Introduction to Business Concepts - FBLA

1/229

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

230 Terms

Monetary Policy and the Role of the Federal Reserve System

A set of actions to control a nation's overall money supply and achieve economic growth. The Federal Reserve System is the central banking system.

- Supervises and regulates banks.

- Maintains financial stability.

- Provides banking services.

- Promotes max employment and minimize and contain systemic risks.

Self-Funding

Involves taking money from your savings account, dipping into retirement funds, using credit cards, or asking for donations.

- Risk of long-term debt or loss of personal savings

- Retain full ownership of the business.

Crowdfunding

Where entrepreneurs pitch their products and request financial backing.

- Lets you maintain full ownership of your company if you are willing to thank your donors with free or discounted products.

Small Business Loan

A loan used to fund expenses connected with operating a small business. Preparing a business plan and financial projections for the next five years might be necessary to get the loan.

Venture Capital from Investors

Raising venture capital from investors.

Develop, Evaluate, and Modify a Spending/Savings Plan

1. Decide on a time frame.

2. List all your income.

- Properly understand where the money is coming from.

3. Anticipate expenses.

4. Evaluate your plan.

- Subtract expenses from the total income to determine whether it is necessary to find an additional source of income.

Describe the Purpose of Budgets

- Helps you manage money and ensure your money does not run out each month.

- Saves money and goals for emergencies.

Steps in Preparing a Good Budget

1. Calculate your net income.

2. Track your spending.

- Categorize into fixed and variable.

3. Set realistic goals.

- Short-term and long-term.

4. Make a plan.

- Set specific and realistic goals for spending.

Proper Procedures for Managing a Checking Account

1. Automation

- Set up a direct deposit so the paycheck lands in account automatically.

2. Knowing your Balance

- Makes it easier to plan for bills, avoiding fees, and easier to budget spend.

3. Embrace Potential Earnings

- Getting extra money deposited into your account makes it easier to manage the checking account and budget.

4. Avoid Fees.

5. Decide Where to Keep your Extra Money.

- Spend only what you have

- Record interest earned

- Record service charges

Services by Banks

- More branches.

- Stricter rules and less flexibility.

- More options for banking, retirement and investments.

-

Services by Credit Unions

- Tend to have lower interest rates for loans and lower fees.

- Surcharge-free ATMS.

- Not for profit.

- CU profits are returned to members through benefits.

- Members get to vote on policies and decisions.

- National Credit Union Administration (NCUA) insures up to $250,000 per share owner.

Fixed Expenses

Costs that are the same amount on a routine basis.

- Car Payments.

- Mortgage or rent.

- Insurance premiums.

- Utility bills.

Variable Expenses

Costs that vary over time. Not stable and the cost is not uniform.

- Groceries.

- Movie tickets.

