Chapter 1

1/38

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

39 Terms

What is auditing?

gathering and examining evidence to determine whether information is accurate and follows certain rules or standards.

“Auditing is the accumulation and evaluation of evidence about information to determine and reporting on the degree of correspondence between the information and established criteria.”

Who hires the auditor for public and private companies?

Public - Public company audit committee

Private - Management

What is an independent auditor?

A neutral outside accountant with no bias or personal interest in the company.

Must be objective and unbiased

Cannot have conflicts of interest

Independence makes the audit trustworthy

Usually a CPA firm

What is the purpose of an audit of financial statements?

To confirm that are:

fairly presented

in all material respects

according to GAAP

“The objective of the ordinary audit of financial statements by the independent auditor is the expression of an opinion on the fairness with which they present, in all material respects, financial position, results of operations, and its cash flows in conformity with generally accepted accounting principles”

What is the auditor’s report and why is it needed?

A document issued by the independent auditor that states:

whether the financial statements are fairly presented

whether they follow GAAP

whether the audit was conducted according to GAAS

It is the auditor’s written conclusion about whether the financial statements are reliable and follow GAAP.

“The auditor's report is the medium through which he expresses his opinion or, if circumstances require, disclaims an opinion. In either case, he states whether his audit has been made in accordance with generally accepted auditing standards. These standards require him to state whether, in his opinion, the financial statements are presented in conformity with generally accepted accounting principles and to identify those circumstances in which such principles have not been consistently observed in the preparation of the financial statements of the current period in relation to those of the preceding period.”

What are the outcomes? (expression of opinions)

Unqualified opinion (“clean opinion”) → statements look good

Qualified opinion → mostly okay, with issues

Adverse opinion → statements are misleading

Disclaimer of opinion → auditor cannot give an opinion

What does an auditor opinion provide?

They give reasonable assurance

Main goal is to state whether statements are reliable

Opinion is based on audit evidence

Can a auditor grantee financial statements accuracy?

No

Auditors only provide reasonable assurance, not a guarantee. Their opinion is based on the audit evidence obtained, and users use the audit report to help evaluate the reliability of the financial statements.

What is reasonable assurance?

A high, but not absolute, level of assurance to allow an auditor to detect a material misstatement.

What is the difference between auditing and accounting?

Accounting involves preparing and recording a company’s financial information, such as transactions and financial statements.

Auditing is the independent examination of that information to determine whether it is accurate and follows GAAP.

In simple terms, accountants create the financial statements, while auditors verify and evaluate them.

Accounting is the…

– Recording, classifying and summarizing of economic events for the purpose of providing financial information used in decision making.

Auditing is the…

– Determining whether recorded information properly reflects the economic events that occurred during the period."

Who are the users for accounting information & audit information?

Users of Accounting Information

Management

Investors/shareholders

Creditors/lenders

Banks

Government agencies (IRS, SEC)

Employees

Purpose:

Used to make business and financial decisions.

Users of Audits

Investors

Banks/lenders

Creditors

Regulators

Outside users of financial statements

Purpose:

They use the auditor’s opinion to decide whether the financial statements are trustworthy and fairly presented

What is evidence auditors use?

Evidence is any information the auditor uses to determine whether the information being audited follows the established criteria (usually GAAP).

Evidence is the proof auditors collect to support their opinion.

To:

verify accuracy

detect errors or fraud

support their audit opinion

What are some different types of evidence?

Invoices

Receipts

Bank statements

Contracts

Checks

Financial records

Confirmations from banks/customers

Physical inspection of assets

Observations

Calculations/recalculations

Interviews/inquiries with employees

What criteria do auditor use to evaluate evidence?

For financial statements:

US: GAAP

International: IFRS

For internal controls audits:

COSO (Committee of sponsoring organizations)

What is the definition of opine? (probably not important but i didn’t know what this meant)

To give a professional opinion or judgment.

“Auditors opine on whether the financial statements conform with GAAP”

What is the differences between financial accounting and auditing?

