SOA Exam FM Master Review Flashcards

1/38

Earn XP

Description and Tags

A comprehensive set of vocabulary flashcards covering interest theory, annuities, loans, bonds, duration, and immunization for the SOA Exam FM.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

39 Terms

Effective Rate per Period (Nominal Rate Trick)

For a nominal rate i(m), the effective rate per period is expressed as i(m)/m, not i(m).

Accumulation Function

Simple Interest

</p><p>a(t)=1+it</p><p>

Compound Interest

</p><p>a(t)=(1+i)t</p><p>

Force of Interest

</p><p>a(t)=eδt</p><p>

Discount Function

</p><p>v(t)=a(t)1</p><p>

Accumulation Factor from Time \(s\) to Time \(t\)

</p><p>a(s)a(t)</p><p>

Discount Factor from Time \(t\) to Time \(s\)

</p><p>a(t)a(s)</p><p>

Interest Earned During Year \(n\)

</p><p>In=a(n)−a(n−1)</p><p>

Effective Interest Rate During Year \(n\)

</p><p>in=a(n−1)a(n)−a(n−1)</p><p>

Effective Discount Rate During Year \(n\)

</p><p>dn=a(n)a(n)−a(n−1)</p><p>

Relationship Between Effective Interest and Effective Discount

</p><p>d=1+ii</p><p>

</p><p>i=1−dd</p><p>

\section*{Special Case: Simple Interest}

Accumulation Function

</p><p>a(t)=1+it</p><p>

Interest Earned During Any Year

</p><p>In=i</p><p>

Effective Interest Rate During Year \(n\)

</p><p>in=1+i(n−1)i</p><p>

Effective Discount Rate During Year \(n\)

</p><p>dn=1+ini</p><p>

\section*{Special Case: Compound Interest}

Accumulation Function

</p><p>a(t)=(1+i)t</p><p>

Interest Earned During Year \(n\)

</p><p>In=i(1+i)n−1</p><p>

Effective Interest Rate During Every Year

</p><p>in=i</p><p>

Effective Discount Rate During Every Year

</p><p>dn=d=1+ii</p><p>

\section*{Force of Interest Relationships}

Accumulation Function

</p><p>a(t)=eδt</p><p>

Discount Function

</p><p>v(t)=e−δt</p><p>

Convert Force to Effective Interest

</p><p>i=eδ−1</p><p>

Convert Effective Interest to Force

</p><p>δ=ln(1+i)</p><p>

Accumulation Over \(t\) Years Using Force

</p><p>(1+i)t=eδt</p><p>

\section*{Useful FM Facts}

Present Value at Time 0 of Amount \(A\) at Time \(t\)

</p><p>PV=Av(t)</p><p>

Future Value at Time \(t\) of Amount \(A\) at Time 0

</p><p>FV=Aa(t)</p><p>

Accumulation Function Must Satisfy

</p><p>a(0)=1</p><p>

For Compound Interest

</p><p>a(t+s)=a(t)a(s)</p><p>

For Simple Interest

</p><p>a(t+s)=a(t)a(s)</p><p>

Force of Interest Accumulation Factor

This is one of the highest-yield FM topics because it ties together accumulation functions, interest rates, discount rates, and calculus.

Here's the version I'd put in a cheat sheet.

Force of Interest ((\delta))What does Force of Interest represent?

The force of interest is the instantaneous rate of growth of an investment.

Think of it as:

"If I zoom in to an infinitely small moment in time, how fast is the account growing right now?"

For compound interest:

<br>δ=ln(1+i)<br>

For example, if

<br>i=8

then

<br>δ=ln(1.08)=0.07696<br>

Notice:

\delta<i

Definition of Force of Interest

Given an accumulation function (a(t)),

<br><br>δt=a(t)a′(t)<br><br>

Interpretation:

Numerator = rate of change

Denominator = current balance

So force of interest is:

<br>current balancegrowth per year<br>

The Most Important Formula

Starting with

<br>δt=a(t)a′(t)<br>

we get

<br>a′(t)=δta(t)<br>

Integrating:

<br><br>a(t)=e∫0tδs,ds<br><br>

This is the master formula.