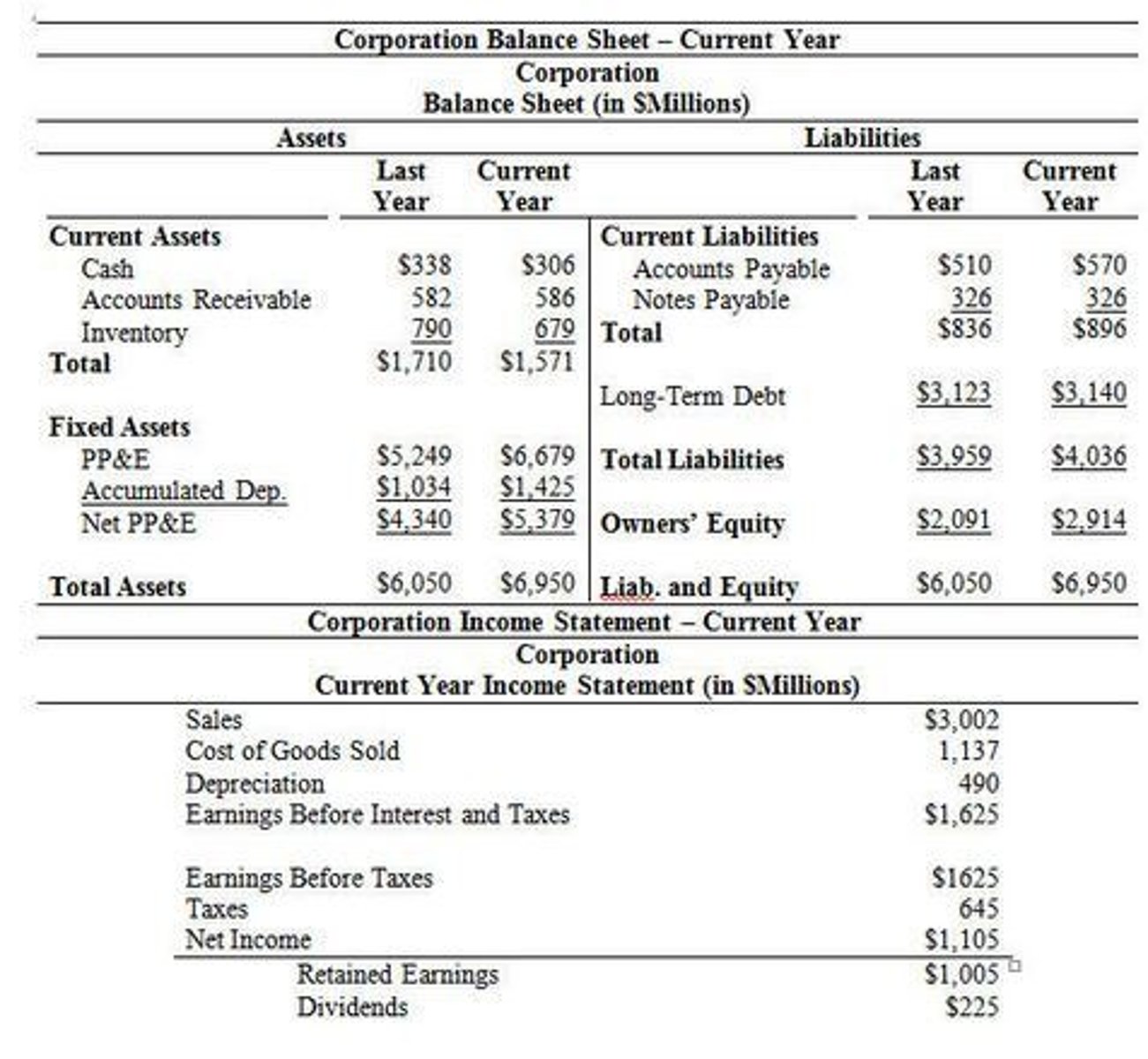

Financial Statements

Written records that convey the financial activities of a company. Provides an overview of assets, liabilities, and shareholders' equity as a snapshot in time. Investors and analysts rely on this to analyze a company's performance.

