Master copy, auditing (copy)

1/285

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

286 Terms

How is Auditing Different from Accounting

Accounting is the recording or economic events while auditing is based on determining if those economic events actually happened

Define - Assurance Services

Individual professional services that improves/enhances the quality of infor for decision making

Define - Attestation services

Type of assurance service in which the cpa firm issues a report about a subject matter or assertion that is the responsibility of another party

Define - Audits

Define - Reviews

CPA issues a report that provides limited assurance of the financial statements. CPA indicates that no material modifications are needed to be in accordance with GAAP. No opinion issued

Define - Non-assurance Services

Services that do not need an auditor - Tax, bookkeeping, payroll

3 types of Audits

Financial

Compliance

Operational

Operational Audit

Evaluates the efficiency and effectiveness of an organization’s operating procedures

3 requirements to become a CPA

Credit hours

Pass the exam

Service hours

Role of PCAOB

Overviewed by the SEC, issues Auditing Standards and rules for CPA firms that audit public companies

Describe Sarbanes Oxley Axt of 2002 and key sections of the act

Restore investor confidence after the Enron crisis

made the PCAOB

Role of the AICPA and 4 major areas

Sets professional requirements for CPAs

Auditing standards, preparation, other attestation standards, and code of professional conduct

Define Peer review

People in the same field review your material/work

When you are auditing publically traded company, what audititng standards are used

PCAOB

What auditing standards are followed for audits of a private company

GAAS

The following questions deal with auditing standards. Choose the best

response.

a. Which of the following best describes what is meant by U.S. auditing standards?

(1) Acts to be performed by the auditor

(2) Measures of the quality of the auditor’s performance

(3) Procedures to be used to gather evidence to support financial statements

(4) Audit objectives generally determined on audit engagements

2

The Responsibilities principle underlying AICPA auditing standards includes a

requirement that

(1) the audit be adequately planned and supervised.

(2) the auditor’s report state whether or not the financial statements conform to

generally accepted accounting principles.

(3) professional judgment be exercised by the auditor.

(4) informative disclosures in the financial statements be reasonably adequate.

3

Who establishes auditing standards applicable to private companies and other non-

public entities in the U.S.?

(1) The Private Company Audit Standards Board

(2) The Financial Accounting Standards Board

(3) The Auditing Standards Board of the AICPA

(4) The Public Company Accounting Oversight Board

3

1

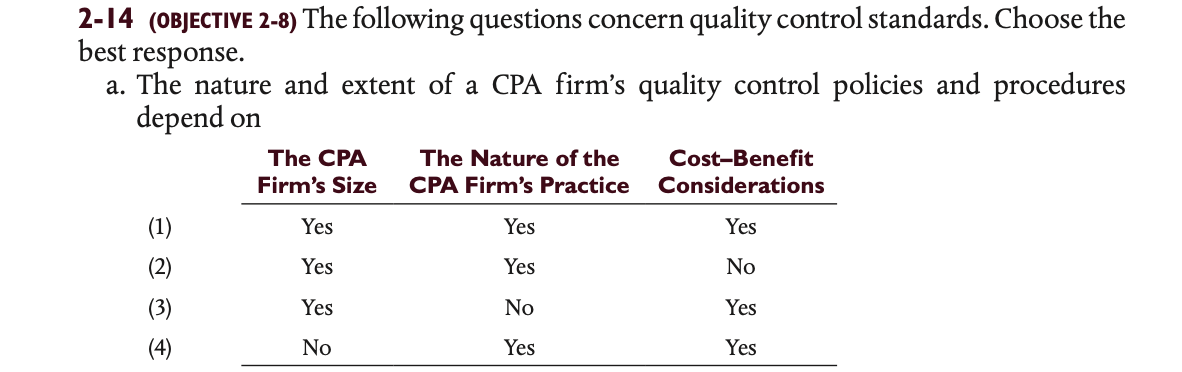

Which of the following is an element of a CPA firm’s quality control system that

should be considered in establishing its quality control policies and procedures?

(1) Complying with laws and regulations

(2) Using statistical sampling techniques

(3) Managing human resources

(4) Considering audit risk and materiality

3

One of a CPA firm’s basic objectives is to provide professional services that conform with professional standards. Reasonable assurance of achieving this objective is provided through

(1) continuing professional education.

(2) a system of quality control.

