock’s expected dividend yield?

ED1/P0

You expect the price of IBX stock to be $59.77 per share a year from now. Its current market price is $50, and you expect it to pay a dividend of $2.15 per share one year from now.

What is the stock’s rate of price appreciation? aka capital gains yield

(EP1 - P0)/P0

You expect the price of IBX stock to be $59.77 per share a year from now. Its current market price is $50, and you expect it to pay a dividend of $2.15 per share one year from now.

What is the total holding period return?

(ED1 + (EP1 - P0)) / P0

If the stock has a beta of 1.15, the risk free rate is 6% per year, and the expected rate of return on the market portfolio is 14% per year, what is the required rate of return on IBX stock?

The question gives you Beta, Rf, and E(Rm) — those are your three CAPM inputs. Any time you see those three things on an exam you know to use CAPM to find k.

k = Rf + B(ERM - RF)

What is the intrinsic value of IBX stock, and how does it compare to the current market price?

PO = Current market price

V0 = (ED1 + EP1)/(1+k)

If V0 is greater than P0, the stock is undervalued and it is a buying opportunity

Let’s say you expect the economy to do poorly going forward, would you want to invest in companies with a high beta or a low beta?

Low beta stocks are less volatile; if the market does poorly, they move less dramatically. A low beta stock will drop less than a high beta stock

In CAPM, do you multiply the beta by the return on the market?

k = Rf + B(ERM - RF)

No you multiply by ERM - RF which is the market risk premium

A company has a lot of cash invested at the risk free rate. The company announces that it plans to use this cash to either repurchase some of its stock or pay dividends. Would you expect the stock price to rise or to fall?

Cash sitting at the risk-free rate adds little value to shareholders. Returning it through buybacks or dividends puts that cash in the hands of investors who are taking on risk, making the stock more valuable and driving the price up.

When a company uses cash to pay dividends or repurchase stocks the stock price increases because the cash is being returned to shareholders who are taking on risk, making the stock more valuable than it was when that cash was sitting idle at the risk free rate

Which tends to have higher P/E ratios, high growth stocks or no to low growth stocks?

High growth stocks tend to have a higher P/E ratio. The market is willing to pay a higher price today in anticipation of high future earnings, so even if current earnings are low, the price is high, making the P/E ratio large

P/E stands for Price per Share / Earnings Per Share

A high growth company has a big P because investors are willing to pay a high price today in anticipation of big future earnings even if current earnings are small

Do high growth stocks always have a higher expected return than low or no growth stocks?

Because everyone knows the company will grow, demand drives the price up meaning you will pay a premium today that reduces your actual return. Expected return depends on what you pay not just what a company earns.

By the time everyone knows a company is high growth, the opportunity to earn a high return from it has already passed. You are paying a premium for growth that is already expected.

A company can have high earnings and still give you a low return as an investor if you overpaid or paid a lot for it.

Your return as an investor depends not just on what the company earns, but on what you paid to get in.