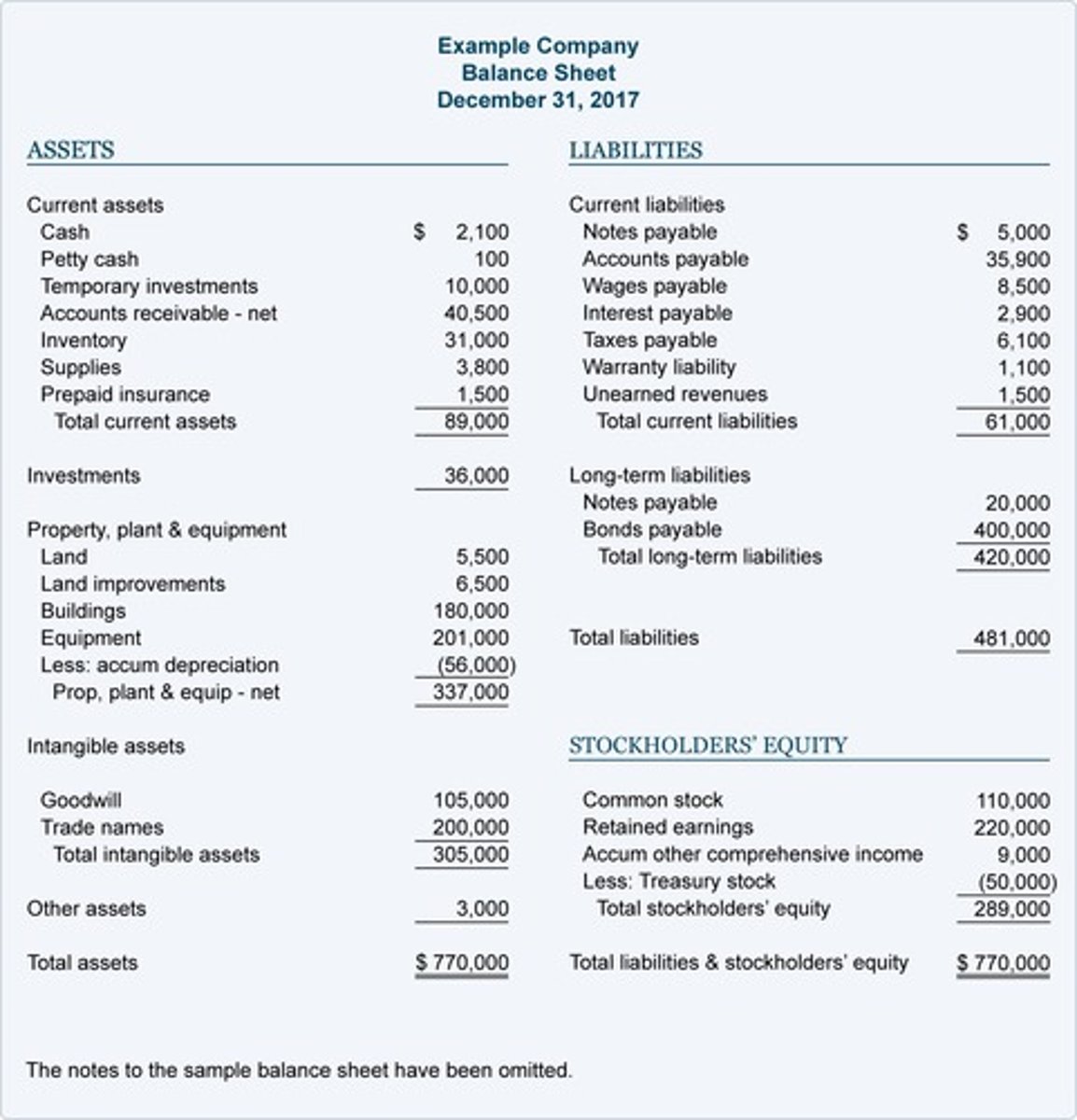

Balance Sheet

Provides an overview of a company's assets, liabilities, and shareholders' equity at a specific time and date.

Assets

Cash and other property with a monetary value.

Liabilities

Accounts payable are the bills due as a part of a business's operations. This includes utility bills, rent invoices, and obligations to buy raw materials.

Shareholders' Equity

A company's total assets minus its total liabilities. It represents the amount of money that will be returned to shareholders if all assets were liquidated.

