LO8–3 Account for employee and employer payroll liabilities.

1/39

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

40 Terms

Why are payroll liabilities significant for labor‑intensive companies?

Because wages, taxes, and benefits make up a large portion of their current liabilities.

Why is an employee’s take‑home pay less than their salary?

Because the employer must withhold:

✔ Federal income tax

✔ State income tax

✔ Social Security (6.2%)

✔ Medicare (1.45%)

✔ Employee insurance premiums

✔ Employee retirement contributions

These are liabilities for the employer until they send the money to the IRS, insurance company, etc.

Two sides of payroll liabilities

Employee costs (taken OUT of the employee’s paycheck): These reduce the employee’s take‑home pay.

Employer costs (ADDED ON TOP of the employee’s salary): These increase the employer’s expenses.

What are the required employee payroll withholdings?

Federal income tax, state income tax, Social Security tax, and Medicare tax.

What optional amounts may employees have withheld?

Insurance premiums, retirement contributions, and charitable donations.

What is the employee’s FICA tax rate?

7.65% (6.2% Social Security + 1.45% Medicare).

6.2% Social Security (only up to $168,600 in 2024)

1.45% Medicare (no limit)

So employees pay 7.65%.

If someone earns above the Social Security cap, they stop paying the 6.2% part and only pay the 1.45%.

What is the Social Security wage base in 2024?

$168,600 — Social Security tax applies only up to this amount.

How is FICA applied for employees earning above the wage base?

7.65% on the first $168,600, then 1.45% withheld on the remaining amount earned during the rest of the year.

How does the employer record employee withholdings?

As liabilities until paid to the government or benefit providers.

What FICA taxes must the employer pay?

The employer must match the employee’s 7.65% FICA tax.

What is the total FICA collected by the government per employee?

15.3% (7.65% employee + 7.65% employer).

Total = 15.3% going to the government.

What do employers end up paying after FICA is collected?

✔ FUTA (Federal unemployment tax)

6.0% on first $7,000 of wages

Usually reduced to 0.6% after credits

✔ SUTA (State unemployment tax)

Varies by state and company history

✔ Employer insurance contributions

(health, dental, life, disability)

✔ Employer retirement contributions

These are expenses for the employer.

This is why a $5,000 salary can cost the employer over $6,000.

What is FUTA?

Federal Unemployment Tax Act — employer pays 6.0% on the first $7,000 of wages.

This rate can be reduced by a maximum 5.4% tax credit for companies making payments on time and in full to their state unemployment programs, so the net federal rate often is only 0.6%.

Why is FUTA often only 0.6%?

Employers receive up to a 5.4% credit for paying state unemployment taxes on time.

What is SUTA?

State unemployment tax; rate and wage base vary by state and employer history.

Do employees pay unemployment taxes?

No — only employers pay FUTA and SUTA.

What are fringe benefits?

Employer-paid benefits such as insurance and retirement contributions.

Many companies provide additional fringe benefits specific to the company or the industry. For instance, a fringe benefit in the airline industry is free flights for employees and their families. Some fringe benefits, like free skiing for employees of a ski resort, are usually not recorded in the accounting records.

Examples:

Employer-paid insurance

Employer-paid retirement

Free flights (airlines)

Free skiing (ski resorts)

Some are recorded in accounting, some aren’t.

How are employer-paid fringe benefits recorded?

As Salaries Expense with a credit to Fringe Benefits Payable.

Debit: Salaries Expense

Credit: Fringe Benefits Payable

Why do employer payroll costs exceed the employee’s salary?

Employers must pay matching FICA, unemployment taxes, and employer benefit contributions.

Example: If an employee earns $5,000 per month, why might employer cost exceed $6,000?

Because employer FICA, unemployment taxes, insurance, and retirement contributions add to total cost.

What is a common mistake people make about FICA?

Thinking only employees pay it — employers must match the full amount.

What happens to withheld amounts?

They remain liabilities until the employer remits them to the government or benefit providers.

What is Hawaiian Travel Agency’s total January payroll?

$100,000 for 20 employees.

Employee withholdings

Money your employer takes out of your paycheck BEFORE giving it to you.

