MFI Unit 4- Microfinance issues and policies

1/4

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

5 Terms

Sustainability in microfinance

The organisational sustainability depends upon the ability of the MFI to cover it's cost by bringing down the operating cost and designing products which can be affordable to the client's. MFI will be sustainable if its access to fund is higher, if products are affordable, cost of operation is less, client dropout is less and outreach is high.

Sustainable interest rate formula

R = FC+LL+OE+M-I/

1-LL

R= Sustainable interest rate that should be charged

FC=Financial Cost(cost of borrowing, fund used to raise the organisation)

LL=Loan Losses (losses that can be incurred)

OE/OC= Operating expenses/cost

M=Margin for future growth

I= Investment income

New market

New market is a market where less financial products and services are available. The demand for financial products and services are also less. In new markets, MFIs focus on development of appropriate products and creation of a market for microfinance products.

For an MFI, market research is very necessary .

Methods :

Personal discussion

Participatory rural appraisal

Rapid rural appraisal

Questionnaire

Secondary data

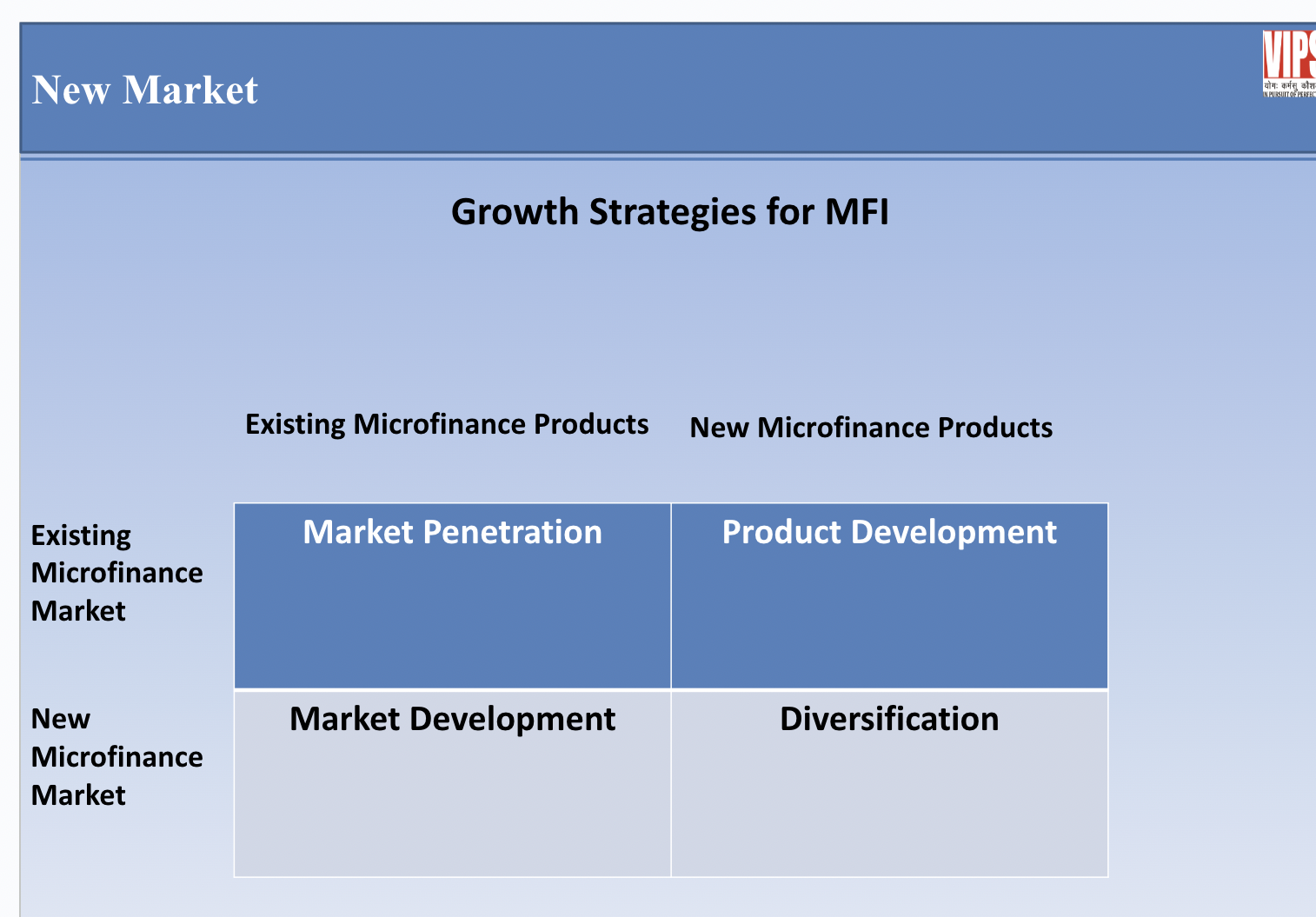

Growth Strategies for MFI in microfinance sector :

Market Penetration - In-depth knowledge about market

Market Development - New markets, developing and developed

Product Development – Modifying the existing products

Diversification - Different products and services through different portfolio

what are the 4ps of marketing?