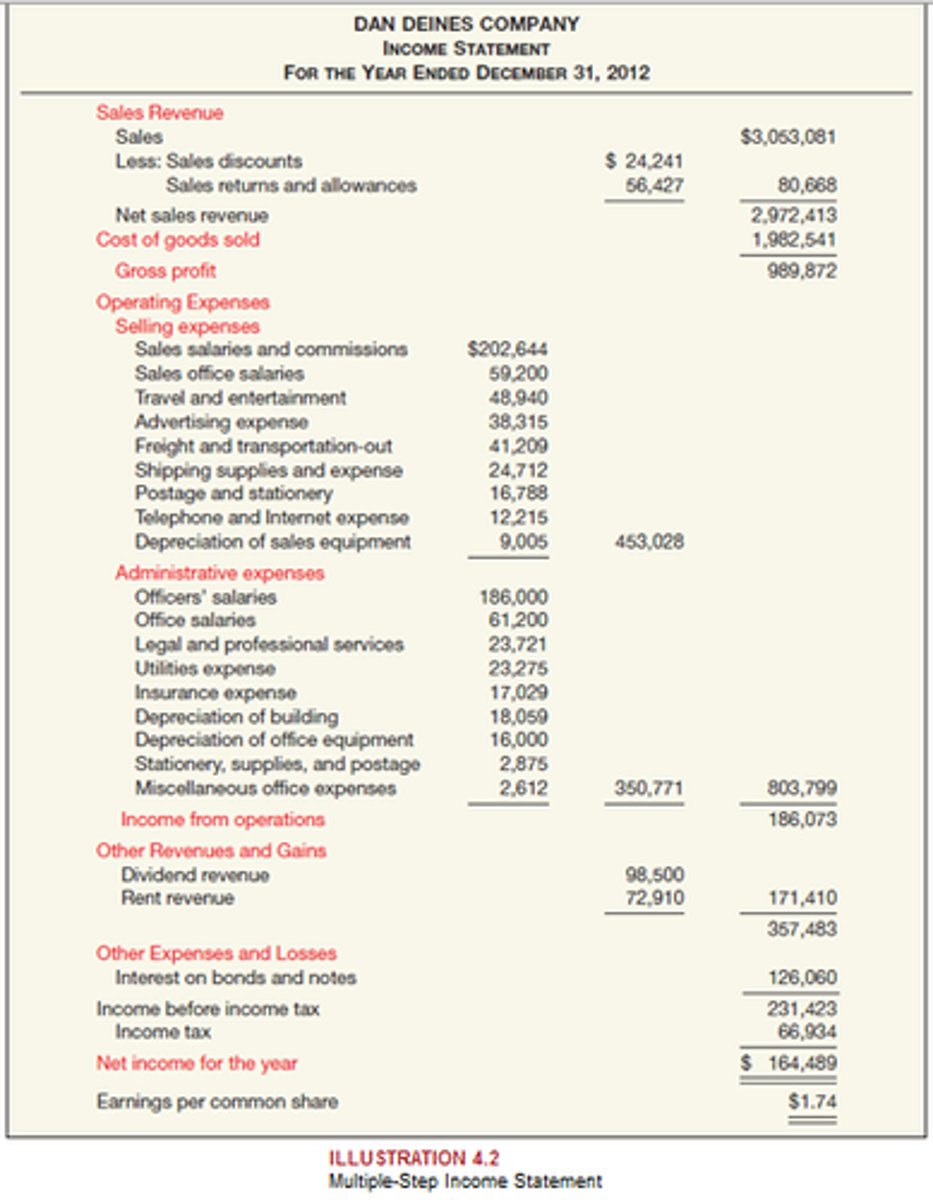

Income Statement

Covers a range of time which is a year for annual financial statements and a quarter for quarterly financial statements. Provides an overview of revenues, expenses, net income, and earnings per share. Shows details of profitability. Depicts how well a company can control and handle expenses.

Revenue

Total earned by selling a company's products or services.

Operating Revenue

Total earned by selling a company's products or services.

Non-Operating Revenue

The income earned from non-core business activities.

- Interest earned.

- Rental income.

Expenses

The cost of assets consumed, or services used in the process of generating revenues. Includes the cost of goods sold, selling, general, and administrative expenses, depreciation or amortization, and research and development.

Cash Flow Statement

A summary of how cash flows throughout a company. Provides insight as whether a company is economically stable.

1. Operating Activities

- Sources and uses of cash.

2. Investing Activities

- Any sources of cash from a company's investments in its long-term future.

3. Financing Activities.

- Includes the cash from investors or banks and the cash paid to stakeholders. Includes debt issuance, loans, and debt repayments.

Interpret Financial Statements

Compared to prior periods to understand changes over time better. Also read when comparing results to competitors.

Online savings or Money Market Account

Best for short-term investments. (Less than 3 years)

CD

It is not liquid and is FDIC insured. Intermediate-term investments. (3 to 10 years)

Short-Term Bond Funds (Index or ETF)

It has some risk and may have an investment minimum. (3 to 10 years)

Equity Index Funds (Stocks)

May have an investment minimum. Long term growth with a higher amount of risk. (10 or more years).