Financial:

Usually objective (GAAP)

Report to CFO or Controller (upper management)

Answer questions about companies financial results

Auditing:

Usually subjective (GAAS)

Reports to Board (above upper management)

Asks questions about companies financial results

What are the 2 must have qualities for an auditor?

Independence

Auditor has to stay independent and neutral from the client—if they’re biased or too close, the audit loses trust even if they’re technically skilled.

Competence

The audit is to be performed by a person or persons having adequate technical training and proficiency as an auditor. (AS 1010.01)

Independence - This standard requires that the auditor be independent; aside from being in public practice (as distinct from being in private practice), he must be without bias with respect to the client since otherwise he would lack that impartiality necessary for the dependability of his findings, however excellent his technical proficiency may be. (AS 1005.02)

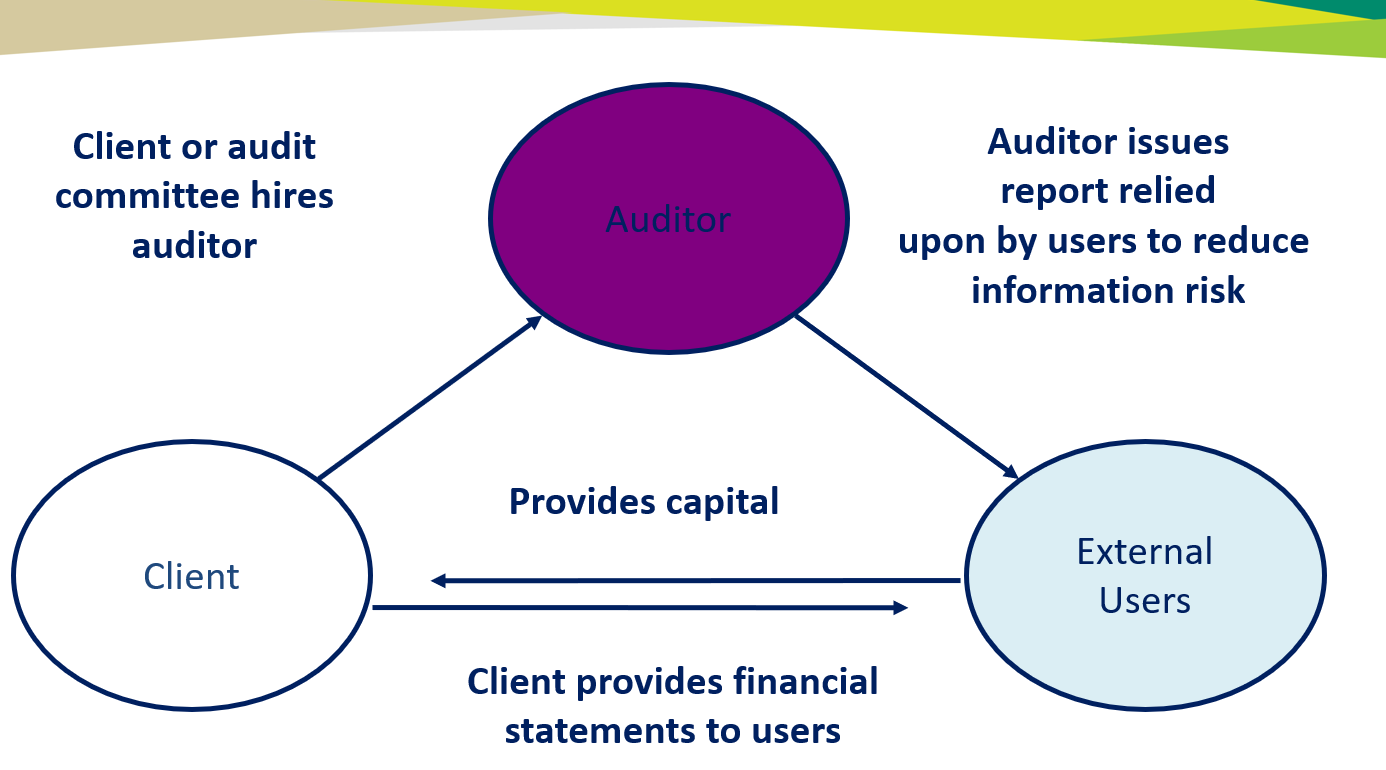

Relationship

Potential risk:

The External Users (investors, banks, creditors) provide financial capital to the Client (the company/management) so the company can grow and operate.

