Accounting Week 6 - Auditing

1/23

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

24 Terms

Principle Shareholders

Absentee Owners

Not involved in day-to-day operations

Agent Management

Involved in the day-to-day of the business

Responsible for financial statements, not accountants/auditors/audit committee, etc…

Information Asymmetry Gap

Time gap between Agent and Principal

due to principle not being involved in the day-to-day to see changes in bus ops

Auditor

Goal is to fill the asymmetry gap so shareholders have more reliable information

independent

free from bias

Big Dilemma

Who pays the auditors?

= The agent does

Why do we Audit?

Fosters Trust in financial information

Ensures Accuracy and Reliability for investors, lenders, & general public

Essential for business to Secure Investors

Vital for maintaining Operations

Definition of Auditing

To objectively obtain and evaluate evidence regarding assertions made by management

Main Goal of Auditing

Ensure a business is free from material misstatements

They are NOT responsible for —>

Do NOT detect fraud

do consider that, but not their goal

Do NOT test every transaction

Do NOT certify statements, rather ensure reliability

Materiality Limit

Threshold above which any misstatement or omission in F/S is considered significant enough to potentially influence investors’ decisions

Do not share the materiality threshold with management or the company, as knowing this limit could encourage them to intentionally commit fraud up to that threshold.

Auditing accuracy based in accordance to GAAP

Systematic process (lots of planning)

GAAS (Generally Accepted Accounting Standards)

Risk-based approach to auditing by calculating the materiality limit

Objectively collect and evaluate evidence to support testing

auditors must be independent (objectivity)

must act with integrity and objectivity

Assertions made by management

Assertions: everything in the financial statement

ex) management asserted that the A/R balance is 500k

Assertions should conform to specific rules (GAAP & IFRS)

ex) “Financial statements is fair in all material aspects and in accordance with GAAP.”

Report results (auditing findings) to users - BOP, Debt & Equity & Equity Investors

Present and Audit Opinion: Report of independent registered accounts + found in 10k

Types of Assertions

Occurrence

Completeness

Accuracy

Cut-off

Classification

Existence

Valuation

Rights & Obligations

note: all are fairly self explanetory and can be understood by what the word means

Occurrence

Transactions actually happened/took place

Reporting a sale - auditor checks occurrence

Completeness

Did all transactions get recorded

makes sure that all sales/expense transactions are on F/S

Accuracy

Number & Details in F/S are correct

transactions are recorded in proper amounts

Cut-off

Ensures transactions are recorded in the correct accounting period

December expenses are not recorded in January’s #s

Classification

Transactions are recorded in the correct accounts

Existence

Ensures that the transaction really exists on the F/S date

Valuation

Assets/Liabilities on F/S at the correct value

inventory not recorded @ made up expense

Rights & Obligations

Owns assets and is responsible for liabilities

does company have the title for the asset

Audit Risk

Auditors do not audit every transaction. Therefore, audit risk can never be 0

Auditors grant reasonable assurance that the financial statements are free from material misstatements

Types of Opinions

Unmodified/Unqualified: “Clean” and free from material misstatements

Modified: Minor misstatements, and parts do not present fairly

Adverse: Do not present fairly (RUN!)

Disclaimer: ^

may not be independent

the auditor could not obtain enough evidence

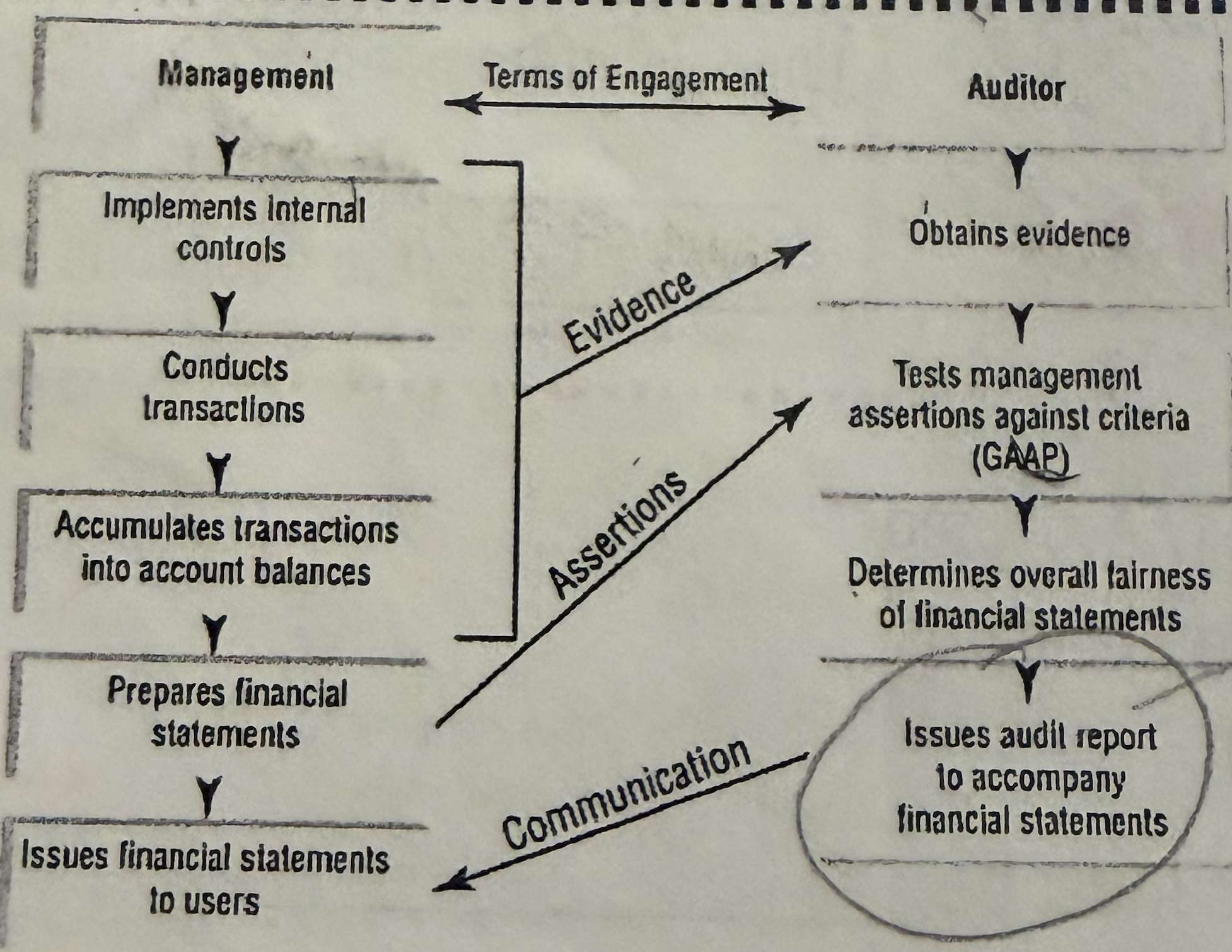

Management ←→ Auditor

Types of Fraud

1) Misappropriation of Assets (stealing)

more common, smaller losses

2) Fraudulent Financial Reporting

less common, larger losses

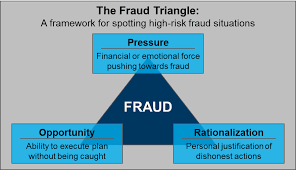

Fraud Traingle

Opportunity

the only point of the Fraud Triangle that management can control by using internal controls: activities to safeguard assets and minimize errors/fraud in financial reporting

Management/Company cannot control →

Rationalization

“I don’t get paid enough.”

“I was going to pay it back.”

Pressure

Financial medical bills

Expensive taste