Intro to Financial Accounting Chapter 2

1/31

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

32 Terms

Debits and Credits

Record of increases and decreases in a specific asset, liability, stockholders' equity, revenue, or expense item.

Debit = "Left"

Credit = "Right"

Debit

An amount recorded on the left side of an account

Credit

An amount recorded on the right side of an account

Double-Entry System

A system that records in appropriate accounts the dual effect of each transaction. Recording done by debiting at least one account and crediting at least one other account. Debits must equal Credits.

Debit Balance

When the sum of Debit entries are greater than the sum of Credit entries

Credit Balance

When the sum of Credit entries are greater than the sum of Debit entries

Account

A record of increases and decreases in specific asset, liability, or stockholders' equity items.

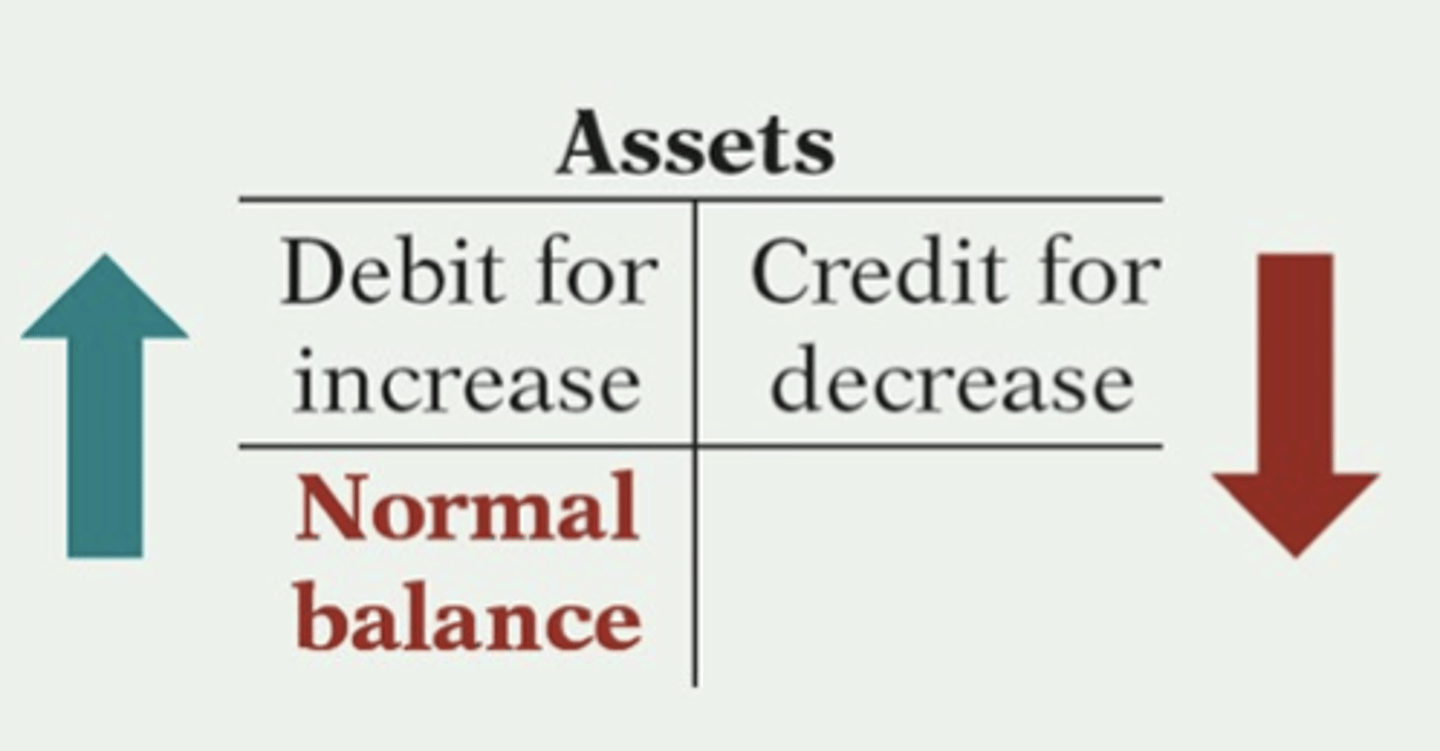

Assets

Debits should exceed credits

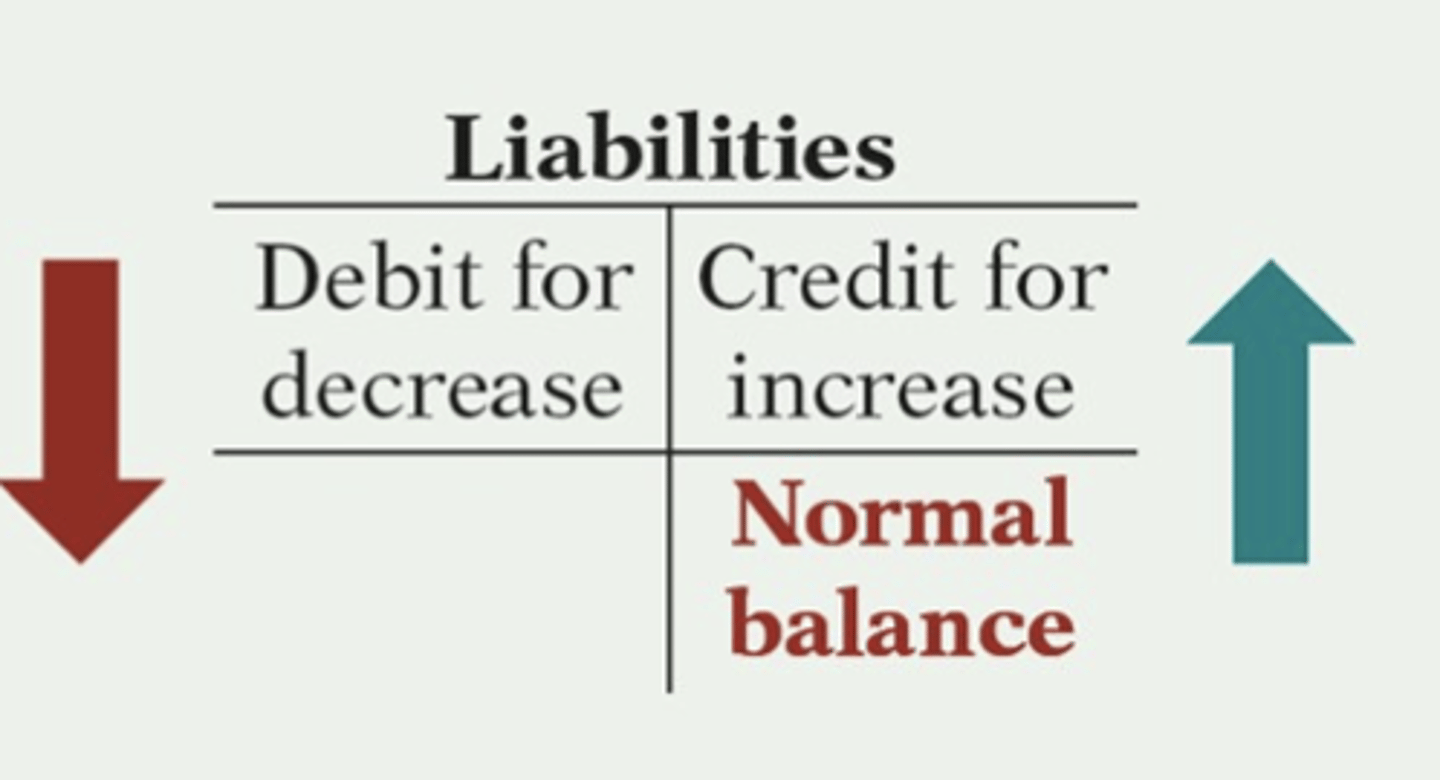

Liabilities

Credits should exceed debits.

Normal balance

Is on the increased side.

How owner's investments and revenues affect stockholders' equity

Increases stockholders' equity (credit).