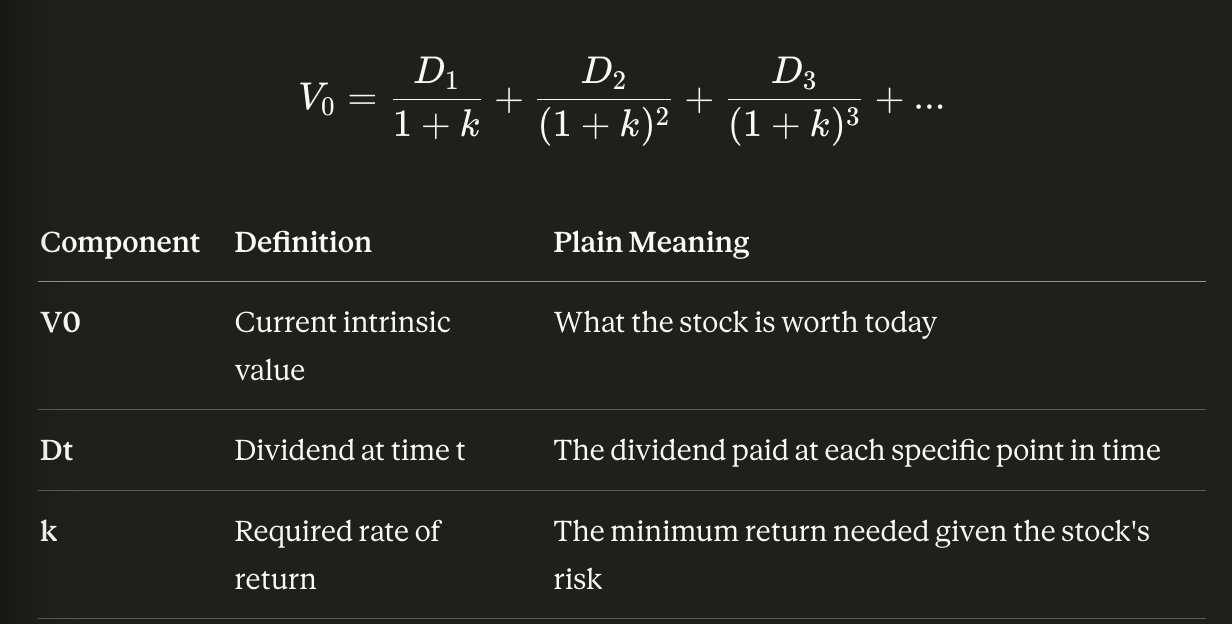

DDM (Dividend Discount Model)

DDM IS used when an investor wants to know what a stock is worth if the only thing they will ever receive from holding it is dividend payments, no plans to sell just collecting dividends year after year

DDM is a model that says the intrinsic value of a stock is equal to the present value of all expected future dividends paid into perpetuity

DDM assumes that the company will keep paying dividends forever into the future. Each future dividend gets discounted back to today’s value and they all get added together. That total is the intrinsic value of the stock today

The professor makes an important note that we must use k in DDM because these are risky cash flows.

Unlike a government bond, where every payment is guaranteed, dividends are never certain. The company can cut or eliminate its dividend at any time. Because of that uncertainty, you discount future dividends using k - the risk-adjusted required return - rather than the risk-free rate. The riskier the company, the higher k is, and the more those future dividends get discounted.

DDM is an expanded version of the intrinsic value formula

In DDM we aren’t given a future sale price, we are holding the stock forever and collecting dividends forever

-

-

Derivative

A Financial instrument/contract whose value depends on the value of other more basic underlying assets or variables such as bonds, stock, currencies, commodities, interest rates, and market indexes

A derivative has no value on its on

Derivatives are also called contingent claims because their value is contingent which means dependent. They are dependent on the performance of the underlying asset.

The types of Derivatives are:

Forwards: A private agreement to buy or sell an asset at a set price on a future date

Futures: Same as forwards but traded publicly on an exchange with standardized terms

Swaps: An agreement between two parties to exchange cash flows over time

Options: The right but not the obligation to buy or sell an asset at a set price

Hedging (Transfering Risk): Using a derivative to protect yourself against an unfavorable price movement in an asset you already own or need to buy “Reduces risk by protecting against unfavorable price moves”

The corn farmer and cattle ranch example:

The corner farmer is worried about the price of corn will go down, this would hurt his income

The cattle ranch is worried the price of corn will go up, that would hurt his costs since he buys corn to feed cattle

By both of them agreeing on a fixed price today for a future transaction, both parties eliminate their risk. They have transferred their risk to each other through a derivative contract

Speculating: Using derivatives to bet on the future direction of an asset’s price without owning the underlying asset. In speculating you take on risk to make a profit. “Takes on risk by profiting from predicted price moves”

Arbitraging: Using derivatives to exploit price differences between markets to make a risk free profit

“Eliminates risk by profiting from price differences between markets”