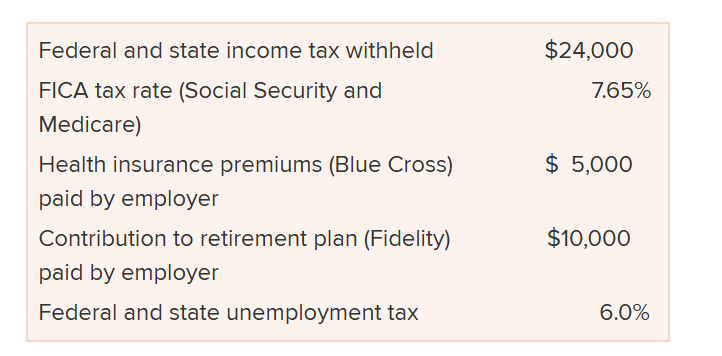

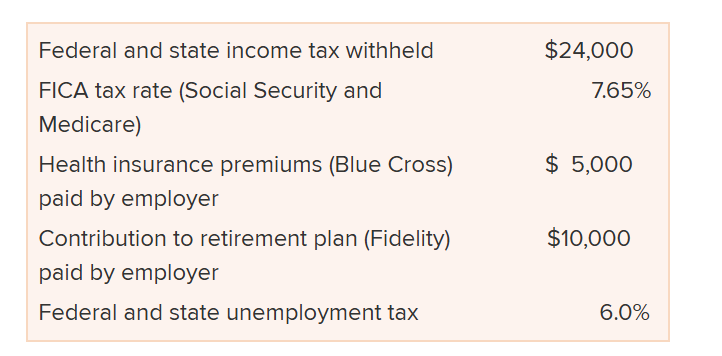

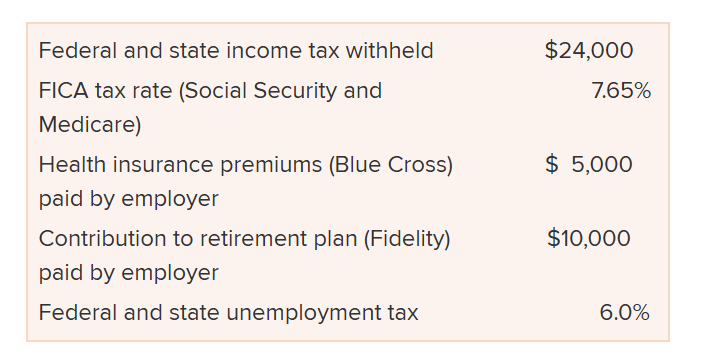

How much federal & state income tax is withheld from employees?

$24,000.

What is the FICA tax rate applied to employee wages?

7.65% (6.2% Social Security + 1.45% Medicare).

How much FICA tax is withheld from employees on $100,000 payroll?

$7,650 (0.0765 × $100,000).

What employer‑paid fringe benefits does Hawaiian Travel Agency provide?

$5,000 health insurance + $10,000 retirement contributions = $15,000 total.

What is the unemployment tax rate?

6.0% of wages.

Journal entry to record employee salary expense & withholdings (Jan 31)

Debit: Salaries Expense 100,000

Credit: Employee Income Tax Payable 24,000

Credit: FICA Tax Payable 7,650

Credit: Salaries Payable 68,350

How is Salaries Payable calculated?

100,000 − 24,000 − 7,650 = 68,350 (amount owed to employees after withholdings)

Journal entry to record employer‑provided fringe benefits (Jan 31)

Debit: Salaries Expense (fringe benefits) 15,000

Credit: Fringe Benefits Payable (Blue Cross) 5,000

Credit: Fringe Benefits Payable (Fidelity) 10,000

What are fringe benefits?

Employer‑paid benefits such as insurance and retirement contributions.

How much employer FICA tax does Hawaiian Travel Agency owe?

$7,650 (same 7.65% as employees).

How much unemployment tax does the employer owe?

$6,000 (0.06 × $100,000)

Journal entry to record employer payroll taxes (Dec 31)

Debit: Payroll Tax Expense 13,650

Credit: FICA Tax Payable 7,650

Credit: Unemployment Tax Payable 6,000

Total employer cost beyond the $100,000 salary

$28,650 (15,000 fringe benefits + 13,650 employer payroll taxes).

Why is FICA Tax Payable the same for employees and employer?

Because the employer must match the employee’s 7.65% FICA tax.

What happens to withheld amounts?

They remain liabilities until paid to government agencies or benefit providers.

Key point about payroll costs

Employees’ paychecks are reduced by withholdings; employers incur additional payroll taxes and benefit costs.