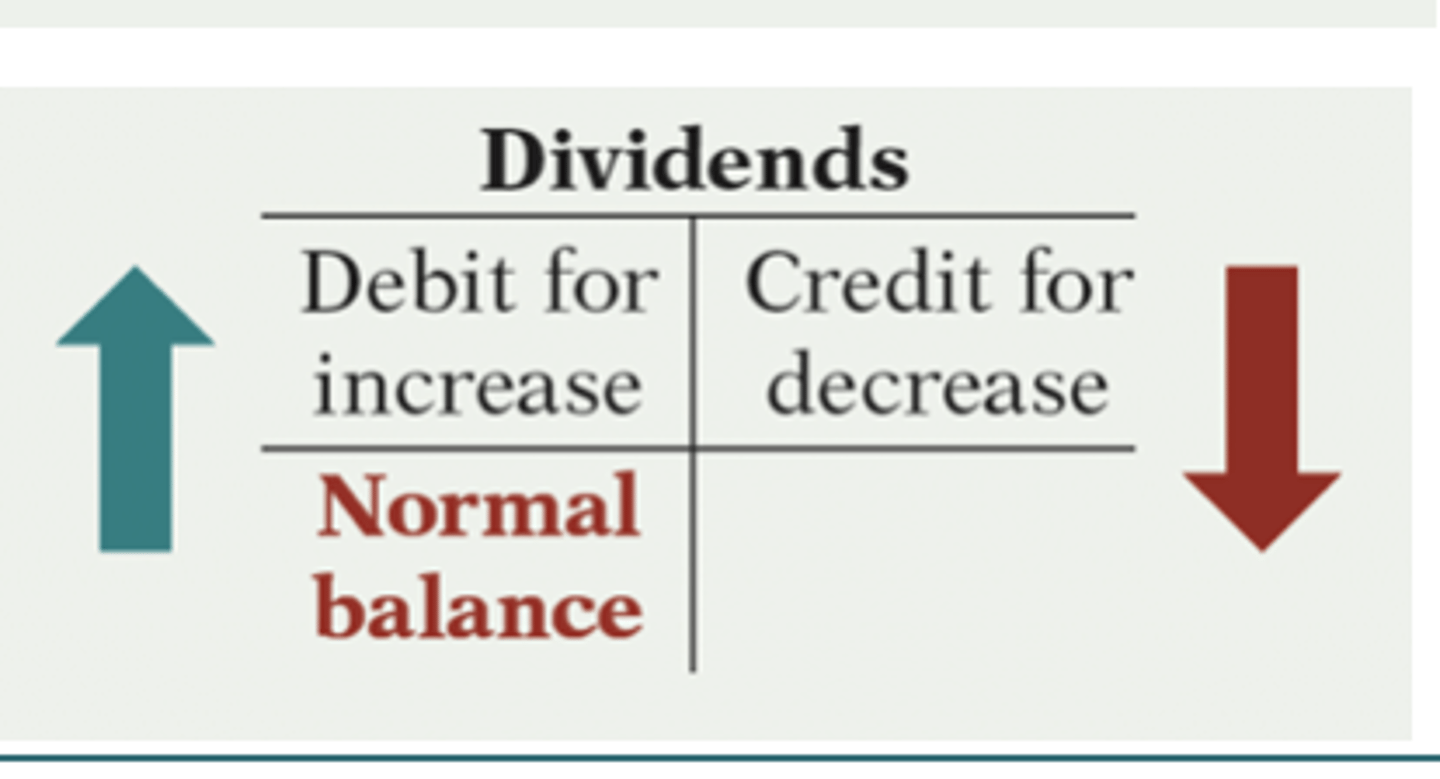

How dividends and expenses affect stockholders' equity

Decreases stockholders' equity (debit).

Purpose of earning revenues

To benefit the stockholders.

The effect of debits and credits on revenue accounts is the same as...

...their effect on stockholders' equity.

Expenses decrease...

...stockholders' equity.

Assets (Debit vs Credit)

Debit: +

Credit: -

Liabilities (Debit vs Credit)