Whenever FM gives a force of interest, your first thought should be:

Integrate (\delta), then exponentiate.

Constant Force of Interest

If

<br>δt=δ<br>

is constant:

<br>a(t)=eδt<br>

This is the continuous-compounding formula.

Relationship Between (i), (d), and (\delta)

Given force:

<br>i=eδ−1<br>

<br>d=1−e−δ<br>

Given effective interest:

<br>δ=ln(1+i)<br>

Given effective discount:

<br>δ=−ln(1−d)<br>

Quick Conversion Triangle

Starting with (i):

<br>d=1+ii<br>

<br>δ=ln(1+i)<br>

Starting with (d):

<br>i=1−dd<br>

<br>δ=−ln(1−d)<br>

Starting with (\delta):

<br>i=eδ−1<br>

<br>d=1−e−δ<br>

Discount Function

If

<br>a(t)=e∫0tδsds<br>

then

<br>v(t)=a(t)1<br>

Therefore

<br><br>v(t)=e−∫0tδsds<br><br>

For constant force:

<br>v(t)=e−δt<br>

Effective Interest Rate During Year (n)

If force varies with time:

<br>in=<br><a(n)−a(n−1)br>a(n−1)<br>

Using force:

<br><br>in=<br>e∫n−1nδtdt−1<br><br>

This shortcut appears often on FM.

Effective Discount Rate During Year (n)

<br>dn=<br><a(n)−a(n−1)br>a(n)<br>

Using force:

<br><br>dn=<br>1−e−∫n−1nδtdt<br><br>

Simple Interest and Force

Simple interest:

<br>a(t)=1+it<br>

Differentiate:

<br>a′(t)=i<br>

Thus

<br>δt=<br>1+iti<br>

Key Understanding

Simple interest does NOT have a constant force.

Instead:

<br><br>δt=<br>1+iti<br><br>

which decreases over time.

Example:

<br>i=8

At (t=0):

<br>δ0=0.08<br>

At (t=5):

<br>δ5=<br>1.40.08</p><p>0.0571<br>

Force gets smaller as time passes.

Compound Interest and Force

Compound interest:

<br>a(t)=(1+i)t<br>

Differentiate:

<br>a′(t)=<br>(1+i)tln(1+i)<br>

Thus

<br>δt=<br>ln(1+i)<br>

which is constant.

Therefore:

<br><br>δ=ln(1+i)<br><br>

Deriving (a(t)) from Force Quickly

When given (\delta_t):

Step 1

Integrate

<br>∫0tδsds<br>

Step 2

Exponentiate

<br>a(t)=e∫0tδsds<br>

Step 3

Simplify

Example:

<br>δt=10+t2<br>

Integrate:

<br>∫0t10+s2ds</p><p>2ln(1010+t)<br>

Exponentiate:

<br>a(t)</p><p>e2ln((10+t)/10)<br>

<br><br>a(t)=(1010+t)2<br><br>

FM Shortcut for Finding (a(t))

When you see

<br>δt=<br>a+btk<br>

immediately think

<br>∫a+btkdt</p><p>bkln(a+bt)<br>

and therefore

<br>a(t)</p><p>(aa+bt)k/b<br>

This pattern appears repeatedly on FM.

Three Facts to MemorizeConstant force

<br>a(t)=eδt<br>

Simple interest

<br>δt=1+iti<br>

Compound interest

<br>δ=ln(1+i)<br>

If you know those three formulas plus

<br>a(t)=e∫0tδsds,<br>

you can solve essentially every FM force-of-interest problem.

Annuity-Immediate

Payments of 1 at the end of each period for n periods, with PV=an∣=(1−vn)/i.