Equity ETFs

Long-term growth. It trades like stock and carries a high risk.

Robo-Advisors

Computer programs that provide detailed and personalized investment advice in place of a financial advisor. Management fees. (10 or more years)

Mutual Funds

Combine money from many investors to buy a variety of investments. Designed for longer-term investors.

Real Estate

Long-term investment. It is a good way to generate a steady income stream.

Savings With Higher and Lower Risks

High - Stocks

Low - U.S. Treasury Securities

Annual Report

Audited document required by the SEC and sent to a public company's or mutual fund's shareholders at the end of each fiscal year. It reports the financial results.

SEC Filing

A document, usually containing financial data, that a company delivers to the SEC and to the public.

EDGAR

Electronic data gathering, analysis, and retrieval. Used by all public companies to transmit required filings, such as quarterly reports and annual reports.

Financial Statement

A written report which quantitatively describes the financial health of a company. Includes an income statement and a balance sheet.

Bank Loans

Generally competitive interest rates and it is easier to obtain for people with varying credit histories. Repayment behavior can positively impact credit scores if on time.

Credit Cards

Typically have higher interest rates. Easy to obtain for people with varying credit histories. Timely payments can improve credit scores, but not on time can negatively affect it.

Personal Lines of Credit

Interest rates are usually lower than credit cards. Requires a good credit history and solid income stability. Repayment history influences credit scores.

Payday Loans

A short-term, high-interest loan that usually must be repaid on the borrower's next payday.

It is rather easy to obtain with minimal requirements.

Peer-to-Peer Lending

Financial transaction that occurs directly between individuals or "peers". Repayment behavior influences credit scores similarly to traditional loans. Accesible to borrowers with fair to good credit scores.

Home Equity Loans

Home owners can borrow against the appraised value of their already purchased homes. Typically has a lower interest rate and requires homeownership.

Revolving Credit

Credit that is automatically renewed as debts are paid off. Comes with a capped limit and can be used up until you reach a threshold.

Installment

Includes a fixed payment schedule for a specified duration.

Open Credit

Requires that all money borrowed must be repaid in full every month.

Credit

A loan or an agreement in which the lender supplies the borrower with money, goods or services which is to be returned in the future.

Advantages of Using Credit

- Allows you to make purchases and investments that you do not have immediate funds for.

- Provides a way to pay for goods and services.

- Helps you establish a positive credit history.

- Allows for flexibility in managing payments.

- Offers reward programs, cashback, travel benefits, and other perks for cardholders.

Disadvantages of Using Credit

- The cost of borrowing, including interest charges and fees, which can accumulate over time.

- Mismanagement of credit can lead to excessive debt accumulation.

- Late payments, high credit utilization ratios, and defaulting on credit obligations can damage your credit score, affecting borrowing and interest rates.

- Easy access to credit can tempt people to overspend and accumulate too much debt.

- Risk of fraud and identity theft.

- Relying to heavily on credit can create a dependence on these borrowed funds.

Computing Simple Interest Loans

Principle amount x Annual interest rate x Term of the loan in years.

Maintaining and establishing a good credit score.

- Consistently making on-time payments.

- Check credit reports regularly.

- Pay loans on time.

- Stay away from the credit limit.

- Only apply for credit that you actually need.

Sources of Consumer Information

- Consumer Reports: published by various organizations which contains detailed analysis of products and services.

- Government agencies.

- Newspaper and electronic media.

- Social media.

- Advertisement.

- Word of mouth.

- Consumer reviews.

- Business sources.

Rights and Responsibilities of Consumers

- Right to safety.

- Right to choose.

- Right to be heard.

- Right to be informed.

- Right to redress.

- Right to be informed.

- Right to service.

- Right to a healthy and sustainable environment.

Ways to Protect Consumer Rights

- Consumer warranties.

- Key Consumer Protection Laws.

- Being aware of scams.

- Learning your basic consumer rights.

- Evaluate large or risky purchases.

- Asking about warranties.

- Checking reviews at the Better Business Bureau.

- Careful about online purchases.

Federal Securities Act

Limits the sale of investment contracts.