In return, the Client provides financial statements to the users to show how their money is being spent.

External users are naturally skeptical. Because management's job, bonuses, and reputation depend on good performance, they have a natural incentive to make the financial statements look as perfect as possible. (INFORMATION RISK)

Solution:

To build trust, the client (specifically the independent audit committee on behalf of shareholders) hires an objective, external Auditor to review the books.

The auditor gathers evidence, tests internal controls, and verifies the client's financial records against GAAP or IFRS standards.

The auditor issues an official Audit Opinion (the report) directly to the external users.

What is information risk?

Information risk is the risk that the financial information upon which a business decision is made is inaccurate, incomplete, or unreliable

External users rely on financial information, so relying directly on clients (which the information is based on), leads to the possibility of inaccurate, incomplete, or unreliable information

Auditors are there to reduce _____ ___.

Information Risk

What are causes of information risk?

Remoteness of Information

Biases & Motives of the Provider

Voluminous Data

Complex Exchange Transactions

Remoteness of Information (Cause of Information Risk)

Decision-makers are separated from day-to-day operations. They can't personally verify the data, so they must rely on reports that might be distorted.

Biases & Motives of the Provider (Cause of Information Risk)

Management prepares the financials and has a conflict of interest. They have an incentive to manipulate or overstate numbers to protect their bonuses and jobs.

Voluminous Data (Cause of Information Risk)

Large companies process millions of transactions. The sheer volume increases the likelihood that honest errors or improper recordings slip through.

Complex Exchange Transactions (Cause of Information Risk)

Modern business transactions (like derivatives or complex mergers) are highly complicated and difficult to record correctly, even for honest accountants.