Annuity-Due

Payments at the beginning of each period, where a¨n∣=(1+i)an∣.

Deferred Annuity (k∣an∣)

An annuity valued at time k and then discounted back k periods using vk⋅an∣.

Perpetuity

Immediate: An annuity with payments continuing forever, with a present value of 1/i.

Due: An annuity with payments continuing forever starting at time 0, with a present value of 1/d.

Geometric: A perpetuity where payments grow by rate g each period, valid if g < i, with a value of 1/(i−g).

Increasing Arithmetic

Decreasing Arithmetic

Increasing Annuity-Immediate (Ian∣)

An annuity with payments of 1,2,3,…,n ; valued as Ia=(a¨n∣−nvn)/i.

Decreasing Annuity-Immediate (Dan∣)

An annuity with payments of n,n−1,…,1; valued as (n−an∣)/i.

Arithmetic Identity

(Ia)n∣+(Da)n∣=(n+1)an∣

Continuous Level Annuity

The present value (PV) of receiving $1 per year continuously for n years is defined as:

an∣=lim_m→∞a_n∥(m)=δ1−vn =δi⋅i1−vn=δia_n∥.

The accumulated value (AV) for the same annuity is described as:

s_n∥=a_n∥(1+i)n =δ1(a_n∥(1+i)n)=s_n∥.

Varying Continuous Annuity

The present value (PV) of a continuous annuity with varying payment rate f(t) and force of interest δt is defined as:

PV=∫0nf(t)exp(−∫0tδsds)dt.

The accumulated value (AV) is given by:

AV=∫0nf(t)exp(∫tnδsds)dt.

If f(t)=t for a continuous increasing annuity:

(Ia)n∣=∫0ntvtdt=δan∣−nvn.

(Is)n∣=∫0nt(1+i)n−tdt=(Ia)n∣(1+i)n.

(Ia)∞=δ21.

For a continuous decreasing annuity where f(t)=n−t:

(Da)n∣=∫0n(n−t)vtdt=δn−an∣.

(Ds)n∣=∫0n(n−t)(1+i)n−tdt=(Da)n∣(1+i)n

Prospective Outstanding Balance (OBk)

The present value of remaining payments: PMT⋅an−k∣.

Retrospective Outstanding Balance (OBk)

The accumulated value of the loan minus the accumulated value of payments: L(1+i)k−PMT⋅sk∣.

Sinking Fund Method

A loan repayment method where the borrower pays interest to the lender and separately accumulates a fund at rate j to repay the principal in one lump sum.

IRR (Internal Rate of Return)

The interest rate r∗ that sets the Net Present Value (NPV) of a cash flow stream to zero.

Dollar-Weighted Rate of Return (DWRR)

The rate of return equivalent to the IRR on a fund, which is affected by the timing and size of external cash flows.

Time-Weighted Rate of Return (TWRR)

A measure of a fund manager's performance that eliminates the effect of external cash flows by chain-linking sub-period returns.

Par Bond

A bond where the coupon rate r equals the yield rate i, resulting in the Price P equaling the Redemption Value C.

Premium Bond

A bond where the coupon rate r is greater than the yield rate i (r>i), resulting in a Price P>C.

Discount Bond

A bond where the coupon rate r is less than the yield rate i (r<i), resulting in a Price P<C.

Premium/Discount Formula

P=C+(Fr−Ci)an∣

Makeham Formula

P=K+ig(C−K), where K=Cvn and g=Fr/C.

Callable Bond Pricing

The process of pricing a bond at every possible call date and selecting the minimum price to account for the worst-case yield.

Spot Rate (st)

The effective annual rate for an investment made from time 0 to time t.

Forward Rate (ft,m)

The rate agreed upon today for lending that occurs from time t to time t+m.