Fair Credit Reporting Act

Regulates the collection of credit information.

Dodd-Frank Act

Regulates subprime mortgages and other predatory lending practices.

Fair Housing Act

Act banning refusal to sell or rent a dwelling to any person because of race, color, religion, sex or national origin.

Fair Debt Collection Practices Act

Prohibits unfair, abusive, and deception methods of collecting debt.

CAN-SPAM Act

A federal law that placed guidelines on mass commercial emails. Establishes requirements for commercial messages, including not using false or misleading headers and subject lines.

Gramm-Leach-Bliley Act (GBLA)

Requires U.S. financial institutions to reveal in writing how they handle, share, and protect consumers' information.

Children's Online Privacy Protection Act (COPPA)

Governs what information directed to children under 13 years of age can collect from their visitors.

Better Business Bureau and Federal Trade Commission Functions

To protect the public from deceptive or unfair business practices and from unfair methods of competition through law enforcement, advocacy, research, and education.

Characteristics, Motivations, and Behaviors of Consumers.

Characteristics: Demographic, geographical, psychographic, and behavioristic.

Motivations: Emotions, situation, personality, perceptions, and non conscious beliefs.

Behavior: Observe how people choose, use, and discard products and services.

Income Level (Impact on Consumer Behavior)

Consumers with higher incomes may be more willing to spend on premium products while lower incomes may prioritize budget-friendly options.

Interest Rates (Impact on Consumer Behavior)

High interest rates may lead consumers to delay major purchases or opt for alternative financing options.

Inflation (Impact on Consumer Behavior)

During high periods of high inflation, consumers may prioritize essential purchases and cut down on other things.

Credit Availability (Impact on Consumer Behavior)

Easy access to credit can encourage spending and borrowing.

Employment Stability (Impact on Consumer Behavior)

Stable employment and income prospects promote confidence and spending.

Tax Policies

Changes in tax policies can influence disposable income levels and affect consumer spending patterns.

Use of Advertisements

To inform, to persuade, and to remind. A marketing strategy should include: Product, price, place, and promotion.

Other Marketing Strategies

- Social media.

- Content marketing.

- Influencer marketing.

- Search engine optimization.

- Email marketing.

Importance of Comparative Shopping

- Make informed decisions.

- Find the best deals.

- Quality assessment.

- Consumer education.

Promotional Sale

For a limited time that is trying to pull in customers.

Clearance Sale

A sale in which the goods in a store are sold at reduced prices, because the store wants to get rid of it quickly or it is closing down

Main Goals and Functions of a Business.

- Generate cashflow.

- Growth and expansion.

- Customer satisfaction.

- Employee satisfaction and development.

- Social Responsibility and Sustainability.

Marketing, operations, human resources, and finance.

Gross Profit

Revenue - cost of sales.

Net Profit

Gross Profit - expenses. The profit a company makes after deducting the costs associated with producing and selling its products or costs associated with its ervices.

Steps in Organizing a Business

1. Identify a Niche

- Determine the specific type of organizational services you are interested in offering.

2. Conduct Market Research

- Research your target market and competition to determine the demand for your service or product.

3. Create a Business Plan

- Clarify goals and identify opportunities and challenges. Develop a roadmap for success.

4. Obtain Licensing and Permits.

- Business license, State local tax permits, home occupation permits, and professional licenses.

5. Establish Your Brand

- Identify your core values, choose a business name, design a logo, build a website, and develop marketing materials.

6. Set up Business Infrastructure

7. Register your Business

8. Build your Team

9. Launch and Market Your Organizing Business

Sole Proprietorship

A business owned by a single person. Owners receive all profits and the profits are only taxed once. Owner makes all decisions and is in complete control of he company and is the easiest and least expensive form of ownership. There is also unlimited liability. No separate legal status.

Partnerships

Two or more people share ownership of the business. Partners share a legal agreement that sets forth how decisions will be made and how profit will be shared. Easy to establish. Divided decision-making.

Sadly, you have to share profits with partners.

Corporations

Businesses that are owned by many investors who buy shares of stock. Considered by law to be a unique entity, separate from those who own it.

