Long - run aggregate supply (3)

1/10

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

11 Terms

What is long run aggregate supply (LRAS) influenced by ?

Long run aggregate supply (LRAS) is influenced by a change in the productive capacity of the economy

Productive capacity is changed by changes to the quantity or quality of the factors of production

What two opposing views do economists have on how LRAS works in an economy ?

The original view is called the classical view

The insights developed by John Maynard Keynes in 1936 are called the Keynesian view

What does the classical view believe ?

The classical view believes that the LRAS is perfectly inelastic(vertical) at a point of full employment of all available resources

This point corresponds to the maximum possible output on a production possibilities frontier (PPF) -(The maximum possible production (output) that a country can generate if it uses all of its factors of production to produce only two goods/services)

What does the classical view believe will happen in the long - run ?

The classical view believes that in the long- run, an economy will always return to this full employment level of output

There may be short-run output gaps in the economy

During extreme periods of economic growth, there can be an inflationary gap (The amount by which the actual level of national output (Real GDP) exceeds potential output) that develops

In the long run this will self-correct and return to the long-run level of output, but at a higher average price level

During slowdowns or recessions there can be a recessionary gap (The amount by which the actual level of national output (Real GDP) is less than the potential output) that develops

In the long-run this will self-correct and return to the long-run level of output, but at a lower average price level

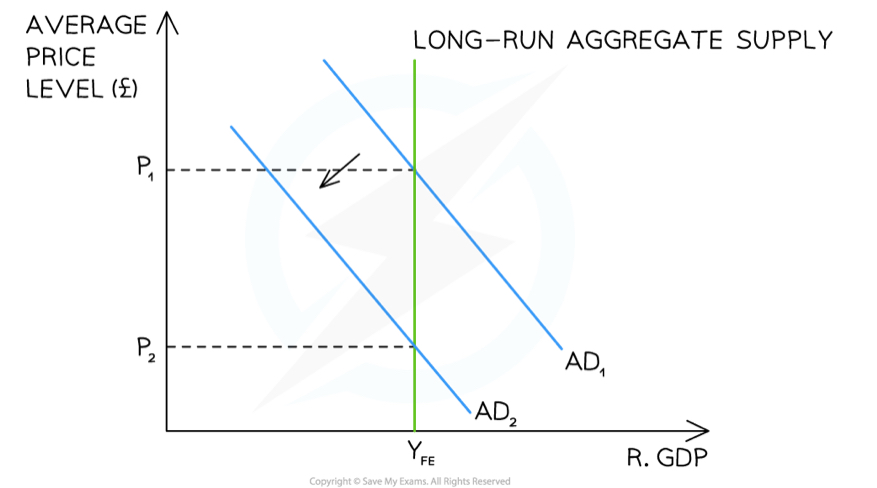

A diagram that shows the Classical View of long-run aggregate supply (LRAS) with a vertical aggregate supply curve at the full employment level of output (YFE) - Diagram Analysis

Using all available factors of prodution, the long-term output of this economy (LRAS) occurs at YFE

The economy is initially in equilibrium at the intersection of AD1 and LRAS (P1, YFE)

A slowdown reduces output from AD1→AD2 and creates a short term recessionary gap

This self corrects in the long term and returns the economy to the long-run equilibrium at the intersection of AD2 and LRAS (P2, YFE)

What did Keynes believe ?

Keynes believed that the long-run aggregate supply curve (LRAS)was more L shaped

Supply is elastic at lower levels of output as there is a lot of spare production capacity in the economy

Struggling firms will increase output without raising prices

Supply is perfectly inelastic (vertical) at a point of full employment (YFE) of all available resources

The closer the economy gets to this point the more price inflation will occur as firms compete for scarce resources

What does the keynesian view believe will happen to an economy ?

The Keynesian view believes that an economy will not always self-correct and return to the full employment level of output (YFE)

It can get stuck at an equilibrium well below the full employment level of output e.g. Great Depression

What else does the keynesian view believe about the government ?

The Keynesian view believes that there is role for the government to increase its expenditure so as to shift aggregate demand and change the negative 'animal spirits' in the economy

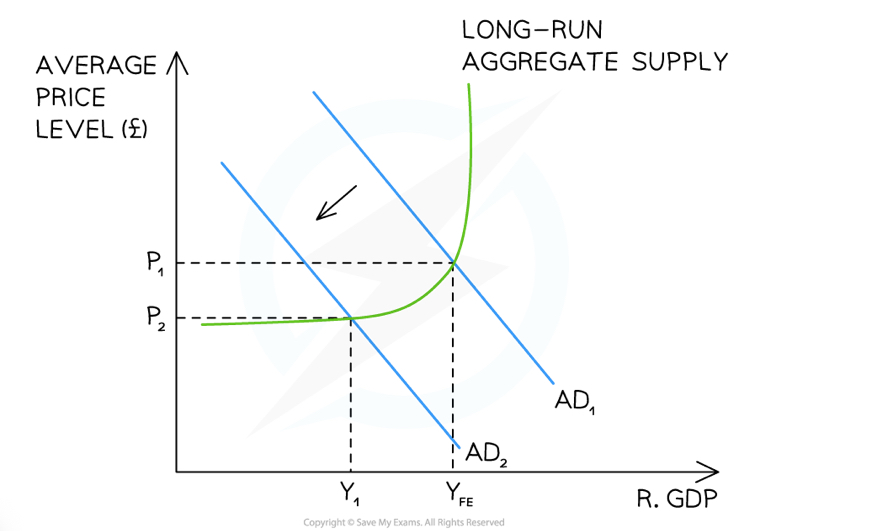

A diagram that shows the Keynesian View of long-run aggregate supply (LRAS) with a vertical aggregate supply curve at the full employment level of output (YFE) becoming more elastic at lower levels of output - Diagram Analysis

Using all available factors of production, the long-term output of this economy (LRAS) occurs at YFE

The economy is initially in equilibrium at the intersection of AD1 and LRAS (P1, YFE)

A slowdown reduces output from AD1→AD2 and creates a recessionary gap Y1-YFE

The economy may reach a point where average prices stop falling (P2), but output continues to fall

This economy may not self-correct to YFE for years

The low output leads to high unemployment and low confidence in the economy

This stops further investment and further reduces consumption

Keynes argued that this was where governments needed to intervene with significant expenditure e.g. Roosevelt's New Deal; response to financial crisis of 2008

What will impact the long - run aggregate supply (LRAS) ?

Any factor that changes the quantity or quality of a factor of production will impact the long-run aggregate supply (LRAS) of an economy:

This corresponds to an outward or inward shift of the potential output of an economy on the PPF

The following factors will shift the entire LRAS curve outwards and increase the potential output of the economy:

Technological advances: these often improve the quality of the factors of production e.g. development of metal alloys

Changes in relative productivity: process innovation often results in productivity improvement e.g. moving from labour intensive car production to automated car production

Changes in education and skills: over time this increases the quality of labour in an economy

Changes in government regulations: these can improve the quantity of the factors of production. e.g. deregulation of fracking (extracting oil from shale deposits) increased oil reserves

Demographic changes and migration: a positive net birth rate or positive net migration rate will increase the quantity of labour available

Competition policy: regulating industries so as to prevent monopoly power results in more firms supplying goods/services in an economy and this increases the potential output of an economy