financial accounting (Chapter 8)

1/21

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

22 Terms

Receivable

A monetary claim against a business or an individual.

asset, due to money someone owes you

Debtor

The party to a credit transaction who takes on an obligation/payable.

owes you money from credit

Notes Receivable

A written promise that a customer will pay a fixed amount of principal plus interest by a certain date in the future.

I will pay you back plus interest

Maturity date

The date when a note is due

due date

Subsidiary Ledger

Record of accounts that provides supporting details on individual balances, the total of which appears in a general ledger account.

provides the detailed information that supports the total balance reported

Bad Debts Expense

The cost to the seller of extending credit. It arises from the failure to collect from some credit customers.

accounts receivable that are estimated to be uncollectible and recorded as such

Direct Write-off method

A method of accounting for uncollectible receivables in which the company records bad debts expense when a customer’s account receivables is uncollectible.

record bad debt ONLY when you’re sure its uncollectible

“wait until it becomes uncollectible, then write it off.

Allowance method

A method of accounting for uncollectible receivables in which the company estimates bad debts expense instead of waiting to see which customers the company will not collect from.

estimates bad debts expense

Allowance for bad debts

A contra asset account, related to accounts receivable, that holds the estimated amount of uncollectible accounts.

estimated amount of receivables that the company expects will not be collected.

Net realizable value

The net value a company expects to collect from its accounts receivable. (Accounts receivable -Allowance for bad debts)

accounts receivable, after subtracting estimated uncollectible accounts

Percent-of-Sales method

A method of estimating uncollectible receivables that calculates bad debts expense based on a percentage of net credit sales.

Net Credit Sales × Estimated % (based on past experience)

The percentage is an assumption based on past data and judgment

Percent-of-Receivables method

A method of estimating uncollectible receivables by determining the balance of the Allowance for Bad Debts account based on a percentage of accounts receivables.

Ending Accounts Receivable×Estimated Uncollectible %

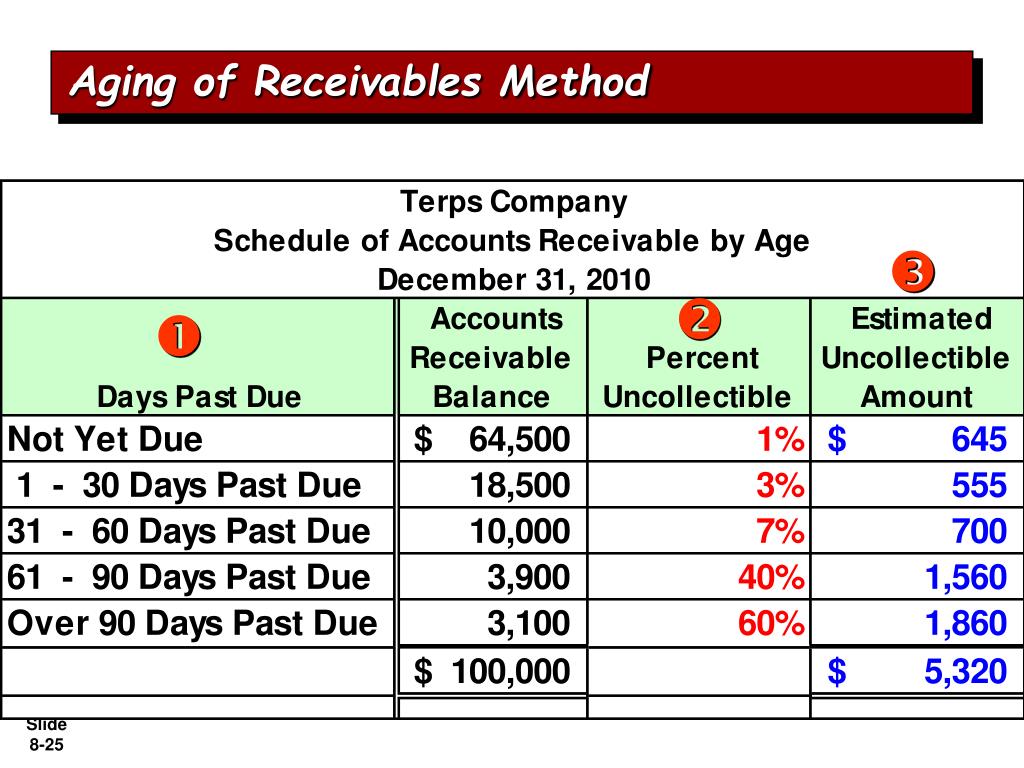

Aging-of-receivables method

A method of estimating uncollectible receivables by determining the balance of the Allowance for Bad Debts account based on the age of individual accounts receivables.

based on how long receivables have been outstanding,

Principal

The amount loaned by the payee and borrowed by the maker of the note.

the original amount of money borrowed

loan = (this) + interest

Interest

The revenue to the payee for loaning money-the expense to the debtor .

Principal × Rate × Time

Interest period

The period of time during which interest is computed. It extends from the original date of the note to the maturity date.

length of time for having interest

Interest Rate

The percentage rate of interest specified by the note.

Maturity value

The sum of the principal plus interest due at maturity.

total amount that must be paid upon maturity date

Dishonors a note

Failure of a note’s maker to pay a note receivable at maturity.

note failed to pay on its due date.

Acid-test-ratio

The ratio of the sum of cash, cash equivalents, short-term investments, and net current receivables to total current liabilities. The ratio tells whether the entity could pay all its current liabilities if they came due immediately (cash, including cash equivalents + short term investments, + net current receivables) / Total current liabilities).

Quick Assets ÷ Current Liabilities

Current Liabilities=Cash + Cash Equivalents + Accounts Receivable

Accounts receivable turnover ratio

A ratio that measures the number of times the company collects the average accounts receivable balance in a year. (net credit sales / average accounts receivable).

indicates the number of times, a company collects its receivables

Days’ Sales in Receivable

The ratio of average net accounts receivable to one day’s sales. The ratio tells how many days it takes to collect the average level of accounts receivables. (365 days / Accounts receivable turnover ratio).

about how many days does it take to collect cash from accounts receivables