In microfinance, the traditional 4 Ps of Marketing (Product, Price, Place, Promotion) are adapted to address the unique needs of low-income, often unbanked populations. Because microfinance is a service-based sector with a strong social mission, the marketing mix focuses on accessibility, affordability, and trust.

1. Product (The Financial Service)

In microfinance, the "Product" is not just a loan; it is a tool for poverty alleviation. MFIs must design products that match the irregular and small cash flows of the poor.

Micro-Credit: Tailored loans like "Consumption Loans" for emergencies or "Income Generating Loans" for small businesses.

Micro-Savings: Products with no minimum balance requirements to encourage the habit of saving.

Micro-Insurance: Bundled life or crop insurance to protect against external shocks.

Flexible Terms: Features like "Grace Periods" (moratoriums) and "Joint Liability" (group guarantees) instead of physical collateral.

2. Price (The Cost of Borrowing)

Pricing in microfinance is sensitive. While MFIs have high operational costs (due to field visits), the price must remain ethical and competitive.

Interest Rates: Often expressed as a Declining Balance Rate or Flat Rate. Transparency is key to prevent "predatory" perceptions.

Transaction Costs: Beyond interest, this includes processing fees, insurance premiums, and even the "opportunity cost" for the borrower (time spent in group meetings).

Prompt Payment Incentives: Discounts or rebates for clients who pay on time, which acts as a "loyalty price."

3. Place (Distribution & Accessibility)

"Place" refers to how and where the client accesses the service. For the rural poor, distance is a major barrier to financial inclusion.

Doorstep Banking: Loan officers (field staff) visiting the borrower’s home or village to collect repayments.

Agent Banking: Partnering with local grocery stores or pharmacies to act as "mini-branches" for deposits and withdrawals.

Digital Banking: Using mobile apps or USSD codes for "cashless" disbursements and collections, significantly reducing the need for physical branches.

Group Meeting Points: Utilizing community centers or a group leader's house as the primary point of contact.

4. Promotion (Communication & Awareness)

Promotion in microfinance is less about flashy TV ads and more about trust-building and financial literacy.

Personal Selling: The loan officer acts as a "brand ambassador," building deep relationships with the community.

Word of Mouth: Since trust is paramount, positive testimonials from successful group members are the most effective promotional tool.

Financial Literacy Programs: MFIs often promote their services by holding "educational workshops" on debt management, which builds the MFI's reputation as a "helpful partner" rather than just a lender.

Bilingual/Local Language Material: Using flyers, posters, and radio ads in local dialects to ensure the message is understood by non-literate populations.

technology role and challenges

Technology, innovation, and knowledge have become the key drivers of economic growth today. The effective absorption and utilization of data and information is extremely important for any sector at various developmental stages.

ROLE

a) Mobile banking :

Mobile banking is a popular method of technologically oriented banking. Also called as M-Banking or SMS banking. Mobile banking allows the user to log into his account from a cell phone, and then use the phone to make payments, check balance, transfer money between accounts, view monthly statements and etc.

This service will provide convenience to consumers by not having to go to a bank branch physically logon from their home computer or make a phone call.

But one can beware of security problems that may arise with mobile banking service.

b) ATM :

This facility enables the population to have banking services without physical direct recourse to the bank premise. ATMs with operating instructions in vernacular languages facilitate the access poor people with reading ability.

ATMs with voice recognition for the illiterates for transactions relating to savings, credit and payment services. Biometric enabled ATMs to bring more illiterate people to the banking fold. Mobile teller low cost ATMs in the rural and remote areas also facilitate poor people.

c) Phone banking :

Phone banking is the process of conducting banking transactions over a secure telephone network was catching the fancy of customers. A majority of common transactions including balance enquiry, requests for cheque books, insurance, loans, mutual funds and other investments could be done through an Automated Interactive Voice driven Menu or a Customer Service Associate. Customers have the convenience of calling up their banks from the comfort of their homes or offices or from their mobile phones while on the move.

This is an efficient system which provides prompt solutions to customer complaints and generates high customer satisfaction levels when utilized effectively.

Customers are at times put off by the queuing and waiting times and impolite and slow customer service associates.

d) Internet banking :

Internet banking or e-banking is the latest in the series of technological advancements in the delivery of banking products and financial services.

In Internet banking any inquiry or transaction is processed online without any reference to the branch (anywhere banking) at any time.

Now it has become the cheapest way of providing financial services in many developing countries.

PROBLEMS in the implementation of technology

An introduction of technology necessarily brings with it problems in the education and acceptance by microfinance customers.

Problems also arise in the implementation of technological infrastructure.

Many of the areas that microfinance institutions serve do not have adequate electrical or communication wiring.

When a microfinance institution attempts to introduce a sophisticated or unfamiliar technology into its business structure, an important consideration is the level of knowledge the average customer possesses on that technology

The lack of infrastructure - in areas such as transportation, communication, and electric wiring - is a major hurdle for MFIs attempting sustainability.

PROBLEMS in the adoption of technology

Lack of skilled staff to support the MIS.

Lack of local IT support and services environment for after-sale service, training and support.

Lack of budget to procure and update/upgrade technology.

Very basic technology needs, which are not addressed well by existing sophisticated solutions.

High need for localization (language of interface, iconography etc)

Gender issues

through ppt