(3) a system of peer review.

(4) compliance with generally accepted reporting standards.

2

a. An auditor of an entity subject to the rules of the SEC must conduct the financial

statement audit in accordance with

(1) PCAOB standards.

(2) Statements on Standards for Accounting and Review Services.

(3) International Auditing Standards.

(4) Generally Accepted Government Auditing Standards.

1

b. Which of the following provides authoritative guidance for the auditor of a nonpublic

company?

(1) An article in the Journal of Accountancy that discusses new audit requirements

(2) Information obtained from continuing professional education programs

(3) Publication from state CPA societies that provides questions and answers on

frequently asked audit questions

(4) Statements on Auditing Standards

4

The Public Company Accounting Oversight Board (PCAOB) has the duty to

(1) select the public accounting firm for the issuer’s annual audit.

(2) establish rules related to the preparation of audit reports for nonissuers.

(3) conduct investigations concerning registered public accounting firms.

(4) conduct disciplinary proceedings for nonpublic accounting firms.

3

8 elements of an unmodified audit report

Report Title, Audit Report Address, Opinion, Basis for Opinion, Managements Responsibility, Auditors Responsibility, Signature and Address of CPA Firm, Audit Report Date

7 elements for audits of publicaly traded companies

Report Title, Audit Report Address, Opinion, Basis for Opinion, Critical Audit Matters, Signature-tenture and Address of CPA Firm, Audit Report Date

What are the elements of the auditor’s internal control report (SOX section 404)

Report title, Audit report Address, Auditors Opinion, Cross Reference Paragraph, Basis for opinion, Definition Paragraph, Inherent Limitations Paragraph

Described and explain when issued: Unmodified opinion - standard wording

Financial statements are presented fairly

Described and explain when issued: Unmodified opinion - with explanatory paragraph

Opinion is unmodified but the auditor belives it is necessary to provide additional communication

Described and explain when issued: Unmodified opinion - modified wording

unmodified opinion but needs to point out special circumstances

Described and explain when issued: Qualified Opinion - GAAP Departure

Auditor finds misstatements that are material but no pervasis to the finaancial statements

Described and explain when issued: Qualified opinion - Scope limitation

The auditor is unable to obtain sufficient evidence to form an opinion. could be material but no pervasive

Described and explain when issued: Advers opinion

Auditor obtains enough evidence to conclude the misstatements are material and pervasve

Described and explain when issued: Disclaimer of opinion

Auditor was unable to obtain evidence for an opinion, causes for undetected misstatements could be both material and pervasive

What accounting standards setter issues guidelines for performing reviews and compilations

ARSC overview SSARS

What are the standards that cpas follow in performing reviews and compilations

SSARS

What is a review? how is one completed, and how does it differ from an audit of financial statements

Engagement to obtain limited assurance that there is no material modifications need to be made. doing analytical procedures, and inquires.

What is a compilation? What are the requirements? how does it differ from a review and an audit of financial statements

Assist in the format of financial statements, go through, and point out any obvious omissions.

Can there be different types of compilation reports? if so, what are they?

yes, with or without footnotes

CPAs are sometimes requested to perform attestation engagements. define this term

A CPA is engaged to issue a report

What are the agreed-upon procedures

CPA Agrees to perform a specific set of steps and does results in a report to specified users

Which of the following is not a required element of a standard unmodified opinion

audit report issued in accordance with AICPA auditing standards?

(1) A title that emphasizes the report is from an independent auditor

(2) The city and state of the audit firm issuing the report

(3) A statement explaining management’s responsibilities for the financial

statements

(4) The name of the engagement partner

4

The date of the CPA’s opinion on the financial statements of the client should be the

date of the

(1) completion of all important audit procedures.

(2) closing of the client’s books.

(3) finalization of the terms of the audit engagement.

(4) submission of the report to the client.

1

If a principal auditor decides to refer in his or her report to the audit of another auditor, he or she is required to disclose the

(1) Name of the other auditor.

(2) nature of the inquiry into the other auditor’s professional standing and extent of

the review of the other auditor’s work.

(3) reasons for being unwilling to assume responsibility for the other auditor’s work.

(4) portion of the financial statements audited by the other auditor.