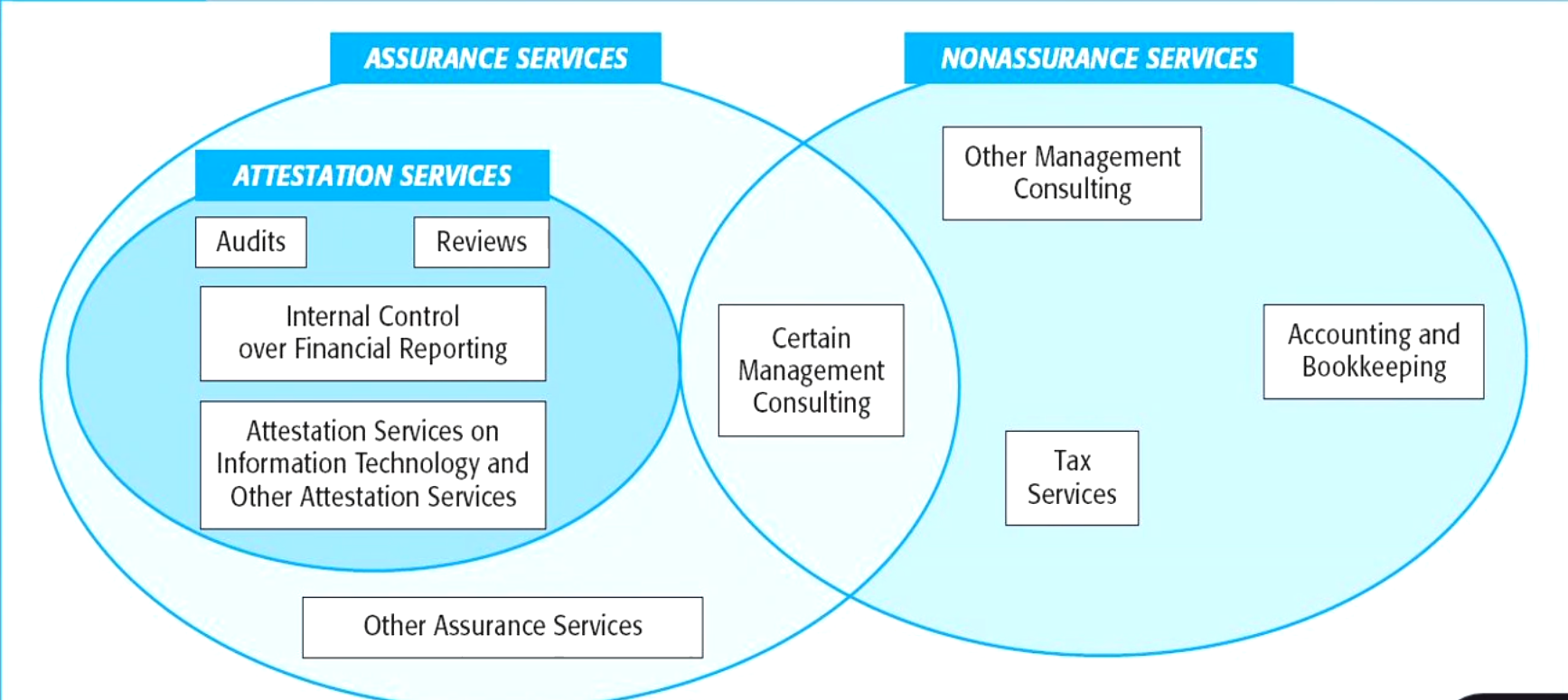

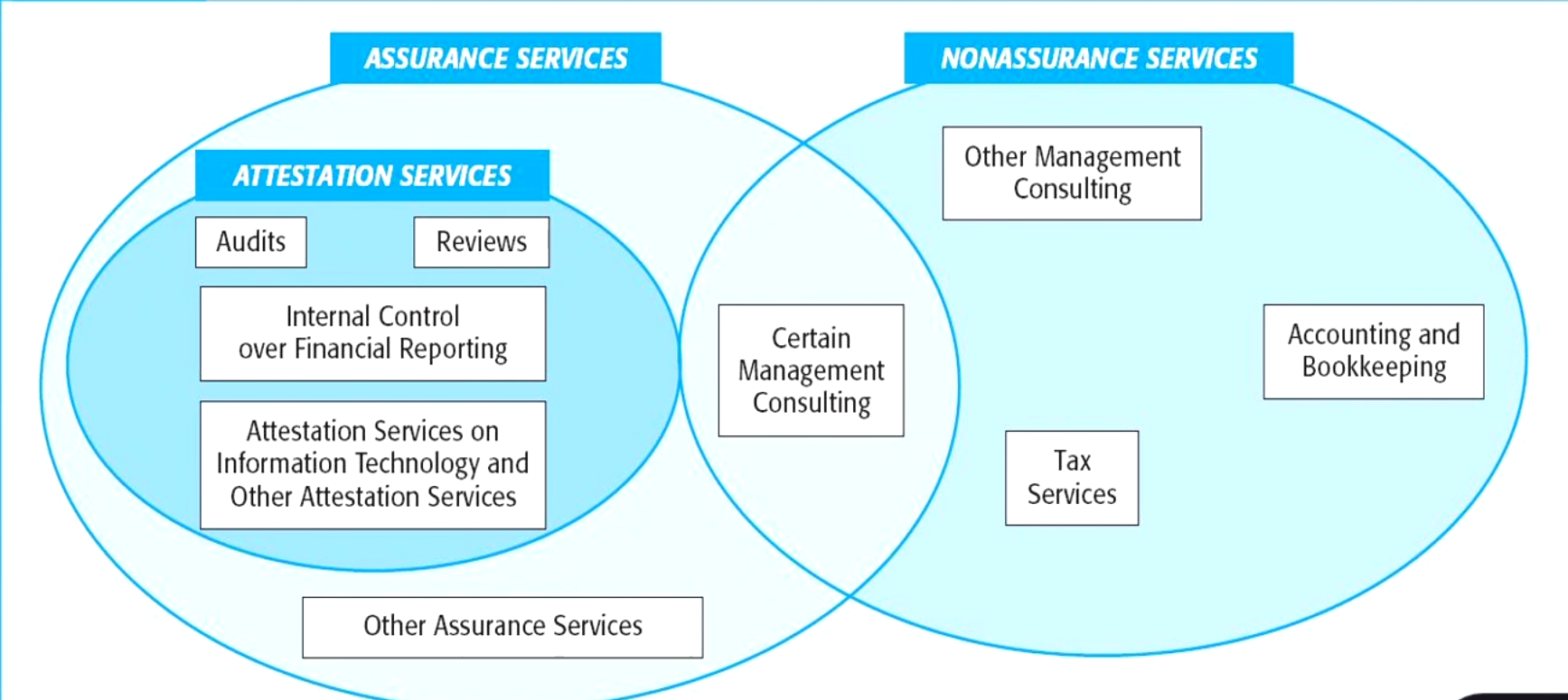

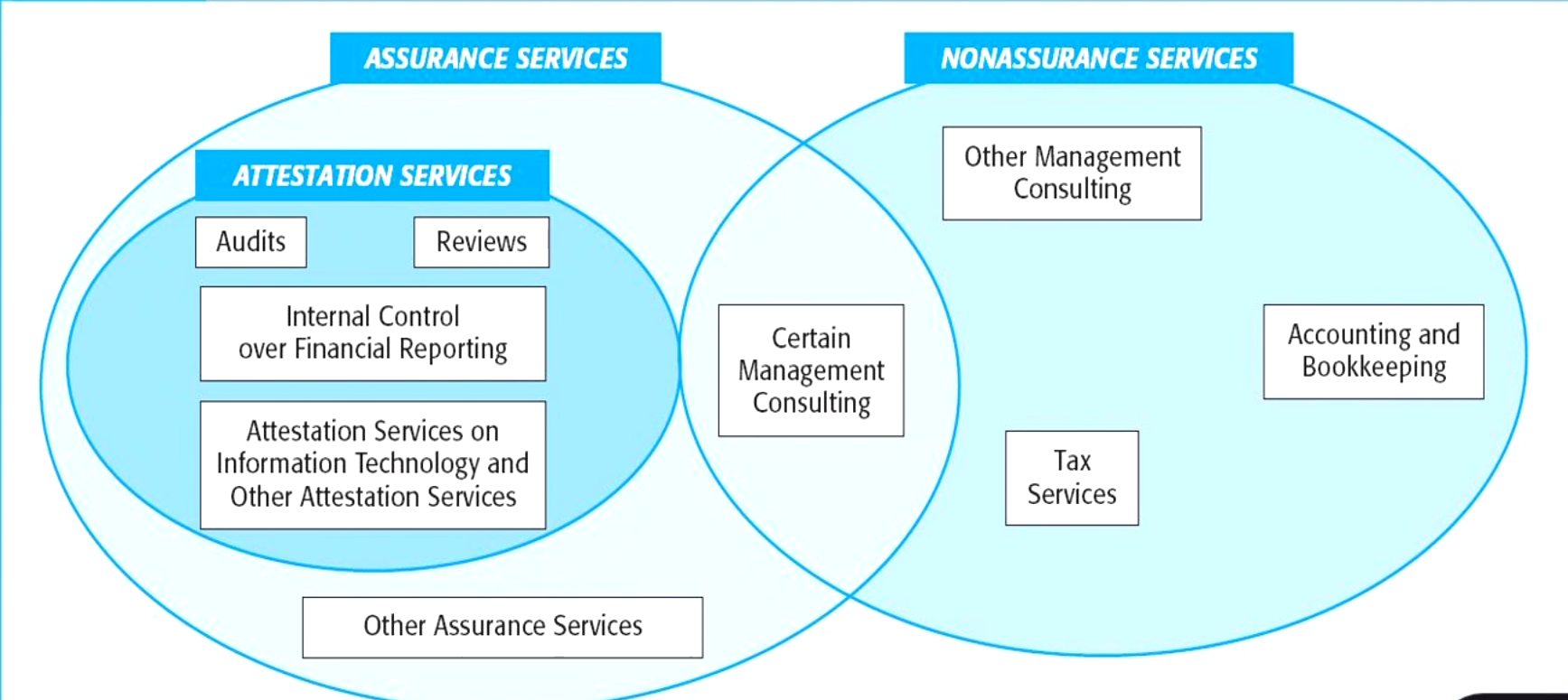

What are assurance services?

Assurance services are independent professional services that improve the quality of information, or its context, for decision-makers.

Can be performed by CPA’s or other professionals

No formal report is required

A broad category of services designed to improve the quality of decision making by improving confidence in the information on which decisions are made.

In broad terms not just for audit

What are attestation services?

Audit is inside attestation services which is inside assurance services

Attestation services are a specific type of assurance service. To "attest" means to witness something and confirm it is true.

Sub-category of assurance services

Requires independence

Result in a report

An engagement in which a practitioner is engaged to issue or does issue a written communication that expresses a conclusion about the reliability of a written assertion that is the responsibility of another party. (AICPA)

What are non-assurance services?

Goal is to generate a recommendation to management

Accounting and bookkeeping services

Tax services

Management consulting services

Can audit perform both assurance and non assurance services for the same client?

NO!

but

They can also provide tax services ONLY when approval is given by the audit committee