C-Corporation

The most common type of corporation, which is a legal business entity that offers limited liability to all of its owners and is taxed separately from its owners. Encourages more risk-taking and potential investment. Limited liability and capital is easier to raise through the sale of stock. Tax benefits. Double taxation and can be costly to form. Required to have annual meetings and many other things.

S-Corporation

Offers limited liability to the owners. They do not pay income taxes, rather the earnings are treated as distributions. Shareholders must report their income on their own income tax returns. There is limited liability and easy transfer of ownership. It can be costly to form and stockholders are limited to citizens of the US.

Limited Liability Company

A hybrid business structure that provides the legal liability of a corporation and the operational flexibility of a partnership or sole proprietorship. More complex than a partnership. Created for small businesses and has an unlimited amount of owners. It can be costly to form and there are yearly administrative costs.

Marketing

Identifies customer needs, promoting products or services, pricing strategies, distribution channels, and market research. Closely interacts with sales as it provides strategies and tools necessary for sales to reach target customers.

Sales

Focuses on generating revenue by selling products or services to customers, negotiating contracts, managing client relationships, and meeting sales targets. Collaborates with marketing to implement sales strategies based on market insights and customers' needs.

Finance

Manages the financial resources of the business, including budgeting, financial planning, investment decisions, financial reporting, and risk management. Works with all other functions to ensure financial stability and support other business operations.

Operations

Involve the management of production processes, supply chain logistics, inventory management, quality control, facilities management, and efficiency improvements.

Human Resources

Manages personnel-related activities, including recruitment, training, performance management, employee relations, compensation, benefits administration, and workforce planning. Makes sure with other functions that there is the right talent and resources to achieve goals. Works with operations to assess staffing needs, finance to manage payroll, and marketing to align hiring strategies with business growth.

Information Technology

Handles technology-related infrastructure, systems development, data management, cybersecurity, digital innovation, and technology support services. Supports and enhances the functions of every other function. Makes customer experiences much better and ensures data security.

Digital Transformation (Current Business Trend)

Businesses need to adopt new technologies. Businesses need to invest in digital tools such as cloud computing, data analytics, automation, and collaboration platforms.

E-Commerce Expansion (Current Business Trend)

Growth of online shopping and e-commerce platforms. Businesses must enhance their online presence, optimize e-commerce platforms, offer personalized shopping experiences, and smooth logistics.

Remote Work and Hybrid Models (Current Business Trend)

Adoption of these models lets employees work from anywhere and promotes work-life balance. Businesses need to implement flexible work policies. Outcome-based performance evaluation rather than strict hours worked.

Sustainability and ESG Practices (Current Business Trend)

Growing emphasis on environmental, social, and governance practices. Consumers favor businesses that prioritize sustainability, diversity, inclusion, and ethical business practices. Businesses need to integrate sustainability into their operations.

Supply Chain Resilience (Current Business Trend)

Businesses need to focus on supply chain resilience, localization, and risk management. Businesses should diversify suppliers, enhance inventory management systems, and invest in alternative logistic routes.

Customer Experience and Personalization (Current Business Trend)

Customers expect personalized experiences, fast response times, and exceptional customer service. Businesses should invest in customer relationship management systems, data analytics, and have wonderful employees.

Rise of the Gig Economy (Current Business Trend)

Gig economy continues to grow, with an increasing number of freelancers, independent contractors and gig workers contributing to the workforce. Provide gig workers with the necessary tools and resources and ensure compliance with labor regulations.

A Business Plan (pt.1)

1. Executive Summary

- Brief summary of your business concept, mission statement, and key objective.

2. Business Description

- A detailed description of your business.

3. Market Analysis

- Conduct an analysis of the market to ensure you can compete with rival competitors. market size and growth opportunities.

4. Organizational Structure and Management

- Outline the structure of your business, including key roles, responsibilities, and reporting lines.

5. Product or Services

- Describe your product or services in detail including pricing strategy and technology.

6. Marketing and Sales Strategy

- Develop a comprehensive marketing plan, including branding, positioning, promotion strategies, and customer acquisition tactics.