4

An entity changed from the straight-line method to the declining-balance method

of depreciation for all newly acquired assets. This change has no material effect on the current year’s financial statements but is reasonably certain to have a substantial effect in later years. If the change is disclosed in the notes to the financial statements,

the auditor should issue a report with a(n)

(1) unmodified opinion.

(2) qualified opinion.

(3) unmodified opinion with explanatory paragraph.

(4) qualified opinion with explanatory paragraph regarding consistency.

1

When the financial statements are fairly stated but the auditor concludes there is sub-

stantial doubt whether the client can continue in existence, the auditor should issue a(n)

(1) adverse opinion.

(2) qualified opinion only.

(3) unmodified opinion.

(4) unmodified opinion with explanatory paragraph.

4

The auditor’s report contains the following: “We did not audit the financial statements of EZ, Inc., a wholly owned subsidiary, which statements reflect total assets and revenues constituting 27 percent and 29 percent, respectively, of the consolidated totals. Those statements were audited by other auditors whose report has been furnished to us, and our opinion, insofar as it relates to the amounts included for EZ, Inc., is based solely on the report of the other auditors.” These sentences

(1) assume responsibility for the other auditor.

(2) indicate a division of responsibility.

(3) require a departure from an unmodified opinion.

(4) are an improper form of reporting.

2

a. As compared to an unmodified opinion, an opinion qualified due to a material departure from generally accepted accounting principles would

(1) include an extra paragraph in the opinion section.

(2) include a slight modification to the auditor’s responsibility section.

(3) include a slight modification to the introductory paragraph in the opinion

section.

(4) indicate that, except for the problem noted, the financial statements are pre-

sented fairly

4

An adverse opinion and a disclaimer of opinion

(1) may be used interchangeably.

(2) both require modification of the opinion section.

(3) result in the auditor’s withdrawal from the engagement.

(4) indicate situations in which there are material GAAP departures.

2

Which of the following best describes the responsibility of the CPA in performing

compilation services for a company?

(1) The CPA has to satisfy only himself or herself that the financial statements were prepared in conformity with accounting standards.

(2) The CPA must understand the client’s business and accounting methods and read the financial statements for reasonableness.

(3) The CPA should obtain an understanding of internal control and perform tests

of controls.

(4) The CPA is relieved of any responsibility to third parties

2

The standard compilation report includes which statement or phrase?

(1) Management is responsible for the financial statements.

(2) The accountant does not express an opinion but expresses only limited assurance on the compiled financial statements.

(3) The objective of a compilation is to assist management in presenting financial

information in the form of financial statements.

(4) The accountant has compiled the financial statements in accordance with standards established by the Auditing Standards Board.

1

A CPA is performing review services for a small, closely held manufacturing company. As a part of the follow-up of a significant decrease in the gross margin for the current year, the CPA discovers that there are no supporting documents for $40,000 of disbursements. The chief financial officer assures her that the disbursements are proper. What should the CPA do?

(1) Include the unsupported disbursements without further work in the statements on the grounds that she is not doing an audit.

(2) Modify the review opinion or withdraw from the engagement unless the unsupported disbursements are satisfactorily explained.

(3) Exclude the unsupported disbursements from the statements.

(4)Obtain a written representation from the chief financial officer that the disbursements are proper and should be included in the current financial statements.

2

A Type 1 service auditor’s report on internal controls at a service organization

(1) includes an opinion about the suitability of the design of controls at the serviceorganization.

(2) is based on the performance of tests of controls and substantive tests of transactions at the service organization.

(3) contains an opinion about the operating effectiveness of internal controls at the service organization.

(4) provides an opinion about the fair presentation of the service organization’s financial statements in accordance with accounting standards.

1

Which of the following professional services would be considered an attestation

engagement?

(1) Preparing the income statement and balance sheet for one year in the future

based on client expectations and predictions.

(2) Providing financial analysis, planning, and capital acquisition services as a part-time, in-house controller.

(3) Advising management in the selection of a computer system to meet businessneeds.

(4) Advocating on behalf of a client about trust tax matters under review by the

Internal Revenue Service.

1

An auditor is reporting on cash basis financial statements. These statements are best referred to in the opinion of the auditor by which of the following descriptions?

(1) Cash receipts and disbursements and the assets and liabilities arising from cash transactions

(2) Financial position and results of operations arising from cash transactions

(3) Balance sheet and income statements resulting from cash transactions

(4) Cash balance sheet and the source and application of funds

1

When asked to perform an audit to express an opinion on one or more specified elements, accounts, or items of a financial statement, the auditor

(1) may not describe auditing procedures applied.