What the the 9 prohibited activates that auditors can not do at the same time as an audit?

bookkeeping or other services related to the accounting records or financial statements of the audit client;

financial information systems design and implementation;

(appraisal or valuation services, fairness opinions, or contribution-in-kind reports;

actuarial services;

internal audit outsourcing services;

management functions or human resources;

broker or dealer, investment adviser, or investment banking services;

legal services and expert services unrelated to the audit; and

any other service that the Board determines, by regulation, is impermissible.

What the the services auditors are allowed to do at the same time as an audit?

Anything that is not listed 1-9 and IS APPROVED by the audit committee of the issuer

A registered public accounting firm may engage in any non-audit service, including tax services, that is not described in any of paragraphs (1) through (9) of subsection (g) for an audit client, only if the activity is approved in advance by the audit committee of the issuer

What are the 3 main types of audit?

Operational

Compliance

Financial Statement

Operational (type of audit)

A review of any part of an organization's operating procedures to evaluate efficiency (cost/time) and effectiveness (meeting goals).

Management's Goals / Benchmarks

Ex: An audit evaluating whether a package delivery company can route trucks faster to reduce fuel costs and save time.

Compliance (type of audit)

An audit to determine whether the entity is following specific rules, laws, regulations, or covenants set by a higher authority.

Laws / Regulations / Contracts

Ex: Hospital get audited to make sure they are following HIPPA

Financial Statement (type of audit)

Determines whether financial statements are stated in accordance with specified criteria.

GAAP / IFRS

Ex: An audit checking a retail company's balance sheet and income statement to prove to a bank that their profit numbers are accurate.

Do you think users of audit reports view each type of audit as equally important?

No, it all depends on the user and what is most valuable to them.

External Users (Investors, Banks, Creditors) - Financial Statement Audits

Internal Users (Management, Board of Directors) - Operational Audits

Internal Users (Management, Board of Directors) - Compliance Audits

What are some different types of auditors?

CPA

Governmental accountability office auditors

Internal Revenue agents

Internal auditors

What are the 3 requirements for becoming a CPA?

150 credit hours

Taking exams

Audit and Attestation (4 hours)

Financial accounting and reporting (3 hours)

Regulation (3 hours)

Business Environment and concepts (3 hours)

Experience

Private company auditors report on ____ ____, public company auditors report on ____ _____ and ____ _____.

Financial statements

Financial statements &

Internal control