No-Arbitrage Relationship

(1+st+m)t+m=(1+st)t⋅(1+ft,m)m

Macaulay Duration (D_Mac)

Macaulay Duration (MacD) is a measure of the average time until cash flows from a financial asset are received, weighted by the present value of those cash flows. Mathematically, it is defined as:

MacD=P∑tA_t=−P_δdδdP_δ

where:

P = price of the asset

A_t = present value of the cash flow at time t

Interpretation:

MacD represents the average time at which cash flows occur, considering their present value.

If there is only one cash flow, then: MacD=time until that cash flow occurs

A bond with higher coupon payments tends to have a shorter MacD.

A bond with a higher yield also tends to have a shorter MacD.

Par Bond Shortcut: If a bond is priced at par, MacD can be approximated as:

MacD=a¨_n∥(m)−m1a_n∥mj

where:

j=mi(m) is the effective interest rate per period.

m = number of coupon payments per year.

Important Note:

The par value of the bond does not influence MacD.

If not specified, it is common to use a par value of 100.

Duration of a Portfolio: The MacD for a portfolio of multiple assets is defined as:

MacD_P=P_1+P_2+⋯+P_nP_1MacD_1+P_2MacD_2+⋯+P_nMacD_n

where:

P_i = market price of asset i

MacD_i = MacD of asset i

Approximation Using Macaulay Duration: The future price of a bond can be approximated as:

P_i_1≈P_i_0(1+n_11+n_0)MacD

where:

P_i_0 = price at the original effective annual yield i_0

P_i_1 = price at the new effective annual yield i_1

Notes:

It is crucial to express interest rates as effective annual rates since MacD is measured in years.

Using MacD provides a better price approximation compared to Modified Duration when cash flows are positive.

FM Memory Box: Macaulay Duration = weighted average time of cash flows

To remember this concept, think of: MacD=PriceTime-Weighted PV of Cash Flows

Quick Facts:

Higher coupon rate ⟹ Lower Duration

Higher yield ⟹ Lower Duration

Zero-coupon bond ⟹ MacD = maturity

Portfolio duration = weighted average of component durations

The par bond shortcut is a key concept in financial mathematics

MacD is measured in years

Modified Duration (DMod)

Modified Duration (ModD) quantifies a bond's price sensitivity to changes in yield. It is mathematically defined by:

ModD=−P1didP

where:

P = price of the bond,

dP = change in price due to yield change,

di = change in yield.

Interpretation: This formula allows us to approximate the percentage change in price for small changes in yield:

PΔP≈−ModD⋅Δi

A larger ModD indicates greater sensitivity to interest rate fluctuations.

ModD serves as the slope of the price-yield curve, illustrating the inverse relationship between interest rates and bond prices.

Relationship Between Modified Duration and Macaulay Duration:

The relationship can be expressed as:

ModD=v⋅MacD=1+iMacD

where:

v=1+i1 is the present value factor.

Equivalently, Macaulay Duration (MacD) can be expressed as:

MacD=(1+i)ModD

Macaulay Duration (MacD):

Macaulay Duration is defined as:

MacD=P∑tAt=−PδdδdPδ

Interpretation:

MacD represents the weighted average time until cash flows are received, measured in years.

For a single cash flow, it simplifies to:

MacD=time until that cash flow occurs

For zero-coupon bonds:

MacD=maturity

Higher coupon bonds generally exhibit shorter MacD values, as do bonds with higher yields.

Approximating Bond Prices Using MacD:

To approximate bond prices when yields are expressed as effective annual rates:

Pi1≈Pi0(1+i11+i0)MacD

where:

Pi0 = price at yield i0

Pi1 = price at yield i1.

When to Use ModD:

Utilize ModD when you need:

An approximate percentage change in price due to small yield changes,

To assess the sensitivity of the bond price to interest rate changes,

An answer to questions regarding price sensitivity:

PΔP or "How sensitive is price to yield?"