(2) should advise the client that the opinion can be issued only if the financial statements have been audited and found to be fairly presented.

(3) may assume that the standards of reporting with respect to GAAP do not apply.

(4) should comply with the request only if they constitute a major portion of the

financial statements on which an auditor has disclaimed an opinion based on

an audit.

2

Which of the following is a prospective financial statement for general use upon

which an accountant may appropriately report?

(1) Financial projection

(2) Partial presentation

(3) Pro forma financial statement

(4) Financial forecast

4

Which of the following procedures would most likely be performed during an

engagement to compile the financial statements of a nonissuer?

(1) Read the financial statements and consider whether they are appropriate in form and free from obvious material errors

(2) Perform inquiry and analytical procedures

(3) Obtain a representation letter from management

(4) Send accounts receivable confirmations

1

Which of the following procedures would most likely be performed during the

engagement to review the annual financial statements of a nonissuer?

(1) Observation of inventory

(2) Confirmation of notes receivable

(3) Communication with the predecessor accountant

(4) Comparison of the current financial statements with prior period financial

statements

4

Key sections of the AICPA code of professional conduct (6)

Responsibilities, public interest, integrity, objectivity and independence, due care, and scope and nature of services

What is the rule of independence and why is it important

all members to be independent in fact and appearance

What are examples of non-audit servics and which ones can be provided along w/ audit services?

Tax services, pre approved by audit committee

What is an audit committee? What are their main responsibilities?

a select number of members of a company’s board of directors whose responsibilities include helping auditors remain independent of management

Describe what a cpa will need to disclose regarding their client if asked? (Rule 301 confidentiality)

Cannot give out any confidential information

What is a contingent fee

Fee is based on completed work

Can CPA’s advertise? what are the restrictions, if any?

they can but cannot provide false and or misleading ads

What are commissions and referral fees and when is it allowable to receive?

The fees you get when you refer a client to someone. its acceptable if you disclose it with your client that you will get a referral

Ramifications of the key cases that have shaped auditor’s legal liability

What is the meaning of the rule that requires the auditor be independent?

(1) The auditor must adopt a critical attitude during the audit.

(2) The auditor’s sole obligation is to third parties.

(3) The auditor may have a direct ownership interest in the client’s business if it is not material.

(4) The auditor must be without bias with respect to the client under audit.

4

Which of the following services can be offered to public company audit clients under

SEC requirements and the Sarbanes–Oxley Act?

(1) Tax services for executives involved in financial reporting

(2) Tax planning not involving tax shelters

(3) Internal audit outsourcing

(4) Bookkeeping and other accounting services

2

An auditor strives to achieve independence in appearance to

(1) comply with auditing standards related to audit performance.

(2) become independent in fact.

(3) maintain public confidence in the profession.

(4) maintain an unbiased mental attitude.

3

In which one of the following situations would a CPA be in violation of the AICPA

Code of Professional Conduct in determining the audit fee?

(1) A fee based on whether the CPA’s report on the client’s financial statements results in the approval of a bank loan.

(2) A fee based on the outcome of a bankruptcy proceeding.

(3) A fee based on the nature of the service rendered and the CPA’s expertise instead of the actual time spent on the engagement.

(4) A fee based on the fee charged by the prior auditor.

1

The AICPA Code of Professional Conduct states that a CPA shall not disclose any confidential client information obtained in the course of a professional engagement except with the consent of the client. In which one of the following situations would disclosure by a CPA be in violation of the Code?

(1) Disclosing confidential information in compliance with a subpoena issued by a court.

(2) Disclosing confidential information in order to properly discharge the CPA’s responsibilities in accordance with the profession’s standards.

(3) Disclosing confidential information to another accountant interested in purchasing the CPA’s practice.

(4) Disclosing confidential information during an AICPA-authorized peer review.

3

A CPA’s retention of client records as a means of enforcing payment of an overdue audit fee is an action that is

(1)not addressed by the AICPA Code of Professional Conduct.

(2) acceptable if sanctioned by the state laws.

(3) prohibited under the AICPA rules of conduct.

(4) a violation of generally accepted auditing standards.