Debit: -

Credit: +

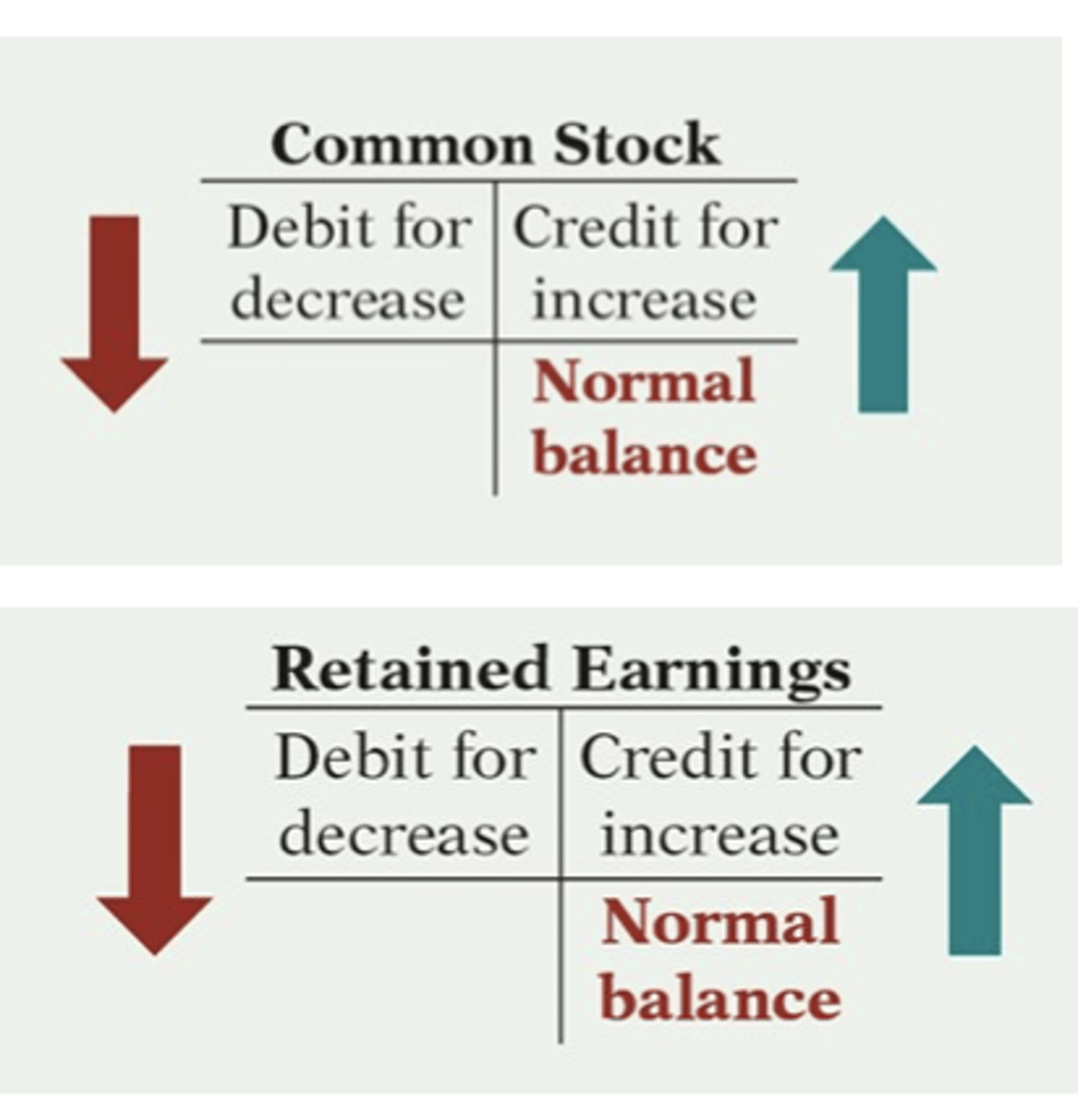

Common Stock (Debit vs Credit)

Debit: -

Credit: +

Retained Earnings (Debit vs Credit)

Debit: -

Credit: +

Revenues (Debit vs Credit)

Debit: -

Credit: +

Expenses (Debit vs Credit)

Debit: +

Credit: -

Dividends (Debit vs Credit)

Debit: +

Credit: -

The Recording Process

1. Analyze each transaction in terms of its effect on the accounts.

2. Enter the transaction information in a journal.

3. Transfer the journal information to the appropriate accounts in the ledger.

The Journal

Book of original entry with the transactions recorded in chronological order.

Journal's contributions to the recording process:

1. Discloses in one place the complete effects of a transaction.

2. Provides a chronological record of transactions.

3. Helps to prevent or locate errors because the debit and credit amounts can be easily compared.

Journalizing

Entering transaction data in the journal.

Ledger

(or general ledger) is the central, organized record of a business's financial transactions. It serves as a master book where chronologically tracked entries are sorted into specific accounts (assets, liabilities, equity, revenue, and expenses) to form the foundation of your financial statements.

Posting

the process of transferring recorded financial transactions from a chronological journal to the specific accounts in the general ledger.

Three-Column Form of Account

A form with columns for debit, credit, and balance amounts in an account.

Chart of Accounts

A list of accounts and the account numbers that identify their location in the ledger.

Steps of the Recording Process

1. Determine what type of account is involved.

2. Determine what items increased or decreased and by how much.

3. Translate the increases and decreases into debits and credits.

Trial Balance

A list of accounts and their balances at a given time.