When to Use MacD:

Opt for MacD when:

You are analyzing the average timing of cash flows,

Engaging in duration matching or immunization strategies,

Approximating bond prices with:

Pi1≈Pi0(1+i11+i0)MacD,

Considering interest rates expressed as effective annual yields.

FM Memory Box:

MacD=Weighted Average Time

$$ Mod

Convexity (C)

A measure of the curvature of the price-yield curve, calculated as C=P1dt2d2P=P1∑(1+i)tt(t+m1)vt+2⋅CFt=P1∑(1+i)tt(t+m1)v2⋅PV(CFt).

Convexity (C) measures the sensitivity of the duration of a bond to changes in interest rate, indicating how the price of a bond changes as interest rates fluctuate (second derivative of Price formula).

Where:

C = Convexity

P = Price of the bond

t = Time period

CFt = Cash flow at time t

i = Yield to maturity

v = Present value factor, calculated as v=1+i1.

Redington Immunization

A strategy to protect against small parallel yield shifts by matching PV of assets and liabilities, matching durations, and ensuring Asset Convexity > Liability Convexity.

Full Immunization

A strategy that protects against any single yield shift by requiring asset cash flows to bracket liability cash flows (one before, one after).

Portfolio Yield Method

A method where new investments earn the same rate as the existing portfolio average.

New Money Method

Also known as the investment year method; new investments earn a rate based on current market conditions, tracked separately by cohort.

Zero-Coupon Bond Cheat Sheet

Definition: A zero-coupon bond pays:

✅ No coupons

✅ One payment at maturity

Key Formulas:

Price: P=Cvn

Duration: D=n

Yield: i=PC1/n−1

Book Value: BVt=Cv−(n−t)

Properties:

Highest duration for a given maturity.

Most price sensitive to interest rate changes.

No reinvestment risk.

Highest convexity.

Ideal for immunization strategies.

FM Exam Clues: Remember these facts for zero-coupon bonds:

One payment only

Duration = Maturity

Highest duration

Highest interest-rate sensitivity.

Interest Rate Behavior

Connection with Bond Prices:

When interest rates fall, bond prices increase.

Long-term bonds are more sensitive to interest rate changes than short-term bonds because they have a higher duration.

Low-interest-rate bonds benefit more in percentage terms when rates drop.

In a falling rate environment, the bond that offers the most price sensitivity maximizes profit opportunity.

Common Linh’s mistake

Duration:

First payment at time 0 as will be multiplied by 0!

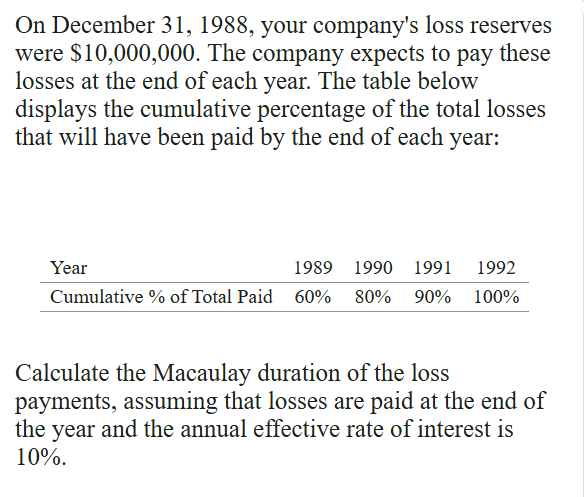

whenever you see a cumulative loss payment pattern, immediately convert it to incremental payments by taking differences between consecutive cumulative percentage

Special Case: Simple Interest

Accumulation Function: a(t)=1+it. The interest earned during any year is given by In=i and the effective interest rate during year n is in=1+i(n−1)i. Effective discount rate during year n is dn=1+ini.

Special Case: Compound Interest

Accumulation Function: a(t)=(1+i)t. The interest earned during year n is given by In=i(1+i)n−1, and the effective interest rate during every year is in=i. The effective discount rate during every year is dn=d=1+ii.