3

The concept of materiality would be least important to an auditor when considering the

(1) adequacy of disclosure of a client’s illegal act.

(2) effects of a direct financial interest in the client on the CPA’s independence.

(3) discovery of weaknesses in a client’s internal control structure.

(4) types of evidence to use in testing accounts receivable.

2

According to the profession’s ethical standards, which of the following events may

justify a departure from GAAP?

I. New legislation

II. Conflicting industry practices

III. Evolution of a new form of business transaction

(1) I and II

(3) I and III

(2) II and III

(4) I, II, and III

3

Which of the following is not a provision of the Sarbanes–Oxley Act of 2002?

(1) The auditor of an issuer may not provide internal audit outsourcing services forthe issuer.

(2) Audit documentation must be maintained for five years.

(3)The lead and reviewing partners must rotate off the audit after five years.

(4)Tax services must be preapproved by the audit committee.

2

What are some defenses available to the auditor in defending against a lawsuit brought against the auditor for an audit failure

Lack of Duty to perform service, Nonnegligent performance, Contributory Negligence, absence of causal connection

Other Services - 2

Agreed upon procedures

Forecasts and projections

Which of the following best describes why an independent auditor is asked to express an opinion on the fair presentation of financial statements

a. The opinion of an independent party is needed because a company may not be objective with respect to its own financial statements

b. it is managements responsibility to seek available independent aid in the appraisal of the financial information shown in its financial statements

c. it is difficult to prepare financial statements that fairly present a company’s financial position, operations, and cash flows without the expertise of an independent auditor.

d. It is a customary courtesy that all stockholders of a company receive an independent report on management’s stewardship of the affairs of the business

A

b. Which of the following professional services is an attestation engagement?

(1) A consulting service engagement to provide computer-processing advice to a client

(2) The preparation of financial statements from a client’s financial records

(3) An income tax engagement to prepare federal and state tax returns

(4) An engagement to report on compliance with statutory requirements

4

c. Which of the following attributes is likely to be unique to the audit work of CPAs as

compared to the work performed by practitioners of other professions?

(1) Independence

(3) Due professional care

(2) Competence

(4) Complex body of knowledge

1

a. Operational audits generally have been conducted by internal auditors and governmen-

tal audit agencies but may be performed by certified public accountants. A primary

purpose of an operational audit is to provide

(1) a means of assurance that internal accounting controls are functioning as

planned.

(2) the results of internal examinations of financial and accounting matters to a

company’s top-level management.

(3) a measure of management performance in meeting organizational goals.

(4) aid to the independent auditor who is conducting the audit of the financial

statements.

3

Which of the following best describes the operational audit?

(1) It requires the constant review by internal auditors of the administrative controls

as they relate to the operations of the company.

(2) It concentrates on implementing financial and accounting control in a newly

organized company.

(3) It focuses on verifying the fair presentation of a company’s results of operations.

(4)It concentrates on seeking aspects of operations in which waste could be reduced

by the introduction of controls

4

Compliance auditing often extends beyond audits leading to the expression of opinions

on the fairness of financial presentation and includes audits of efficiency, economy,

effectiveness, and

(1) adherence to specific rules or procedures.

(2) accuracy.

(3) evaluation.

(4) internal control

1

Which of the following is considered an assurance engagement?

(1) Bookkeeping

(2) Preparation

(3) Compilation

(4) Audit

4

Which of the following engagements is most likely to be considered an operational audit?

(1) The auditor determines whether the organization is following provisions of laws

and regulations.

(2) The auditor examines information presented in an entity’s financial statements

to determine whether the financial statements are presented fairly in accordance

with the applicable financial reporting framework.

(3) The auditor evaluates the organization’s efficiency in processing payments.

(4) The auditor assists the client in preparation of financial statements.

3

In a financial statement audit, the auditor obtains a reasonable level of assurance

about whether the financial statements are free of material misstatement in order to

express an opinion. To obtain reasonable assurance, the auditor must

(1) have prior experience in the industry in which the audit client operates.

(2) examine all documents available that support the financial statements.

(3) obtain sufficient audit evidence.

(4) test controls around significant transaction cycles.

c

Subsequent to the date of the financial statements as part of their post-balance sheet

date audit procedures, a CPA learned that a recent fire caused heavy damage to one

of a client’s two plants; the loss will not be reimbursed by insurance. The newspapers

described the event in detail. The financial statements and footnotes as prepared by

the client did not disclose the loss caused by the fire.

Audit Report?

Adverse or Qualified opinion - Gaap departure

During the course of their audit of the financial statements of a corporation for the

purpose of expressing an opinion on the statements, a CPA is refused permission to

inspect the minutes of board of directors’ meetings that document significant deci-

sions of the board. The corporation secretary instead offers to give the CPA a certified

copy of all resolutions and actions involving accounting matters.

Audit Opinion?

Disclaimer

A CPA is engaged in the audit of the financial statements of a large manufacturing

company with branch offices in many widely separated cities. The CPA was not able

to count the substantial undeposited cash receipts at the close of business on the last

day of the fiscal year at all branch offices. As an alternative to this auditing procedure used to verify the accurate cutoff of cash receipts, the CPA observed that deposits in transit as shown on the year-end

bank reconciliation appeared as credits on the bank statement on the first business

day of the new year. The CPA was satisfied as to the cutoff of cash receipts by the use

of the alternative procedure.

Audit Report

Unmodified - standard wording

On January 2, 2024, the Retail Auto Parts Company received a notice from its pri-

mary supplier that effective immediately, all wholesale prices will be increased by

10 percent. On the basis of the notice, Retail Auto Parts revalued its December 31, 2023, inventory to reflect the higher costs. The inventory constituted a material proportion of total assets; however, the effect of the revaluation was material to current assets but not to total assets or net income. The increase in valuation is adequately disclosed in

the footnotes.

Audit Opinion?

Qualified - Gaap Departure

A CPA has completed the audit of the financial statements of a bus company for the

year ended December 31, 2023. Prior to 2023, the company depreciated its buses over

a 10-year period. During 2023, the company determined that a more realistic esti-

mated life for its buses was 12 years and computed the 2023 depreciation on the basis

of the revised estimate. The CPA is satisfied that the 12-year life is reasonable.

The company has adequately disclosed the change in estimated useful lives of its

buses and the effect of the change on 2023 income in a note to the financial statements.

Auditor Opinion?

Unmodified - standard wording

E lotions, Inc., is an online retailer of body lotions and other bath and body

supplies. The company records revenues at the time customer orders are placed on

the website, rather than when the goods are shipped, which is usually two days after

the order is placed. The auditor determined that the amount of orders placed but not

shipped as of the balance sheet date is not material.

Audit Opinion

Unmodified-standard writing

A number of frozen yogurt stores have opened in the last few years and your client,

YogurtLand, has experienced a noticeable decline in customer traffic over the past

several months that has caused you to have substantial doubt about YogurtLand’s

ability to continue as a going concern.

Auditor Opinion

Unmodified-Explanatory Paragraph

Intelligis Electronics is a manufacturer of advanced electrical components. During

the year, changes in the market resulted in a significant decrease in the demand for

their products, which are now being sold significantly below cost. Management re-

fuses to write off the products or to increase the reserve for obsolescence.

Auditor Opinion

Qualified opinion - GAAP Departure or Advers

In the last 3 months of the current year, Oil Refining Company decided to change

direction and go significantly into the oil drilling business. Management recognizes

that this business is exceptionally risky and could jeopardize the success of its exist-

ing refining business, but there are significant potential rewards. During the short

period of operation in drilling, the company has had three dry wells and no successes.

The facts are adequately disclosed in footnotes.

Auditor Opinion

Unmodified-standard wording

Your client, Harrison Automotive, has changed from straight-line to sum-of-the-years’

digits depreciation. The effect on this year’s income is immaterial, but the effect in fu-

ture years may be highly material. The change is not disclosed in the footnotes.

Auditor Opinion

Unmodified-standard wording

Circumstances prevent you from being able to observe the counting of inventory at

Brentwood Industries. The inventory amount is material in relation to Brentwood

Industries’ financial statements. But, you were able to perform alternative procedures

to support the existence and valuation of the inventory at year-end.

Auditor Opinion

Unmodified-standard opinion

Approximately 20 percent of the audit of Lumberton Farms, Inc., was performed by

a different CPA firm, selected by you. You have reviewed their audit files and believe

they did an excellent job on their portion of the audit. Nevertheless, you are unwilling

to take complete responsibility for their work.

Auditor Opinion

Unmodified-nonstandard